There are still 460 million natural people in China who do not have credit records.

Editor’s note: This article is from WeChat public account Think tank” (ID: laikazk), author G3007.

In recent years, China’s consumer finance has grown rapidly, and its credit structure has been optimized. It has formed a multi-layered approach to different groups based on commercial banks, licensed consumer finance companies and Internet financial platforms. Consumer financial services system.

The rapid development of the consumer finance industry has created new risks and problems while meeting consumer financial needs and promoting consumption upgrades.

Specifically, it mainly includes the following four questions:

“ First, the structural imbalance in the consumer finance sector still exists. The overall coverage of consumer finance in China is much lower than that in developed countries, and the coverage of long-tail customers is still insufficient;

Second, the credit model of traditional commercial banks restricts the development of consumer finance due to the high credit cost and lack of credit;

Third, due to imperfect credit information system and increased competition, the long-term credit problem still exists; and in recent years, the phenomenon of consumer financial violations moving to the housing market and other investment channels is more prominent;

Fourth, consumer protection needs to be strengthened. ”

In response, the National Financial and Development Laboratory issued the “2019 China Consumer Finance Development Report” (hereinafter referred to as the “Report”), on the current status of China’s consumer finance development, the value of social development and future development. Detailed analysis.

The Status Quo of China’s Consumer Finance Development

Consumer finance, or consumer credit, refers to a form of credit that is provided by commercial banks, consumer finance companies, Internet platforms and other institutions to provide consumers with funds to meet consumer demand.

China’s consumer finance business started with the durable goods consumer credit business and credit card business started by commercial banks in China in the 1980s. It was not until the launch of the pilot of the consumer finance company in 2009 that the support for the consumer finance industry was clearly defined from a policy perspective.

At present, China eliminatesThere are three main types of participants in Fei Finance: commercial banks, licensed consumer finance companies and internet finance platforms. In terms of scale, banks are still the mainstay of consumer finance stocks, but the three major players have their own characteristics and their corresponding advantages and disadvantages.

Commercial Bank is the earliest institution providing consumer finance in China. Its product categories include housing mortgage loans, auto loans, durable goods loans, travel loans, student loans, credit cards, consumer credit loans, etc. Most of the personal consumer finance comes from bank loans.

Among them, credit cards and consumer loans are important points of bank consumer finance. Bank consumer finance is mostly dominated by urban white-collar customers, and some banks have begun to try to grant credit to families.

Under the market competition, the bank’s consumer financial product system is rapidly enriched, and many emerging consumer financial products continue to emerge. Such as lightning loan, new one loan, Xing flash loan and so on.

Consumer Finance Company is a non-bank financial company approved by the Banking Regulatory Commission to provide loans for consumption purposes for individuals in China who do not absorb public deposits on a small and decentralized basis. mechanism.

The market positioning of consumer finance companies complements commercial banks, targeting low- and middle-income and emerging customer segments, providing financial services by offering broad and flexible credit products, extensive regional coverage and fast markets.

The current consumer finance company business model can be divided into three categories. The first category is based on offline channels, such as Jincheng Consumer Finance, Gitzo Consumer Finance, etc.; one category focuses on O2O models, such as Haier Consumer Finance, Suning Consumer Finance, and China Post Consumer Finance; and another category that positions itself as the Internet. Financial companies, such as Zhaolian Consumer Finance, Immediate Consumption Finance, etc.

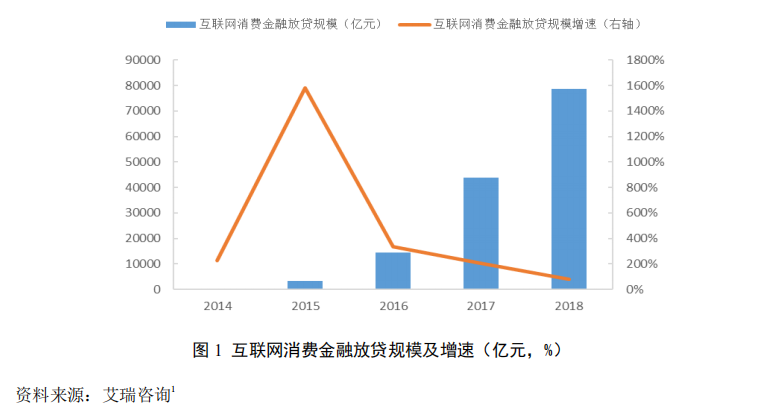

The active participation of Internet finance is a very significant feature in the development of China’s consumer finance. Relevant data show that from 0.02 trillion in 2014 to 7.8 trillion in 2018, the scale of Internet consumer finance lending has increased by nearly 400 times.

