History is a mirror, let us see more clearly.

Editor’s note: This article is from WeChat public account “10 billion research institute” (ID: yibaiyiyanjiusuo) .

In 2018, the US GDP was about 18 trillion US dollars, about 1.5 times that of China. However, China’s consumption accounts for more than one-third of GDP, up to 44.32%, 1.5 times that of the United States. In 2018, the important data of China’s total social retail sales reached 3.8 billion yuan, which is only a little worse than the US data. 2019 China is expected to exceed 40 trillion, which is likely to exceed the United States.

A decade ago, this figure was only a quarter of the United States.

Of course, given the current international situation, the disposable income of urban and rural residents has steadily increased, and the government’s support for consumption has increased. What kind of growth path will China’s consumption take in the future, and how will the consumption structure change? Contrast the growth curve of American consumption growth and the pattern of consumption structure change, with a view to guiding the future development direction of China’s consumption.

1,The total US personal consumption is on the rise, which is strong for the economy

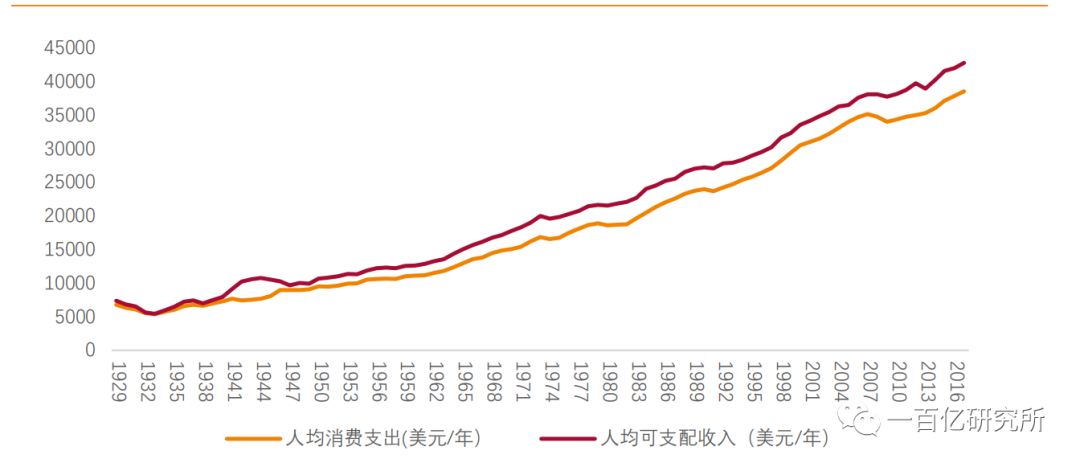

Overview of the history of consumption in the United States from 1929 to 2017. It can be seen that the total personal consumption of the United States after the removal of inflation has steadily increased. The growth rate in the past 40 years has basically stabilized below 6%. Consumer spending is more affected by macroeconomic factors such as the global economic crisis. During several severe economic crises, the growth rate is negative, but after the end of the economic crisis, the recovery rate is also faster, and there is very little negative growth for two consecutive years and above. Very strong.

In terms of per capita consumption expenditure, per capita consumption expenditure is highly correlated with per capita disposable income. The correlation coefficient between the two exceeds 0.9, showing that per capita disposable income is a very important determinant of consumer spending.

2,American historical experience:From mass consumption-Brand consumption-rational consumption, from product consumption-service consumption

