This is the spring of sinking market users and the reconfiguration period of the e-commerce platform.

Editor’s note: This article is from WeChat public account “Lu Ming Finance” (ID: Luminglab), author Qiang Jiahong, editor Jin Delu.

The essence of game and balance lies in the diversification of stakeholders.

In April 2003, in order to attack the eBay eBay, Sun Haoyu returned to Hangzhou Lakeside Garden with 8 people and secretly developed a C2C e-commerce website.

After 24 days, Taobao was officially launched.

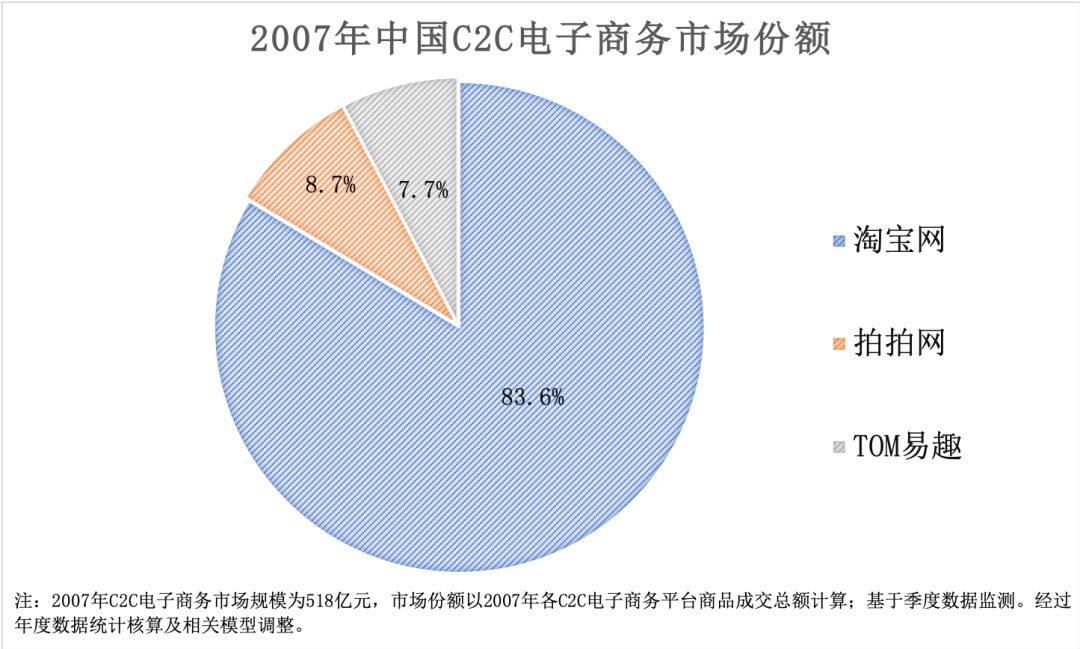

As the earliest C2C website in China, eBay has a market share of over 90%. In the face of the newly established Taobao, eBay’s global president Whitman has been arrogant to the extreme. He even concluded that “Taobao can only survive for up to 18 months. “.

The results we all know: two years later, eBay’s share fell to 29.1%, Taobao rose to 67.3%. Afterwards, Taobao topped the scenes, and eBay and new eggs were wiped out. Shanghai e-commerce has gradually drifted away.

When China’s C2C market was booming, Tencent launched its own e-commerce trading platform “Patting Network”, relying on the strong community advantage of Goose Factory, the pat network was established for three months, and the traffic ranking entered the world. Ranked in the top 500, the overall growth rate is as high as 1640%.

There are not the ones that they are robbing, not the e-commerce e-commerce eBay, which is not in the Chinese market.

For another two years, eBay handed over the position of the industry’s second child, and Patpa became the fastest growing community-based e-commerce trading platform in China.

Data Source: iResearch Consulting, 2007-2008 China Online Shopping Development Report

At this time, Taobao has occupied more than 80% of the domestic C2C e-commerce market. As long as it does not dig its own graves, the growth rate of the pat network is fast, and it is difficult to shake its points.

One side is a tepid e-commerce business, and the other is a video game in full swing. The choice of the goose factory is clear and clear: in 2008, it became a Tencent game.One year after the transition, Tencent has grown step by step to become one of the most profitable game companies in the world.

