Domestic cloud computing has entered the 2.0 stage.

Editor’s note: This article is from the WeChat public account “First New Voice” (ID: thefirstnewvoice), author: okay, editor: Tian Yanhong, proofreader: Hao Lingling, planning: Eason.

In the past ten years, in addition to mobile Internet, domestic cloud computing has also made a glorious history.

For example, China is one of the fastest growing markets for cloud computing in the world, maintaining an average annual growth rate of more than 30%. Alibaba Cloud, Tencent Cloud and Huawei Cloud are among the top ten global cloud computing lists.

After more than ten years of development, the upstream and midstream patterns of the domestic cloud computing market have basically been determined, but there is huge room for development in the downstream market, especially SaaS will usher in an explosion.

In addition, the first new sound in the “digital China” enterprise cloud technology segment companies in the process of research found that with the continuous deepening of the digital transformation of Chinese enterprises, cloud computing has expanded from simple market expansion, allowing enterprises to use the cloud and use Cloud and purchase of SaaS software have gradually entered the deep water area of restructuring systems based on cloud native technology.

So, who are the main players in the industry? What is the pattern of the future market? In which direction will it continue to move forward?

01 Upstream and midstream patterns are basically determined

The beginning of the cloud computing industry is difficult to accurately define. Although the concept of “cloud computing” was first proposed in 2006, it was not until 2008 that the era of global cloud computing gradually opened, and many giants joined in .

In the Chinese market, in 2009, Alibaba established Alibaba Cloud, a cloud computing subsidiary, which actually raised the banner of “Go IOE”. The following year, the giant Huawei also officially announced its cloud computing strategy.

Since 2012, some start-up cloud vendors have been born in China. In March 2012, Ji Xinhua, known as the “white hat hacker” in the rivers and lakes, founded UCloud; in April of the same year, three people with IBM work experience Huang Yunsong, Lin Yuan and Gan Quan co-founded QingCloud; September 2013 , Tencent Cloud announced that it is officially open to the whole society…

From 2017 to 2018, the domestic cloud computing market continued to invest in mergers and acquisitions. Public clouds generally entered the PE phase, while private clouds were concentrated in the VC phase. The layout of giant manufacturers in the public cloud market has basically been completed, and the private cloud and hybrid cloud markets have not yet formed absolute giants. There are many directions that can be penetrated in depth. Private cloud and hybrid cloud have become the focus of investment institutions. China’s cloud computing market is blossoming.

Data from China Academy of Information and Communications Technology (CAICT) shows that from 2015 to 2018, China’s cloud service market achieved a compound growth rate of 38%. It is expected to achieve a compound growth rate of 28% from 2019 to 2024. It is expected that the scale of China’s cloud service market will beReached 560 billion yuan, of which public cloud was about 370 billion yuan.

Data source: CAICT, BCG analysis, graphics: First New Sound

In 2020, Meituan Cloud and Suning Cloud successively announced the closure of public cloud services. From the perspective of the entire market, this is just a splash.

After more than ten years of development, the upstream and midstream patterns of the domestic cloud computing market have basically been determined.

In the cloud computing market, it’s not just technology. After all, the gap in technology is not enough to become the only criterion for companies to choose cloud services. Behind this need to consider factors such as product integrity, service capabilities, community ecology, brand operation and so on. Among them, product integrity is the core issue of market concern.

