Beer has entered the era of a glass of ocean

Editor’s note: This article is from the WeChat public account “TideSight” (ID: TideSight), author: Wang Tonton, editor: Perilla.

From the high spirited to the hard to return, 30 years later, the industry has been waiting for the “pickles”, and there is no last one that can be beaten.

“Wang Yibo no longer endorses Yanjing Beer.”

On May 10th this year, Yanjing Beer officially announced its brand-new brand spokesperson Cai Xukun in the wailing voices of the “Sisters of Motorcycles”. The official announcement of the two partners immediately appeared on the Weibo Hot Topic List as soon as they were released. Third place.

It took only one year from Wang Yibo to Cai Xukun. The time period for Yanjing Beer to change its spokesperson has been continuously shortening. It is not difficult to see the urgency of its transformation to younger, fashionable and individualized.

The same sense of urgency also appears in many leading beer companies such as Tsingtao Brewery, Chongqing Brewery, and China Resources Brewery. Marketing methods such as signing top-tier, IP co-branding, and popular variety shows have emerged in endlessly, and the effect seems to be immediate. The 2021 Q1 financial report shows that the revenue and net profit of the 7 domestic beer companies have achieved double-digit double-digit growth.

However, even though the share price of domestic beer can still swell periodically during the peak consumption season of each summer, it is a pity that the adolescence when beer is held in the palm of ordinary consumers has long passed.

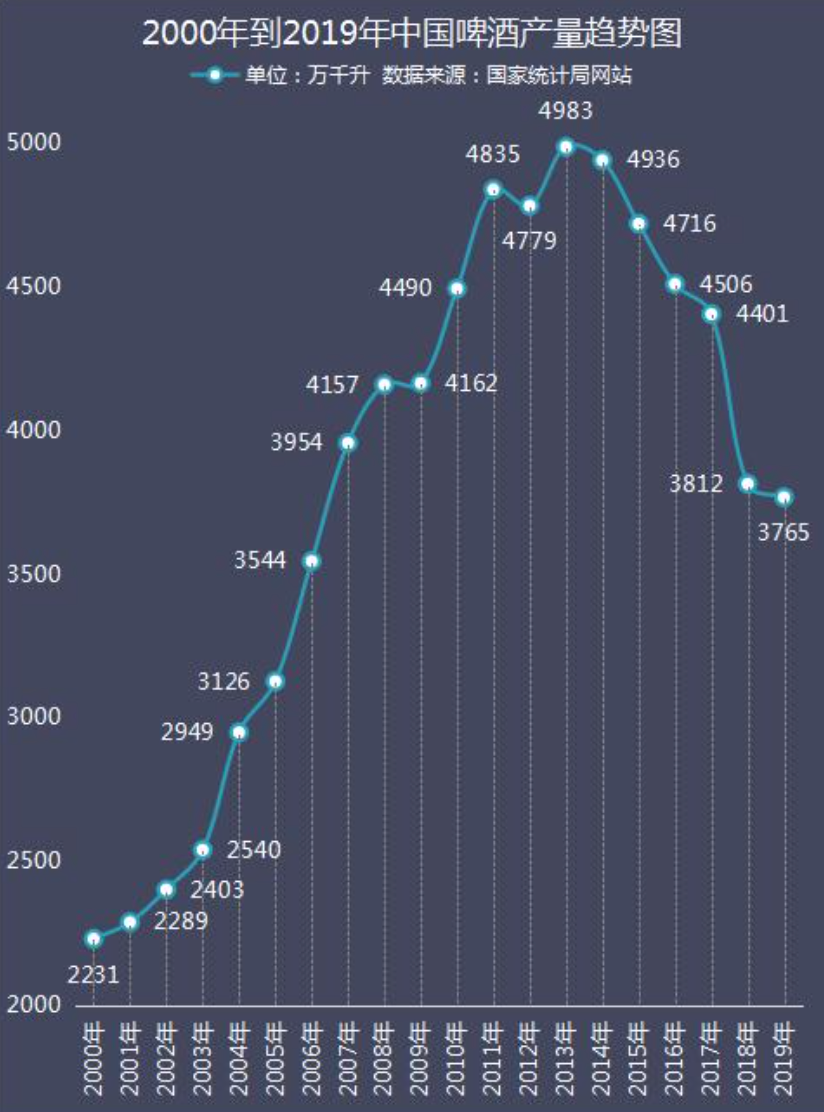

Data shows that the national beer output in 2020 is 34.11 million tons, a year-on-year decrease of 7.04%. This is the seventh consecutive year of decline in domestic beer production since 2013. In terms of specific companies, compared with Moutai’s early cut of 2.5 trillion market value, the beer leader Tsingtao Brewery’s market value of less than 150 billion is pitiful.

