Every marketing change and channel change brings a new wave of opportunities to overtake the corner.

Editor’s note: This article is from WeChat public account “Huaxing Capital” (ID: iChinaRenaissance), author Hua Xingxin Economic fund.

If you want to use a word to describe the cosmetics industry, we think it will be “segmentation”, far exceeding the high-level and dynamic segmentation of other industries. Look at your dressing table at a glance.

Segmentation creates an unparalleled long tail in the cosmetics industry – small brands, new brands, and entrepreneurs always have opportunities. The secret of cutting in is always niche, flexible, and quick to respond; but it is easy to cut in and make it difficult. The vast majority of branding aims to build awareness on the consumer side and reduce the cost of decision making for instant purchases. Manageable is brand awareness, and brand loyalty is hard to expect.

Revenue growth, intergenerational switching is the key to driving growth

1. Per capita consumption is still low, and the growth potential of China’s cosmetics market is huge

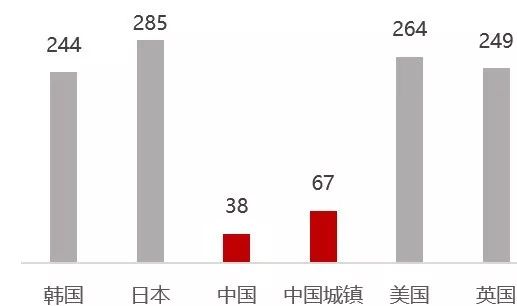

China is the second largest cosmetics market in the world. According to Euromonitor data, the size of China’s cosmetics market in 2017 was 361.6 billion yuan, and the market compound growth rate in 2008-2017 was 9%, far exceeding the growth rate of 2% in the global market. However, the current per capita consumption of cosmetics in China is 38 US dollars, far behind the spending of more than 240 US dollars per capita in Japan, South Korea and the United States. The size of China’s cosmetics market still has a large growth potential.

Photo: China’s cosmetics market size and growth rate in 2008-2017

Source:Euromonitor

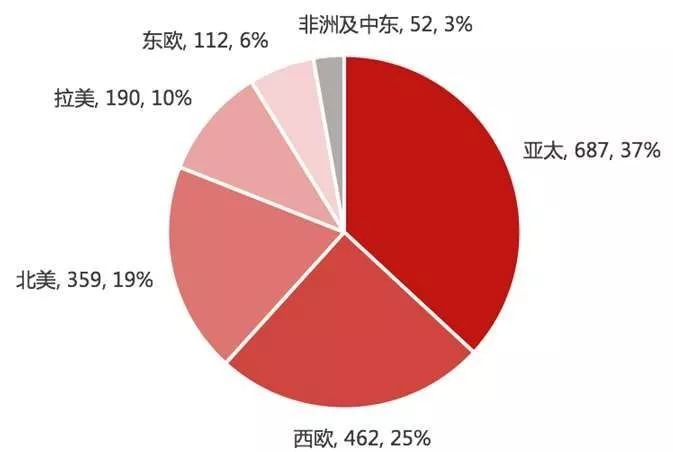

Photo: Cosmetics market in 2016 (100 million euros) and percentage

Source:Euromonitor, Everbright Securities

Figure: Per capita cosmetics consumption in countries (US$)

Source:Euromonitor, Ipsos, Essence Securities

2. Revenue growth is the foundation driver

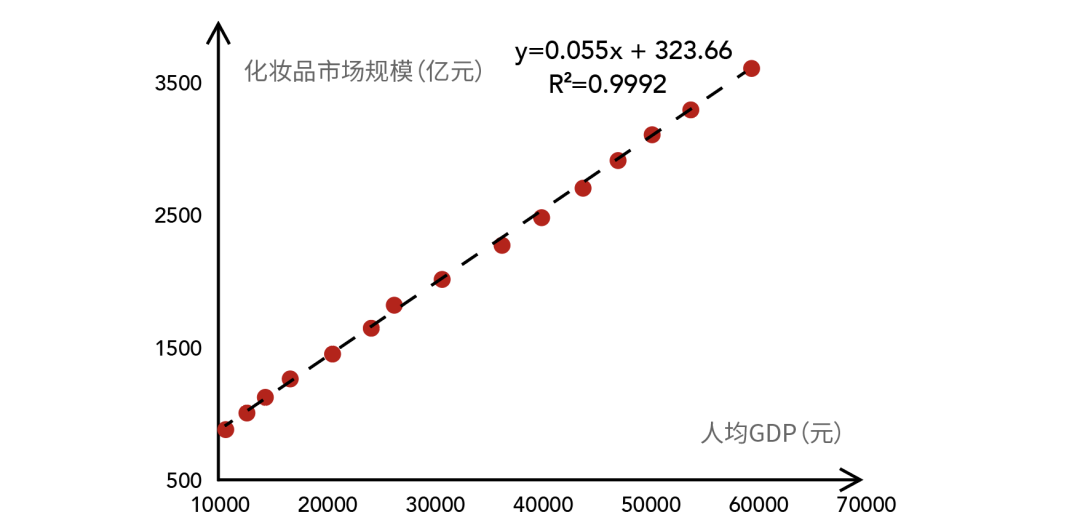

Revenue growth is the driving force driving the rapid growth of the cosmetics industry and the upgrading of consumption. The overall consumption scale of the Chinese cosmetics market and the per capita GDP show a strong linear correlation. As women’s spending power grows, consumer willingness increases, and policies actively support cosmetics consumption, reducing cosmetics consumption tax and import tariffs, driving the growth of the cosmetics industry and market size.

