Arterial network vcbeat|Policy bonus + blank market has become a bundle of bright light for orphan drug research and development companies

Editor’s note: This article is from WeChat public number “Arterial Network” (ID: vcbeat), author Hao Han.

September 13th, 2019, US time, the rare disease drug research and development company SpringWorks Therapeutics landed on the NASDAQ, the issue price of 18.00 US dollars, the opening price of 24.50 US dollars, real-time stock price of 22.63 US dollars, an increase of 45.22%. The “new company” that was spun off from Pfizer in 2017 was completed in just two years, and the secondary market has shown a positive attitude toward the “small cake” of rare diseases.

SpringWorks’s share price was finally fixed at $22.63 and the total market capitalization was approaching $1 billion

Since the FDA issued the orphan drug bill in the 1980s, the development of rare-dose drugs has always been an industry promoted by drug regulatory authorities in various countries. The policy dividend + blank market has become a unique light for orphan drug research and development companies. This market seems to have found new directions after policy promotion, and SpringWorks is one of them.

Financial Information: Continued losses, but sufficient cash flow

SpringWorks Therapeutics is a clinically based rare disease and oncology drug development company that was separated from Pfizer in October 2017 and is responsible for the development of some of Pfizer’s rare disease drugs.

The splitting of a business line that is not in line with the company’s strategy into an independent company is one of the things that pharmaceutical giants have done in recent years, but it does not mean that these lines of business no longer have investment value.

From the perspective of SpringWorks’ financing history, both pharmaceutical companies and capital are still interested in these drug pipelines. Pfizer itself is continuing to inject capital into SpringWorks.

Investors in SpringWorks include Pfizer, GlaxoSmithKline (GSK), Bain Capital, and Aobo CapitalOuter head pharmaceutical companies and well-known investment institutions.

After its establishment in September 2017, it completed a $103 million Series A financing, and in April 2019 it completed a $125 million Series B round of financing. According to the description in the prospectus, the IPO, SpringWorks issued a total of 7352941 common shares, the issue price of 18 US dollars, a total of $ 132 million. The funds will be used for the clinical development of its drug pipelines Nirogacestat and Mirdametinib.

SpringWorks Revenue Sheet

SpringWorks Cash Flow

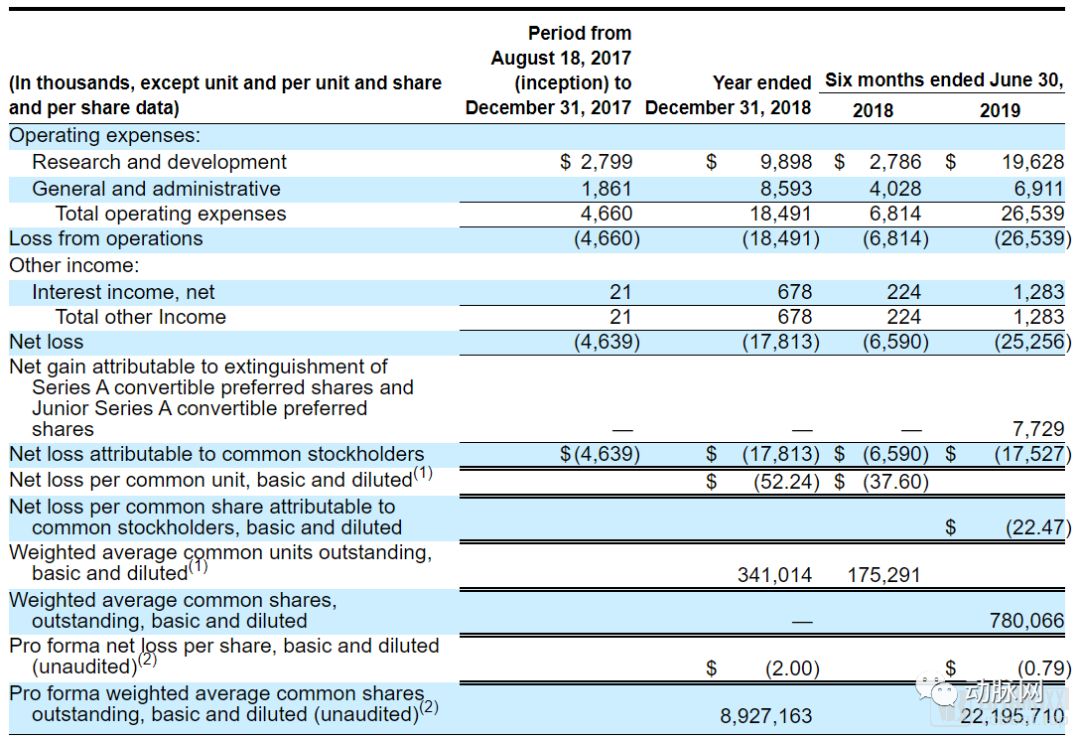

For start-up pharmaceutical companies, it is a normal situation to make ends meet. SpringWorks’ net loss in 2018 has reached $17.8 million, but this seems to be just the beginning of burning money. With the opening of two new clinical trials, R&D investment in 2019 rose sharply, reaching $25.3 million in the first half of 2019 alone, exceeding the 2018 annual loss.