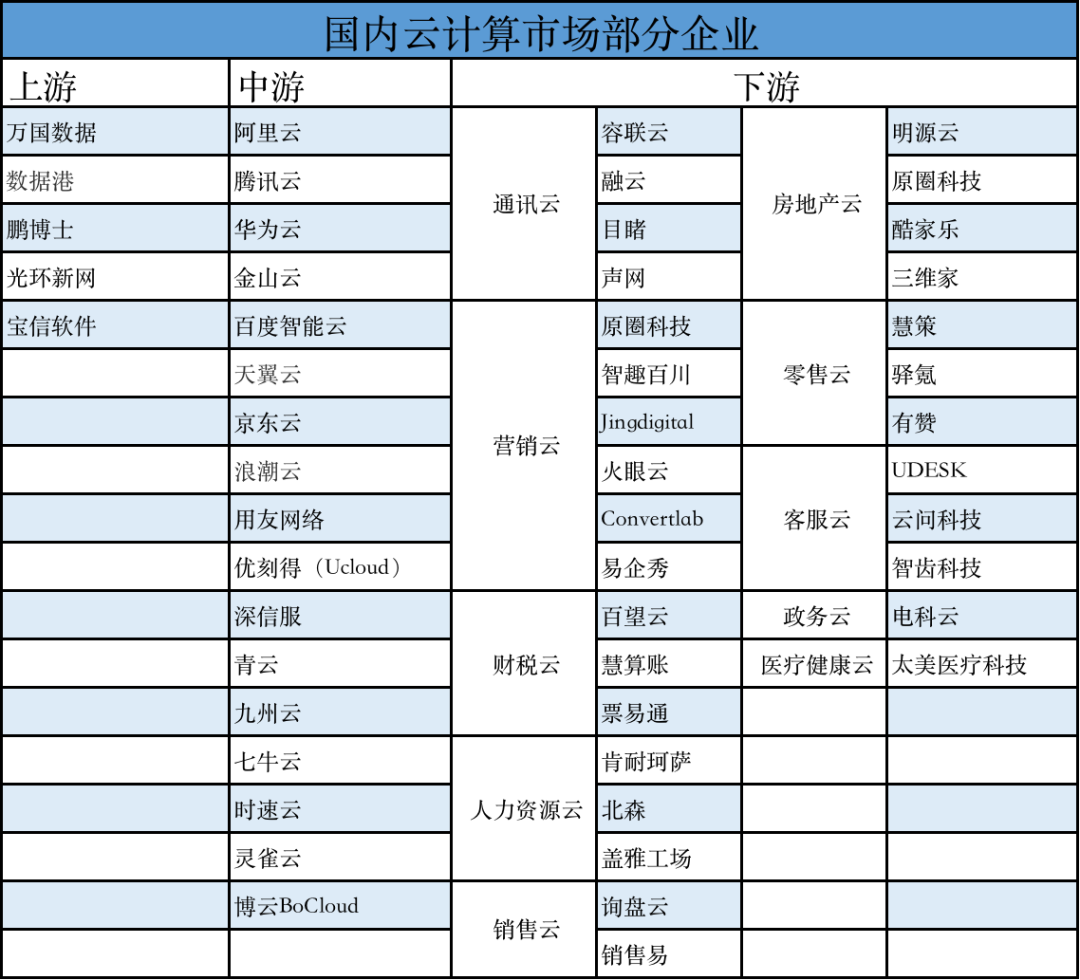

The cloud computing industry can be divided into four parts, namely upstream hardware service providers, mid-upstream IDC service providers, midstream cloud service providers, and downstream software service providers. According to the type of service, cloud computing can be divided into three categories: basic equipment as a service (IaaS), platform as a service (PaaS), and software as a service (SaaS), with increasing depth of service.

Drawing: The First New Sound

The middle and upper reaches are IDC companies. There are many IDC companies in China, the largest of which is GDS (US stocks), the data port and Dr. Peng that are deeply tied to Alibaba, and the Sinnet, Baosight Software, which is deeply involved in first-tier cities.

Midstream is the leader in providing cloud computing technology. In China, Alibaba Cloud, Tencent Cloud, and Huawei Cloud belong to the first echelon, and Jinshan Cloud, Baidu Cloud, and Tianyi Cloud belong to the second echelon. In addition, Youyou.com, Ucloud, Shenxinfu and Qingyun are listed on the A-share market.

Players in the midstream have basically achieved positive revenue growth, and the overall player is thriving. For example, Alibaba’s financial report shows that for the quarter ended March 31, 2021, Alibaba’s cloud industryBusiness revenue reached 16.76 billion yuan, a year-on-year increase of 37%; Tencent’s 2021 Q1 financial report data showed that Tencent’s financial technology and corporate services business revenue increased by 47% year-on-year to 39 billion yuan. In addition, Jinshan Cloud’s Q1 revenue in 2021 was 1.814 billion yuan, a year-on-year increase of 30%; Ucloud’s Q1 revenue in 2021 was 710 million yuan, a year-on-year increase of 72.31%.