Photo: China’s cosmetics market size and per capita GDP

Source:Euromonitor, National Statistical Yearbook, Huachuang Securities

Picture: Per capita GDP is strongly correlated with the size of the cosmetics market

Source:Euromonitor, National Statistical Yearbook, Huachuang Securities

3. Intergenerational switching drives market change and upgrade

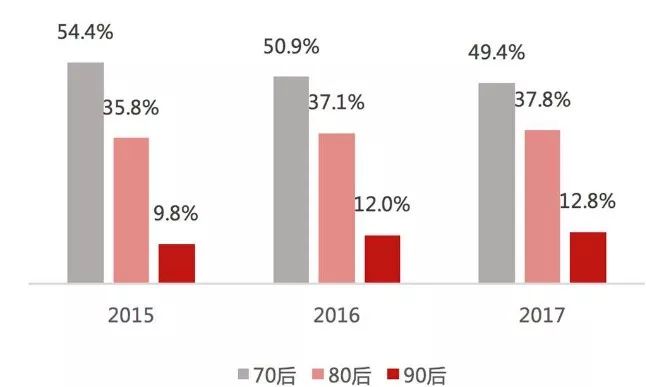

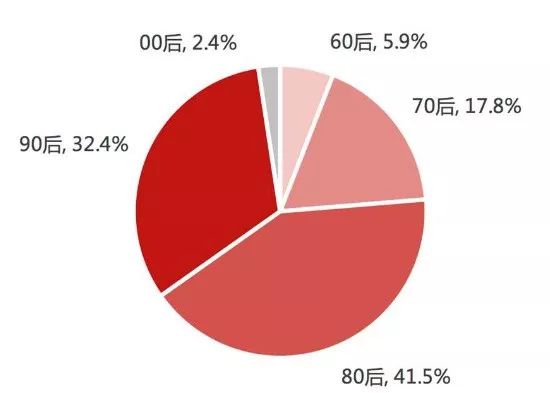

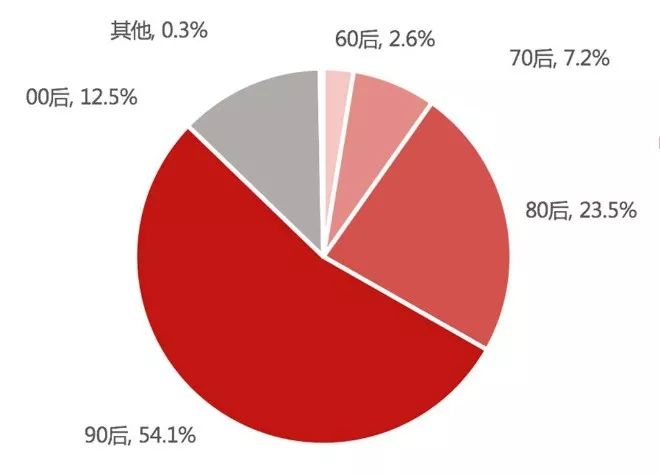

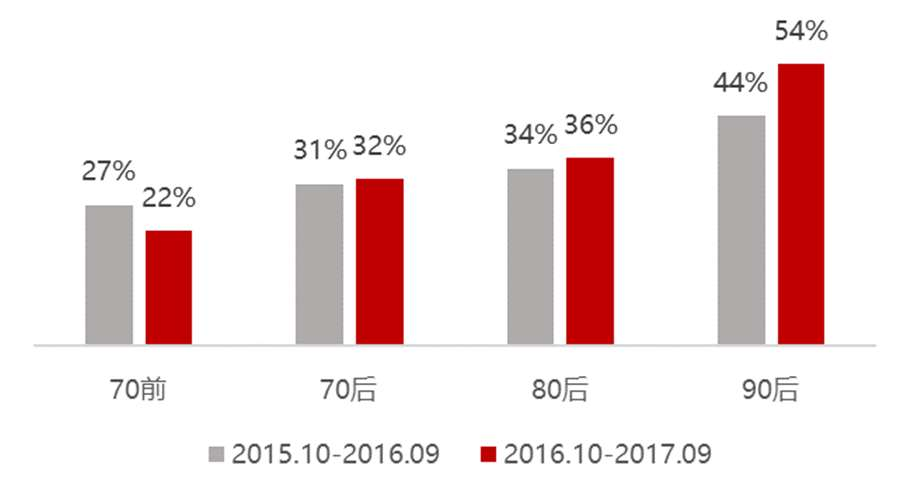

In addition, cosmetics consumption is becoming younger and there is a clear intergenerational switch. Young consumers drive market changes and drive the market further. It is estimated that more than 70% of the online cosmetics market is supported by 80/90, and mainstream target consumers are rapidly shifting from 70 to 80/90.

Picture: Total consumption of each population in 2017

Source: China UnionPay & JD Finance “2017 Consumer Upgrade Big Data Report”, Huachuang Securities, Star Map Data, Caitong Securities

Picture: 2017 online share of cosmetics online buyers

Source: China UnionPay & JD Finance “2017 Consumer Upgrade Big Data Report”, Huachuang Securities, Star Map Data, Caitong Securities

The intergenerational differences in cosmetics are mainly derived from the age group of consumption awakening, the brand of initial consumption, the difference in the concept and willingness of consumption.

Source: Guosheng Securities (Note: 55 is the retirement age for women)

The consumption structure of Chinese cosmetics is a clock curve, which is significantly different from the logarithmic curve in Europe and America. Women in Europe and the United States increase their spending on cosmetics as they get older. In China, cosmetics consumption is dominated by young consumers, with greater consumer awareness and willingness to pay, and more spending than older people.

Figure: Distribution of cosmetics market by age of consumers

Source: Guosheng Securities

In the future, with the age of consumers and the popularity of cosmetics consumption, China will move closer to the European curve, but the change will be 10 years. Given the investment cycle of most VC/PE, the research focus can be on the brands and models after borrowing 80/90.