What’s even more heartbreaking is that as of press time, the total market value of the seven listed A-share beer companies is only 280.8 billion yuan, which is not even comparable to Yanghe shares, which is currently ranked fifth among listed liquor companies.

From high spirits to hard to come back, 30 years later, the industry has been waiting for the “beer”, the last one can be beaten.

01 Prosperity ends

An industry consensus is that the “golden age” belonging to beer has long passed, even if the commercialization process of beer is not long.

Compared with the craftsmanship origin of rice wine and white wine for thousands of years, beer, a pure foreign product, did not enter China until 1900, when the Qing Dynasty was about to fall. And like most local consumer products, the commercialization process of the domestic beer industry is only after the “reform breeze blows all over the ground” before making flowers all over the world.

In 1985, a “Beer Special Project” led by the central government to introduce assembly lines and jointly funded by local and commercial banks was announced. In just a few years, there were as many as 813 local beer brands. “, “One county, one beer” grand occasion has become commonplace.

In 1993, my country’s beer production surpassed Germany for the first time, and it ranked second in the world for eight consecutive years. In the ninth year, with a record of total beer production of 23.868 million tons, my country squeezed out the United States and jumped to the top of the world, becoming a veritable beer country.

Everything in the world will merge for a long time. When the cake is big enough and there are enough players, the capital story of big fish eating small fish will come as promised. Especially for beer, which requires high fresh-keeping requirements and high unit transportation costs, and can only be produced on-site in order to expand its sales radius, the battle for mergers and acquisitions is more urgent than other consumer products.

The most typical is China Resources.

In 1994, China Resources Group acquired Snow Brewery from the Shenyang government, and trained a team of dealers with strong combat effectiveness on the borders of the declining “eldest son of the Republic” in the northeast. Soon, this iron army helped Snow Beer lay the market in Shenyang, and backed by the huge resources of China Resources Group to “advance in two lines” along the coast and along the river.

In the process of conquering cities from north to south, China Resources grabbed not only the consumer market but also the local breweries. This national merger strategy is called the “mushroom strategy”-each acquisition of a company is equivalent to planting a mushroom, thereby delineating the sphere of influence, increasing market share and pricing power.

Like China Resources, Tsingtao Brewery, Budweiser Asia Pacific, Yanjing Beer, Carlsberg and other Chinese and foreign breweries are also the “main battle parties” in this process. After years of strategic battles, domestic beer has basically ended the “separation of powers” situation after large-scale foreign capital inflows into domestic and foreign mergers and acquisitions, expansion and integration, and has formed an overall stable and highly concentrated “5 strong competition for hegemony” market pattern.

Data shows that the CR5 of the beer industry today is about 92%. The sales market share in 2020, from high to low, will be 31.9% of China Resources Beer, 22.9% of Tsingtao Brewery, 19.5% of Budweiser InBev, and 10.5% of Yanjing Beer.3% and Carlsberg’s 7.4%.

The fresh clothes and angry horses of large wine companies are at the cost of the decline of countless small and medium wine companies. Compared with the misfortune of the defeated general, the era of shrinkage that the beer industry inevitably sinks after reaching the peak of production capacity is a more tragic industry tragedy.

Data shows that from 1980 to 2013, China’s beer production continued to grow, with a compound annual growth rate of about 13%, and the highest year-on-year growth rate exceeded 40%. In 2013, the total domestic beer production peaked after reaching a historical peak of 50.62 million tons. As mentioned earlier, today’s domestic beer production has been reduced by 1/3 compared to the peak in 2013.

Beer production capacity is shrinking, and the increase is stretched. The past practice of staking the market and sales is out of date; in the era of inventory gaming, price wars have become the mainstream tactics of beer companies.

But the side effect of the low price share is that the price per ton of beer companies in my country is very low. Taking the data of 2019 as an example, the average price per ton of major beer listed companies in my country’s A-share market is 3144 yuan, which is only 48.95% of AB InBev, a leading European and American company, and 64.88% in the Asia-Pacific region of AB InBev.

In addition, the running volume model under the low-price model also directly affects the company’s overall profit level.

Data shows that in the first half of 2020, the average gross profit margin of 10 beer listed companies was 31.49%, a decrease of 0.67 percentage points from the same period last year. Correspondingly, the gross profit margin of foreign wine companies represented by AB InBev has been maintained at a high level of more than 50%.

This beer company is still struggling in the whirlpool of low prices. The “Eight Regulations” of the central government, the “Prohibition” and trade protection in some regions, and the increase in raw material prices in trade frictions followed one after another. .

Several sets of combined punches have made the frontal battlefield of the beer industry more anxious.