The relevant person in charge of Ronglianyun said to First Xinsheng: “The upstream and midstream patterns are stable. How to build a cloud service ecosystem with partners in the head vertical business and broaden the moat is the barrier. Because of cloud computing It is impossible for giants to complete all their businesses. Just like Ronglian Cloud’s business, based on the upward expansion of communications, it can be integrated with the company’s marketing, operations, and services. Giant companies cannot do it. The trend is with upstream and downstream companies like Ronglian Cloud. Manufacturers work together to accelerate the comprehensive digital transformation of domestic companies while expanding overseas markets.”

At present, various cloud vendors have established their own SaaS ecosystems. For example, Tencent’s latest financial report shows that Tencent will continue to strengthen efficient office SaaS products and security software, as well as partnerships with and investment in SaaS vendors and independent software vendors to support customers’ digital needs. Further enhance the advantages in the SaaS ecology.

“The so-called ecologicalization, First, in terms of meeting customer needs, vendors in various fields complement each other and work hand in hand. For example, Shisu Cloud has united many ecological partners around the cloud-native technology base. Including manufacturers of data, security, storage, hardware resources, etc., facing customers to form a relatively complete solution, that is, an ecological technology stack; The second is that they can cooperate with each other in business, because they can form complementary With technical solutions, the customers and needs that the ecological partners can meet will become more extensive, and they will be more motivated to achieve collaboration in business acquisition.” said Yang Lexiang, the COO of Speed Cloud.

Wang Qingchen, founder and CEO of Yunwen Technology, told First New Sound that midstream is a leading company that occupies most of the market, but there are also scattered vendors that provide detailed services. In the future, a system of ecological cooperation will be formed with leading manufacturers as the core and scattered manufacturers to jointly build a domestic cloud computing service circle.

The downstream are mainly software companies. Communication cloud, fiscal and tax cloud, human resource cloud, marketing cloud, etc., are all industries and scenarios where specific cloud computing applications are implemented.