4. Consumer spending power in low-tier cities is in the release period

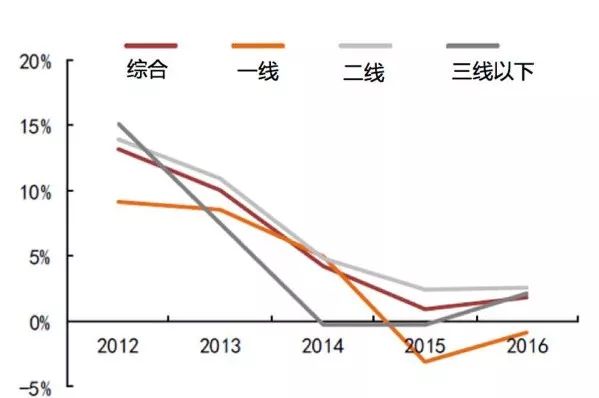

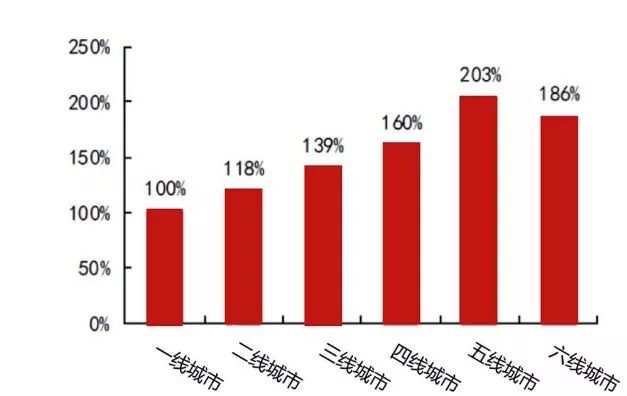

The current growth rate of the cosmetics market is mainly contributed by the second- and third-tier cities and below. According to data from the Jingdong Consumer Research Institute, the growth index of low-tier cities below the third- and fourth-tier cities is significantly higher than that in the first- and second-tier cities. In 2016, the growth index of the third, fourth and fifth-tier cities was 139% and 160% respectively. With 203%, which is much higher than 100% in first-tier cities and 118% in second-tier cities, the coverage of logistics services in superimposed low-tier cities is gradually improved, and supply capacity is strengthened. At present, the consumption power of cosmetics in low-tier cities is in the release period.

Figure: Year-on-year changes in retail sales of key large retailers

Source:Euromonitor, Caitong Securities

Photo: 2016 City Consumption Growth Index

Source: Jingdong Consumer Research Institute, Caitong Securities

New generations of consumers change consumption patterns and information channels

1. Word of mouth? Quality? Young people want to love themselves

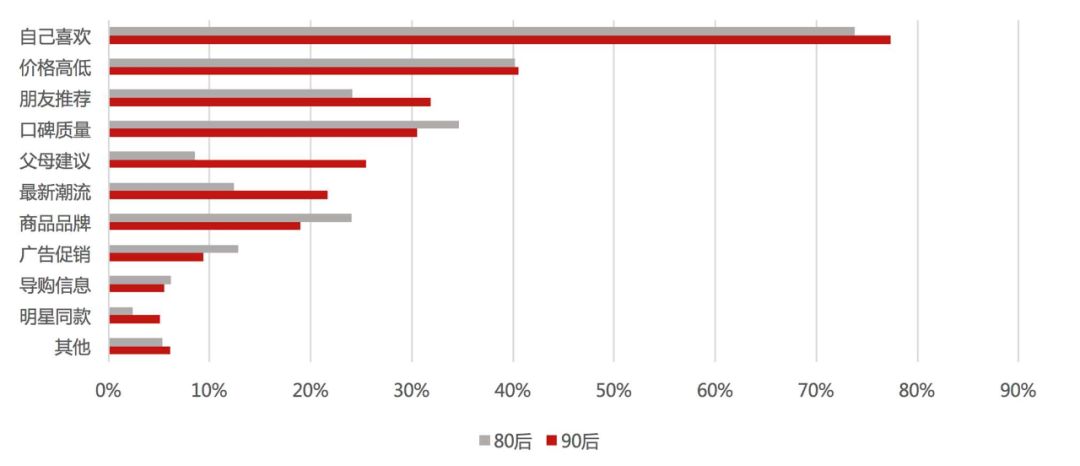

Young cosmetics consumers are more self-esteem, more concerned with their own preferences and brand tonality. A single brand was forced to narrow its positioning, further segment its own customer base in order to form a match, and the new brand also found more room for growth, which objectively led to the dispersion of brand concentration. Compared with the choice of brand after 80/90, it is more inclined to “self-like”, “friend recommendation”, “newest trend” and other factors. The simple product brand and word-of-mouth quality are no longer so important.

Figure: After 80, 90 after consumption concept

Source: Analysys think tank & Tencent “China Post-90s Youth User Survey Report”

Picture: The target audience of the beauty target on the WeChat TopTop beauty brand interest concentration TGI

Source: Tencent Social Big Data

(Note: TGI is the target group index, reflecting the strength or weakness of the target group for a particular research goal)

We believe that the loyalty of cosmetics brands is not high. Cosmetic companies are not earning money from consumers, but they are washing users like game companies. Low brand loyalty has further driven brand decentralization and given new brands more opportunities. According to Tencent’s social big data, among the beauty brands that WeChat put Top10, there are 6 brands whose interest concentration is within 1 standard deviation of the mean, and the difference is small.

