Not only is the battlefield between e-commerce giants, but also an important test for express delivery giants.

Editor’s note: This article is from WeChat public account “US Stocks Research Institute” (ID: Meigushe), author of the US Stock Research Institute.

After more than a month, the “Double 11” of 2019 is coming again.

On September 27th, a mobilization meeting for the express company of Double 11 took the lead. The 2019 Double 11 Express Startup Conference hosted by China Express Association was held in Hangzhou. China’s 11 mainstream express companies officially launched the 2019 Tmall Double 11 Global Carnival Logistics Preparation with Tmall and Rookie. The courier giants have prepared for the Double 11, which has become an important critical point for their growth in this year’s express business.

Now the Double 11 is not only the battlefield between e-commerce giants, but also an important test between the express giants in this year. Double 11 test whether the express giant can face the delivery of hundreds of millions of express orders in a short period of time, how to efficiently and high-quality delivery tasks, test their internal strength.

Before preparing for the double 11, the domestic express delivery industry has already set off a round of price wars, which also caused the net profit of Zhongtong, Yuantong, Yunda and Shentong to decline in the first half of this year, with the launch of SF and JD. Affordable mail service, the price war between the express giants will continue. Grab the order of the express mail, grab the market share, and the competition between the express giants is becoming more and more fierce. Who can stand out in the competition in the future?

Prepare for the double 11 to kick off the competition

For express delivery giants, the logistics orders generated by Double 11 became one of the most important sources of revenue for their year. Last year, Tmall “Double 11” hit a turnover of 213.5 billion yuan, and all-day logistics orders reached 1.042 billion. According to the data of the State Post Bureau, on November 11 last year, the major domestic e-commerce companies produced 1.352 billion express logistics orders. In 2018, China’s express delivery business volume was 50.71 billion pieces, and its business income was 603.84 billion yuan. According to institutional research, in 2018, e-commerce express delivery parts accounted for more than 80% of express delivery business volume.

From these data, this year’s double 11 logistics orders will achieve further breakthroughs, which is both an opportunity and a challenge for the express delivery giants, and the total proportion of express delivery business with e-commerce express parts. The rise of the express giants such as Santong Yida, SF Express, Jingdong Express, etc.How to get more express orders on the e-commerce giant platform in the future is crucial, which may determine their revenue growth.

At present, the domestic e-commerce industry has formed Ali, Jingdong, and the fight for more than one strong situation. For the express giants, the close cooperation with the e-commerce giants directly affects their ability to be allocated in the field of e-commerce express delivery. How many cakes. Ali has always had many layouts in the logistics industry. In addition to the rookie wrapped in this “pro-son”, it also has strategic investment and access to the five companies.

In March of this year, Ali entered the stock market with a share of 4.66 billion yuan. In July, he again obtained the right to purchase 31% of the shares of Shentong Express at a price of 9.982 billion yuan. If the purchase is successful, Alibaba will become the actual Shentong. Controller. Prior to this, Ali has been holding Baishi, and has entered the company of Yuantong and Zhongtong, and Yunda has long been a partner of rookie.

In addition, JD.com has Jingdong Logistics, which is an important weight for JD.com to establish its own advantages in the e-commerce field. According to the current development of Jingdong Logistics, in the second quarter, Jingdong also disclosed the break-even balance of Jingdong Logistics, in addition to breaking the various anxiety of Jingdong and Jingdong Logistics itself since the second half of 2018. In addition to the steady development of the first and second lines, Jingdong Logistics entered the third to sixth tier cities four years ago. At the beginning, the logistics cost is relatively high, because the competitiveness is relatively small, and with the gradual improvement of the layout in the low-line market, the performance fee rate is Gradually decreased (has dropped to 6.1%).

There are a lot of remaining spells that have become the object of courier giants vying for cooperation, especially in the past two years, the development speed is fast, the order business on the platform is rising, but what kind of cooperation form may be achieved. The focus is on consideration.

For SF, Ali and JD have their own investment and development of express delivery companies, which also makes SF in a certain disadvantage in e-commerce express delivery, especially SF itself in the express delivery industry to take a high-end positioning, its charging standard Still higher than the three links, in this case, SF’s advantage is constantly chased by other competitors, for SF, its situation is increasingly disadvantageous.

Although the three links and the behind-the-scenes have the strategic investment of Ali, the internal competition between these companies is fierce. It can be said that none of the current express delivery industries have an absolute competitive advantage. It is foreseeable that with the approach of the double 11, the competition of the express giants will be more intense.

