It is said that more than one-third of the investment institutions have already existed in name only. The money earned by luck in previous years has been lost due to the facts this year.

Editor’s note: This article is from WeChat public account “Sanyan Finance” (ID: sycaijing) , author DorAemon.

Time flies, the winter of 2019 is about to come.

There is a rumor in the industry today: It is said that more than one-third of the investment institutions have already existed in name only. The money earned by luck in previous years has been lost by this year.

There was an entrepreneur who revealed that when looking for investors, he was directly told by phone that “there are no money for the organization now”; and entrepreneurs said that this year is very difficult, the organization’s money is LP, and LP is very cautious. .

2019 Is it really difficult for investment institutions and investors? What is the number of financing events in 2019 and what has changed?

The arrival of capital winter: the amount of financing fell by 48% year-on-year in 2019, and the total financing fell 60% year-on-year

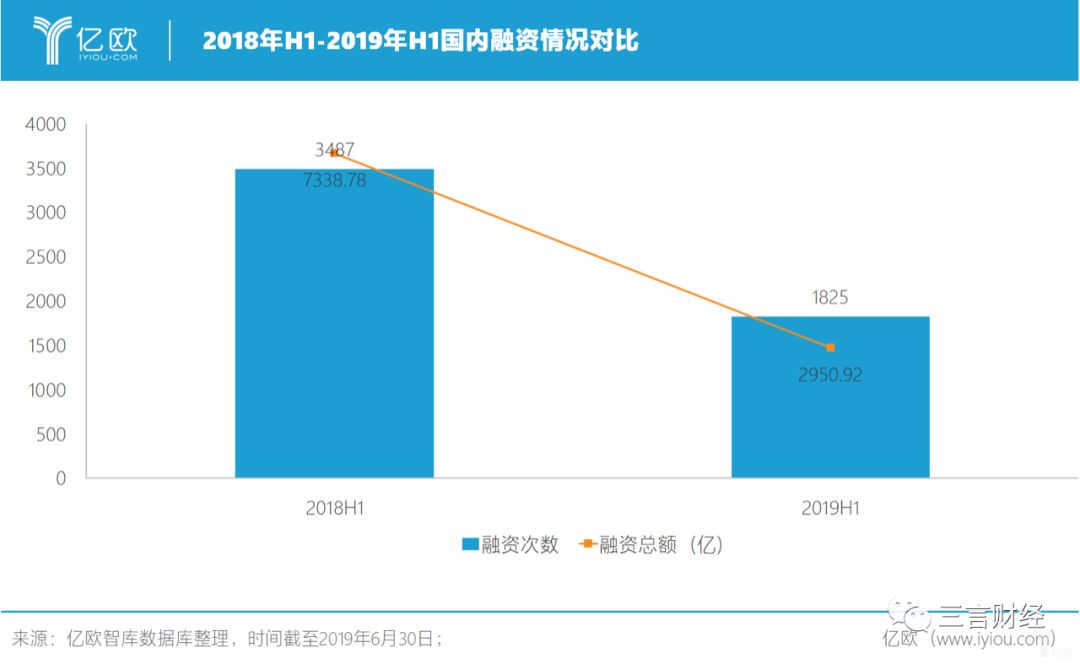

According to the “2019H1 China Venture Capital Report” issued by Yiou, the overall financing events and financing amount of the industry in 2019 both fell significantly.

As of June 30, 2019 In the first half of the year, a total of 1825 financing incidents occurred in the whole industry, and the total financing amounted to approximately 295.92 billion yuan. Compared with the same period of 2018, the amount of financing in the first half of 2019 decreased by 47.66% year-on-year; the total financing decreased by 59.79%.

The year-on-year decline is nearly half. This data is sufficient to show that the industry financing situation in 2019 is not optimistic.

