The maturity of the US credit card system has made mobile payments lack the support of merchants in the United States.

Editor’s note: This article is from WeChat public account “iFeng Technology” (ID: ifeng_tech), author Xiao Yu.

Although Americans are increasingly dependent on smartphones, most Americans still don’t use mobile phones to make payments.

In other countries, the development of mobile payments is another picture. Countries such as China and India are witnessing the rapid spread of smart phone payments.

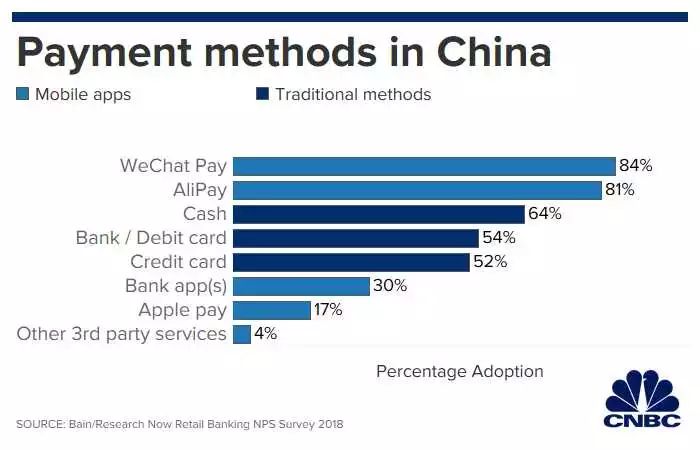

The data released by management consulting firm Bain shows that in China, more than 80% of consumers used mobile payments last year. Among them, Apple Pay has a penetration rate of 17%. In contrast, most mobile payment applications in the United States have a penetration rate of less than 10%, and Apple’s payment rate is only 9%.

“The United States is not a leader in mobile payments. Compared to other countries, the level of mobile payment development in the United States is at best a mid-stream country.” Barry North America Financial Services Business Partner and Head of Banking and Payments, Gerard According to Gerard du Toit.

Given that iPhones and Android phones are everywhere in the United States, the current state of development of mobile payments in the United States is somewhat strange. According to the Pew Research Center, more than 81% of Americans own smart phones, compared with 35% eight years ago. Although experts believe that the development of mobile payment in the United States will eventually narrow this gap, the traditional financial system, the lack of other options and the credit card rewards will become a major obstacle to the development of mobile payment in the United States.

Why can mobile payments rise in China and India?

In some countries, one reason mobile phones can become mobile payment methods is that cash is the only additional payment option in these countries and is not very attractive.

“China and India have always been two very cash-dependent economies. Mobile payments have made tremendous progress in managing large amounts of cash,” Dutoit said.

Apple payment penetration rate in China is 17%

For example, Indian regulators have been encouraging the abandonment of cash and the use of digital payments. Since cash transactions are often carried out in secret, abandoning cash can also increase the country’s tax revenue. India also requires real-time completion of low-cost interbank transfers to expand the scope of use. Dutoit said that this promotes mobile payments in India as “unbelievableThe super-fast speed is popular.

Mature credit card system in the US Mobile payment lacks merchant support

But in the US, the credit and debit card systems are mature enough to be good for most people. “One of the driving forces behind the popularity of mobile payments is its huge improvement,” Dutoit said. “But in the US, there are already good solutions here.”

Bank cards are widely accepted in the United States. In some cases, it is more convenient to swipe your credit card, because you also need to take out the digital device, unlock it before putting it on your face, then double-click the button and lift it to the front of the monitor to scan the code. Arieh Levi, senior analyst at CB Insights, a market research firm, also believes that the popularity of credit cards is a key reason why mobile payments cannot rise in the United States.

“In the US and Europe, the saturation of debit cards and credit cards is surprisingly high. Therefore, people already have a digital payment method that does not use cash,” Livay said. “In the field of mobile phone popularity, There are no established companies that have truly established market position.”