And their e-commerce dreams, in the strong enemy ring in the middle of the line: from the pat network, QQ mall, to Yi Xun network, trading treasure, Tencent in the e-commerce field again and again to smash sand In exchange for a hat with no “e-commerce gene”.

Since then, from south to north, China’s e-commerce rivers and lakes have been taken over by Hangzhou, and it seems that only Jingdong, which started in Beijing, has stood up.

Until today, we are still saying that the fundamental reason for Tencent’s e-commerce dream is that the Goose Factory has abandoned the strategic deployment of the e-commerce gold diggers in the case of unsuccessful personal results, relying on its strong WeChat QQ and other Social traffic is transformed into a role as a waterman.

The rise of many fights, the hope of JD.com, and the future of Vipshop will all depend on this strategic change. Tencent, despite being at the height of the temple, can turn its hands to cover the e-commerce for the rain. Rivers and lakes.

Now, this strategy of Tencent is encountering challenges. The distribution of traffic has entered the Red Sea stage of stocks. Balancing the game relationship between various companies (especially Jingdong and Jianduo) has become its primary problem.

01 Origins, The rise, prosperity and adjustment of the micro-business state

In 2013, things started to change.

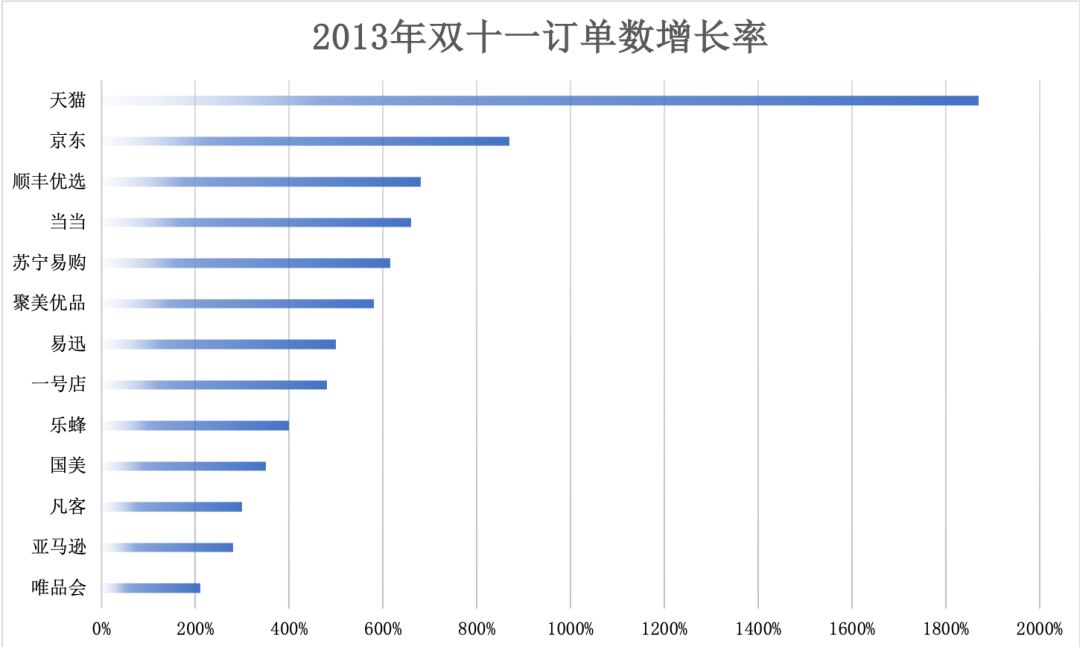

This is the second year that “Double Eleven” has become the carnival of all e-commerce platforms. In this year, Tmall became the biggest winner of the e-commerce platform with sales of 35.519 billion.

Data Source: Taobao Mall, “2013 E-commerce Double Eleven Analysis Report”

In the same year, the micro-business with the purchase and purchase of non-standard products as the main form quietly appeared in the WeChat circle of friends.

Although the birth of WeChat is not for the trading and trading of commodities, along with the iteration of the version and the promotion of payment functions, a group of business-savvy businessmen began to stock up and sell image ads in the circle of friends. It differs from traditional e-commerce in that it proposes a new social e-commerce model based on a strong relationship between people.

The burgeoning stage of micro-business starts with a mask from the circle of friends. When he was ten years old, he was the most popular mask brand in the circle. The overwhelming advertisements were not only spread over the circle of friends and Weibo, but also invited star platforms such as Bai Li and Zhao Wei.