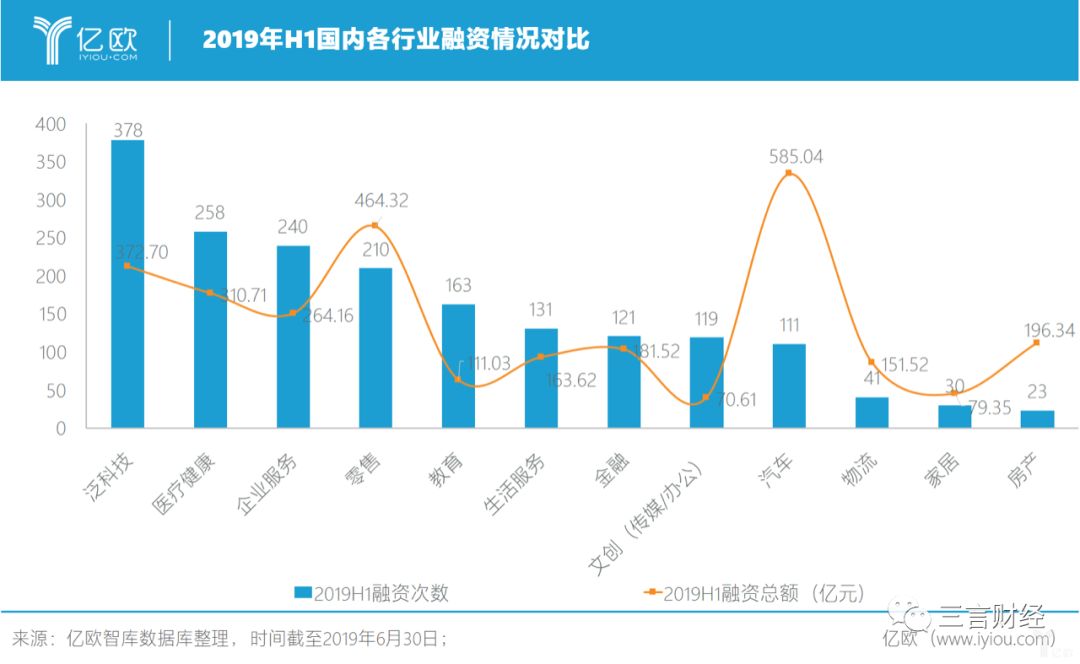

In the first half of 2019, the pan-technical sector maintained its leading position with 378 times, with a total financing of 37.27 billion yuan. In terms of total financing, the total financing of the auto industry in the first half of 2019 ranked first, about 58.504 billion yuan. However, compared to the same period in 2018, these two numbersAccording to both, it has fallen sharply.

