In the next five years, a new era of smart cleaning is coming.

First, the era of family smart cleaning is coming soon

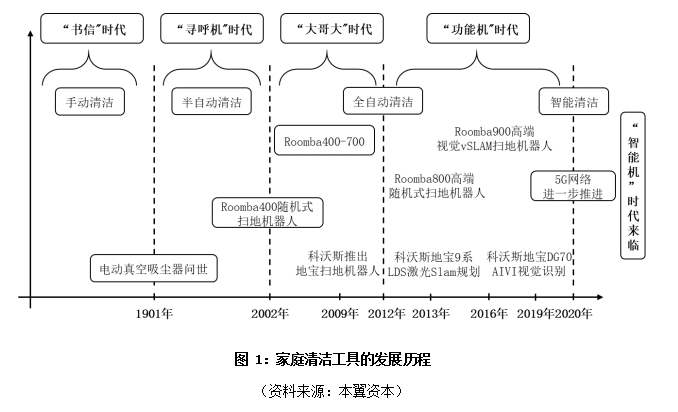

Family cleaning is a just-needed problem in family life. Since the industrial revolution, with the development of science and technology, the family cleaning methods have undergone many changes. Macroscopically, in the major countries of the world, household daily cleaning tools have basically completed the evolution process from manual to semi-automatic to fully automatic.

In 1901, British engineer Hubert Booth invented the world’s first electric vacuum cleaner. By the 1990s, the popularity of vacuum cleaners in developed countries and regions such as Europe, America, and Japan had exceeded 90%. In 1996, based on the principle of vacuuming, Swedish appliance giant Electrolux invented the world’s first sweeping robot, Trilobite, and mass production in 2001. In 2017, the penetration rate of sweeping robots in the United States reached 10%, and it is about to enter the turning point of rapid growth.

In China, due to the short history of development, electric vacuum cleaners were used in small batches in the 1950s. It was not until the 1990s that the entire vacuum cleaner market began to enter the initial stage. Ningbo Fidelity, Cobos, and Aipu Electric appeared. A group of early-stage entrepreneurs such as Chunhua Electric Appliance Co., Ltd., the annual output of vacuum cleaners in the domestic market reached 1.28 million units in 1995, of which the export volume was close to 50%.

In 2017, due to the development time and population, China’s vacuum cleaners have only 8 households per 100 households, and the penetration rate is much lower than that of developed countries such as the United States and Japan. However, since the 21st century, with the development of the national economy, the improvement of people’s living standards and the rise of the 80s and 90s of the new generation, China’s consumer market has begun to demonstrate its strong spending power and ability to accept new things. In 2009, Cobos launched the first generation of “Dibao” sweeping robots from the vacuum cleaner OEM business. In 2018, the sales volume of its brand robots has exceeded 3.5 million units, while the sales volume of the industry’s big brother iRobot has only reached 4.5 million units. . According to Zhongyikang data, in 2013-2018, the sales volume of sweeping robots in China’s domestic market increased from 570,000 units to 5.77 million units, and sales increased from 800 million yuan to 8.66 billion yuan, both of which achieved more than 10 times growth.

From the specific development history of the domestic and international household cleaning tools market, the first generation of household cleaning tools are the original brooms and mops, which require people to clean manually. The second industrial revolution brought mankind into the electrical age, mastered the power generation and electricity technology, and provided the technical foundation for the emergence of electric vacuum cleaners. In this context, the second generation of household cleaning tools has been upgraded to a semi-automated electric vacuum cleaner with improved cleaning and cleaning efficiency. Since the third scientific and technological revolution, the development of electronic computer technology has enabled the machine to have the processing and processing capabilities. The third generation of automatic sweeping robots came into being. It is equipped with various sensors such as infrared and ultrasonic to make it anti-collision, ranging and turning.To the basic movement and perception.

From the product evolution route of iRobot and Cobos, two sweeping robot leading enterprises, with the development of new technologies such as artificial intelligence, cloud computing and big data, the sweeping robot itself is undergoing three stages of product intelligence. upgrade.

The first phase was from 2002 to 2012. The main product form was a random collision type sweeping robot, which improved the coverage of ground cleaning through repeated cleaning. At this stage, the US iRobot company took the world’s leading position with its original random-type sweeping robot Roomba400-800 series. The Roomba800 series was launched in 2013. It can be said that it is the ultimate form of the first stage sweeping robot. On the one hand, the cleaning ability of the motor, battery, roller brush and other components has been upgraded to the highest level at that time. The wall realizes the segmentation and navigation of the working area of the sweeping robot, which improves the cleaning efficiency to some extent.