02 Winery self-help

The industry is warm and cold, no one is in itPeople are more self-aware of the words. In fact, the road to self-rescue for traditional beer companies has already begun.

The first one to be adopted was the passive ability to reduce production.

In 2014, after beer production capacity peaked, Chongqing Beer took the lead in starting the process of capacity optimization. The specific measures were to shut down and transfer to low-efficiency factories, and to reduce the overall sales and management expense ratio.

However, in 2015, Chongqing Beer had an annual loss of 66 million yuan, a drop of 189%, which was an “exceeding-expected return”. This was also the company’s first year of loss since its listing in 1997.

The effect of throttling is limited, and beer companies have not thought about taking the initiative to increase revenue. The most significant is the transition to a high-end product line.

Tsingtao Brewery has successively launched high-end product lines such as August, Fortune Dangtou, Classic 1903, and pure draft beer. At the same time, it has continuously replaced packaging, upgraded quality, and launched a century-old series of products.

China Resources Beer has gradually formed four core mid-to-high-end products through the direct acquisition of Heineken China through the direct acquisition of Heineken China, the new Facebook, SuperX, Ingenuity, and Mars Green.

Chongqing Beer chose to reorganize its assets with Carlsberg to accelerate its high-end brand strategy. Financial data shows that Chongqing Beer’s high-end product line has contributed more than 20% of the company’s main business revenue in recent years, an increase of more than 50% year-on-year, in sharp contrast with the negative growth of mainstream and mass products.

It’s just that after years of intensive cultivation, China’s high-end beer still remains at the conceptual level of “huge potential for value-added”.

Data shows that in 2018, the sales volume of high-end beer in the United States has reached 42.1%, while China’s share is only 16.4%. Budweiser, Carlsberg, and other foreign brands that have always demonstrated high-end beer, have a rich product matrix and a healthier structure, still have a clear first-mover advantage and have so far accounted for half of the high-end beer sales.

The industry is declining, and the optimization of production capacity is tantamount to surviving with a broken arm; foreign capital is preemptive, and high-end iteration is not a one-day effort. However, under many symptoms, the changes in the consumer market may be the crux of the deeper development of beer companies.

The research report shows that from 2010 to 2019, the proportion of the main people (the population aged 20-49) of beer consumption in my country has dropped by more than 3 percentage points, and the total population has also fallen by more than 40 million. Calculated on the basis of my country’s annual per capita consumption of 30 liters of beer, this is equivalent to a reduction of 1.2 billion liters of potential beer consumption.

In addition to the decline in young people, the decline in the number of young people “beating workers” is also affecting beer sales. Bain Consulting mentioned in a research report that after the number of workers in China peaked in 2012, the number of low-income and retirees has continued to increase.

With the gradual decrease in the number of workers, the sales of “blue-collar consumer products” represented by instant noodles and beer have fallen. In contrast, young people born in 1995 and 00 who migrated to high-end office buildings have gradually become the main consumers, and their unique consumption habits have begun to influence the beer market.

From the perspective of Generation Z, the high-calorie attributes of traditional beer are not conducive to integrating into the consumption space of young people, while the power culture and luxury symbols that come with liquor and red wine make young people instinctively repel it.

With this background, more imaginative and diversified alcoholic beverages began to emerge.

03 Rising Stars

“Drunk” is no longer the pursuit of wine by contemporary young people. In the eyes of these sensitive stars who look as stable as an old dog but have endless hearts and minds, wine represents fashion, trend, and beauty. It is health, culture, and life philosophy.

What kind of alcohol can represent Generation Z? The latest answer is that the alcohol content is between 0.5%-12%, with fruit wine, pre-mixed wine, soda wine, and rice wine as the main categories of low-alcohol wine.

2019-2021 is the explosive period of the low-alcohol circuit, especially since the middle of last year, capital movements have increased.

In May 2020, the low-alcohol wine brand “Likoubai” completed a multi-million dollar seed round of financing led by Zhen Fund; in August, the fruit wine brand “Berry Sweetheart” received tens of millions of investment from Jingwei China Yuan A round of financing.

In November, the fruity low-alcohol wine brand “Lanzhou” received angel round financing from Angel Bay Ventures; in the following December, the low-alcohol wine brand “Zouqi Qingnian” and the tea fruit wine brand “Liuyin” The financing has been completed one after another, and the investors behind are Dexun Investment, XVC and Tiantu Investment.

Entering 2021, the low-alcohol race track continues to be hot. At the beginning of the year, the “Horsepower Ton Ton” brand was launched on the market and received tens of millions of yuan in angel round financing. The investor is the Unilever Alumni Association’s U Family Association Fund.