According to the statistics of 2017, the banking industry accounted for 12% of the standard. After removing the Internet loans from the banking industry, the scale of Internet consumer finance lending in 2017 and 2018 still reached 3.9 and 6.9 trillion. The scale should not be underestimated. .

Compared with commercial banks and licensed consumer finance companies, the Internet platform is mainly targeted at young people under the age of 35 and consumer groups in specific scenarios (such as small-scale consumption, shopping, travel, etc.), including a large number of Whitelist groups that do not have credit behavior, and the amount of a single loan should be smaller to meet the high-frequency, small-value inclusive financial needs.

Consumer Finance and Economic Structure Upgrade

Whether based on policy theory or international experience analysis, consumer finance plays a very important role in the process of economic transformation in a country, and it is no exception in the process of economic restructuring and upgrading in China.

From the report, the value of China’s consumer finance development is mainly reflected in the following aspects:

Expanding domestic demand and driving consumption

Expanding domestic demand includes expanding investment demand and expanding consumer demand. In the context of high corporate leverage, expanding investment demand is increasingly constrained, and expanding consumer demand is promising.

The development experience of developed countries shows that as the economy of a country is maturing, the increase in the quantity and quality of household consumption will become an important driving force for economic growth and structural upgrading. The contribution of household consumption to the GDP of the world’s major economies has been more than 50% for a long time, and the United States is close to 70%.

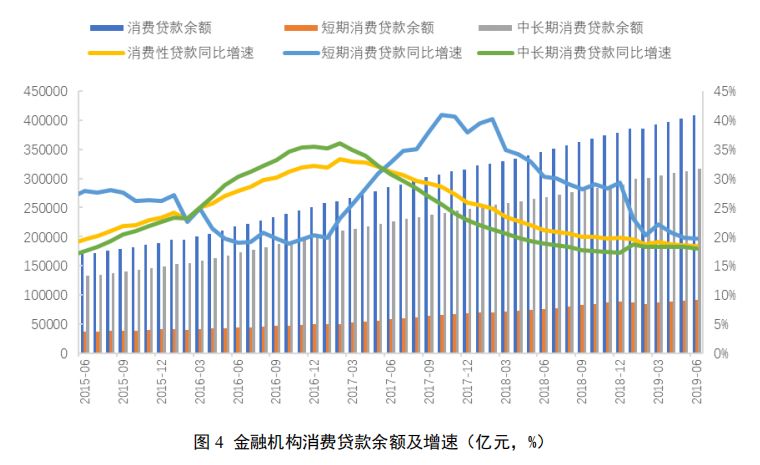

The report shows that moderate development of consumer finance can help drive consumption growth. In recent years, the scale of China’s consumer loans has grown rapidly. According to the data of the People’s Bank of China, the balance of China’s consumer loans increased from 15.7 trillion yuan in early 2015 to 40.8 trillion yuan in September 2019, an increase of 159.9%.

Evidence data shows that consumer finance and per capita consumption show a significant positive correlation. It can be seen that the development of consumer finance can effectively promote consumption growth, while stimulating domestic demand and stable growth, significantly optimizing the aggregate demand structure.

Promoting consumption upgrades and driving industrial restructuring

For consumers, consumer finance can increase its current available funds, so that its liquidity constraints can be alleviated, thereby promoting consumers to increase consumption.

