Tencent’s philosophy of survival: low-key and self-aware.

This article was published in the Tiger Securities Community.

[Introduction]

Getting Tencent’s Q1 earnings report, lamenting that the stock price is too high and not getting on the car, investors who are sour in their hearts will focus on revenue and growth. The rate of 25% may be more sour; investors who are already on board are the first Seeing the net profit, the high year-on-year growth made them happy. Tencent’s Q1 earnings report, which has a huge amount of information, is not that simple.

Since March, Tencent’s share price in the secondary market has almost been “sealed”. Investors worry about uncertainty, which is not unreasonable, so waiting for an earnings report may be the only thing that can be done.

It happens that the amount of information in this financial report of Tencent is quite large.

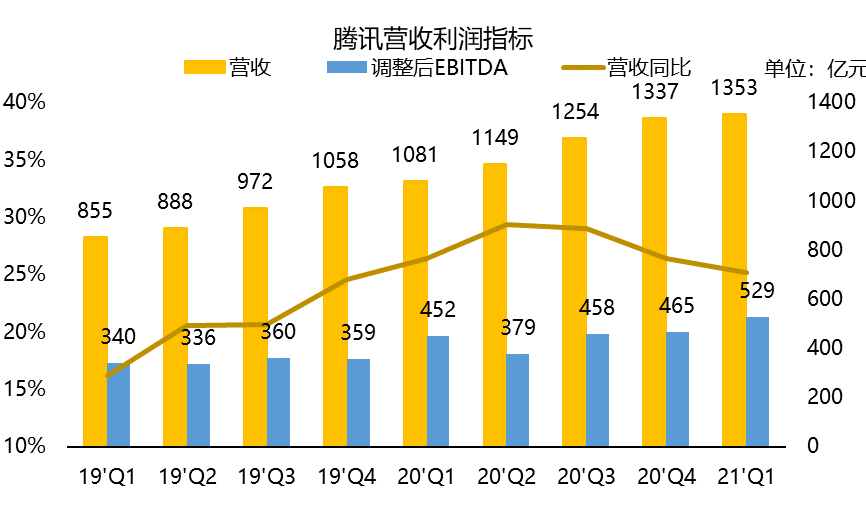

In general, there are three core basic indicators: 1. The total revenue of a single quarter was 135.3 billion yuan, an increase of 25% year-on-year; 2. The profit for the period was 49 billion yuan, an increase of 67% year-on-year; 3. Adjusted EBITDA It was 52.9 billion yuan, a year-on-year increase of 17%.

(Drawing: Tiger Securities)

I sigh that the stock price is too high to get into the car, and investors who are a little bit sour in their hearts will focus on the ceiling revenue and whether the growth rate can break through the impact of the epidemic is a very critical point. Obviously, the 25% year-on-year growth rate has made almost all non-monopoly and non-resource-based companies ashamed.

Investors who are already on board will look at the net profit at first glance. The high year-on-year growth also reflects their outstanding investment ability, similar to the book profit brought by events such as the Kuaishou listing.

But what should really be used to analyze its true profit should be its adjusted EBITDA, in short, it is the true operating profit that is closer to the cash perspective. This value increased by 17% year-on-year, which is actually lower than the revenue growth rate. The main reason is the decline in gross profit margin.

With rising expenses and rising costs, has Tencent’s profits really fallen?

Not really.

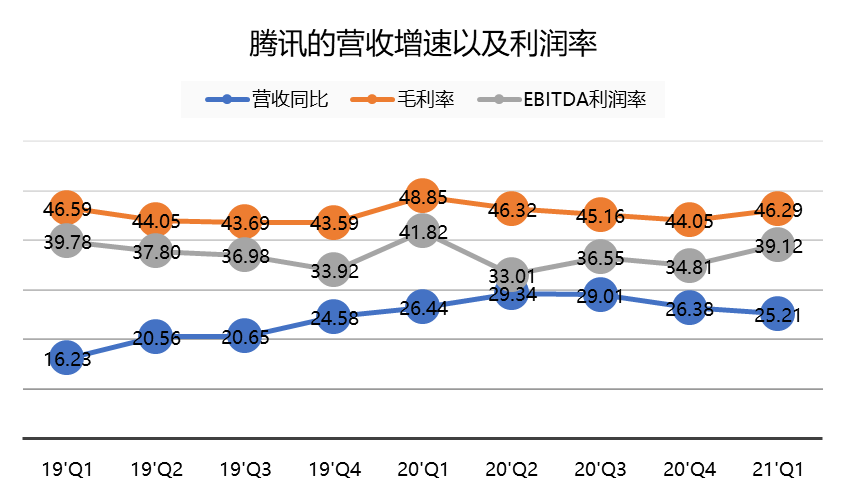

Q1 of 2020 is a relatively special season. Due to the epidemic, game businesses with higher profit margins have grown faster and accounted for a higher proportion of overall revenue, thus greatly boosting the company’s profit margins. (Gross profit and net profit). From the perspective of fairness, the business environment closer to Q1 in 21 years is Q4 in 20 years.