An era has consumer products of an era. It is no surprise that young consumers who originally belonged to beer fans switched to low-alcohol alcohol.

On the outside, low alcohol is interestingThe design is more in line with the unique aesthetics of Generation Z; in terms of taste, the easy-to-eat sweet and fruity flavor and the low-alcohol that are not easy to top make it easy for low-alcohol wine to expand into the more concentrated and broader beverage market for young people.

In terms of ingredients, the indications of low-alcohol, low-calorie, and low-sugar products are more in line with young people’s pursuit of health; in the scene, the circle and emotional marketing that comes with low-alcohol are more suitable for parties, small gatherings, and solo drinks. Informal social scenes are more in line with the lifestyle of young people.

“I have to drink a glass of sweet wine almost every night to (fall asleep), otherwise I can’t sleep at all.” Jiang Lan (pseudonym), a post-95 girl who has a certain dependence on low-alcohol alcohol, has a new consumption of watching tide ( ID: TideSight) said.

For Jiang Lan, the low-alcohol wine has a sweet and soft taste. It is not easy to pick up and has a certain sleep aid effect. It is most suitable for dispelling the loneliness of working alone in the field.

Although, judging from the current market size, beer ranks in the front row in terms of market share and sales volume, and the only category that can compete with it is the liquor category. But from the perspective of growth, the beer market, which has been hardly turbulent for many years, is obviously not as imaginative as low-alcohol wine.

Only 5 minutes after the opening day of Double 11 in 2020, the fruit wine transaction volume of JD Supermarket increased by 40 times year-on-year; the transaction volume of cocktails increased 15 times year-on-year. According to data from the Tmall platform, fruit wines and pre-mixed wines are the fastest-growing wine category on Tmall, with a rapid growth of about 300% in 2020.

It is worth mentioning that there is no national brand in the low-alcohol wine sector. When the beer companies on this shore have already battled into the Red Sea, the budding low-alcohol liquor has just ushered in the blue sea and blue sky.

In addition to low-alcohol, another candidate answer is craft beer.

Craft beer is a concept relative to industrial beer. Different from the latter’s mass production’s popular positioning, craft beer takes a fine and characteristic niche route.

Since 2018, craft beer has started to make waves in the capital circle. Under the slogan of “Fresh Beer Suitable for Contemporary Young People”, many projects have stepped into the territory of mainstream beer with the promotion of consumption upgrades.

For a time, many cutting-edge brands such as Panda Craft, Zebra Craft, Monkey Craft, Whale Wine, Niu Beer Hall, Boxing Cat, etc. received capital attention, and major mainstream wineries have also tried to use the concept of “craftsmanship”. Regain market confidence.

Facts have proved that the strong demand indeed drives the continuous expansion of the craft beer market. numberAccording to statistics, from 2012 to 2018, the number of craft beer manufacturers increased from 7 to 848 in just 6 years, a 120-fold increase. The sales volume of craft beer increased from 567,000 tons to 879,000 tons, an increase of more than 50%.

To this day, craft beer still shows vigorous growth potential. According to the “Survey and Analysis of China’s Craft Beer Market Supply and Demand from 2020 to 2024 and Research Report on Investment Development Prospects”, the scale of my country’s craft beer market in 2019 will exceed 24 billion yuan.

In the future, benefiting from consumption upgrades, the market size of craft beer will continue to show an increasing trend. By 2024, the market size is expected to reach 68 billion yuan, with a compound annual growth rate of approximately 23.2%.

04 Conclusion

How can the traditional wineries remain indifferent when the challengers are coming down the city?

Take Tsingtao Beer as an example.

In July 2019, Tsingtao Brewery officially released Prince Soda and announced its entry into the soda market. In 2020, Tsingtao Brewery once again announced the increase in the scope of whisky and distilled spirits, and even revealed its intention to enter the rice wine field.

“Crossover Wine King” is becoming the future competitive strategy of major wine companies.

As stated in the article “One can to the top, the braveness of beer stocks”, for the beer industry, now the entire industry has entered a stable situation of oligopoly, and the main contradiction of the company has begun to fight for market share. Product structure change. In the past, it was the brand and channel. In the future, the beer war will return to the product level.

Beer has entered the age of a glass of ocean, and taste will determine the survival of the fittest in the next stage.

From brand channel as king to product as king, this is not just the story of beer.

Reference material:

“Dismantling 10 Beer Earnings: High, High, High”, Yunjiu Headline

“Beer bubbles, who can become the “Moutai” of the beer industry? “, Yiouwang

“What happened to the beer when the liquor skyrocketed?” “, New Retail Business Review

“A Brief History of Chinese Beer”, Kuaidao Finance

“One can to the top, the brave journey of beer stocks”, Yuanchuan Research Institute