2. Category expansion never stops, “component party” is popular

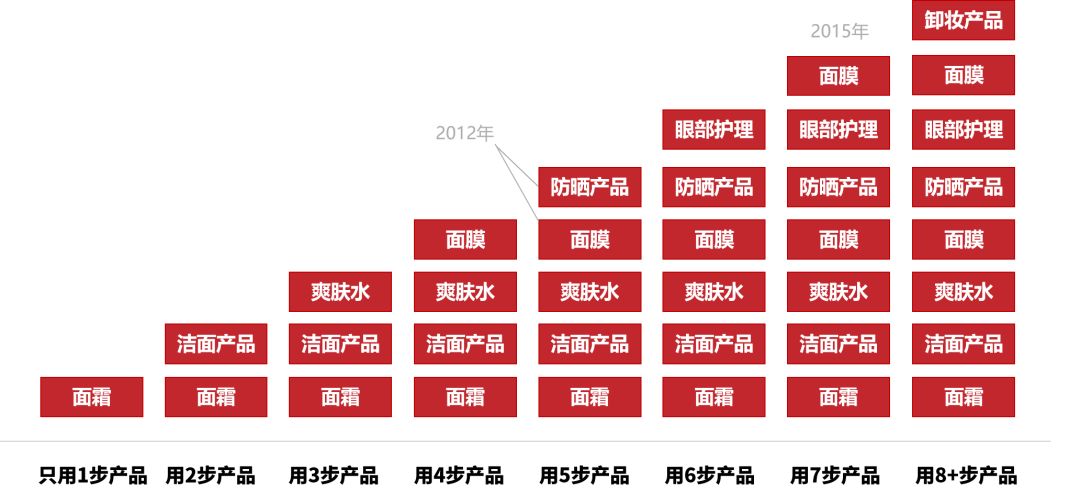

Early consumers have only one step of makeup, and now they have advanced to more than eight steps. The increasingly complex makeup demand has pushed the increasing complexity of product categories, and has also made consumer demand increasingly fragmented.

Figure: Skin care steps tend to be complicated

Source: Kaddu Data, Tianfeng Securities

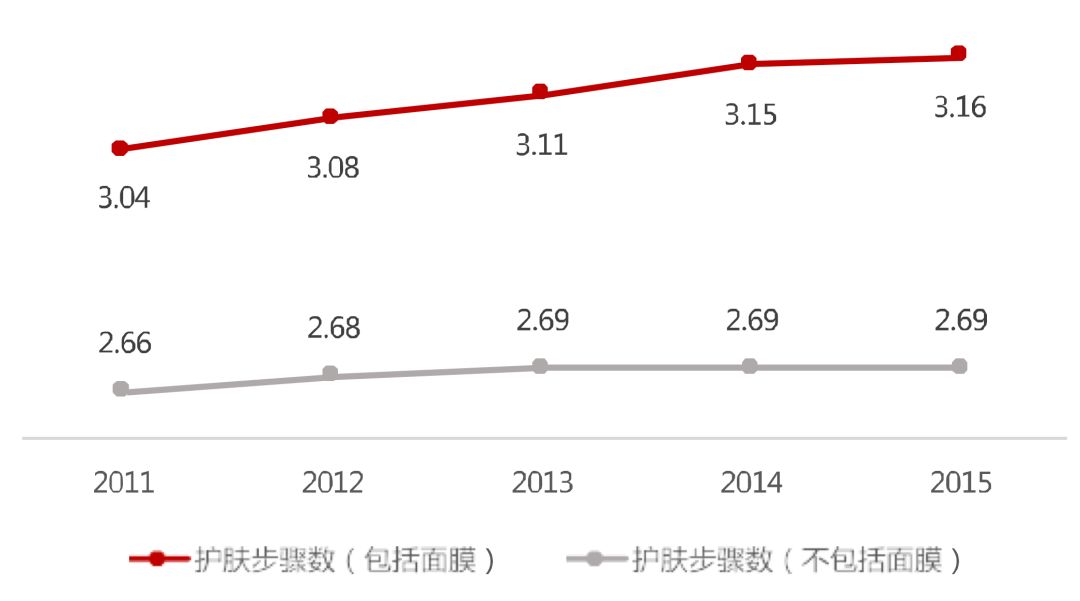

Figure: Personal average skin care steps are gradually increasing

Source: Kaddu Data, Tianfeng Securities

Consumers no longer only use the brand as a purchasing decision indicator, but instead pay more attention to the principle of beauty makeup. The “component party” is popular, and the proportion of beauty bloggers who see the elderly in the composition analysis has also increased significantly.

Figure: Top Skin Care Ingredients Discussion Ranking

Source:CBNData

3. New Media:Hold the young consumer group

The habitual preference of young consumers has increased the importance of new media channels, and the traditional delivery model of cosmetics companies is facing reform. Online attention to cosmetics is gradually becoming younger, and more than two-thirds of users who pay attention to cosmetics on Weibo are after 90/00.

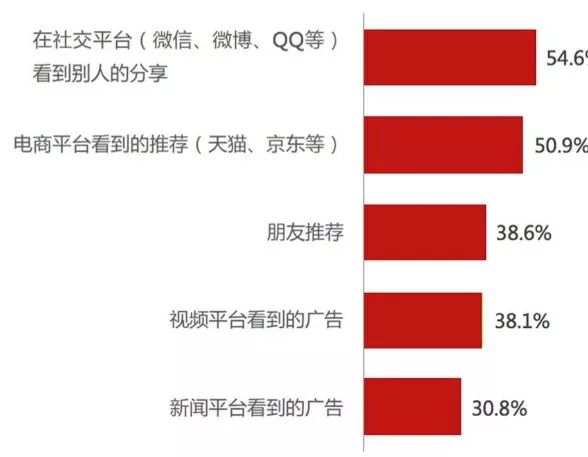

After 90, consumers mainly learn about new products and new brands through social platform and e-commerce platform recommendation. Online marketing (social platform, etc.) has a unique carrier advantage for the new generation of cosmetics consumers.