Three-point world formation, head enterprise competitionfierce

After years of development, the domestic express delivery industry has basically formed a three-point world. The main factions are divided into: Ali (Tongda + Baishi), SF and non-Ali SF. According to the semi-annual reports issued by five domestic listed express delivery companies, such as SF, Shentong, Yuantong, Yunda and Debon, each family has its own problems.

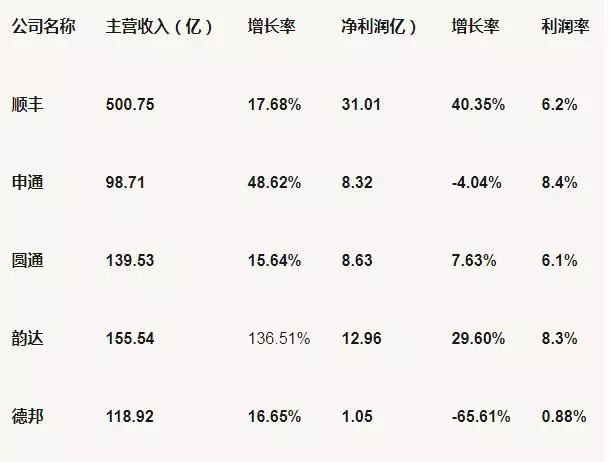

From the perspective of main business income, SF’s revenue is still the highest. The performance in the first half of the year was 50.075 billion yuan, and it successfully crossed the 5 million mark. The lowest Shentong was 9.871 billion yuan, and it still failed to pass the 10 billion mark. The five profit rankings were SF, Yunda, Yuantong, Debon and Shentong. The four main businesses were 51.2 billion yuan and SF, and Shentong was a little behind;

From the performance of the main revenue growth rate, Yunda ranked first with a growth rate of 163.51%. This growth rate surprised the outside world. Others were Shentong 48.62%, SF 17.68%, Debon 16.65%, and Yuantong 15.64%. Judging from the growth rate of these companies, although SF Express has the highest revenue, its business growth rate is not bright, which also shows that its competitiveness in the e-commerce field is not prominent enough.

From the perspective of net profit attributable to shareholders of listed companies, SF ranked first with 3.101 billion yuan, which grew rapidly. Others were rhyme up to 1.296 billion yuan, Yuantong 836 million yuan, Shentong 832 million yuan, and Debon 105 million yuan. .

From the revenue, net profit, and the development of the main business, several major express giants are facing great growth pressure. In addition to the listed, Jingdong Logistics is only turning losses into profit, for them to further Increasing revenue growth is particularly fierce in business competition. In the view of the US stock research institute, the points of competition among several express giants are mainly concentrated in the following aspects.

First, the price war is getting worse and worse, and the low price strategy is not conducive to improving profitability

In the express delivery industry, the price factor is an important data that affects the express giant’s revenue and net profit. In order to grab market share, the price war has become the most common strategy among express delivery giants.

Although the price can shake the business and users, but because the cost of a single piece of delivery is less than the decline in single-ticket revenue (single-piece express income), the express delivery giants also have a price reduction strategy affecting their performance. According to the Southwest Securities Research Report, in the first half of 2019, the revenues of Zhongtong, Yuantong, Yunda and Shentong Express were 1.74 yuan, 3.19 yuan, 3.3 yuan and 3.19 yuan respectively, down by 0.18 yuan, 0.38 yuan and 0.04 yuan respectively. 0.04 yuan. In the first half of this year, the performance of Zhongtong and Yuantong, which had a large decline in single-ticket income, was not satisfactory, and the net profit fell by 0.37% and 4.04%.

Before, SF Express did not show weakness in terms of price. As it ploughed into the business component market, it firmly occupied the mid-to-high-end e-commerce market. It is only the premise that the proportion of total express delivery is higher and higher in e-commerce express delivery.Next, SF also had to bow to the low-cost strategy to fight for e-commerce.

This year, SF has launched a special special product for e-commerce customers. Parcels are not transported by SF Air, but are slower than the time-dependent parts, but they are cheaper to charge. According to the August operating data disclosed by SF Express, SF’s business volume growth rate exceeded 30% in the current month, surpassing the industry average for the first time, driving the market share in August to increase by 0.5 percentage points. It is generally believed in the industry that the increase in SF’s business volume is not unrelated to the return to the e-commerce parcel market in May this year.

In fact, the low-cost strategy between the express giants is mainly aimed at the e-commerce market. After all, the e-commerce shipments are much more. If you can get more shipments, this can actually reduce the impact of the price reduction. In the future, the competition between the giants for e-commerce express shipments will only become more and more fierce, and this may become the biggest resistance to the monopoly of each family.

