The disillusionment of the fast fashion myth is an indisputable fact. According to the incomplete statistics of Winner.com, 2019, the fast fashion brand added 84 stores in the first half of the year, which was significantly reduced compared with the previous three years, behind the multiple brands. “Sweet Tears”: After New Look and Topshop were withdrawn from China, FOREVER 21 also staged a big defeat this year. ZARA, H&M, UR and MJstyle closed the store one after another and slowed down the pace of expansion.

In contrast to the fast fashion, it’s the sportswear brand and the street brand that are constantly attacking. For example, Guo Ning represents China’s Li Ning from 27 stores last year to 70 stores, and will hit 100 at the end of the year; FILA FUSION has entered China for more than a year to open 100+ stores; the American street brand Champion new store constantly, repeatedly raised the topic…

The performance differentiation of the apparel industry has also raised new issues for shopping malls. Then, what is the overall performance of the shopping mall apparel industry in the first half of the year? In addition to fast fashion, what other subdivision developments are unsatisfactory? Sportswear, fashion brands, designer brands, what emerging brands are worthy of attention?

1,The first half of the 2019 shopping mall apparel retail business changes:Sportswear/Tide/Designer brand development, fast fashion/Men’s development down

The overall development of apparel retail formats is down

According to the big data monitoring of the winners, in the first half of 2019, the proportion of clothing retail brand closings was higher than that of opening stores, and the overall living space narrowed and the development declined.

Current shoppingThe center apparel retail format faces two aspects of “snapshot”: on the one hand, the shopping center in order to highlight its experience advantages compared with e-commerce, and constantly increase the experience of entertainment, children and children, and reduce the retail space. On the other hand, as the retail environment tends to be weak and consumer demand changes rapidly, the apparel industry is accelerating the reshuffle, especially in the fast fashion that has been raging in the past.

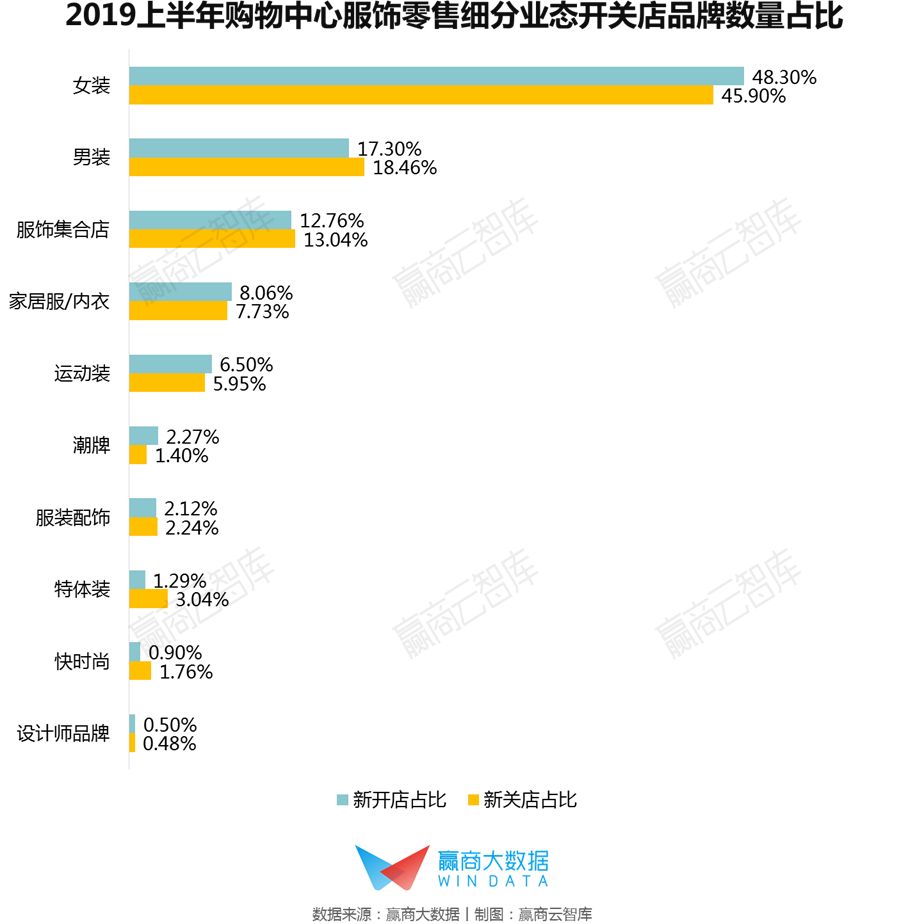

▌快时尚/Men’s clothing/clothing collection store development down, sportswear/women’s/designer brand development goes up

