After a lapse of two months, Budweiser Asia Pacific has renewed its prospectus, and its pricing has also been reduced from the previous 40-47 Hong Kong dollars to 27-30 Hong Kong dollars.

Editor’s note: This article is from the WeChat public account “Tiger Community Selection” (ID: tigerbrokers2015).

Baiwei Asia Pacific $(01876) $7 hit failed in the market, a large part of the reason is that the price did not talk. At that time, Budweiser intends to raise up to HK$76.4 billion (approximately US$9.8 billion) at a price of HK$40 to HK$47 per share, with a total market capitalization of up to HK$509.6 billion. On the investment bank, the price is expected to fall below HK$37, which means that the valuation is too high.

After two months, Budweiser Asia Pacific has renewed its prospectus, and its pricing has also been reduced from the previous 40-47 Hong Kong dollars to 27-30 Hong Kong dollars. So the question is coming. What is the difference between the prospectus and the Budweiser Asia Pacific that has divested the Australian business? What happened to the two valuations? Is it still overvalued?

Australian sales: strong cash, weak growth

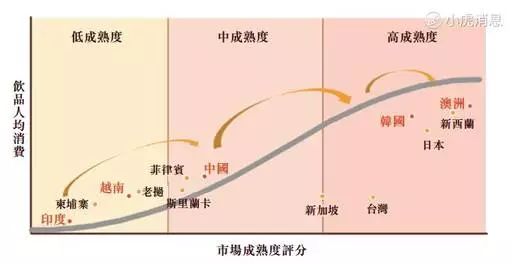

The West Asia Pacific region includes China, India, Vietnam, etc., while the East Asia Pacific region includes South Korea, Japan, New Zealand and Australia. When the Australian business is sold, it does not count towards the performance of the eastern Asia Pacific region. Among them, Australia is a region with a high maturity.

According to the second edition of the prospectus, in 2017 and 2018, the total revenue of Budweiser Asia Pacific except Australia was 6.1 billion and 6.74 billion US dollars, up 10.5% year-on-year, and the endogenous growth after removing the influence of currency was 7.4%. . In contrast, the total business income of Australia during the same period was 1.69 billion and 1.72 billion US dollars, a year-on-year increase of only 1.7%, far from the overall average. According to the company’s endogenous growth rate in the eastern Asia-Pacific region, it was 4.6% when it was removed from Australia, and only 2.9% when it was included.

The exchange rate of the Australian dollar against the US dollar fell in 2018, but from the year-on-year data of Q1 in 2018 and Q1 in 2019, the endogenous income of Australia’s eastern AsiaThe growth rate is 1%, which is 8.6% when it is not included, which is a far cry. In dollar terms, the Australian region has fallen by 10% this year.

In addition, from the point of view of sales, Australia’s sales in 2008 were 800 million liters, accounting for 7.8% of Budweiser Asia Pacific, with a year-on-year increase of zero. In the same period, the overall sales volume outside Australia was 9.62 billion liters, a year-on-year increase of 2.2%.

Therefore, although the Australian region is important, it is a drag on both the sales volume and the growth of income.

Baiwei uses normalized EBITDA to compare profits. In 2018, the profit in the Asia-Pacific region was US$2.48 billion, up 12% year-on-year, and Australia’s profit was US$800 million, down 3.5% year-on-year. In 2019, the Australian region fell by 17.3% year-on-year, even though the impact of the 10% exchange rate was still unsatisfactory, while the profit growth in other parts of Asia reached 23%.

Although the profit growth in Australia is unremarkable, the profit margin is higher. In 2018, sales in Australia accounted for 8% of the entire Asia-Pacific region, with revenue accounting for 20% and profit at 29%. In other words, the more mature Budweiser Australia business has a higher liquidity. We can also see from the cash flow statement that the cash flow from Q1 business activities in 2019 was $90 million in the first prospectus and only $36 million in the second prospectus.

Balance sheet: half of goodwill is still halfway

Among Budweiser Asia Pacific’s previously considered high valuation factors, huge debt and high goodwill are among the most worrying parts of investors.

In the first prospectus, goodwill was as high as $13.2 billion, accounting for 51% of total assets, and intangible assets were also $4.4 billion, accounting for 17% of total assets. The sum of the two accounts for more than two-thirds. . The goodwill after the update of this prospectus only marks 6.7 billion US dollars, nearly waist, intangible assets 1.7 billion US dollars, bothAccounted for 52% of total assets. Although this has somewhat reduced investor concerns about future goodwill and impairment of intangible assets, it is still relatively high compared to other companies in the same industry.

The change in goodwill is obviously not all from the business of Australia. The management of the company also intends to reduce the risk of investors.

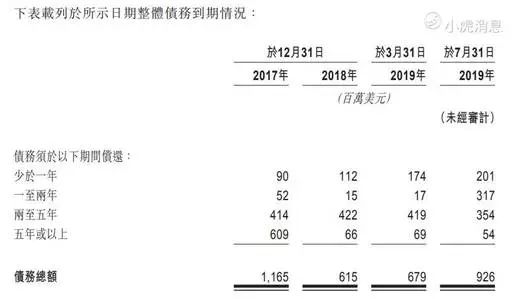

The current liabilities remain at $4.3 billion by the end of March 2019. According to the first prospectus, Budweiser Asia Pacific’s total debt at the end of May was US$2.63 billion, and it was US$930 million after the removal of Australian business at the end of July, which was related to the transfer of part of the debt of the Australian business. Because the debt due within one year is 200 million US dollars, according to the part of the new prospectus related transaction, Budweiser Asia Pacific will establish a “cash pool” and allow funds to be aggregated into the “cash pool” of Anheuser-Busch InBev, and “cash pool” All participants can withdraw funds from the pool or obtain overdraft loans.

In other words, the money raised by Budweiser Asia Pacific is mainly for blood transfusion to the parent company. By the way, the parent company of Budweiser Asia Pacific, Budweiser InBev, had net debt of $102.84 billion as of 2018.

Is there any dilution of shareholders’ equity?

Company CEO explained the rare adjustment of the Hong Kong stock IPO. It said that 465 million shares could be issued according to market subscriptions, that is, more than HK$14 billion, and the additional issuance will not dilute investors’ shares.

A closer look at the total number of shares after the issuance is 13.24 billion shares, of which 1.26 billion shares are the starting point for public offerings (selling may fail to sell), 7.5 billion shares are already issued, and 23 million shares It is the trustee of the capitalization issue, and the remaining 4.42 billion shares are issued to the parent company that transfers the Korean business.

If the subscription is 460 million shares, then the issuance to the parent company will be less than this part, the public shareholder accounted for 13.3%, while the parent company accounted for 86.