Figure: Weibo pays attention to the distribution of cosmetics population

Source: Weibo Data Center, Caitong Securities

Figure: After 90, learn about new products/new brands channels

Source: Ai Rui, a little bit of information

The growth after 80/90 is accompanied by the rapid development of the Internet. As this group enters the growth period of consumption, the e-commerce channel has also begun to flourish. From 2009 to 2017, Taobao’s annual growth rate is 47.37%, which is the period of independence and living after 85 and 90.

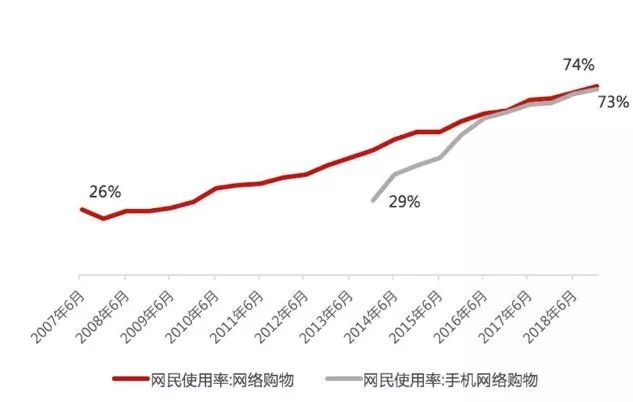

At the same time, the rapid development of e-commerce channels, the corresponding logistics distribution, e-commerce platform to promote the standardization of merchants, the credit mechanism is gradually improved, online shopping is more convenient, more consumer groups have begun to “touch the net” shopping. The online shopping market has reached a total of 20% of the company’s total, and the online shopping penetration rate has reached 2/3. The proportion of e-commerce sales of cosmetics companies has also increased year by year. Many cosmetics companies have launched online channels to expand sales.

Figure: The size of the online shopping market accounts for the total amount of zero in society

Source: iResearch

Figure: Internet shopping and mobile internet shopping usage rate

Source:WIND

Highly subdivided, the explosion strategy has become the best choice for the rise of the company

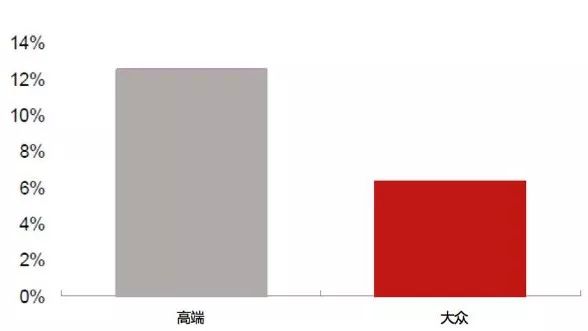

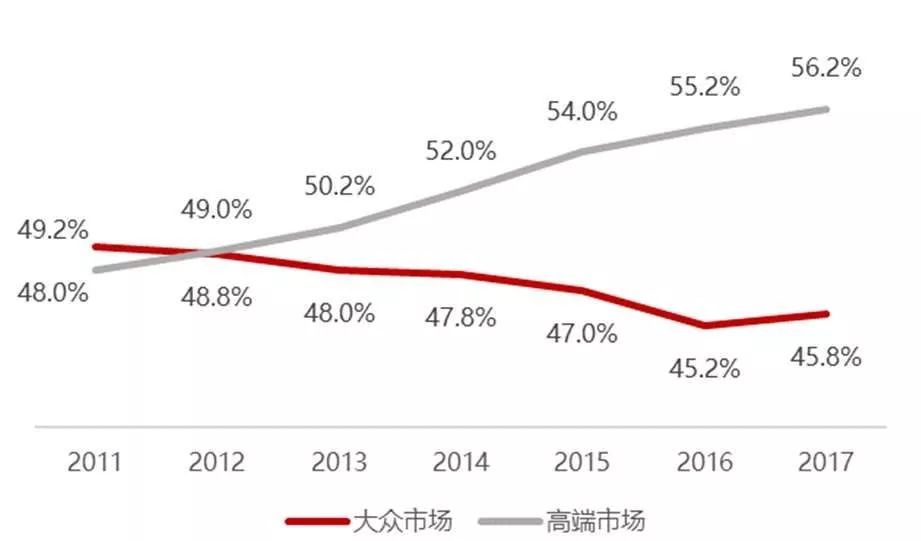

Based on the positioning of the market, we use 500 yuan as the line, 500 yuan or less as the mass market, and more than 500 yuan as the high-end market. From the data of 2003-2007, Volkswagen products occupy a major market share. Although the growth rate of high-end products is high in recent years, in the long run, Volkswagen single products will still occupy the absolute mainstream.

