Since 2021, the new “three red lines” financing regulations have been superimposed on the “two red lines” housing loan concentration management policy, and both ends of the financing supply and demand of housing companies have been restricted, and the financing environment for housing companies can be described as tightening across the board.

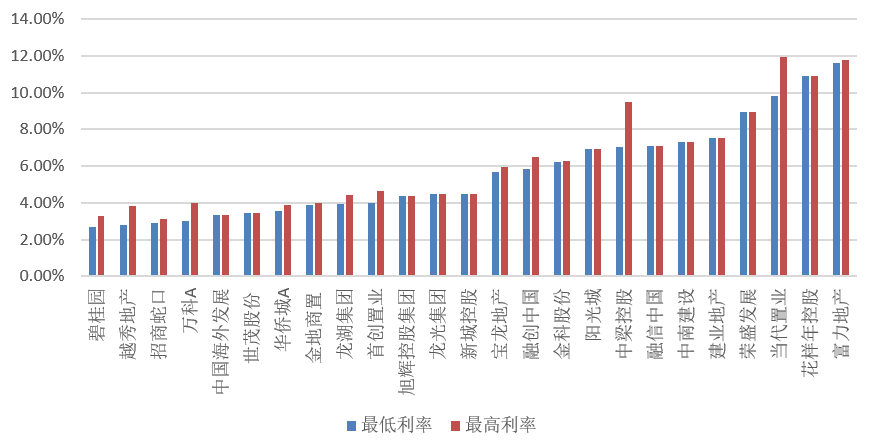

On April 13, the “Top 40 Typical Housing Companies Financing Interest Rate List in the First Quarter” published by the Tongce Research Institute showed that the total financing of 40 typical housing companies in the first quarter was 1917.793 billion yuan, a sharp drop of 19% year-on-year in the first quarter of 2020. Under the background of the country’s continued implementation of the real estate industry to reduce leverage and the continued strict regulation of real estate bond financing, only 25 of the 40 typical real estate companies announced in the first quarter The specific financing interest rate is disclosed in China, and financing costs range from 2.7% to 11.95%.

Image source: Tongce Research Institute

According to the data released by Tongce Research Institute, there are not many real estate companies with a large financing range, that is, the lowest interest rate and the highest interest rate are arranged in almost the same distribution.

Specifically, among the 25 real estate companies that issued financing announcements in the first quarter, Country Garden, Yuexiu Real Estate, China Merchants Shekou, Vanke A, and China Overseas Low, ranking in the top five among 25 real estate companies, among which Country Garden’s lowest financing interest rate is 2.7%; CCRE, Rongsheng Development, Modern Land, Fantasia Holdings, and R&F Properties have higher comprehensive financing costs, ranking the bottom five Among them, the highest financing interest rate of R&F Properties is 11.75%.

From the perspective of 25 real estate companies’ financing interest rate details, 49 financing interest rates were publicly disclosed in the first quarter, of which a total of 26 financing interest rates were below 5%; A total of 11 transactions with an interest rate between 5% and 7%; a total of 8 transactions with a financing interest rate between 7% and 10%; and a total of 4 transactions with a financing interest rate of more than 10%.

Combined with the latest three red lines, almost all real estate companies with low financing costs are in the green or yellow stage, and almost all real estate companies with high financing costs are in the green or yellow tier. Red file or orange file.

Image source: Tongce Research Institute

The “three red lines” refer to the regulatory authorities’ capital monitoring and financing management rules for key real estate companies in August last year, according to the four levels of “red, orange, yellow, and green” management, and the “three red lines” are set accordingly: removed The debt-to-asset ratio after advance collection is greater than 70%; the net debt ratio is greater than 100%; the cash short-term debt ratio is less than 1 time.

According to regulations, if all three red lines are touched, the interest-bearing liabilities of real estate companies cannot increase; if two are touched, the annual growth rate of the scale of interest-bearing liabilities shall not exceed 5 %; if one item is touched, the growth rate shall not exceed 10%; if it is not touched, it shall not exceed 15%.

Combined with data from the Tongce Research Institute, among the real estate companies with higher financing costs monitored by it, such as China Evergrande and R&F Properties, they are in the red category, and they are all Three red lines; Modern Land is the yellow file, stepping on two lines.

The Tongce Research Institute report pointed out that these real estate companies have been implementing more aggressive financing strategies, and their own debt ratios are already very high. Taking R&F Properties as an example, the debt-to-asset ratio of R&F Properties after excluding advance receipts is 76.66%, the short-term debt ratio is only 0.4, and the net debt ratio is as high as 145.71%. Almost all are above 10%. However, from historical data, the weighted financing cost of R&F Properties in 2010 was only 5.3%. In the past few years, R&F Properties has repeatedly faced difficulties such as huge debts, debt crisis, and decline in sales revenue. In addition to scale and growth rate, R&F’s debt and capital status have long been the focus of the industry’s attention. According to the financial report, in order to “reducing debt and deleveraging”, R&F will also launch actions in 2020, including speeding up sales collection, achieving full circulation of H shares, and selling assets. The results have been remarkable. In 2019, the net debt ratio of R&F Properties reached 198.9%. At the end of 2020, the net debt ratio fell to 145.71%, a sharp drop of 53.2 percentage points, which is good for R&F’s financing costs in the future.

From the perspective of financing channels for real estate companies, overseas financing costs are relatively high, and domestic financing costs have fallen. Taking corporate bonds as an example, the financing cost of overseas bond issuance is higher than that of domestic bond issuance. In terms of specific financing events, Modern Land issued a US$77 million senior note in January with an interest rate of 11.95%, which was the highest financing rate during the monitored financing period. In addition, R&F Properties issued two senior notes totaling US$825 million in January and February, with interest rates higher than 11%; and the lowest financing cost was Country Garden’s US$500 million senior notes issued in January, both with interest rates as low as 2.7 %.

Overall, the cost of financing US dollar debt will decline in the first quarter of 2021, Other innovative financing channels such as debt financing and medium-term notes have relatively low financing costs, and financing interest rates are mostly below 5%.