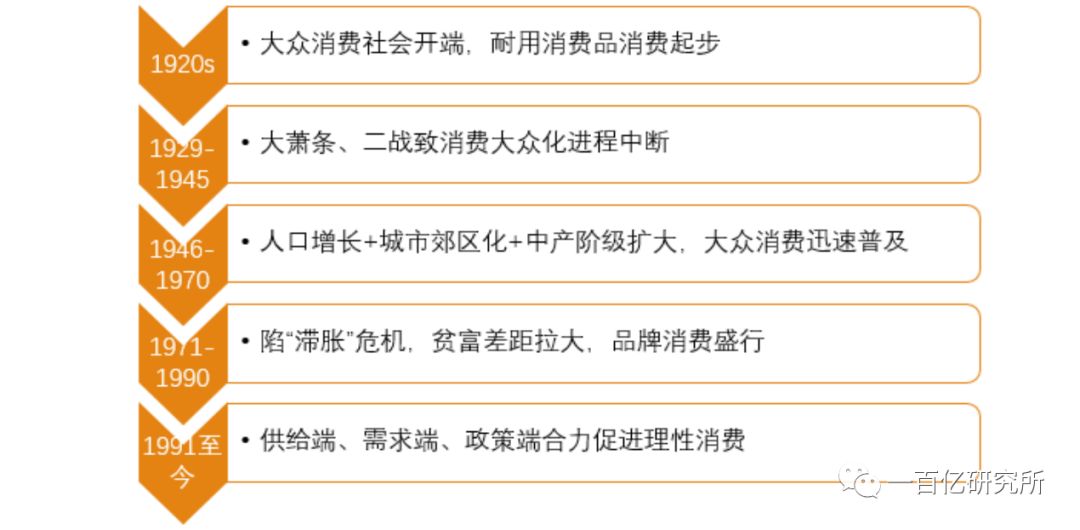

The history of consumption in the United States for nearly a hundred years can be roughly divided into the following stages:

American Consumer History-

1920S: The beginning of the mass consumer society, the beginning of consumer durables consumption1929-1945: The Great Depression and the disruption of consumer popularity in World War II1946-1970: Population growth + Suburbanization of the city + expansion of the middle-income class, rapid popularization of mass consumption1971-1990: Crisis of stagflation, widening gap between rich and poor, brand consumption prevails

From 1991 to the present: the supply side, the demand side, and the policy end together promote rational consumption.

The US consumer structure as a whole follows the development path of non-durable goods-durable goods-services, in line with Maslow’s hierarchy of needs. With the development of the economy and the improvement of people’s living standards, the basic needs of food, clothing and other basic needs have been met, and the consumption of durable goods such as automobiles, furniture and home appliances has begun to increase. Finally, the service consumption such as leisure and entertainment has increased to meet the high demand. Hierarchical hedonic needs. Current service consumption dominates consumer spending. In 2017, durable goods, non-durable goods, and service consumption expenditures accounted for 10.6%, 20.6%, and 68.8%, respectively.

3,History of five stages of US consumption evolution

First stage1920S:The beginning of the mass consumer society, the beginning of consumer durables consumption

The 1920S was the most prosperous period of the US economy before World War II, and it was called “Ko Lizhi Prosperity.”

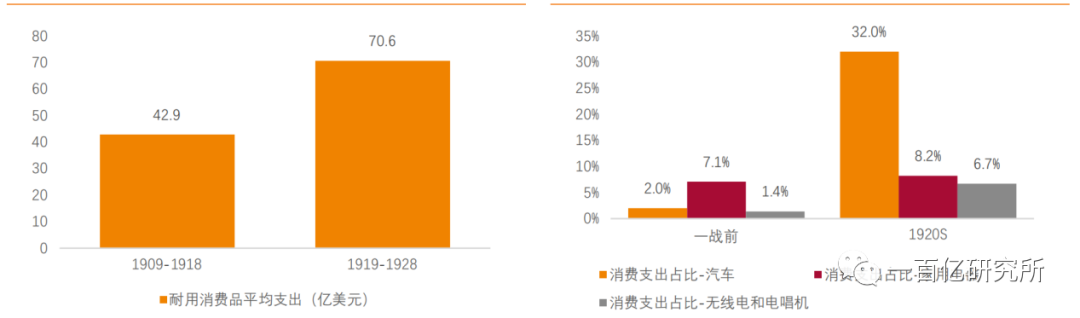

In this period, benefiting from the substantial increase in productivity, the consumer goods industry economy has prospered unprecedentedly, and the types and quantities of consumer goods available are gradually enriched. At the same time, the increase in per capita disposable income and the establishment of a consumer credit system have led to a significant increase in American spending power.