Mapping: Tiger Securities

From a month-on-month comparison, the gross profit margin has increased by 2 points instead. Of course, this also has certain seasonal factors, after all, winter and summer vacations are often the peak of the game industry.

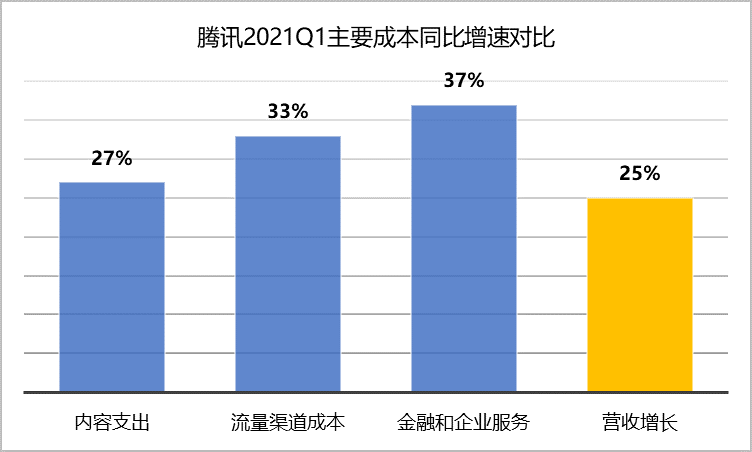

In terms of operating expenses, with the exception of the 34% year-on-year increase in administrative expenses that exceeded revenue growth, other marketing expenses and financial expenses are in a state of contraction. The reason for the increase in Tencent’s administrative expenses is that all non-goose factory employees are jealous-the sun shines on the year-end bonus of 100 shares per person.

The main reason for the pressure on profit margins is the content expenditure on video and live broadcast (Tencent members, Huya, and Weishi three golden beasts), on the one hand, the traffic acquisition cost of video ads (20Q1 low base , And 20Q4 merged with Bitcar report).

Of course, the more important reason is the cost of financial and corporate services, including cloud service projects, 38% of corporate service costs VS 25% of revenue. Tencent expanded its PaaS and SaaS business scale in 21Q1, which also reflects that Tencent’s cloud computing costs are still very large. Considering that Alibaba Cloud has already made two consecutive quarters of cloud computing business earnings (EBITDA), Tencent’s competitive pressure in the cloud is very high, and competition has shifted from the government and large enterprises to full-market enterprises, so the future expenditure in this area will still be obvious. .

(Drawing: Tiger Securities)

If profit margins are under pressure due to cloud business expenses, presumably most investors are still very happy to accept it.

“Creation Camp” pushes back “Youth with You” with quality, Tencent Video’s membership growth crushes iQiyi

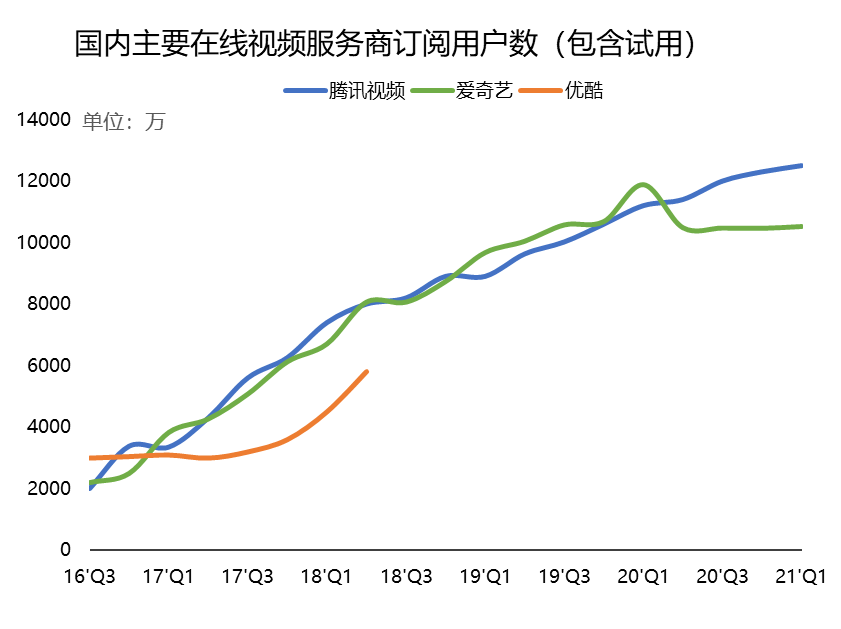

Among Tencent’s various business lines, the most eye-catching one this quarter was Tencent Video, which did not even list revenue separately.

21Q1 Tencent Video’s expenditure on content is not at all ambiguous. What is the result of the content?