02 The downstream pattern is undetermined, SaaS blooms in bloom

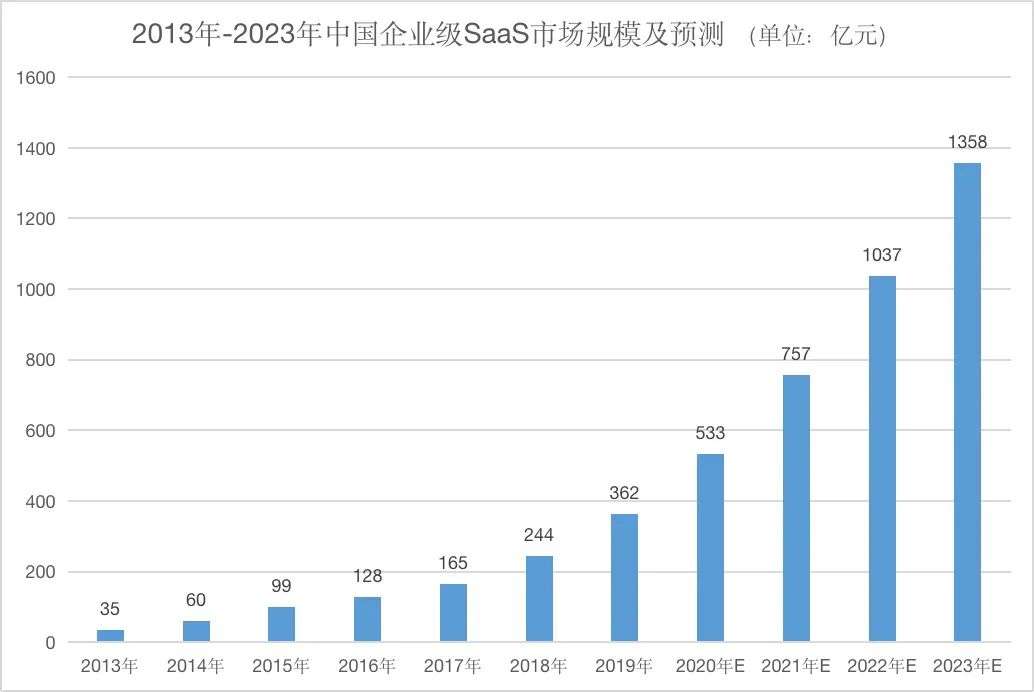

The downstream market has huge room for development, especially SaaS will be the most mature market segment in the cloud computing field.

According to iResearch’s “China Enterprise SaaS Industry Development Report 2020”, the scale of China’s enterprise SaaS market in 2019 has increased by 48.7% compared to 2018. In the future, the market will continue toMaintaining a rapid growth rate, it is expected that the scale of China’s enterprise-level SaaS market will exceed 100 billion yuan in 2022.

Data source: iResearch Graphics: First New Voice

In response to the phenomenon of domestic cloud service providers that are perpendicular to the industry, Wang Xiao, founder of Jiuhe Venture Capital, said to the first new voice that as China’s transition from a flow economy to an efficiency economy, Chinese companies are also moving from extensive The rapid growth has entered the stage of refined operation, and digitalization is needed to reduce costs and increase efficiency. The increase in cloud penetration of SMEs has brought about a wave of digitalization in marketing, HR, and other management links. The SaaSization of software in vertical fields has stronger connectivity, connecting upstream and downstream along the industrial chain, and it is possible to develop from SaaS tools into a trading platform, empowering roles in the industry and improving industrial efficiency.

What is the development status of the downstream cloud computing market in the future?

Wang Xiao believes that the infrastructure players at the IaaS layer have been relatively fixed. However, there are many subdivisions of PaaS and SaaS on cloud computing infrastructure, such as cloud-native core middleware, development tools, databases, data warehouses, security, multi-cloud management, and scene-based applications for SaaS. There are still many development opportunities. .

“Enterprise services, business software, and operation management software are more suitable for SaaS types, while PaaS itself is a platform type and requires more technical bases to support it, which is more suitable for technology-driven companies like Shisu Cloud< /strong>. The midstream has now reached a certain stage. It is very difficult for startups to enter this market if they do not have a good foundation. After all, the midstream market space has been basically finalized, and the first movers have the first-mover advantage. Currently including Shisuyun in Many companies in China have basically formed advantages in the market, technology, and customer scale in the field of cloud computing that they focus on. The establishment of barriers to advantages requires a lot of R&D and market investment. However, with the development of Internet technology, the demand for digital transformation of enterprises continues Expansion, the downstream market is likely to have many new business models in the future. With the growing demand for cloud services in more industries, there will be more new opportunities for exploration in the future.” Yang Le said.

Ronglianyun is the first Chinese SaaS company to go public in the United States. It will be listed on the New York Stock Exchange on February 9, 2021.

Introduced by the relevant person in charge of Ronglian Cloud, the company is based on the cloud computing and artificial intelligence departmentA series of technologies to help enterprises and government organizations realize the all-digital upgrade and integration of production management, marketing, operation services and other systems. The main products include CPaaS communication capabilities (voice, SMS, etc.), CC (Smart Cloud Customer Service and Cloud Contact Center), UC&C (IM and enterprise mobile portal, dual recording, CV visual intelligence).

“In fact, the communication cloud solves the connection problem. How to integrate data, marketing and operations after the connection is a problem that all cloud communication industries or companies that are perpendicular to communication must think about. Internationally, we used twilio, the target company, to provide basic cloud communication services, serving very large customers, such as Coca-Cola and other companies. How does it make the thickness of its products? The integration and acquisition of data companies, and then expand horizontally and deepen vertically, such as extending to CRM and other directions.” said the relevant person in charge of Ronglianyun.