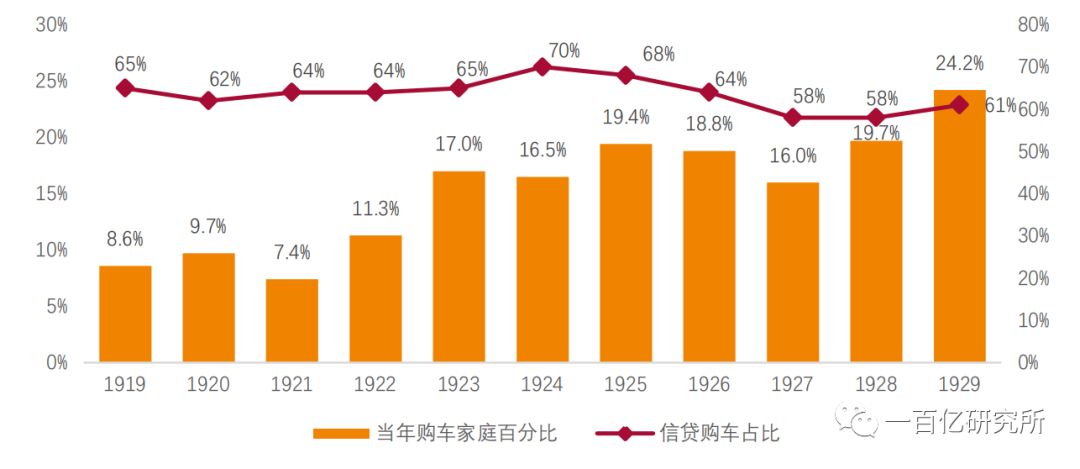

In 1913, the first car mortgage loan company was established to provide auto consumption credit to the general public. Buying a car is no longer a patent of the wealthy class, consumers pay only one quarter of the advance payment, and the rest Partial payment can be made.

The development of consumer credit has prompted more and more car consumption to take place in the form of installments. Credit purchases account for more than half of the total. After that, consumer credit has been gradually extended to radios, washing machines, jewelry, clothing and other commodities.

China’s auto consumption loan first started in 2005. This stage is also the burgeoning period of China’s consumer finance. It is mainly for high-income and high-net-worth individuals. The review is strict, mainly involved. Products are credit cards, car loans, and so on.

The car consumption cycle in China rose in 2008, and the China Mobile Internet cycle broke out in 2012. Since the superposition of car consumption and mobile Internet cycles, plus the multiplication of consumer finance, it has begun three stages! Until 2015, with the popularity of P2P online lending, new players such as financial leasing rose rapidly and the auto finance landscape was reshaped. In 2016, there was also a pattern in which the Internet’s 10% down payment was more than a car.

Industrial economic development has increased the types and quantity of consumer goods available, and “income increase” + “consumer credit” has driven up purchasing power. “Can buy” + “capable to buy” jointly promoted the consumption boom of durable consumer goods, automobiles, The consumption of durable goods such as radios and household appliances has soared.

For the first time in the history of the United States, there was a wave of non-productive and non-essential consumer goods consumption. The revolution in durable goods consumption was regarded as the beginning of the formation of the American consumer society.

Second Phase 1929-1945:The Great Depression and the Disruption of Consumer Popularization in World War II

This stage is divided into two periods –

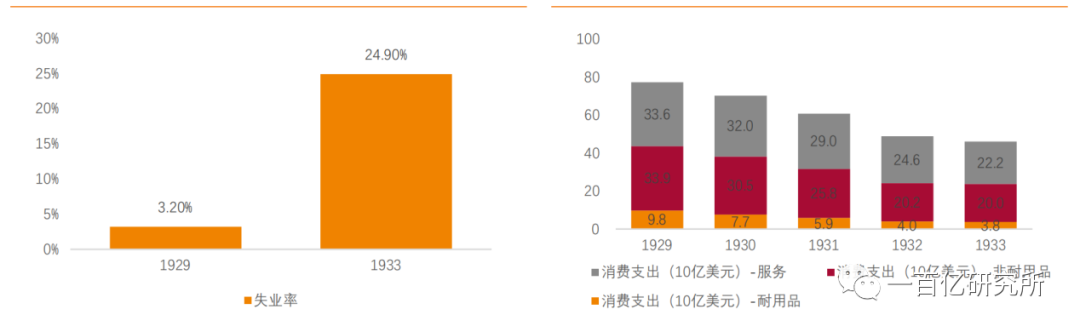

B1:The first period of 1929-1938, The period of the Great Depression, the credit contraction + unemployment rate soared to 10 years of consumption basically stagnated.