Figure: China’s cosmetics market high-end vs. mass proportion

Source:Euromonitor, Everbright Securities

Picture: 2012-2017 high-end vs. mass compound growth rate

Source:Euromonitor, Everbright Securities

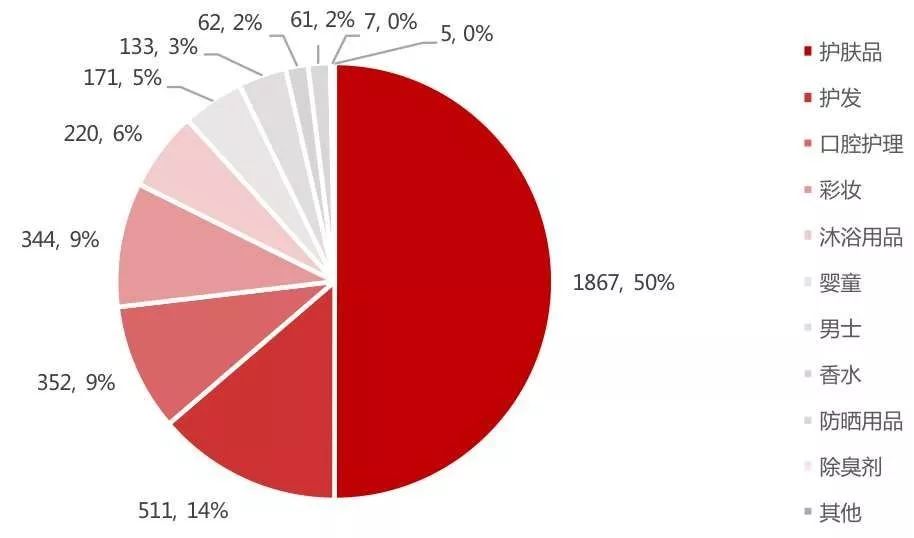

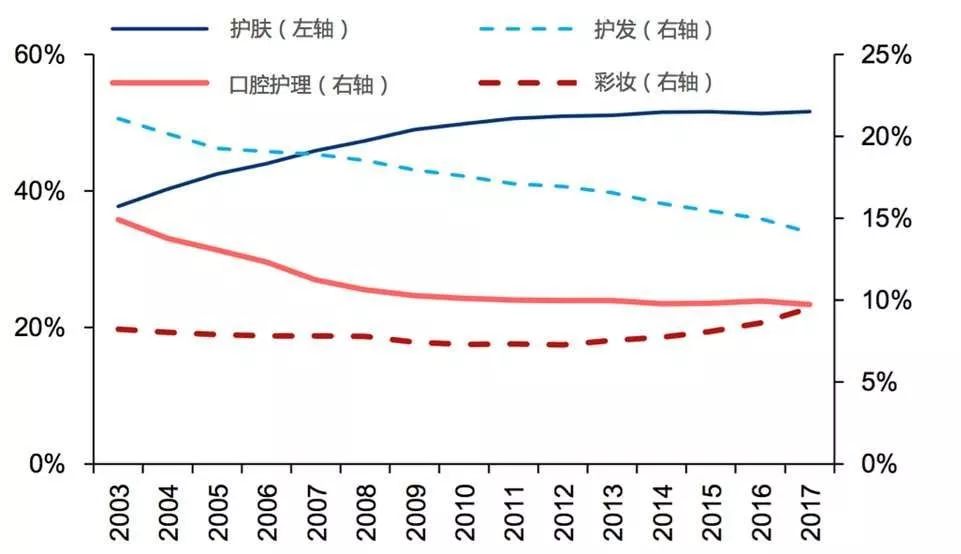

By category, among the five major categories of cosmetics, we classify hair care, bathing, and teeth (oral) into personal care, and skin care and make-up are classified as beauty. Data from 2003 to 2017 show that the beauty market share is large and growing rapidly, while the personal care market is gradually stabilizing. The Volkswagen+Beauty segment has a core growth market opportunity that cannot be ignored.