03 The era of cloud native architecture is about to start

The ultimate development trend of cloud computing may be toward a combination of private cloud and public cloud-hybrid cloud development. Because there is no absolute private cloud, there is no absolute public cloud, pure public cloud and pure private cloud have their limitations, and hybrid clouds will be able to avoid their disadvantages and give play to their advantages.

Specifically, hybrid cloud can reduce the capital and maintenance costs of purely private clouds, and in specific scenarios, hybrid cloud can give play to the strong elasticity of public cloud for computing, storage, etc., but the core privacy data , But it can be processed in a private cloud to ensure security. And some flexible customized functions are handed over to the flexible private cloud to run. This hybrid cloud business model has been successfully practiced on the 12306 website.

In recent years, some people have continuously identified hybrid cloud as the new battlefield in the second half of cloud computing.

In 2018, IBM announced the acquisition of cloud computing open source software provider Red Hat for US$33.4 billion, turning to cloud computing and artificial intelligence, and becoming a promoter of open hybrid cloud. Two years later, IBM divested the traditional technology service business, and completely put the future on the hybrid cloud.

In addition, Cisco acquired CliQr, a provider of application management solutions for hybrid cloud environments, in early 2020 to focus on developing the track. Amazon aws, Microsoft Azure, Google Cloud Computing, and domestic Alibaba Cloud, Tianyi Cloud, Huawei Cloud, UCloud, etc., also entered the game early.

Xu Yan, a researcher at Baiwangyun Innovation Research Institute, said to the first new voice: “Hybrid cloud must be a trend in the future, a long-term model, and the market will not allow one to dominate. For our SaaS products, it will be a while. With a macro strategy, no matter what cloud can support and deploy.”

“The current form of hybrid cloud has been encountered in many products, because many large enterprises are unwilling to put everything on the cloud.Heyun’s model can more flexibly realize the user’s data control and other demands. “Wang Qingchen said.

In the opinion of the relevant person in charge of Ronglian Cloud, the form of cloud is not that important, and the enterprise is basically on the cloud. What everyone needs to do in the future is to innovate on the basis of the cloud, and to continue to expand the business. For example, Alibaba Cloud, Huawei Cloud, etc., in addition to basic cloud services, also involve storage computing, database and other services. How to integrate these services and provide a complete set of industry solutions is the core competitiveness.

As for the trend of domestic cloud computing, the opinions obtained in the interviews with the first Xinsheng are relatively consistent, but they have different views on the future challenges.

Wang Qingchen believes that the current domestic cloud computing challenges are more prominent in the SaaS field. “Because after enterprises go to the cloud, there will be more and more SaaS products, the overlap between products will increase, and the competition will become more fierce. How will the future products be integrated with the vertical industry? How to learn from the core algorithm, core data, product It is the great challenge that most manufacturers face to ensure their core competitiveness at all levels such as application and landing.”

Wang Xiao and Yang Le both believe that data is the biggest problem.

Wang Xiao pointed out that the phenomenon of data islands is obvious, and it is necessary to further open up data and improve data quality. The use of cloud-native architecture can make data flexible and scalable. For example, the cloud-native data platform KubeData™ of Speed Cloud integrates container cloud, data development, data intelligence, data assets, data services and other functions, which can solve the problems of data islands, data maintenance difficulties, and low data value utilization faced by medium and large enterprises. , To help companies make data an asset.

“In the cloud-native era, cloudification is considered from the design stage of applications, which can give full play to the flexibility of the cloud and make applications run better on the cloud. Many SaaS companies in the future will be the cloud since they were founded. The native model is more flexible, easy to use, and highly compatible.There will be development trends such as verticalization and sinking. Cloud native will change the links of the industry chain, such as reducing costs, accelerating delivery, and reducing dependence on channels. The combination with vertical fields will bring structural opportunities. More small and micro enterprises will go to the cloud, and the penetration rate of the cloud will be further increased. The top cloud vendors will establish their own enterprise service ecology, and many application layer opportunities may be established in the top Above the ecology of cloud vendors.” Wang Xiao further explained.