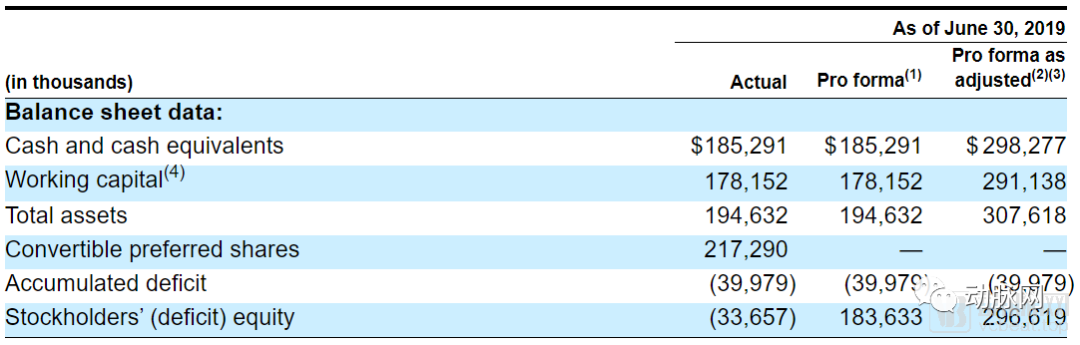

However, investors don’t seem to worry about it for a while, there is still $185 million in cash on SpringWorks’s books. After this IPO, the capital reserve will exceed $300 million. The money should be enough for SpringWorks to burn to the market.

Drug Pipeline: Two core drugs will be available around 2023

Product pipelines for rare disease drug development companies are becoming more and more centralized. In the context of the expansion of other innovative pharmaceutical companies, orphan drugs are constantly shrinking their pipelines, allowing their funds to be concentrated in the clinical advancement of several head drugs.

Charles, a rare disease giant acquired by Takeda in 2018, has a phase III/IV clinical trial that accounts for more than 50% of all clinical trials, a figure that is only 30% higher for most pharmaceutical companies.

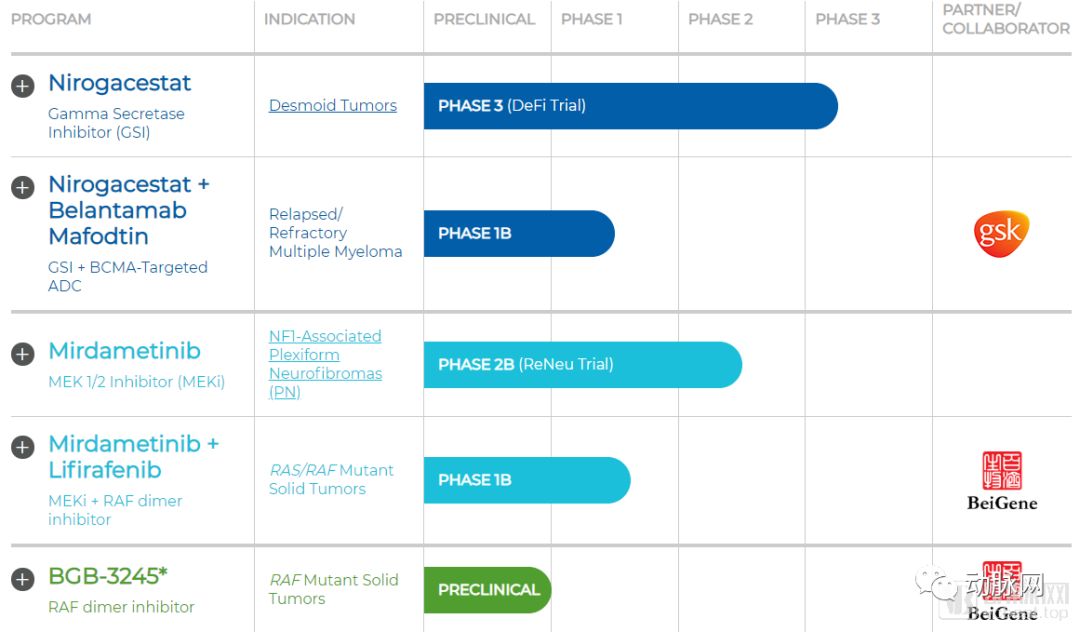

SpringWorks Research Pipeline

SpringWorks’ drug pipeline is extremely streamlined, with only two drug lines belonging to it, originally belonging to Pfizer’s Nirogacestat and Mirdametinib. Another drug is BGB-3245, which was developed in cooperation with Baekje Shenzhou. The original developer of the drug is Baekje Shenzhou.