Photo: China’s cosmetics segment market size (100 million yuan) and proportion

Source:Euromonitor, Everbright Securities

Figure: Changes in major categories in 2003-2017

Source:Euromonitor, Everbright Securities

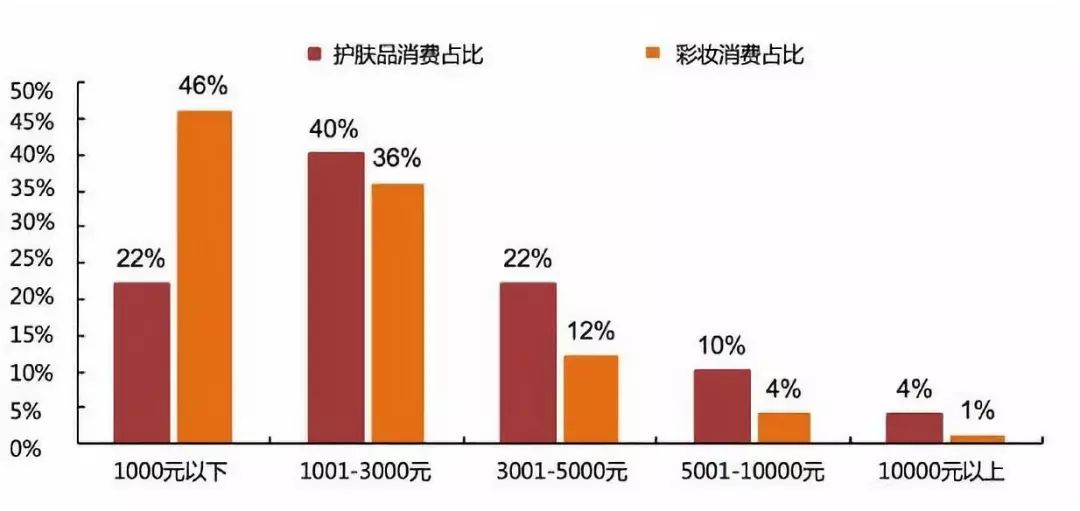

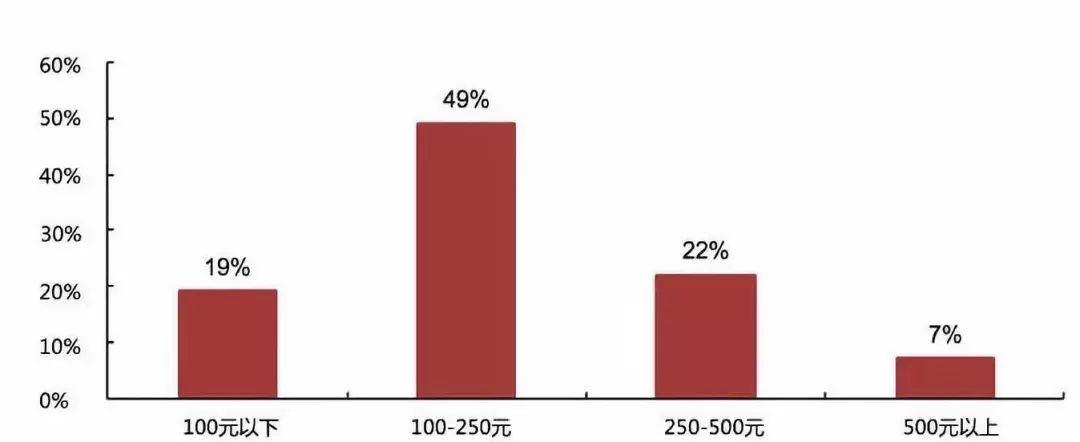

Microblog data center data shows that 62% of cosmetics buyers’ annual consumption of skin care products and 82% of buyers’ annual makeup consumption are below 3,000 yuan, which shows that pricing is still the primary factor in positioning. The price of a single cosmetic product is below 500 yuan, and 250 yuan is the core price segment.

Picture: The annual consumption of skincare makeup is concentrated below 3,000 yuan

Source: Weibo Data Center, Caitong Securities

Picture: Consumers with a single skin care product spending below 250 yuan are high.

Source: Weibo Data Center, Caitong Securities

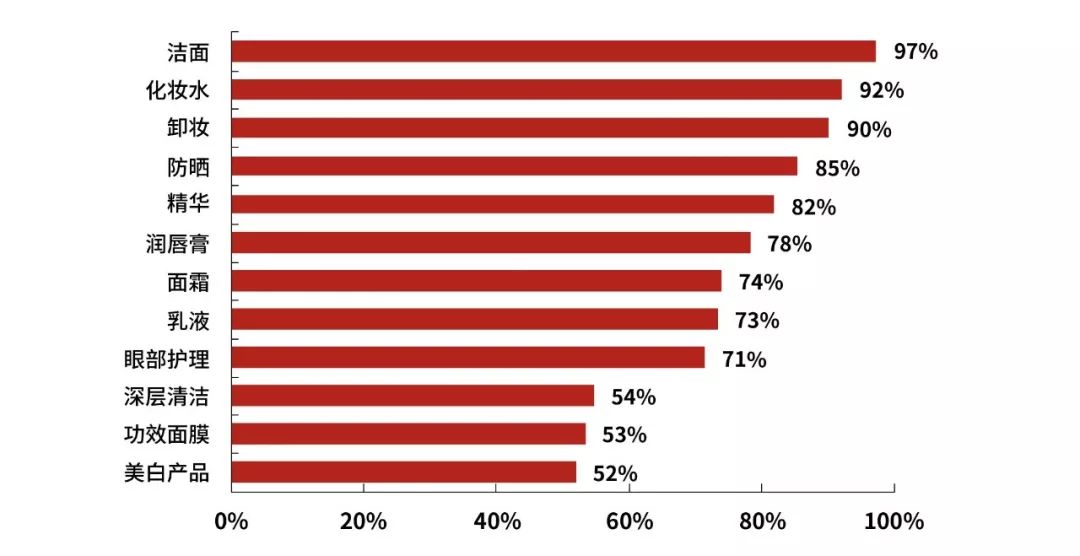

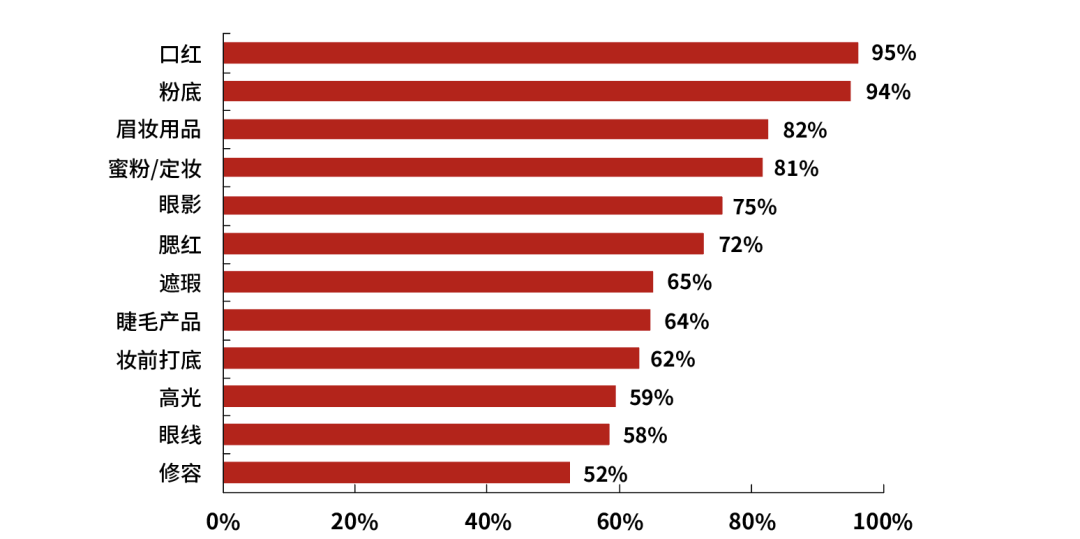

The subdivision of cosmetic products is rare and meticulous. Each sub-category has a scale of about 1-10 billion or even 5 billion, and the market space for subdivided products is still not small. In addition, the penetration rate of skin care products and make-up products has a huge room for improvement. The annual growth rate of the segmentation categories is large and needs close attention.