Yang Le said: “Cloud native will sink the general technical capabilities that support business applications to the infrastructure, and provide continuous and stable services in the complete life cycle of business applications to maximize the value of the cloud. Allow enterprises to achieve higher efficiency in resource allocation, product delivery, system architecture, etc., and be able to focus more energy on response, analysis and decision-making from a business perspective, so as to enable enterprises to compete in a market environment with fierce competition and changing needs Has a stronger innovationNew advantage. “The introduction, KubeData product released by Shisu Cloud, connects with the storage and computing capabilities of big data, and provides data construction and development capabilities. It assists enterprises in screening business data, model building, algorithm development, mining training, etc. Process and analyze operations, and then capitalize and service data, and enable enterprises to apply data experience to future business decisions, and enhance their data insight capabilities and data value industrialization capabilities.

Coincidentally, during the “Digital China” series of industry and company surveys, Yao Yi, the founder and CEO of First Xinsheng also found that many companies/government departments are in the process of upgrading/transforming from informatization to digitalization. The deep-seated demand problem of system reconstruction through cloud native technology is discussed.

“Once fragmented systems, it is difficult to form integrated applications, cannot be modified in time according to business needs, and it is difficult to support large-scale concurrency. It requires the use of microservices, containers, service networks, immutable infrastructure, and declarative APIs. Cloud-native technologies, represented by other technologies, make applications easier to expand and easier to use, especially in complex multi-cloud environments such as private clouds and public clouds, ensuring that applications and services can run across environments and be flexible Stretch.” Yao Yi introduced.

Xu Yan introduced to the first new voice: “There are two cloud service vendors, one is cloud native. The product design, definition, architecture, and even the entire thinking model are cloud-based. This is this type of cloud-native vendors. Another type of vendor itself started as a traditional offline business, and is now gradually deploying its business to the cloud to meet new market needs, but the logic and thinking may still be traditional. These two categories There will be differences between vendors, because the way of thinking is different, and the future development space and development curve will be different. The second type of cloud service vendors need to carry out thorough iterations along with customer needs. When the old underlying architecture is reborn, Will have more room for development.”

In the beginning, enterprises started to move to the cloud from the demand for flexible resources. Later, the cloud became the technology base, which brought about the shift of strategy. Nowadays, the value of cloud links has also changed from quantitative to qualitative, forming a positive cycle from changing the construction of enterprise IT infrastructure to boosting business progress. At present, the demands of enterprises to go to the cloud are gradually focusing on business reshaping.

In the cloud-native 1.0 stage, companies simply relocate their businesses from offline and run them on the cloud, solving problems such as operation and maintenance, deployment, and capacity expansion. However, the traditional application monolithic architecture is too heavy and caused by the chimney architecture. The series of problems have not been resolved. In the cloud native 2.0 stage, companies need to make their business born in the cloud, better than the cloud, and leap across the deep waters of digital transformation based on cloud-native technologies such as AI, big data, audio and video, and edge computing. They also need to inherit and develop their existing capabilities. The ability to synergize organically, stand and be unbreakable, enables every enterprise to become a new cloud-native enterprise.

In the future, under the general trend of domestic enterprises going to the cloud, more and moreOf enterprises and developers have begun to evolve their businesses and technologies to cloud-native. Faced with the huge dividends released by cloud-native technologies, they will surely reshape all aspects of Chinese enterprise IT and enable enterprise IT to make better use of cloud-native Such facilities and services can be more competitive in terms of efficiency and cost, and further build business intelligence.

For more than ten years, the domestic cloud computing market has been surging, and in the next ten years, cloud computing will enter the 2.0 stage. On the one hand, traditional enterprises start to go to the cloud and use technology to innovate their businesses. On the other hand, enterprises will embrace a more thorough cloud-native technical architecture that supports digital-native organizational forms and business models.

Reference Materials:

“The next battlefield of cloud computing, will it be fully opened soon? 》

“A Decade of Cloud Computing: The Game Between Great Powers and the Life and Death of Internet Giants”

“A Decade of Turmoil: The Past, Present, and Future of Cloud Computing”