From the first half of 2019, the shopping malls are divided into business outlets:

■ The proportion of fast fashion stores is higher than the proportion of open stores, and the overall operating conditions are not good, and the development is down. As consumers become more and more focused on quality and personalization, the once-popular fast fashion brands are getting worse. In the first half of the year, FOREVER 21 withdrew from China and declared bankruptcy at the end of September. H&M, ZARA, MJstyle, UlifeStyle, UR and other brands also tightened their belts and closed stores or adjusted for poorly operated stores.

■ The proportion of men’s clothing, special clothing, clothing accessories, and clothing collection stores is higher than the proportion of open stores, and the development is down. The current consumer’s fashion awareness is constantly increasing, consumer demand is gradually tilting toward internationalization and fashion trends. The lack of innovative men’s and special clothing brands is not enough. The clothing collection store also enters the adjustment stage. .

■ The number of women’s opening and closing stores is at a high level, and the brand competition is fierce, but the overall development is still good. Eveli, Taiping Bird Women’s Wear, Lily and other domestically developed women’s wear brands continue to deepen the shopping mall channels, and the number of newly opened stores in the first half of the year is high.

■ The proportion of sportswear, fashion brands, designer brands, home clothes/underwear stores is higher than that of closed stores, and development is in the upward channel. Under the impetus of the national tide and rising fitness demand, sportswear has become a format that shopping centers are willing to attract; at the same time, the rising demand for new middle-class and new-generation young people is becoming more refined and diverse. Trendy, high-quality and personalized brands, designer brands, homewear/underwear brands are more likely to be favored.

Second,In the first half of the year, 2019, the interpretation of the industry in shopping mall apparel retail development:Sportswear emerging brand has become a recruiting force

< /p>

In the first half of 2019, in the 10 sub-divisions of shopping malls, sportswear, fashion brands, designer brands, womenswear, homewear/underwear performed well, then what are the five formats that won? What brand of innovation is worth paying attention to?

▌ Sportswear:Multiple creative elements, resort to sports lifestyle

The rise of the national tide and the fashion of sports make sportswear a “golden track” in the apparel industry: The design elements of sportswear tend to be diversified, blending into traditional Chinese culture, retro Fantasy and other creative styles; good at fashion week show, star bring goods, cross-border joint name, etc., to attract traffic attention efficiently; do not stop selling sports equipment, try to provide a place to learn and discuss sports lifestyle to improve consumer stickiness .

▼Interpretation of typical emerging sportswear brand cases

[ANNA SUI ACTIVE]The new sports brand of Anna Sui

-

Brand citizenship: United States

-

Create/Enter Chinese Mainland Shopping Mall Time: 2019

-

A typical shopping mall has been established: Shanghai Xingye Taikoo Hui, Shanghai iapm

Anna Sui is a eponymous brand created by American-American fashion designer Anna Sui in 1981. It is labeled with the unique personality and design style of “Fashion Cool Girl”. In June of this year, the brand launched the sports line ANNA SUI ACTIVE, and the world’s first store was located in Shanghai Xingye Taikoo Hui, followed by Shanghai iapm.

ANNA SUI ACTIVEFemale fashion sportswear with both style and function, set the Master Line master series, Design Theme design selection and many other topics The style is changeable. Products include T-shirts, sports shorts, sports underwear and swimwear, etc., prices ranging from $400 to $3,980, designed to cover the diverse needs of fashionable women.

In terms of consumer operations, ANNA SUI ACTIVEFounded ASA GIRL CLUB Fan Sports Club, regularly organizes members to participate in a variety of sports courses and interactions Activities, etc., to enhance consumer loyalty.