1929-1933 was the Great Depression. The tightening of monetary policy in 1929 caused the stock market to plunge, the bank broke out of bankruptcy, and the credit contracted. The reduction in consumer credit has led to a sharp drop in consumer demand, especially for consumer durables, and a corresponding decrease in total supply-side output. The factory has experienced a “reduction of layoffs” and the unemployment rate soared from 3.2% in 1929 to 24.9% in 1933. The decline in disposable income has further reduced consumer demand and created a vicious circle.

In 1929-1933, the total consumption declined significantly, with a negative growth for four consecutive years. It was the most serious and longest-lasting recession in the history of consumption in the United States in the past 100 years.

In 1934, consumption began to pick up, and it was only in 1936 that it recovered to the level of consumption before the Great Depression.

B2:The second period 1939-1945,World War II

World War II has less impact on US consumption. At the beginning of the Second World War, the United States did not participate in the war. The arms trade led the United States out of the shadow of the Great Depression to a certain extent. The total consumption expenditure in 1939-1941 increased for three consecutive years. In December 1941, it officially participated in World War II. In 1942, the total consumption suffered a certain impact, down 2.4% year-on-year, and resumed positive growth again in 1943-1945.

During the Second World War, the United States implemented three consumer credit controls, the durable goods consumption revolution that emerged from the 1920s, and by 1940s, by reducing the purchase of durable consumer goods, the role is to ensure the supply of military production materials, while curbing inflation.

After the war, in order to quickly restore and develop the economy, the US government relaxed restrictions on consumer credit, and consumer credit gained faster.

In the 1960s, banks rushed to issue credit cards in order to compete for customer resources, but limited to the credit system has not been established, fraud is frequent. The urgent need of financial institutions to identify consumer information has promoted the development of the credit reporting industry. By the end of the 60s, the total number of credit reporting companies in the United States reached 2,200.

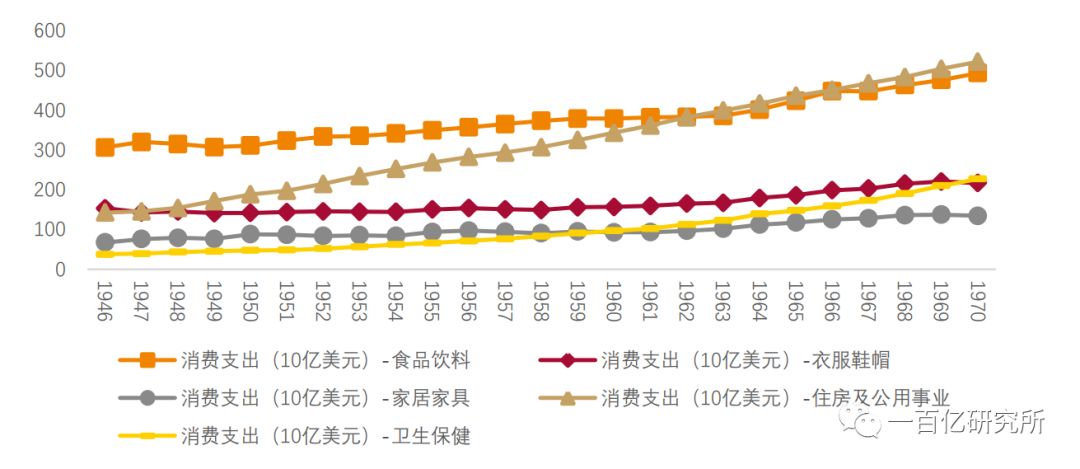

The third phase of 1946-1970:Population growth + suburbanization of the city + expansion of the middle-income class, rapid popularization of mass consumption

During this period, the United States experienced a long-term post-war boom, per capita income levels rose, and total consumption rose rapidly. Even during the first world economic crisis after World War II in 1957-58, the total consumption remained. With a small increase, the driving factors behind this consumption recovery are mainly the following two points:

First, “baby boom” has spawned a number of needs for housing, food, clothing, education, and medical care.

The long-term economic prosperity and improved health conditions in the post-war period have led to an increase in fertility rates and a decline in mortality in the United States, and the opening of the baby boom era of 1946-1964.

