Ng>

Seven thresholds: no market value requirements

I don’t want to tear it down. According to the “Regulations”, the separation of listed companies should meet seven conditions in principle. It is worth mentioning that there is no previous market value requirement.

At the beginning of this year, the industry circulated a threshold for the listing of A-shares in the A-share market, including: listed companies (parent companies) listed for 5 years, 3 months average market value greater than 15 billion, 3 years total deduction The net profit is greater than 1 billion.

The Provisions do not mention the requirement for the market value at all, but set the profit threshold.

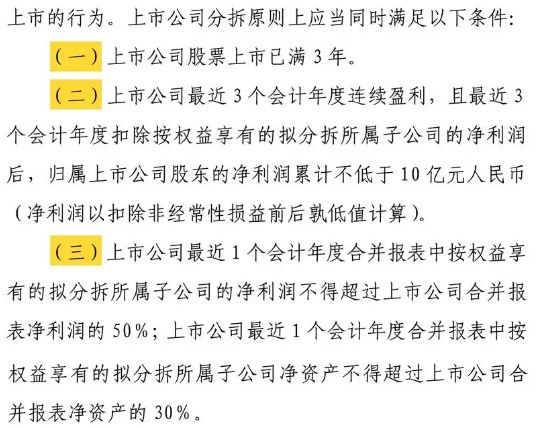

Among them, the three most important financial indicators are: the parent company’s stock has been listed for three years; the last three fiscal years have been continuously profitable, and after deducting the net profit of the proposed subsidiary, the parent company’s net profit is not low. In the recent consolidated financial statements of the parent company, the net profit of the proposed subsidiary shall not exceed 50% of the net profit of the parent company, and the net assets shall not exceed 30% of the net assets of the parent company.

Not limited to the listing of the science and technology board, but also by the shell

Previously, the market generally expected to allow A-share companies to spin off their subsidiaries on the Kechuang Board. This time, the new regulations will be more innovative, and pilots will be launched to split the A-share companies and list them in China.

In the “Provisions”, the CSRC first clarified the concept of the spin-off of listed companies, that is, the listed company will initially issue shares in the domestic securities market in the form of subsidiaries that directly or indirectly control certain businesses or assets. Listing or realizing a reorganization of the listing.

The door to the spin-off was completely opened. Unlimited spin-off target areas, not only can be split into the board of the company, but also small and medium-sized stocks and the Shanghai Stock Exchange can also be used;In addition, it is also allowed to split the backdoor listing, not limited to Can be IPO.

On January 30 this year, the China Securities Regulatory Commission issued the “Implementation Opinions on Establishing a Science and Technology Board on the Shanghai Stock Exchange and Pilot Registration System.” It is mentioned that a listed company that reaches a certain scale can legally separate its independent and qualified subsidiaries from listing on the Science and Technology Board. Since then, the market expectation of the spin-off and listing of the market has been rising, and there have been a number of A-share listed companies getting together and splitting the company into the board.

No more than 100 eligible conditions

Although there is no market value requirement, the “Regulations” are more innovative and broader, but there may be no more than 100 A-share listed companies that meet the requirements.

According to the media calculations, according to the hard indicators set out by the spin-off listing, combined with the listed company’s governance, risk matters and other factors, and at the same time comply with the conditions of the split, and split the subsidiaries that are in compliance with the conditions for issuance and listing, there are less than 100 listed companies. , accounting for 2% to 3% of A-share market companies.

According to Caixin’s new report, nine listed companies have clearly stated that they are “preparing” or “intentionally” to spin off their subsidiaries to go public.

These companies cannot be split and listed

The following conditions are clearly not available for spin-off:

For the business or assets of the subsidiary to be listed, the “Regulations” require that the listed company’s business and assets for the issuance of shares and raised funds in the last three fiscal years, and the passing of major assets in the last three fiscal years. The business and assets purchased by the reorganization shall not be used as the main business and assets of the subsidiary to be split;The subordinate company is mainly engaged in financial business, and the listed company does not score the listing of the subsidiary.