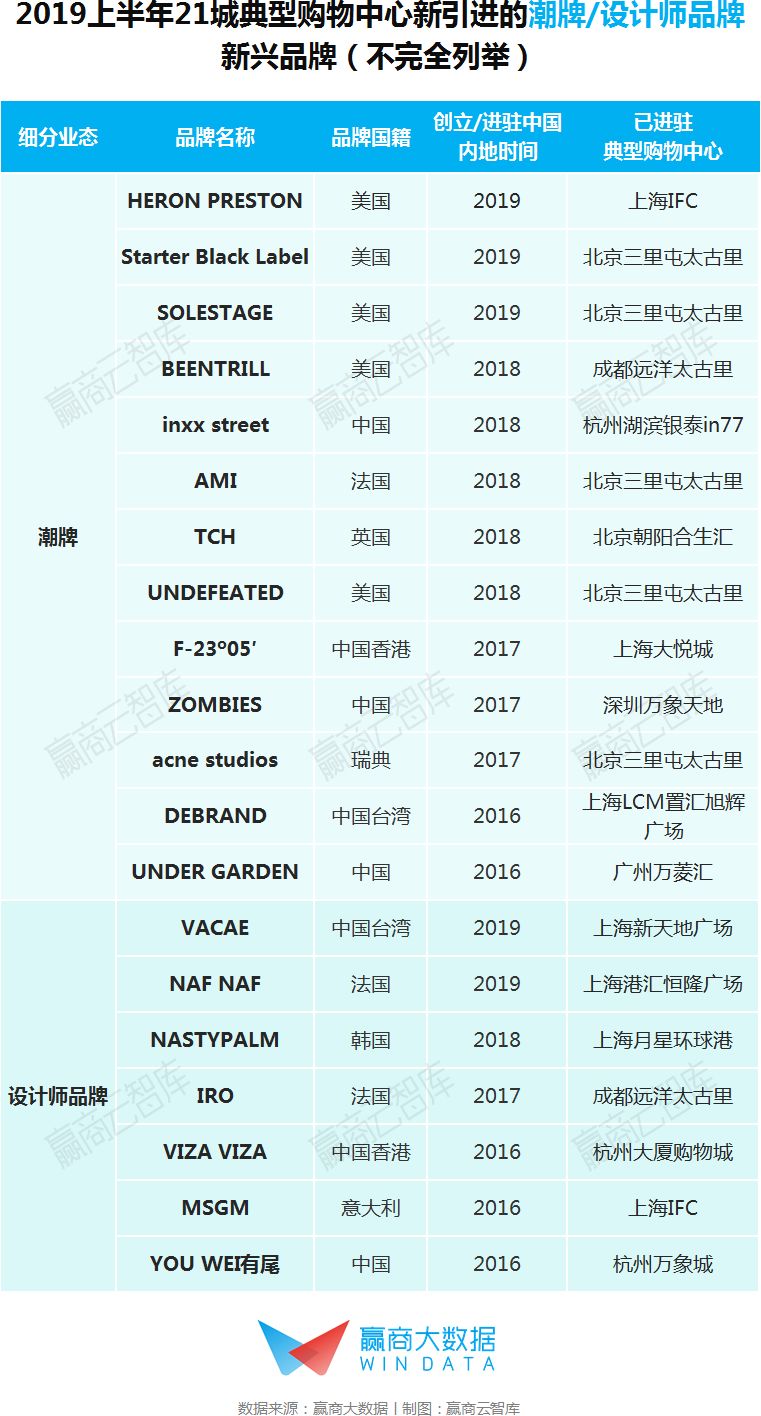

▌潮牌/designer brand:Transfer personalized aesthetic expression

After 90s, after 00, young people became the main force of fashion consumption. Clothing has long exceeded the scope of use and functionality, and has been given more personality, culture, social and other psychological aspects. . This makes the most popular and value-added fashion brands and designer brands increasingly sought after.