According to the census, the population of the United States reached 179 million in 1960, an increase of more than 47 million from 1940, and the proportion of children aged 0-13 was 29.5%. “Baby boom” directly stimulates the consumption needs of housing, home furniture, diapers, baby food, clothing, toys and other necessities, as well as educational resources such as school buildings, books, teachers, medical resources such as medicines and vaccines.

Second, urbanization shifts to suburbanization, promoting the spread of business and services to the suburbs, narrowing the gap between urban and rural areas, and expanding the middle-income class.

After industrialization, manufacturing and service industries have gathered to cities on a large scale. Urban congestion and industrial pollution have made cities less livable. After World War II, a series of technological and transportation revolutions made it possible for industries to spread from cities to suburbs. In addition, the government promoted the suburbanization process in a timely manner. The industry did not need to be confined to cities. Factory owners began to build factories in the suburbs or move factories to the suburbs. At the same time, the middle-income class, wealthy blue-collar workers began to migrate from the city to the suburbs on a large scale, looking for a more livable living environment.

1940-1970In the year, the suburban population surged by 275%, while the urban population grew by only 50%. As the factories and wealthy people migrated to the suburbs, the business and service industries began to expand to the suburbs, and the number of commercial areas and shopping centers increased significantly.

In the mid-1950s, there were only dozens of shopping centers in the United States, 4,500 in 1960, and more than 8,000 in 1970.

In addition to shopping centers, entertainment facilities such as cinemas, restaurants, clubs, and sports fields are also rapidly developing in the suburbs.

As the advancement of science and technology and the improvement of mechanization, rural productivity has been improved, which has boosted the income level of rural residents. At the same time, the rise of industry, commerce, leisure and entertainment industry under suburbanization has brought a large number of jobs to the countryside. The boundary between rural and urban areas has gradually blurred, and the number of middle-income groups has continued to grow.

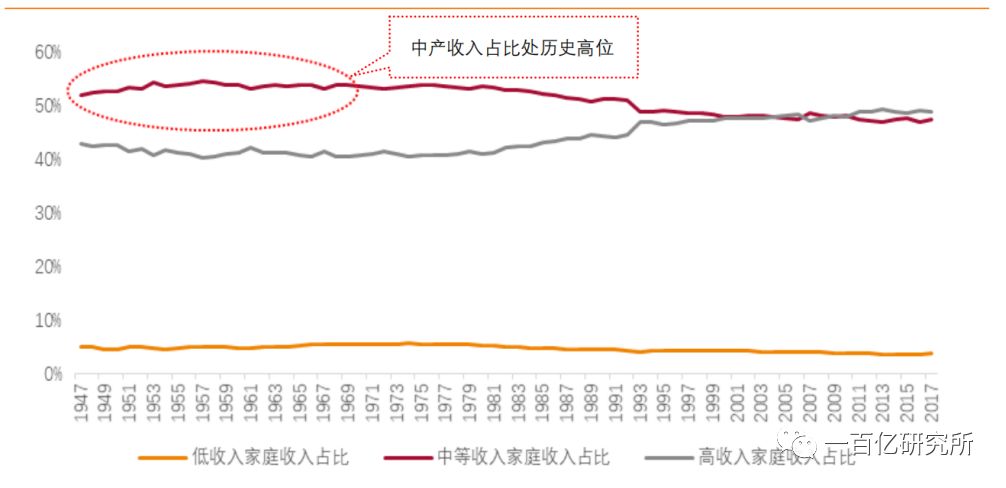

In 1946-1970, the social wealth of middle-income groups reached the highest level since the war., the level of household consumption has generally improved.

1946-1970, in Driven by the expansion of the above-mentioned consumer base and the general improvement of household consumption levels, coupled with the strong yearning for a better life after the war, The United States has experienced a long period of mass consumption boom, and the total amount of personal consumption expenditure has increased. 3.8% faster (excluding inflation).

The fourth stage 1971-1990:The “stagflation” crisis, the gap between the rich and the poor widened, and brand consumption prevailed

The productivity increase has slowed down, other economies have risen, and internal and external troubles have caused the United States to fall into a “stagflation” crisis. The rapid growth of consumer spending after the war has squeezed savings and investment to a certain extent, and labor productivity growth has slowed down. In addition, countries such as Japan and Germany have gradually recovered from the impact of World War II, and the international competitiveness of the United States is facing challenges.