Second, the express giants are actively deploying new businesses and expanding horizontally to drive revenue growth

Although the various courier giants are mainly engaged in the development of the main business, after all, the competition for the courier parts in the e-commerce industry is fierce, and each family may only be able to share a piece of cake. It is difficult to see which one eats. In order to expand the new express delivery market, express delivery giants are actively developing new businesses and expanding new areas horizontally to enhance competitiveness. In recent years, the development of cold chain logistics has been rapid. As the blue ocean market of the logistics industry, some logistics industry giants have rushed to the shore and compete for profit.

The domestic fresh e-commerce market is developing rapidly. In 2018, the transaction volume of China’s fresh e-commerce market exceeded 200 billion yuan. IResearch expects that China’s fresh e-commerce industry will maintain an average annual growth rate of 35% in the next three years. rate. From the perspective of the market growth rate of fresh e-commerce, the future development space is worth imagining. The cold chain distribution link should be regarded as an important lifeline related to fresh e-commerce. For the express delivery giant, the layout of this field is also the most important.

Among them, SF and the American Xiahui Group set up a new Xiahui, the sword refers to the top spot of cold chain logistics, and the cold chain transportation network of Jingdong cold chain storage, cold chain card class and cold chain city with “three in one” has been covered. In dozens of cities, the development is fast. At present, other listed express delivery companies are cutting into this market. Cold chain logistics is more important for express delivery giants to consider their internal strength. It is likely that this area will also set off a new round of market robbing.

The growth of orders in first- and second-tier cities is becoming saturated, and express giants are exploring new growth points

According to the data of Zhiyan Consulting, the proportion of e-commerce components in 2016 reached 72%, nearly 10 years CAGR≈60%, non-e-commerce express CAGR≈29%. With the hardening of the market in the past two years, the rise of the fight has significantly increased the volume of express delivery in low-tier cities. In 2018, the proportion of e-commerce components in express delivery has exceeded 80%. At present, the e-commerce market in first- and second-tier cities tends to be saturated, and user growth has slowed down noticeably. In fact, for the express delivery giants, their business has also experienced a period of rapid growth in first- and second-tier cities. In the future, if they want to further expand their competitiveness, they still need Discover new growth points.

In the view of the US stock research society, the express delivery giants must also dare to explore new markets. After all, they only have to take the lead in better than other competitors, and they will not be overtaken by the other side. E-commerce and real-time logistics are likely to bring new growth momentum to the express delivery giants.

As e-commerce giants turn their business focus to the sinking market, this battlefield will also become an important market for express delivery giants to snatch. Strive to seize the opportunity of the sinking of the consumer market to develop rapidly. In 2018, the number of active buyers on the platform was 419 million, an increase of 174 million from 2017, an increase of 71%, and the GMV was 471.6 billion yuan, a growth rate of 233%, far exceeding the average of the e-commerce industry. Speed up. A lot of high-speed growth, this is actually a good signal for the express delivery giants, keeping up with the e-commerce giant’s footsteps at least will not fall behind.

At present, the market development speed of cross-border e-commerce is also very fast. The development of cross-border e-commerce has driven the further regulation of the logistics industry to a certain extent, the integration of warehouse integration, online expansion and the integration of omni-channel supply chain. This has enabled many logistics service providers to continuously research and develop in intelligence and digitalization, which will test the technical strength of the express delivery giant. Most people in the industry think about the status quo of cross-border e-commerce, focusing on the supply and circulation of goods, but in fact, the logistics link is also crucial for cross-border e-commerce. For express delivery giants, how to establish their own advantages in the field is crucial.

In the past two years, with the continuous development of the lazy economy, instant distribution has become the fastest growing sub-sector in the logistics field. From the outside to the cut, gradually expand to the fresh, flower cake, pharmaceutical distribution and the errands business of the agent, instant delivery continues to expand the service scene. More and more courier giants are launching real-time logistics services, which is actually driven by market demand. The real-time distribution is about efficiency and service. For the express giants, how to establish their own advantages in efficiency still needs to be done in all aspects. it is good.

At the moment, the double 11 is approaching. This is an important assessment for the express delivery giant. It will not only examine the efficiency and speed of their delivery services, but the most important thing is how high they can produce in this important period. This will also be an important case for them to show off their strengths. Although the current price war will continue, but the follow-up to a certain extent, with the market share of the express giants further increased, after the right to speak, their advantage in bargaining will also be highlighted, the future domestic express industry may still Will maintain a few strong hegemonyIn the short-term situation, it is difficult for each family to open up a large competition gap.