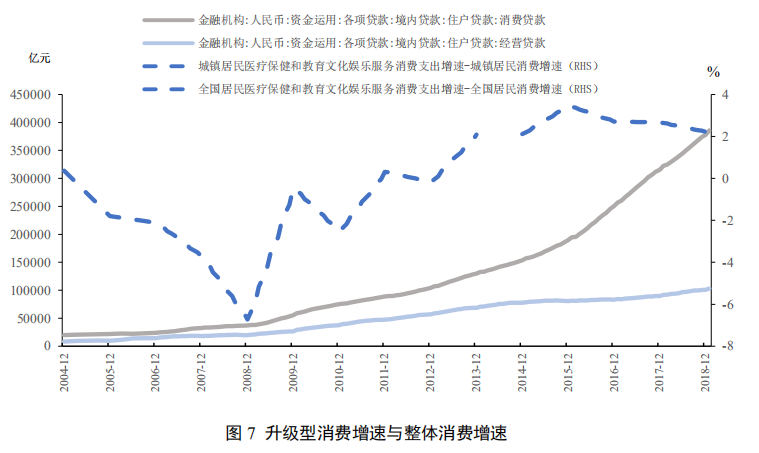

From the actual situation in China, relevant data shows that consumer finance has not only increased consumers’ consumption of durable consumer goods, but has also begun to expand into areas of personal growth and self-improvement in recent years, with health, pension, education, The scale of consumer finance related to “non-traditional” goods such as tourism continues to expand.

The report shows that in the process of promoting consumption upgrade, consumer finance promotes the development of high value-added industries by increasing consumer demand for high value-added products, thereby further eliminating low-end backward production capacity and driving industry consolidation.Adjustment. Especially in the case of weak investment and import and export trade contribution to economic growth, promote the high-quality development of China’s economy and promote China’s industrial structure to move toward the middle and high-end.

Practicing inclusive finance to achieve shared development

With the rapid development of the financial industry, many institutions and individuals have obtained sufficient and even excessive financial services. However, there are still a large number of ordinary residents and vulnerable areas (such as small and micro enterprises, private enterprises and “three rural” areas) that are difficult to obtain effective and sufficient financial support, and some even face gaps in financial services.

The report stated that consumer finance is an important part of inclusive finance. On the one hand, consumer finance has provided strong support for stable economic growth by releasing the consumption power of the long-tailed group; on the other hand, it has greatly promoted consumer affirmation and put the concept of shared development into practice.

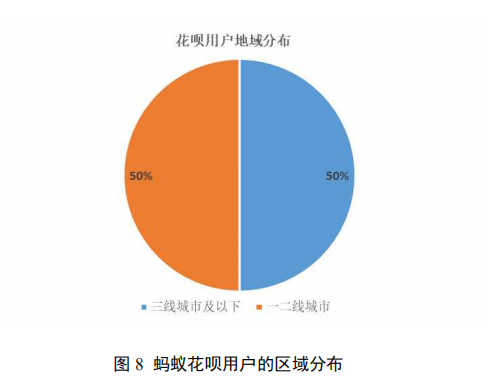

For example, since 2015, Ant Financial has launched two consumer financial products to hundreds of millions of users, namely flower gardens and borrowing, mainly serving China’s relatively insufficient consumer finance and lack of people. At present, the number of users in Huayan is over 100 million. In terms of consumer finance, Ant Financial Services and the commercial banks that mainly serve China’s 480 million credit record people form a complementary trend of hierarchical and dislocation development.

Building a credit information system and improving financial infrastructure

The central bank’s authoritative data shows that up to now, the People’s Bank of China Bank Credit Information System has collected 990 million people’s information. But this data also shows that there are still 460 million natural people in China who do not have a credit record.

The report shows that at present, the development of consumer finance, especially Internet consumer finance, relies on the advantages of the long tail group, using high-frequency, online transactions, using big data, cloud computing and other technologies to generate, precipitate and The personal finance and related data of many “credit white households” were stored, which fully filled the gap of credit information and improved the personal credit information system in China.

Conclusion

From the perspective of the overall development space of the industry, the report also predicts that China’s consumer finance industry will still have a high-speed growth period of more than five years as a whole, and the consumption finance in the table may exceed 25% of the total credit scale.

Although there are still such problems in the consumer finance industry, under the background of structural reforms on the financial supply side, the regulatory environment will become increasingly strict, and the operation of the entire consumer finance industry will become more and more standardized. In this process, the advantages of compliant consumer financial institutions will become more apparent, and their social value will also become larger and larger.