The United States in the 1970s began to fall into a “stagflation” crisis of low GDP growth, high unemployment, and high prices. From 1971 to 1980, the actual compound GDP growth rate was only 2.9%, and the inflation rate was over 5% for a long time.

The rich are rich and the poor are poor and the gap between the rich and the poor is widening.

The development of science and technology and the accumulation of capital have accelerated the concentration of wealth in the hands of capitalists who have mastered assets. The wage growth rate of workers in the 1970s and 1980s was significantly lower than that of corporate profits. In addition, in the context of high inflation, the wealthy class realizes asset preservation and even value-added by investing in gold, real estate, financial assets, and art.

According to “Over-consumed Americans”, the wealthy class purchased Lexus cars, Rolex watches, Montblanc pens, full-brand clothing and art collections at this stage. However, the means of achieving asset appreciation by the poor and middle-income classes is extremely limited. Social wealth is further concentrated in the wealthy class, and the gap between the rich and the poor is widening.

Between 1979 and 1989, the average annual income of 1% of American households increased from $280,000 to $525,000. At the same time, from 1979 to 1991, the proportion of the population below the poverty line rose from 11.7% to 14.2%.

The high-income class has set off a wave of “Yuppie” consumption, and brand consumption is prevalent:

“Yuppie” is the name for the highly educated, high-income, self-motivated younger group in the 1980s. This group is aged 20-40 years old and has received higher education. After graduation, he is engaged in corporate management, scientific and technological research and development, college teachers, doctors, lawyers, etc., with an annual income of more than 50,000 US dollars.

The yuppie dress, consumer behavior and lifestyle have distinctive group characteristics: wine in high-end restaurants, brand-name clothing, top-quality cosmetics, luxury cars, and the pursuit of clothing, food and accommodation. Brand and quality. “Yuppie” advocates extravagant consumption, pays attention to famous brands rather than paying attention to the practical value of goods, and consumes more to show their social status.

After the rich crowd, the “blue-collar upper” and “future yuppies” groups tend to imitate the consumption behavior of “Yuppie”. Although the “blue-collar upper-level” in the high-tech field may not be highly educated, due to the shortage of manpower in the high-tech field, the income level is only slightly lower than that of “Yuppie” (annual income of 45,000 US dollars), and there are also consumption of high-end residential, luxury cars, jewellery. The strength of high-end products.

But the “future yuppies” and yuppies are also highly educated. For professional reasons, the income is far less than that of “Yuppie” (annual income of $2.2-2.4 million), but they have the desire to appreciate the same way of life. This consumer demand is met through consumer credit.

In the third phase of the 1940s-60s, the US government strongly encouraged consumer credit, especially for non-durable consumer goods, while a large number of institutions were able to flood into the consumer finance market, resulting in a significant increase in market competition, and many consumer financial institutions to expand Market share has expanded its outreach services. And toIn the fourth phase of 1970s-90s, in order to prevent excessive competition in the financial industry, the United States imposed restrictions on consumer credit interest rates, resulting in a differentiation in the pattern of consumer credit markets:

Commercial banks mainly serve high Credit customers provide high-value credit products, but commercial banks are still the market-leading institutions, with a share of around 50%; consumer finance companies provide small, high-frequency consumer credit services for low- and middle-income people, ranking second, with a share 20%; large retailers, oil companies through the establishment of non-financial institutions to issue credit cards to carry out the main business-based consumer credit business, reaching a maximum of 14.6% in 1978; savings banks and savings and loan associations are limited to the issuance of housing mortgage loans, the share of In 1985, it reached an all-time high of 9.4%.

At this time, the US personal credit reporting industry also began a wave of mergers. About 2,250 credit reporting agencies experienced a major reshuffle, eventually forming two camps: Experian, Equifax and Transunion, the three giants of the credit company camp and 300 A camp consisting of a number of small credit bureaus.

Since the 1980s, the Big Three began to use the FICO scoring model extensively. The relevant database covered all credit activity records of all consumers in the United States in the 1980s, and released more than 1 billion credit reports every year. The advancement of information technology has greatly shortened the approval process for consumer credit, and the overall efficiency of consumer financial institutions has made a leap forward.