Figure: 2017 skin care product category penetration rate

Source: 2017 Micro-Appreciation Survey, Guosheng Securities

Picture: 2017 Cosmetics Product Category Permeability

Source: 2017 Micro-Appreciation Survey, Guosheng Securities

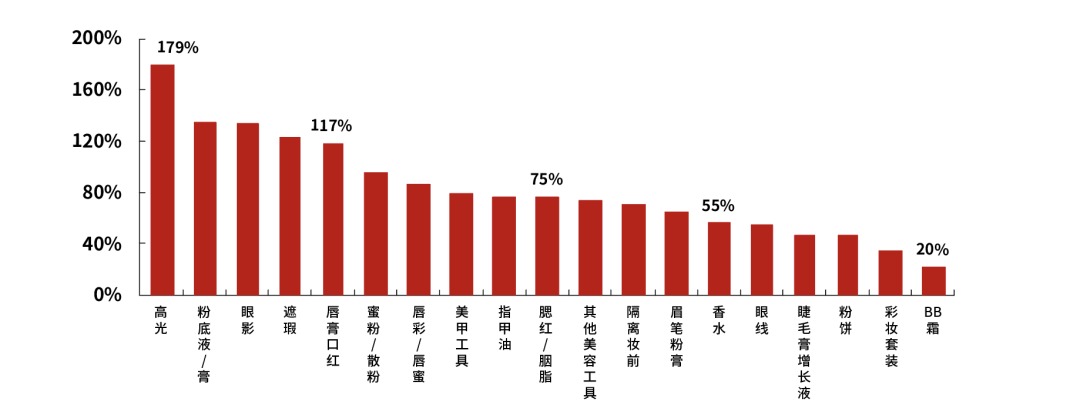

The growth rate of cosmetics category is also high and the annual difference is also large, so you can pay close attention to it by means of data. One of the main functions of Taobao’s category Xiaoji is real-time monitoring, and organize activities/promotions/new concept promotion in advance according to changes.

Photo: 2017 makeup products growth rate

Source: Cloud View Data, 2017 Tmall Makeup Perfume Data Report, Guosheng Securities

In the face of such a high degree of market segmentation, it is difficult for a single brand to have a strong single product in each category. The full coverage is difficult to succeed, and it is the best choice to create a burst or even a classic. At the same time, product innovation, category innovation, and concept innovation are all new.Xing Enterprise to create the core way of explosion, the phenomenon of the explosion of the product category BB cream innovation is a representative case of the industry.

From the point of view of the single item, the explosion is necessary for the start-up phase. How to precipitate into a classic model is a problem that plagues entrepreneurs. Not only the market leader, but also the up-and-coming talents are sticking to the explosion strategy and creating their own star.

From the cosmetics group, the multi-brand (>20) matrix is the only way to become bigger and stronger. L’Oréal owns nearly 50 brands (L’Oreal Paris, Lancome, Kashi, Obiquan, Vichy, Keyan, La Roche-Posay, Maybelline, etc.); Estée Lauder also owns as many as 29 brands (Essence Lancome, Clinique, TomFord, LaMer, DKNY, etc.) ).

China Head Cosmetics Group’s single or second brand sales accounted for a high proportion, long-term growth may have ceiling: Polaiya’s main brand in 2016, Polaiya contributed 88% of revenue; Royal Mufang’s main brand in 2017, Yumifang contributed 70% of the revenue; Baiqueling Group’s main brand Baique Ling has a sales of 13.8 billion in 2016. The rest of the brands such as Sanshenghua, Qiyun and Haizhiji are almost unknown. Shanghai Shangmei mainly relies on two main brands: Han Shu and Yiye. The Jialan Group relies mainly on nature and beauty. Brand.

According to CBNData, there are about 3,500-4,000 major cosmetic brands in the world, except for the brands owned by the CR10 Group (38.5% of the market). The remaining 3,000+ brands compete for 61.5% of the world’s share, and the long tail effect is significant. After the 90s, the small and beautiful brands favored by consumers are rising.

Figure: The penetration of small and beautiful brands is further improved

Source: Ali Platform, CBNData, Zhongtai Securities

In addition to the high degree of subdivision and concentration reduction, consumers’ beauty thinking, brand low conversion/attempting costs provide opportunities for small brands and domestic brands to rise.

In the market of Volkswagen vs. high-end, beauty vs. a total of four, the market concentration of the public + beauty market declined particularly sharply. CR5/CR10 decreased from 36.1%/49.7% in 2008 to 2017 respectively. 30.2%/44.9%, CR20 dropped from 61.7% in 2014 to 59.8% in 2017.

Figure: CR5/CR10 changes in the mass and high-end markets

(Note: The true single-brand dimension will be more dispersed by brand group here)

Source:Euromonitor, Huatai Securities

Compared with the high-end market that requires brand accumulation, in the mass market, the emergence of domestic brand groups and small brand groups.

The internationally renowned cosmetics companies in the high-end market rely on strong brand status and strong financial strength, which mainly occupy the high-end cosmetics market in China’s first-tier cities. Today, in the outbound travel and the emergence of Haitao, this brand has gained further momentum. strengthen.

When most domestic brands rise, in order to avoid competition in first-tier cities and international brands, relying on cost-effective advantages and in-depth understanding and rapid response to Chinese consumers’ consumption habits, they chose the channel leading and the first to sink the third and fourth lines. The market, relying on operational capacity enhancement, has seized a portion of the international brand market share. But this also indirectly leads to low product and brand positioning.

Picture: Changes in CR10 in the beauty market (based on group sales)

Source:Euromonitor, Billion Power

The channel has changed dramatically, and the new wave of grass-growing goods has been launched

1. Changes in channel structure have brought opportunities for overtaking in corners

Main sales channels for cosmetics (by market share)