The number of subscription members of Tencent Video increased by 12% year-on-year to 125 million. You know, Q1 in 2020 is already veryThe base number is high, and iQiyi next door also specifically explained this point. It carefully announced a year-on-year growth rate of 0.9%, but the result is still insignificant.

The growth rate of Tencent Video’s membership has diverged from that of iQiyi. It is impossible to say that it is because of the introduction of animation or movie IP, because it is more and more difficult to exclusively broadcast, and the homogeneity of content is also Beginning of involution. The most important way for major domestic video content manufacturers to increase the number of members is through original variety shows. Mango tv has risen from this point.

In this season, Tencent Video, in addition to “Tucao Conference”, which is popular for “criticism”, also has “Creation Camp 2021”, which has a high reputation in internal entertainment. In contrast to the embarrassment of iQiyi’s “Youth with You 3” main coffee retiring and the program suspension, “Creation Camp” can be said to win by quality, and the impact of the “milk pouring incident” is not even reflected in the Q1 financial report.

In addition, there is a very small “other” in Tencent’s segment revenue, including investing in these originals and co-producing and distributing content with three parties. Although the proportion of this part is not high, but the growth rate exceeds the overall revenue, it also reflects the popularity of these original programs from the side.

Although this does not mean that Tencent’s programs will be successful in the future, Tencent did make good use of this opportunity to overtake its opponents and distance themselves.

Anti-monopoly guillotine is not inevitable, Tencent-style survival philosophy is worth learning from

Compared with Alibaba being punished and iQiyi being criticized by name, Tencent seems lucky that it has not been involved in any key hot spots. This is exactly Tencent’s philosophy of survival-low-key and self-aware.

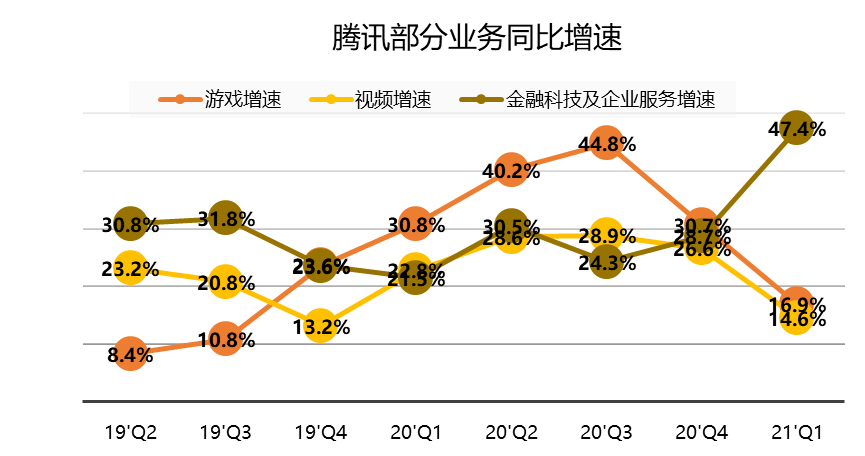

For example, in the game business, the year-on-year growth rate in 21Q1 dropped to 17%, which was the lowest point since the version number was restored. Everyone also knows that 20Q1 has a high base and it is difficult to reproduce “Glory of the King” with new games. But this is not a bad thing for Tencent. Its own channel advantages have always existed. Participating in industry competition and diversifying the industry will reduce the risk of monopoly.

Furthermore, investors may not expect too much of Tencent’s game business to achieve greater brilliance, level the industry, form a dynamic balance, and add a little humanistic care, and everyone will be happy. Anyone who aggressively engages in another “pesticide” may be eye-catchingly. Other businesses, especially finance, cloud computing, and enterprise services, are also full of imagination.

And Tencent can not be successful in any business, such as the short video micro-vision, the entire team has been merged into Tencent Video, which also reflects that its development is not as expected. But Tencent also has fast hands. It is better to be a financial investor and enjoy the growth of the industry than to compete by yourself.

In addition, Tencent, which has a strong desire for survival, also mentioned “investing in the future” in this financial report for the first time. In addition to SaaS and video content related to its own business, it also includes the previously announced 50 billion “future investment”. They are in the fields of science, education, rural areas, and elderly care.

It’s the same principle. Teachers punish students, never aim at punishment itself, but more importantly, regulate order and prevent bigger problems.

What’s more, Tencent is still the obedient kid with self-knowledge.

This article was published in the Tiger Securities Community, which is a community section of Tiger Trade’s stock trading software Tiger Trade, dedicated to creating a “community for US stocks, Hong Kong stocks and British stocks closer to trading”, a warm stock exchange community.

This article does not constitute and should not be regarded as any agreement, offer, invitation to offer, opinion or suggestion for the purchase of securities or other financial products. Nothing in this article constitutes Tiger Securities’ opinions on investment, legal, accounting or taxation, nor does it constitute a statement on whether a certain investment or strategy is suitable for your personal circumstances, or any other personal recommendation for you.