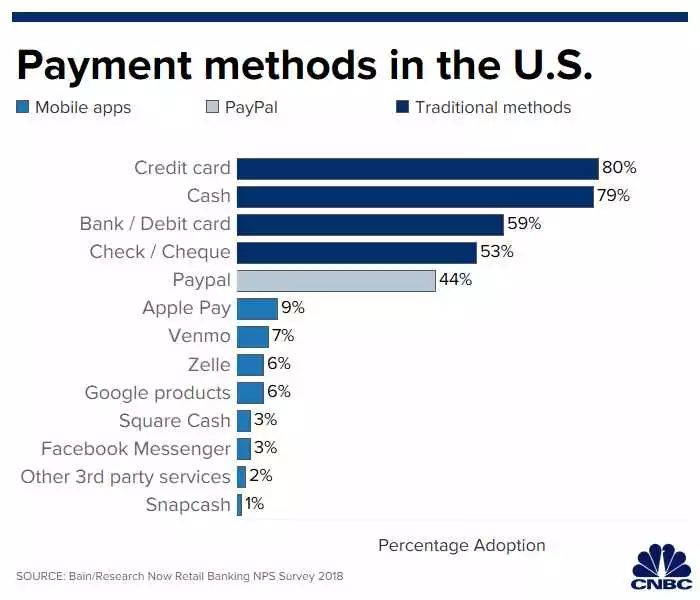

Apple Pay is 9% in the US

The traditional companies in the payment field include Visa, MasterCard and Bank. If the status quo changes, these companies will suffer a lot, including the income they get when they swipe their credit card. Liwai said that the most likely outcome would be the same situation involving the banks and credit card companies. However, the future user experience will happen on the smartphone, not the physical card.

In terms of mobile payment, there are many choices for American consumers, such as Apple Payment, Google Payment, Samsung Payment, PayPal, Square Cash, etc. But to use these applications, merchants such as coffee shops and retail stores need to have the right hardware.

“The reason is not in the consumer mobile experience, they have done very well,” said Peter Gordon, CEO of payment relationship management company PRMPayments. “It is a question of acceptance, which requires merchants to sign up. , costly.”

Bern data shows that traditional payment methods still dominate in the United States. Last year, 80% of consumers used credit cards to shop. PayPal is the most popular non-bank payment method with a penetration rate of over 40%, but is mainly used for online payments. The penetration rate of Apple payments is only 9%.

The payment company LoopPay has been acquired by Samsung. LoopPay founder Will Graylin said that even before allowing early adopters to consider switching to mobile payments, merchant acceptance needs to reach a certain threshold. He said that at least 90% of merchants need to accept it in order to let 1% of consumers change their habits. “The reality is that we haven’t reached this point yet,” Grayling said. “Mobile payments are not universally accepted by merchants.”

Credit Cards and Mobile Payments Help Apple’s Revenue Increase $5 Billion

In order to compete for users, credit card companies have introduced cashbacks and travel rewards that people can’t easily give up. According to the rewards and cash provided by the credit card company, the consumer will use a credit card to refuel, then use one to buy groceries, and then use another travel.

CB Insights’ Livay pointed out that it is not easy to switch consumers to mobile payments. He mentioned an exception: market research firm eMarketer’s statistics show that the Starbucks application is the most widely used payment application in the United States, with 23.4 million users. Apple paid 22 million users and Google paid 11 million.

“At Starbucks, the mobile payment application scenario is obvious: you can get a free cup of coffee with mobile payments,” he said. “For Apple payments and Google payments, this application may not exist.”

The joint credit card that Apple and Goldman has launched is based on this philosophy. The credit card provides 2% cashback for transactions processed through Apple Payments, 3% for transactions that purchase Apple products directly, and 1% for transactions using credit cards.

“Apple Credit Card has injected liquidity into Apple’s payment app,” he said. “This is not the only reason Apple has introduced a credit card, but it must be a part of its push to move funds to other parts of its ecosystem.”

Amit Daryanani, an analyst at investment banking consultancy Evercore ISI, predicts that the introduction of credit cards and the rise in Apple payment penetration will drive Apple’s revenue growth by $5 billion in the next few years.

Drenari believes that as US contactless payments develop on the basis of current small applications, the penetration rate of Apple Payments in the international market will rise, and the amount of transactions paid by Apple will increase exponentially to 2020. It will reach approximately $1 trillion in the year. He said that even if this level is reached, Apple’s payment processing will still be less than 10% of the global turnover of more than 11 trillion US dollars.

Feed system or drive mobile payment development

The Fed’s recently released oneReal-time payment systems may also change the landscape of mobile payments.

The Fed announced a real-time payment system in April that would allow the transfer to arrive in real time. The Fed said the payment system, called FedNow, will go live in 2024, allowing funds to be transferred in real time.

PRMPayments’ Gordon said the project could change the current mobile payment landscape because FedNow allows companies such as entrepreneurs and PayPal to take advantage of direct, real-time connections between the system and customer accounts.

CB Insights analyst Livai believes that this can also enable Facebook’s WhatsApp applications, and even technology giants such as Amazon and Google to launch more bank-like services that are most likely to be rooted in mobile devices.

Bern’s Dutoit believes that although these will help non-banking companies enter the payment field, credit cards will continue to exist. He said that people don’t always want to pay for shopping immediately and in real time, the function of borrowing is still valuable, and there are coveted rewards and points. Credit cards may look like a “hybrid version” of the old model, packaged in mobile form, and sometimes incorporated into the app.

“There will be different patterns in the future, and I really want to see which model will win,” Dutoit said.