The “Regulations” also require the relationship between Dong Jiangao and the proposed spin-off of the listed subsidiaries, that is, the listed company and the directors, senior management personnel and their affiliates of the subsidiaries to be split up hold the shares of the subsidiaries. It shall not exceed 10% of the total share capital of the subsidiary before the listing.

The Regulations also require that listed companies have no funds, assets occupied by the controlling shareholder, actual controllers and their related parties, or other material related transactions that harm the interests of the company; at the same time, listed companies and their controlling shareholders, The actual controller has not received administrative punishment from the China Securities Regulatory Commission in the past 36 months; the listed company, its controlling shareholder and actual controller have not been publicly condemned by the stock exchange in the past 12 months; the listed company has been in the last year and one The financial accounting report was issued by the certified public accountant with an unqualified audit report.

Strictly crack down on flickering

Gao Wei, senior vice president and sponsor representative of Northeast Securities, pointed out that under the parent-subsidiary organization structure, horizontal competition, related transactions, and independence are difficult to supervise, and natural hidden hidden interests are difficult to find and supervise. , related transactions and other activities. This is also the main reason why the regulators have not encouraged domestic listed companies to split their domestic listings.

In order to solve this problem, the “Regulations” are listed.The information disclosure and supervision methods of the company’s spin-off were elaborated. These include: the split of the listed company in accordance with the provisions of major asset restructuring to fully disclose information, but also to implement the special resolution procedures of the shareholders’ meeting; after the spin-off of the subsidiary’s issuance and listing, it should abide by the relevant provisions of the initial public offering of shares, reorganization and listing. In the specific implementation, the listed company is also required to fully disclose the impact of the spin-off and prompt the risk. The procedures for the performance of the board of directors and the general meeting of shareholders shall be approved by 2/3 of the shareholders present at the meeting, and 2/3 of the minority shareholders who are required to attend shall vote.

The CSRC stressed that false information disclosure, insider trading, and manipulation of the market found in the spin-off listing pilot, especially the use of spin-off listing for concept speculation, “flickering” spin-off and other violations of laws and regulations Strike strength.

VC/PE opportunities are coming

For VC/PE, The biggest potential benefit of the “Regulations” is that the exit channel is more open.

In fact, there are not a few spin-off transactions involving VC/PE. In December 2014, Neusoft Group announced an agreement with Hony Capital, Goldman Sachs, Neusoft Holdings and other investors to invest in its Neusoft Medical and Neusoft Xikang – the total amount of the two investments is close to RMB 3.8 billion (converted at the exchange rate on the day of the announcement) ), and become the largest single financing in the domestic medical device field and Internet + medical and health management, and the largest single financing in the global Internet medical and health management field.

According to the agreement, after the completion of the delivery of the investment funds, the parties will start the listing process of Neusoft Medical and Neusoft Xikang, and the deadline for completion of the listing is 6 years.

The six-year period is fleeting. The latest media reports show that Neusoft Medical and Neusoft Xikang are expected to be listed on the Kechuang Board. With the release of the new regulations, VC/PE opportunities have arrived.

However, there are a few points to be aware of.

A senior investment bank knows that the biggest significance of the spin-off listing is not to recreate a shell, but to encourage the listed company to act as an incubation platform for new business and core members of the new sector, and the draft for comments requires listed companies and The directors, senior management personnel and their related personnel of the subsidiary company shall not hold more than 10% of the total share capital of the subsidiary company before the spin-off of the listed company. “The incentive effect of this ratio may be worse, perhaps not The policy is expected.”

In addition, although the “Regulations” are not clearly defined, they actually hide the invisible threshold. “The cancellation of the market value standard is good, but the company with a profit of one billion in the last three years will not be too low in market value,” said an analyst at a leading third-party consulting firm.