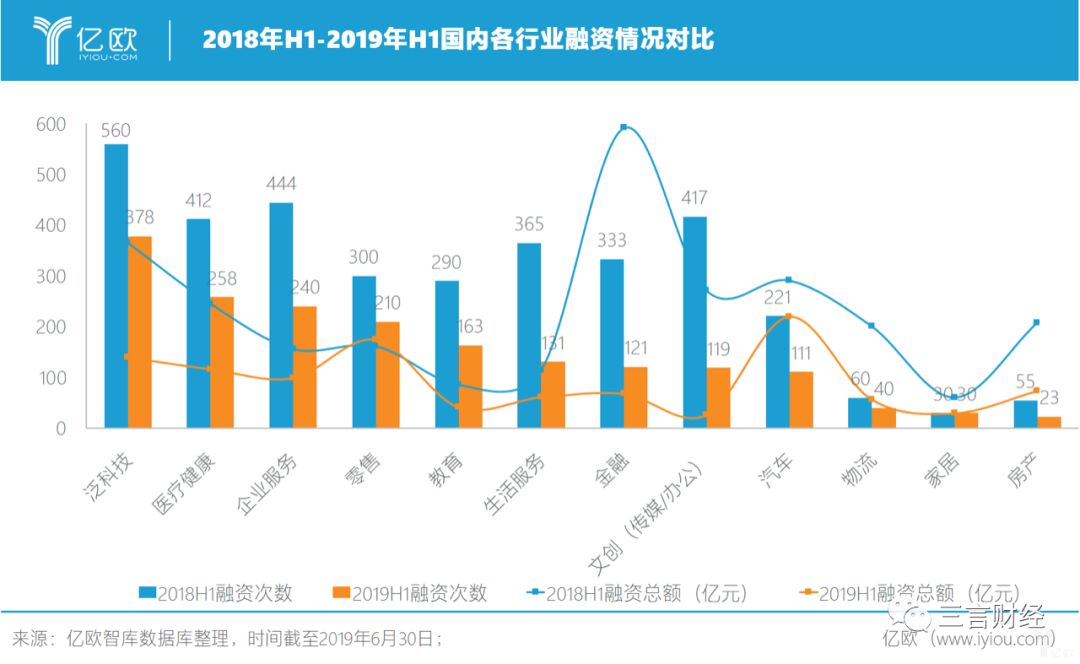

In the first half of 2018, the first half of 2018 led the field of financing in terms of financing times , reached 560 times; and the total amount of financing was the top of the financial sector, reaching 157.747 billion yuan.

Overall, both the first half of 2019 and the first half of 2018 have shrunk in both the number of financings and the total amount.

In the first half of 2018, a lot of large-scale financing occurred in the industry, and in the same period of 2019, the financing amount was relatively low. For example, in the first half of 2018, the financial industry ants Jinfu received financing of 14 billion US dollars; the real estate industry Wanda real estate received 43.5 billion yuan financing, freely received 4 billion yuan financing; SMIC in the technology sector received 3.29 billion US dollars in financing.

In the first half of 2019, the largest amount of financing was ranked in Ali’s local life service, with a financing amount of US$3 billion; the auto industry vehicle received a US$1.5 billion D round of financing, and Weilai Auto’s 10 billion yuan strategy. investment.

In the first half of 2019, the retail industry was the only industry with a steady increase in total financing. In the first half of 2019, there were 210 financings in the retail industry, and 300 financings occurred in the same period in 2018, down 30% year-on-year; in the first half of 2019, the total financing of the retail industry was 46.432 billion yuan, up 7.68% year-on-year.

Segmentation, in retail In the first half of 2019, the investment direction is mainly focused on fresh, department store retail and e-cigarettes. Among them, department store retailing and cross-border e-commerce development are relatively mature, mostly in the middle and late period as well as strategic investment. E-cigarettes have recently become a hot investment direction. In the first half of the year, there were 22 financing incidents, second only to fresh food.

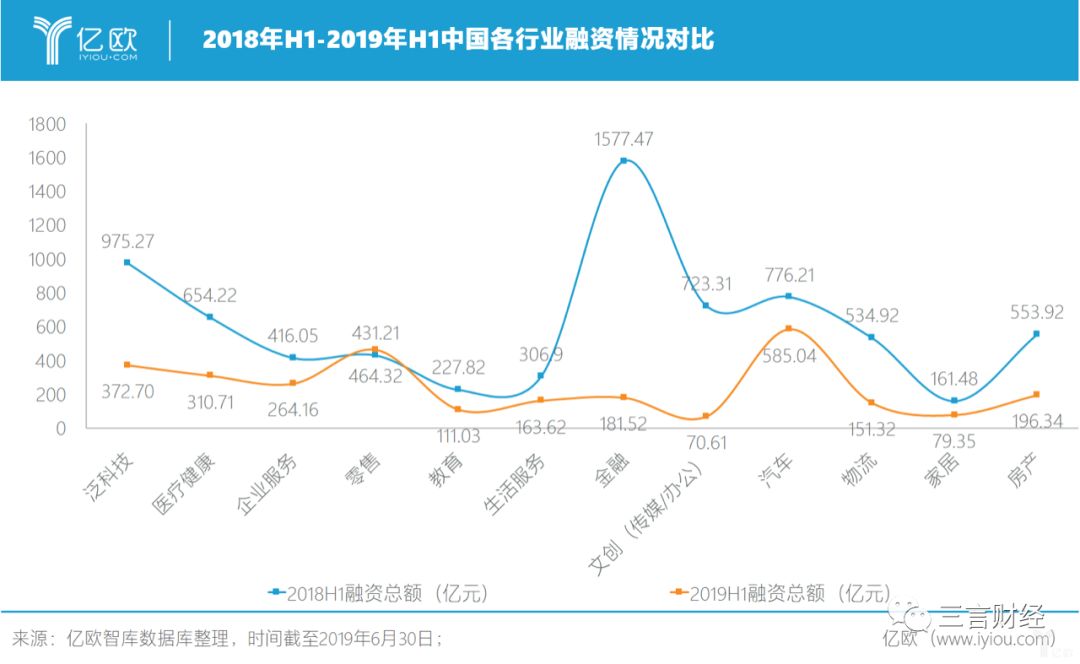

The data of the billion euros reflects the industry financing in the first half of 2019 and 2018. If you do not consider the financing situation in the segment, only from the comparison of the financing amount and the number of financing, as of now, the market situation in 2019 is not even as good as 2014.