We see that this is the fourth stage of the United States in the 1971-1990s – the characteristics of the era of “Yuppie”, the so-called elite consumerism, brand consumption: consumption hedonism, advocating luxury consumption, paying attention to famous brands instead of Then care about the practical value of the goods. It is similar to the epitome of #消费升级# that happened in China today.

Social wealth is further concentrated in the wealthy class, the gap between the rich and the poor is widening, the Matthew effect appears, and the consumption concept led by the rich is transmitted to the incapable people through credit.

At the same time, with the consumption consumption industry microcosm of #消费升级#, China’s current consumer finance has been prospered from a short period of ten years to 2018, and our level of consumer finance is equivalent to the 1980 consumer finance technology and credit rating in the United States. . Sino-US consumer credit technology has a difference of 20 years!

Of course, China’s population structure is very different, and the level of consumption is large. The upgrade of part of our consumption upgrade, that is, the downgrade of consumption, will be carried out in the following.

The fifth stage from 1991 to the present:Supply, demand, and policy to promote rational consumption

The shift in US consumption from luxury brand consumption to rational consumption is mainly affected by the following three factors:

1. Supply side: The big brands pay too much attention to the price, the small brands improve the quality, and consumers begin to pay attention to the price/performance ratio.

The prevalence of brand consumption in the 1980s caused many brands to think that they could occupy the market for a long time by relying solely on brands. The price of branded goods continued to rise for a period of time, but the quality did not improve significantly.

In contrast, some small brands are more effective in terms of quality, and prices are more “approachable”. Consumers, especially price-sensitive consumers, are beginning to pay attention to price/performance ratios and shift to cost-effective small-brand products.

2. Demand side:The polarization between rich and poor leads to diversification of consumption, and the economic crisis teaches consumers to save.

The further widening of the gap between the rich and the poor makes consumption more diversified. Consumers no longer simply imitate the consumption behavior of others. High, medium and low income groups purchase goods and services according to their own consumption power, high and medium. Low-end consumption is all the same.

The subprime mortgage crisis in 2007-2009 has had a profound impact on the United States. Consumers have begun to change consumer thinking, reduce unnecessary consumption, and appropriately increase savings to cope with future uncertainties. Since 2009, the US household savings rate has rebounded significantly.

3. Policy:Policy guides consumers to rational consumption.

1Encourage energy saving and reduce extravagant waste consumption.

The luxury consumption model caused a lot of land and resources in the United States. The government began to introduce policies to encourage consumers to purchase energy-efficient buildings, automobiles, and home appliances. For example, in 2001, tax relief policies were implemented for new energy-efficient homes and high-efficiency construction equipment.

2 Punishment relies excessively on consumer credit behavior to promote the healthy development of the consumer credit market.

As in 2005, the US government made major changes to the Bankruptcy Law through the Prohibition of Bankruptcy Abuse Act and the Consumer Protection Act, canceling the “Super Relief” clause in Chapter 13, and disallowing credit card loans. The amount of bankruptcy relief is raised. The reform of the Bankruptcy Law aims to curb excessive irrational consumption and reduce the risk of consumer credit markets.

According to the typical survey data provided by the central bank’s cargo administration department, the 1 yuan consumer credit can stimulate the consumption demand of 1.5 yuan. Concomitant with the increase in consumption growth rate of GDP, China’s consumer credit balance increased year-on-year. In 2011, the balance of China’s consumer credit was 8.9 trillion yuan. In 2018, this figure has reached 37.79 trillion yuan.

At the same time comparing the US optimization of bankruptcy law in 2005 – prohibiting credit card loans from being included in bankruptcy, while China, only 19 years ago, only the enterprise bankruptcy law, the National Development and Reform Commission, the mostThe High People’s Court and other 13 ministries and commissions issued the “Promoting the Improvement of the Market Main Body Exit System Reform Plan” (hereinafter referred to as the “Reform Plan”), proposing “step by step to establish a natural person bankruptcy system” and complementing the “half” bankruptcy law.

4,What is the consumption upgrade that China has and the US does not have?

