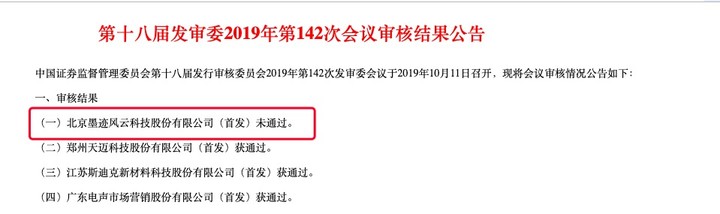

After three years of queuing on the GEM, the IPO application for the ink weather failed to pass the SFC yesterday’s meeting. Although the IPO process of the ink weather has been receiving much attention because of the product itself and the reputation of the shareholders, since the first submission of the prospectus in 2016, the industry has no shortage of bearish voices. This time, it will be said that it is expected. Inside, what is reasonable.

Ink Weather was established in 2010. The weather needs to be updated with the innovative features of the dressing assistant and the pre-installation. The ink weather has eaten the traffic dividend during the mobile Internet outbreak. The 2016 prospectus shows its installed capacity. It has reached 470 million and has more than 35 million daily activities. The huge user base and rapid growth established in the early stage of the exhibition have made the ink weather favored by capital. The list of major shareholders includes Ali Ventures, Venture Capital, Shanghai Shengzi, Innovation Workshop, etc. Well-known investment institutions.

The business model of ink weather is very simple. The main source of income is the advertising business. From 2014 to January-September 2017, the proportion of advertising information service revenue has been over 94%, and it has exceeded 98 since 2015. %. However, the business model is clear and easy to understand. It does not mean that this is a good business. The bruises of the ink weather are equally obvious. The evaluation of many analytical articles is that “the weather is just needed, but the ink is not the weather.”

Usage duration and user stickiness are a nuisance to tool-based applications, not to mention the weather, which can be accessed at a glance, and the weather applications that come with today’s smartphone systems can meet the needs of most people. Ink weather can be said to have no “moat.”

Ink weather is not unaware of the problem. Like all tool-based applications that encounter bottlenecks in development, the transformation of ink weather is also the choice of addition: social, information, taxi, shopping, movies… how to get bloated, the result can be imagined And know, the user experience is getting worse and worse, naturally it is to vote with your feet.

The online is not easy to do, the ink weather has also explored the hardware business. In 2015, a smart hardware called “Air Fruit” was released, but what is embarrassing is that the air fruit with a price of up to 999 yuan can only be detected. Air quality, no air purification, slightly ribbed. From the follow-up development, the ink weather also gave up the treatment of the hardware business. In 2014, 2015, 2016 and January-September 2017, the hardware sales revenue was only 2,223,800, 2,241,800, 1,881,300 and 2,400,600, accounting for 4.97%, 1.77%, 0.89% and 0.91% of the main business income of the current period, which is basically negligible.

C-end growth peaked, and the ink weather turned its attention to enterprise-level services. For the out-of-hospital platforms such as Hungry and Meituan take-out, a weather plan based on short-term forecasting was developed. The platform can adjust the distribution payment strategy according to the weather changes. And dispatch capacity. Ink weather claims to have taken orders from major domestic takeaway platforms, but the business status disclosed in the prospectus is only updated to 2017, and the B-side business revenue status is temporarily unknown.

In the ink weather plan to raise 340 million yuan, 220 million will be used for the ink weather app system upgrade project, only 66.5 million for research and development, indicating that the company’s focus is still on the C side, but also let People are curious about how the system upgrades require the funds raised by most IPOs. What’s more, the ink weather does not seem to lack cash flow. One of the most criticized information in the prospectus is that the company has used funds from financing for several years to obtain income from financial management. This is regarded as the management has no clear development of the company. The planning approach has also been questioned as the listing of the amaranth.

▲ Image from: Sina

The transitional history of ink weather has been frustrated, and perhaps it can also be found in Meitu. Mito started with the retouching software, and then entered the mobile phone business, and successfully listed in Hong Kong, but the Mito mobile phone, which is famous for its beauty, is hard to say success, and it has contributed a lot of revenue while contributing most of the revenue, so Mito Last year, I handed over the mobile phone business to Xiaomi, and turned my attention back to Meitu Xiuxiu, announcing the transition to socialization, but at least so far, whether it’s the beauty show of the community or the beauty of the short video, The video social field can’t compete with the head applications such as vibrato, fast hand, etc. The stock price of less than 2 Hong Kong dollars can also explain the predicament of Mito. It is necessary to know that Mito has reached a maximum of 23 Hong Kong dollars at the beginning of its listing.

Hardware, social, e-commerce, advertising… The application transformation process of tools is inevitably in the process of “wide-spreading the net”, but only a few can find the right direction, and Mito has not yet come out of the curse. There seems to be little time left for the ink weather.