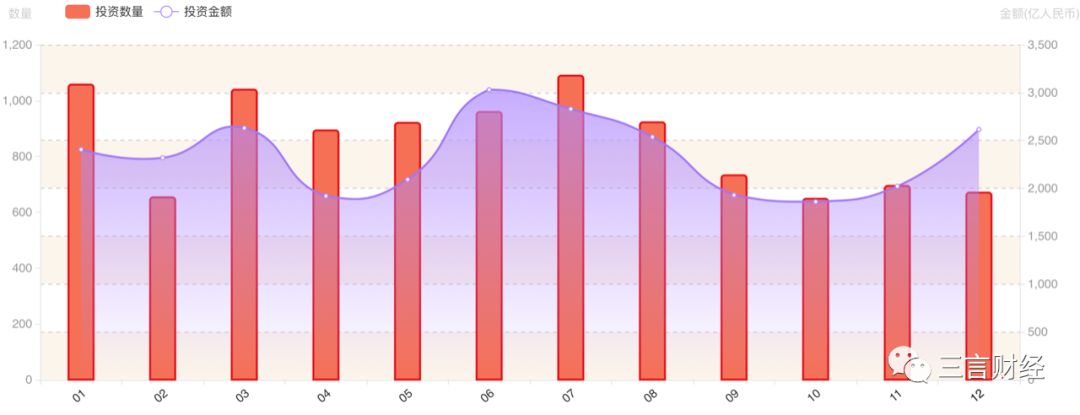

Finance Event Form for January-October 2019

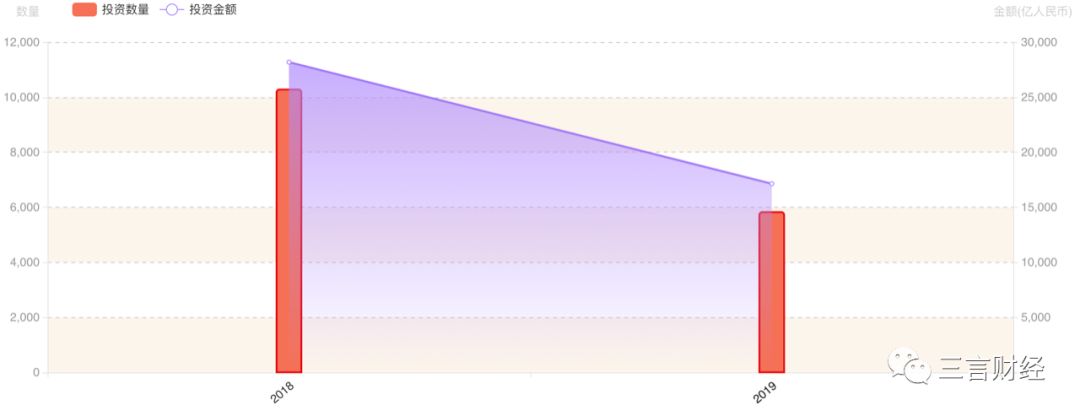

2018 Annual Financing Event Form

Comparison of financing events in 2018 and 2019

According to the data provided by it orange, it can be seen that both the amount of financing and the amount of financing are much lower than the whole year of 2018 in 2019.