China’s consumption upgrades accompanied the development of Internet e-commerce and self-media in just 10 years, entering the era of coexistence of brand consumption and rational consumption, while crossing the characteristics of the two eras of the United States.

Since the Taobao e-commerce has laid the online consumption habits of Chinese users, China’s consumption upgrade is basically accompanied by the development of the user community and self-media. The rise of the first batch of cross-border e-commerce companies such as Haitao and Yangduo led the rise of the UGC community from #什么意思# to #小红书#, they took over the pure e-commerce of Mushroom Street, Beauty and so on. The baton has become a hot platform in the field of content diversion. It is grown by the cultivation, interaction and anti-feeding of overseas advanced products.

It can be said that the small red book born in 2013 has brought about the emergence of the wave of China’s elite consumption upgrade wave since 2015.

The financial deleveraging crisis of 2018, the black cloud of economic downturn, the phenomenon of #consumer grading# appeared. This part of the US has a very similar stage of diversified consumption from 1991 to the present, and is similar to Japan until 1973. At that time, the Japanese economy experienced the first decline, and began to evolve into the era of “mature and simplified consumption”.

Not only that, the current consumption characteristics of China: all kinds of such people, rich and poor people pursuing elites and seemingly operating class consumption, make #雅皮士# consumer culture characteristics very common in China, that is, look good Also cost-effective is the distinctive feature of the latter. This feature combines the US 1971-1990s and 1991-present stages.

Thousands of users are pursuing luxury, while users with money and money have begun to pursue luxury and new domestic alternatives.

What is a new domestic alternative?

This is the enhancement and imitation of brand awareness by young Chinese designers. The awakening and imitation of Chinese brand owners on brand awareness have promoted the replacement of imported luxury goods by new designer brands. It is the 10 billion research institute that was put forward in 2017 #颜值时代资本论#, it is not the luxury goods that have killed the A goods, but the new domestic goods (good design with excellent prices) to kill the A goods market.

In the 1970s, when the United States was the rich were rich, the poor were poor, and the gap between the rich and the poor widened. The development of science and technology and the accumulation of capital accelerate the concentration of wealth in the hands of capitalists who hold assets. This phenomenon is a combination of China’s real estate that began in 2000 and the Matthew effect of the Internet giant in 2019.

5,From content e-commerce to KOL live delivery, the mobile Internet brings China’s consumption upgrade beyond the US and the rapid evolution of user sinking

As mentioned above, the wave of consumption upgrades caused by the first wave of content e-commerce in 2013 by Xiaohongshu is actually reflected in the verticalization of visualization and planting of product functions. Then, various brands and fashion content flocked from the media, the mainstream model covers:

Quality content media resellers (one, two more), KOL-based content from the media (Rebecca), and features IP (Uncle of the same road) is the main content theme media transfer (as for the three squirrels, the foundation of e-commerce is not a typical content media);

The above-mentioned self-media content e-commerce has experienced most of the ups and downs in the 2017-18 transfer experience after the two or three years of ups and downs,, where online content has a copy and short video The trading model has self-operated and purely loaded goods (not involving heavy supply chains).

At this time, the transaction is still separate from the content.

Beginning in 2016, the trend of content e-commerce has greatly promoted the contentization and socialization of mainstream e-commerce companies such as Taobao, Jingdong, and Jieduo, and closely promoted the KOL band of Taobao live broadcast which is in the limelight today. Goods mode.

In fact, in 2015, KOL live broadcasts gradually became popular. Among them, the most typical ones that were broadcasted by Taobao platform to the present are the enthusiasm behind Zhang Dazhao, the beauty behind Li Jiaqi, and the nuances behind Li Zikai. In 2018, Taobao live broadcast platform data growth rate of nearly 400% year-on-year, creating a brand-new incremental market, the e-commerce red people created a record of goods, such as Taobao anchor Wia 2 hours captured 267 million, fast hands Sanda Brother 1 day 160 million sales, seven-day brain five-hour 10 million sales and Li Jiaqi double eleven 320,000 goods, 67 million sales, etc. are stimulating the nerves of the brand owners.

In just three years, the transaction is integrated with the content media.

After the hot e-commerce in 2016, after the Spring Festival in 2017, the video was short-lived and became a strategic product.