In 2014, Sishao Group, which is known as “Wei Business First”, rose rapidly. It broadcasted advertisements on Hunan, Zhejiang, Tianjin and other satellite TV platforms, and won the gold tender advertisement of CCTV 2015 Spring Festival Evening. It was held in the Great Hall of the People. Dream Festival Conference………

Recording to the hot development rhythm of micro-business, it is a short-lived micro-business big coffee: on the network, the circle of friends is full of dazzling record of making money, and a silkworm is doing business for 4 months. Buy BMW, the founder of a micro-business team to show off the inspirational story of the rich car.

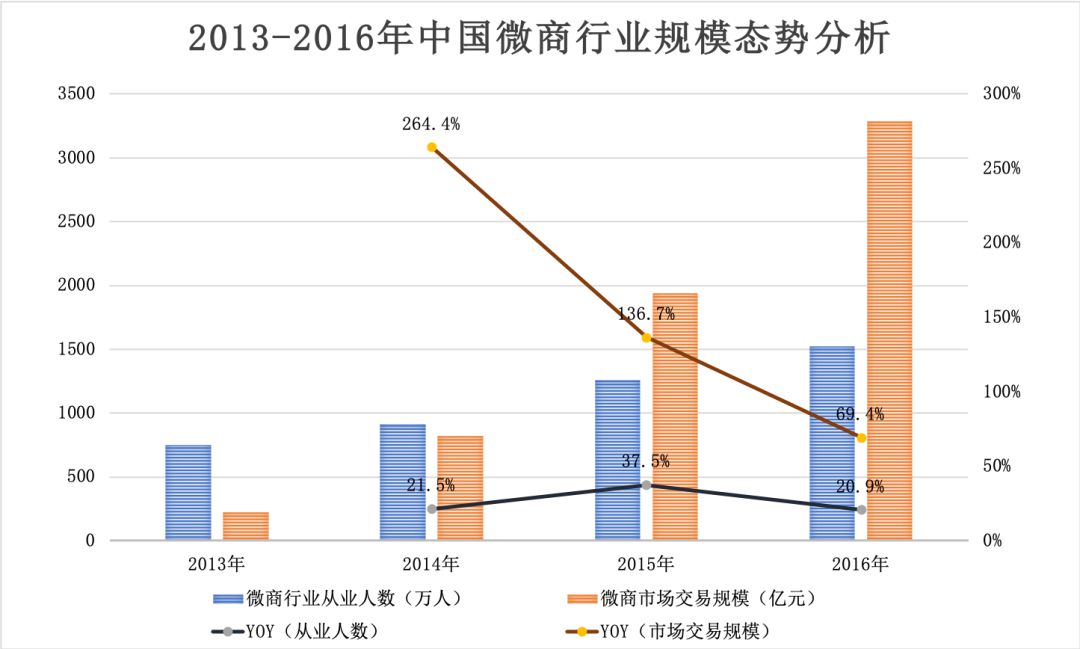

Data Source: iResearch, China Industry Information Network

In this process, Weishang also transitioned from the individualized operation of barbaric growth to the distribution of direct sales with manufacturers and the distribution of offline agents. The categories of goods also spread from masks and cosmetics to toiletries and clothing. , snacks and “Feng, Mei, Zhuang” (bamboo, beauty, impotence) and other miraculous products.

According to the data released by Tencent Research Institute, the customer price of the Weishang brand is not high, and the retail price is generally maintained at around 200 yuan. In fact, the ex-factory price of these products is only 20 yuan or even lower.

The ten-fold profit in the middle is divided by agents at all levels. What is more serious is that in the entire micro-business sector, about two-thirds of micro-businesses do not operate offline physical stores, which means There is no way to guarantee a series of problems such as the qualifications of dealers and the after-sales of goods.

Data Source: Tencent Institute, “A Brief History of Micro-Business: Rise, Prosperity and Adjustment”

In April 2015, CCTV successively broke the industry behind the micro-sales mask and the consumption trap of “micro-sales marketing”. The micro-business industry ushered in “Black May” and the performance of various micro-business brands appeared. The cliff-type decline, the popular brand of various explosions is gradually becoming weaker.

It doesn’t hide.

As a new business model, Weishang has completed the traditional enterprise ten years in less than a year. Soon, traditional companies like Libai, Shuk, and Langsha have joined the wave of micro-business, and the best of them are Han Shu. <