1.Nirogacestat:The leader of hard fibroma

Nirogacestat is the undisputed drug of SpringWorks and is currently in Phase III clinical trials for the treatment of patients with hard fibroma. Nirogacestat has shown good tolerance in previous clinical trials and has observed clinical efficacy in patients with hard fibroids. In June 2018, the FDA granted Nirogacestat an orphan drug certification, which was approved for entry into the fast track in November, and in August 2019 it was given a breakthrough therapy.

Nirogacestat’s Phase III clinical trial opened in April 2019 and is currently in the patient recruitment phase. According to SpringWorks’ information disclosed in the prospectus, Nirogacestat can meet the primary endpoint of this clinical trial as long as it is comparable to previous clinical trials in Phase III clinical trials. The clinical trial is for a four-year period and is expected to end in April 2023.

There are no specific drugs for hard gliomas on the market. Nirogacestat is one of the fastest growing clinically in the field of hard gliomas, and the other two drugs for hard glioma are still in Phase I clinical stage. The number of patients with hard gliomas is only about 0.03% of tumor patients, and the corresponding new cases are about 5,000 people worldwide. According to the per-patient treatment cost of 200,000 US dollars, the market penetration rate of 20% is conservatively estimated, Nirogacestat’s annual sales can reach 200 million US dollars.

2.Mirdametinib:A powerful player in the neurofibromatology market

Mirdametinib is another orphan drug that SpringWorks inherits from Pfizer, originally codenamed PD-0325901, for the treatment of type I neurofibromas. Mirdametinib received FDA orphan drug recognition and entered in 2018The fast track, in July 2019, was awarded the European Commission’s orphan drug status.

Mirdametinib just started a three-year phase II clinical trial in July 2019. According to SpringWorks’ disclosure in the prospectus, if the test results are good, they plan to apply for the market directly in the United States based on the results of the Phase II clinical trial. Therefore, Mirdametinib may be listed before Nirogacestat.

But the market for neurofibromas is not as simple as a hard glioma. A number of pharmaceutical companies are targeting the market for neurofibromatosis, Merck’s Pabolizumab, Roche’s Bevacizumab, Novartis’s trimetinib, and AstraZeneca’s Smetinib are all undergoing nerves. Fibroids are studied and are in the clinical phase II phase. It is also rare that these competing products have obtained neurofibroma orphan drug identification. Therefore, from the current situation, Mirdametinib does not predominate in the market competition of neurofibroma. This may also be a key reason why SpringWorks wants to skip the phase III clinical trials in advance.

External cooperation: Close relationship with Baekje Shenzhou and GlaxoSmithKline

SpringWorks did not have further product exchanges with its old owner, Pfizer, but launched a clinical research collaboration with another international drug company, GlaxoSmithKline, to study the combination of Nirogacestat and GlaxoSmithKline’s Belantamab. Use in relapsed/refractory multiple myeloma.

Belantamab has demonstrated efficacy in patients with multiple myeloma in Phase I/II clinical trials. This combination study will play a key role in the expansion of Nirogacestat’s indications.

SpringWorks also has a close working relationship with Baekje Shenzhou. In June 2019, the two announced the joint establishment of MapKure to develop Baco’s new cancer drug BGB3245. Subsequently, the two announced further cooperation on September 6th, which will jointly open clinical trials to study the safety, tolerability and initial efficacy of combination therapy between BGB-283 of Baekje China and PD-0325901 of SpringWorks.

How does the small and rare disease market attract developers? Under the reward, there must be a brave

Rare drug development is not a market that developers are eager to see. The difficulty in the development of orphan drugs is not as difficult as other drugs, but also through the entire process of drug development from molecular design, animal experiments to clinical trials, post-marketing research. Failures in any one link can directly lead to the death of the project. A rare disease that has been successfully listed on the marketThe drug also faces a very small patient population. This makes the “ceiling” of rare drugs more natural than other drugs.

Evenly, orphan drug research and development has become one of the hottest segments of drug discovery. The reason for this is that the policy has shown a strong driving force, and a large number of policy dividends have raised the profit margin in this small market.