Generally, the street brand and designer brands are positioned in the middle and high end, advocating personalized aesthetic expression, incorporating a large number of artistic themes in the design, and being deeply loved by the trendy men and women; at the same time, paying attention to the offline The immersive experience of the scene creates a space for sales, display, experience, and play to cater to the emotional appeal and life of young people.the way.

▼Interpretation of a typical emerging designer brand case

[VACAE] A romantic holiday style

-

Brand citizenship: Taiwan, China

-

Entering Chinese Mainland Shopping Center: 2019

-

Store demand area: 100-200 square meters

-

A typical shopping mall has been established: Shanghai Xintiandi Plaza, Beijing Qiaofufang Grassland Shopping Center

Founded in 2014, VACAE is a new Taiwanese independent designer womenswear brand. This year, it began to enter the mainland market, and has already entered Shanghai Xintiandi Square and Beijing Qiaofufang Grassland Shopping Center.

Inspired by the Vacation Vacation, VACAE offers a series of early spring vacations, spring and summer collections, and light dresses. The design is based on different holiday stories, and incorporates romantic “fairy elements” such as satin and lace to interpret the charm of women.

The design of the brand’s stores is also quite unique. For example, Shanghai Xintiandi has the theme of island holiday style, the ceiling design and the colorful floor tiles are simple and romantic. Beijing Qiaofufang Grassland Shop is like a museum. The sculptures and art paints are classically elegant.

[YOU WEI has a tail]Play “Scene Thinking”

-

Brand citizenship: China

-

[STUDIO TOMBOY ]Main oversize casual fashion

-

Brand citizenship: Korea

-

Entering Chinese Mainland Shopping Center: 2019

-

Store demand area: 80-150 square meters

-

A typical shopping mall has been established: Beijing SKP, Xi’an SKP, Zhengzhou Denis David City

STUDIO TOMBOY is a well-known women’s wear brand in Korea. It was founded in 1977 and currently has hundreds of stores in Korea. In April this year, the brand opened its first offline store in China at SKP in Beijing, and then entered the shopping malls of Xi’an SKP and Zhengzhou Denis David City.

STUIDO TOMBOYTargeting young women, the oversize (loose) design style is casual and recognizable. For example, the spring and summer series launched this year is inspired by the supermarket life, and the daily comfort is matched. The autumn and winter series are traced back to the 1990s, and the main retro is easy.

[VGRASS STUDIO]Combining Oriental Charms with Western Design Techniques

-

Brand citizenship: China

-

Entering Chinese Mainland Shopping Center: 2019

-

A typical shopping mall has been established: Shanghai Huigang Plaza,

Vigna set up an operational headquarters in Milan, Italy in 2017, and created a new high-end women’s brand VGRASS STUDIO. This year’s brand Appointed former Prada Women’s Design Director Rodolfo PaglialuNga is the creative director, and opened the first domestic store in Shanghai Huilong Plaza, attracting a lot of attention in the fashion circle.

VGRASS STUDIO is based on the concept of “East Meets the West”,Incorporating Chinese traditional Yunjin silk techniques into Western design techniques, bringing artistic and cultural heritage Fashion women’s clothing. In February of this year, the brand appeared in Milan Fashion Week, bringing the autumn and winter series of 2019. The exquisite brocade and Italian craftsmanship with oriental charm highlight its high-end positioning.

▌Homewear/Underwear:Diversification, Quality, Power Marketing

The improvement of spending power and the formation of the “Yue Ji” consumption concept have driven young people and new middle-class products to improve their requirements for personal clothing.More style, better quality Focus on comfort and become the direction of home service/underwear brand upgrade. In addition, homewear/underwear brands also focus on building a KOL marketing matrix that continues to drive the spread of brand information.

▼Interpretation of typical emerging homewear/underwear brand case

[Intimissimi]Main quality underwear, mining KOL marketing

-

Brand citizenship: Italy

-

Entering China Mainland Shopping Center: 2017

-

Store demand area: 60-120 square meters

-

A typical shopping mall has been established: Shanghai Xingye Taikoo Hui, Chengdu Oceanic Taikooli

Underwear brand INTIMISSIMI was born in 1996, and the socks and swimwear brand Calzedo