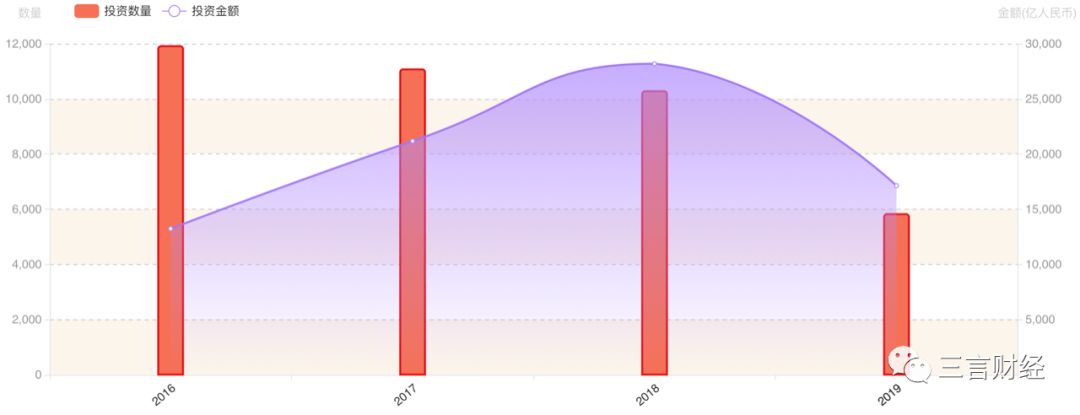

Comparison of financing events from 2016 to 2019

If the time span is traced back to 2016, it can be seen that from 2016 to 2018, the amount of financing will decrease year by year, but the total amount of financing will climb from 2016 until the highest value in 2018, but in 2019 Fall again.

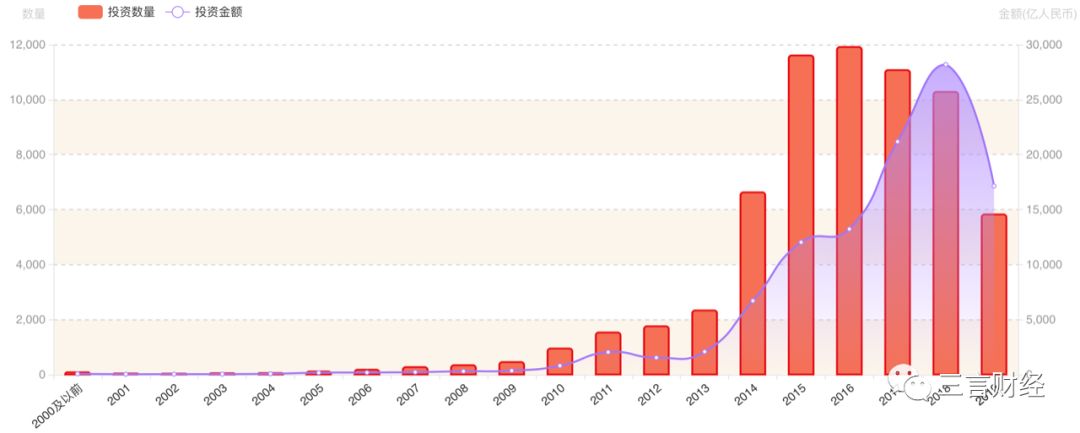

Comparison of financing events from 2000 to 2019

If you go back to 2000, you can see that the number of financing started to rise in 2014, then gradually increased, and reached the highest value in 2016; the financing amount also increased significantly in 2014, The highest point was reached in 2018. butBoth of these indicators began to decline in 2019, and the number of financing in 2019 is even less than the 2014 level.

On the other hand, from the Baidu Information Index, it can also prove the financing situation in 2019.