1. Fast time to market and low clinical trial consumption

Regulatory agencies in various countries have developed regulations to promote the development of orphan drugs. The FDA introduced the Orphan Drug Act as early as the 1980s. China’s newly revised Drug Administration Law also specifically supports the creation of new drugs for rare diseases into the charter, and requires priority review and approval of new drugs for rare diseases. The priority review means the degree to which the regulatory authorities attach importance to orphan drugs. The shortened approval time allows rare drug drug development companies to profit from products earlier, which is a key policy for the orphan drug market.

Low consumption in clinical trials is another key reason for the attractiveness of the R&D industry. In the phase III clinical trial of common diseases, the number of patients enrolled was mostly between 300 and 500. The number of enrolled patients in rare clinical trials only needs 100 people. Although the proportion of patients enrolled in the total patient population is still high, clinical trial recruitment is still difficult, but for companies, the small number of patients means a comprehensive reduction in drug expenditures to experimental management expenses, which can help companies Save a lot of research and development costs.

2. Market exclusivity for strong policy protection

In different countries and regions, orphan drugs have been given a longer period of market exclusivity by the regulatory authorities. During the market exclusive period, generic drugs for protected drugs will not be approved for listing, and other drugs with the same indications will be blocked, unless the drug is approved, or the newly declared drug is confirmed to be more clinically superior. Sex. This time is 7 years in the United States and 10 years in the European Union and Japan. At present, China has also given a 10-year data protection period for rare diseases.

The establishment of the protection period means that orphan drug research and development companies have obtained market monopoly status after listing to a certain extent. This policy can effectively compensate for the low return on investment due to the small size of the orphan drug market. At the same time, this policy has also brought a sense of vision to the development of innovative drugs for the same indications. The first approved products will directly gain the dominance of the corresponding indications and greatly affect the reporting of other follow-up products.

3. The patient’s own pricing is just

The number of patients with rare diseases is small, but most rare diseases have not yet mature treatment options. This blank market means that the first approved orphan drug product will become the patient’s just-needed product. At the same time, the FDA is in the Orphan Drug Act.》 also gave the pharmaceutical company sufficient independent pricing power. Therefore, the price of orphan drugs listed so far is mostly very expensive. In May of this year, Novartis’s Zolgensma, which has been treating spinal muscular atrophy, has just set a record for the most expensive drugs at a price of $2.125 million.

But in reality, high prices may not lead to higher sales. Drug pricing should be negatively correlated with the number of patients who purchase the drug. Setting the drug at a more appropriate price to maximize its own income is the core issue to be considered in the pricing of rare drug research and development companies.

UniQure’s Glybera is the forerunner of drug pricing. Glybera was approved by the European Union in 2012 and officially launched in 2014 for the treatment of lipoprotein lipase deficiency. In addition to being the first to receive gene therapy, Glybera was the most expensive drug at the time, and the price of 1.11 million euros made it impossible for all drugs.

But the patient doesn’t seem to buy it. Only one patient in Glybera’s four-year sales period received Glybera’s treatment and was still in the case of large reimbursement by insurance companies. In April 2017, UniQure announced that it will not be postponed until the upcoming deadline. The first gene therapy drug has withdrawn from the stage.

Real world research and molecular diagnostics are bringing new opportunities for rare disease drugs

Real-day real-world research has a clearer application of rare diseases. Among the relevant policies issued in China, real-world evidence has been included in the research and development of regulatory drugs for rare diseases.

Due to the difficulty of recruiting patients with rare disease clinical trials, real-world data from natural disease cohorts can be used as external controls for non-randomized one-arm trials. In addition, real-world research can accelerate the recruitment of patients in clinical trials by studying the distribution of patients.

Molecular typing of the disease is creating new opportunities for the expansion of indications for rare disease drugs. With the help of scientific research and molecular diagnosis, people’s understanding of the cause of the disease has gradually deepened to the molecular level. The same changes in molecular levels may cause different diseases in different internal environments. These molecularly defined disorders can be treated with drugs that target the same target.

The nature of orphan drugs is still a targeted drug. Orphan drugs have the opportunity to find other indications triggered by the same target in new disease molecular typing. Based on the previously analyzed orphan drug advantages, its marketing approval process and clinical trial process have been significantly shortened. Therefore, after the orphan drug is rapidly listed, it can continue to conduct post-marketing research as a listed drug and explore more possibilities for indications.

The indication approval for listed drugs is much easier than the approval of new drugs. Therefore, it is a target-related drug that affects many diseases.In terms of things, it has been approved as an orphan drug, and research on other indications is also a good choice.