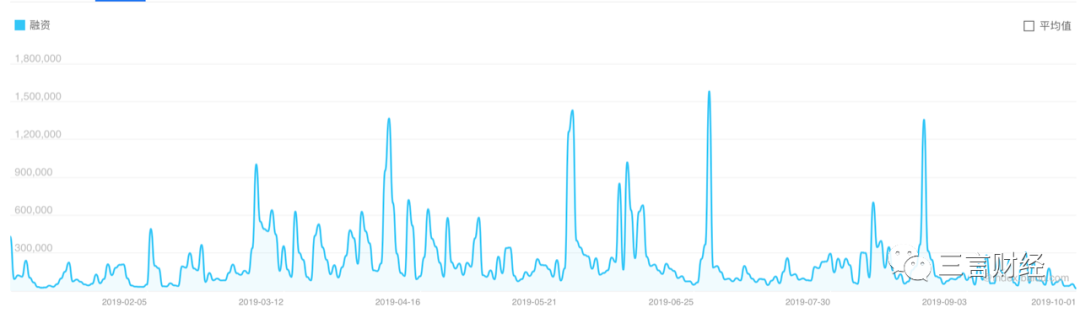

Baidu Information Index from January to October 2019

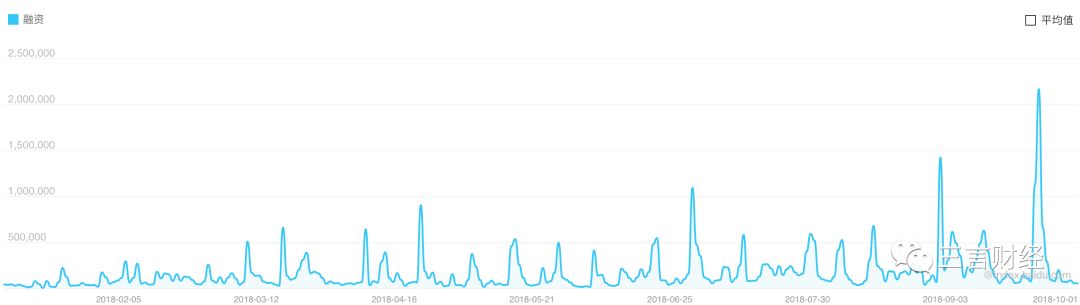

Baidu Information Index from January to October 2018

The above two tables are the Baidu Information Index Trends for financing from January to October 2019 and the same period in 2018. As can be seen from the comparison of the two figures, the information index for financing in 2018 is significantly higher than that in 2019. To a certain extent, the financing situation in 2019 has decreased.

The above data is sufficient to show that the financing environment is cold in 2019, especially for individual entrepreneurs, the poor financing environment means that the project may even be a problem.

However, the data is ultimately an objective fact of coldness. In 2019, the industry situation is cold and warm. I am afraid that only investors and entrepreneurs feel the deepest.

Investors:More than one-third of investment institutions may die, but spring will not be far away

For the financing environment of 2019, Sanyan Finance interviewed several investors. The views of several interviewed investors first affirmed the poor investment environment in 2019. This year, indeed, there are many environmental challenges for investment institutions. However, all investors do not feel “desperate”. Some investors say that any industry has a cyclical nature. It is not far from spring in the spring.

The following is an interview record:

Investor A

Q: 1, it is said that one-third of the investment institutions have died or existed in name only. Many investment institutions have made money in the previous two years. These two years are lost, do you know?

A: According to my own understanding, more than one-third of investment institutions have died, and in fact may be more. Because many institutions have not raised new funds, many well-known funds can’t raise money.. The reason for the lack of money is mainly due to the impact of the big environment. Now everyone is short of money. Many platforms have “thunderstorms” that further exacerbate this situation. I think the LP model is still very challenging in China.

Q: As an investment institution This year’s investment strategy is different from the past, why?

A: The main investment direction this year is new consumption, such as e-cigarettes.

Q:As an investment institution Is there more or less investment projects this year than before?

A: It’s similar to last year.

Xiangfeng Investment Partner Zhao Nan

Q:It is said that one-third of the investment institutions have died or existed in name only. Many investors have made money in the previous two years. These two years are lost, do you know?

A: I think the negative impact of investment institutions is mainly from five aspects:

1. The shortage of RMB funds in the market affects the fundraising of RMB funds;

2. The performance of the IPO market is not as good as expected, which may be related to the high valuation of the primary market projects in the past few years, which has led to the pressure on PE/VC performance;

3. In the last year or two, there are fewer advantages in the primary market, lacking quality track and theme concepts, which is also related to the lack of bonus opportunities in the market;

4. From 2014 to 2015, the number of VC institutions experienced a round of expansion, many new institutions emerged, and the quality projects were relatively lacking, resulting in imbalanced market supply and demand, and fierce competition;

5. Top institutions such as Sequoia have expanded their fundraising quotas, market funds have gathered to top funds, and the large fundraising environment has tightened, resulting in a certain Matthew effect in the VC/PE market. The emerging small funds with unique characteristics continue to have more pressure to survive in multiple rounds of fundraising.

6. The US dollar fund is slightly less expensive than the RMB fund raising, mainly because of the shortage of RMB funds in the market, but the US dollar fund investment will also be affected by some macroscopic unknown factors. However, in the long run, the opportunities in the Chinese market are still the world’s leading. China’s technological innovations, such as 5G and iOT, are also in the forefront of the world and are strongly supported by the government. China’s supply chain has great advantages, and hot money does not flow into China. It is difficult to find a better alternative than China.

Q: As an investment institution This year’s investment strategy is different from the past, why?

A: I think this year’s investment strategy is mainly reflected in the following aspects:

1, technology/technical, due to changes in international relations, resulting inThere has been a “home-made alternative” investment boom in the direction, such as: chip field, security, high-end medical technology, etc.;

2, emerging consumer brands, new people, new categories, investment opportunities brought by new channels;

3. The combination of offline chain + private domain traffic and community fission, especially in the sinking market, the offline format is still the mainstream consumption scenario, based on which private domain traffic and community fission can accelerate efficiency; p>

4, WeChat ecological service industry opportunities, previously mainly social e-commerce emerged, but if the service industry can be based on the WeChat ecosystem more efficient reach users, through decentralized traffic fission, the service industry Will be motivated;

5. Always pay attention to the weakness of the giant or the giant’s monopoly premium interest, the customer’s reaction and inflection point, which often also creates opportunities for new players;

6. Industry Internet, cut the supply chain through the Internet platform, use the saas service to empower upstream and downstream customers and precipitate data, and improve the efficiency of the industrial chain circulation by means of C2B collection;

7, iOT/smart hardware scene application

Founding Partner of Shengjingjiacheng Parent Fund 昊飞

Q: It is said that one-third of the investment institutions have died or existed in name only. Many investment institutions have made money in the previous two years. These two years are lost. Do you know?

A: I think that from the second half of last year to the present, whether one-third of institutional investment institutions die must not have an exact value. In fact, this situation and the temperature in the winter will have been lowered, and the temperature will rise in the summer is a truth. In the investment industry, when making money, more people are involved. This will bring a variety of enthusiasm. Including policy promotion, capital promotion, etc. The boom will also lead to low-quality investment. When the bubble is fading, these low-quality investments will bring low tide or even decline to the industry.

In 2017, there were already a lot of investment institutions in the industry, and the number has exceeded 10,000. And the increase in funds in the entire market is also very high. To a certain extent, there will be a “market saturation” situation, and in fact many industries will have the same problem.

The more money a startup project gets, the more opportunities there are in this industry. Essentially, the quality of an entrepreneurial project determines how much money an investor behind it can earn.

This is true for every track. For example, in many industries, there will be many projects in the vent, but not all projects will come to the end. Then, if you don’t go to the last project, it is equivalent to the “running” on the track. Then the investment institutions behind these “joining” projects, and the money they invested in, are actually ineffective. Therefore, many investment institutions are focused on investing in quality projects and investing as little as possible in “running and running” projects.

Therefore, for investment institutions or the industry’s recession and ebb, it is actually a cyclical performance. This is normal. Any industry has such cyclical changes, such as inventory cycles, financial capital investment cycles, or real estate cycles, which are all the same.

Therefore, investment institutions generally have to make pre-judgments to judge the future market cycle. It’s like summer is very hot, but it will definitely get colder; winter will not be far from spring.

Write at the end

Market survey data is only a representation of the industry situation, and the situation it expresses may not reflect the real situation of the market. As investors have said, the financing events in 2019 have decreased compared to previous years, and investment institutions may also have deaths. But this does not mean the end of everything. There is a survival of the fittest in any industry, and the number is not the decisive standard.

Opportunities and challenges often coexist. Although the overall amount and amount of financing has declined, this year’s capital has gathered in many new areas, such as artificial intelligence, sinking markets, 5G and the Internet of Things.

It will be less than three months in 2019. With the development of the industry, new markets will be opened up and opportunities will follow. The so-called “wind industry winter” will finally usher in spring.

The cover image is from pexels