The second phase is 2012-2020. Based on gyroscope inertial navigation, laser SLAM, visual VSLAM and other technologies, the cleaning method of the sweeping robot is upgraded from random cleaning to planned cleaning. Based on the sensor-based upgrade, the sweeping robot at this stage has a preliminary level of intelligence. By constructing a map of the home environment, it realizes the positioning of its own positioning and cleaning route, and solves the problem of repeated cleaning of the random collision type sweeping machine. , further improving the cleaning efficiency and user experience.

As the product technology matures, the second stage of the sweeping robot market has clearly differentiated. iRobot still maintains its leading position in the high-end market. Domestic brands such as Cobos and Stone Technology are based on the advantages of China’s domestic industrial chain. High cost performance accounts for most mid-markets. Pu Ruike, Fengrui, Jiaweishi and other brands adopt gyroscope inertial navigation, and the planned sweeping robot has achieved a price of less than 500 yuan. It has successfully entered the sinking market and has performed extremely well in the sales of many e-commerce platforms. In addition, the traditional home appliance giants such as Midea and Haier are also eyeing, and product positioning is also aimed at the low-end market. From the perspective of technology upgrade, gyroscope inertial navigation belongs to the primary scheme of planned navigation. Laser Slam is a mature solution for universal application. The visual vSlam solution is limited by the current network, power consumption, processing power and other factors. Currently, it only has positioning navigation function. However, from the perspective of functional scalability, it is obvious that the visual vSlam solution is more imaginative.

The third stage is after 2020, the time node is a large-scale commercial use of 5G network. Based on cloud computing technology, it can make the sweeping robot realize real intelligence with various sensors such as vision and hearing. The next stage of the intelligent sweeping robot will need to process a large amount of information, and with the visual and auditory modules, the images, videos, voices, etc. will be acquired.A great burden on local computing and storage. The large-scale commercialization of 5G networks will solve the current data transmission problems of sweeping robots, making real-time stable cloud processing possible.

In this context, the sweeper industry pattern may evolve in two directions: First, the current machine manufacturers may be more focused on the electromechanical part of the sweeping robot body due to technical limitations, namely, motion, control, and cleaning modules. R & D and manufacturing, and intelligent modules such as visual, auditory, infrared sensors, cloud computing platforms and local edge processors cooperate with ICT giants such as Ali, Amazon and Huawei. Second, random, planned sweeping robots will continue to maintain a certain market share with high cost performance, but as the third generation of intelligent sweeping robot products matures, they will be phased out.

Comparing the development history of the mobile communication industry, the traditional broom and mop is like the original letter, and the vacuum cleaner is equivalent to the popular pager (BB machine) in the 20th century. The first generation of random sweeping robot appeared in 1998-2002. Let the family clean into the era of “big brother”, the planning sweeping robot that began to be popular around 2012 represents the era of “function machine”.

In the next five years, on the one hand, with the breakthrough and advancement of cutting-edge technologies such as 5G network, intelligent vision, intelligent voice, cloud computing, etc., the sweeping robot can realize the collaborative operation of cloud intelligence and edge intelligence; on the other hand, its motor The upgrade of the electronic control system will bring about a significant improvement in cleaning ability and efficiency. The intelligent cleaning robot produced by the combination of the two is the real “smart machine”, and a new era of intelligent cleaning is coming.

Second, from the market performance, the evolution of the sweeping robot industry pattern

In 2002-2012, the first stage of the random sweeping robot belongs to the initial stage of the product, which can only meet the needs of household cleaning. Due to the low level of intelligence, the cleaning efficiency and experience of the product are not optimistic. This stage is basically in the state of iRobot. In 2010, the revenue of iRobot family robots only reached 229 million US dollars, which can basically represent the global market size.

Since 2012, with the advent of planned sweeping robots, the cleaning ability and user experience of their products have been qualitatively improved compared to the first generation of random sweeping robots, bringing the growth rate of the entire industry market. Upgrade.

In the same period, brands such as Cobos, Pusannik, and Fumart began to open the Chinese market, and Cobos relied on its “ground”.”Bao” series of sweeping robots quickly occupied the Chinese market. According to Cobos’ prospectus data, in 2014, the domestic sales of online sweeping robots accounted for the top four brands: Cobos, iRobot, Pusannik and Fumart. The values are 37.2%, 15.0%, 9.7%, and 7.5%, respectively; the sales of offline channels account for the top four brands: Cobos, iRobot, Format and Philips, respectively, with values of 53.4% and 16.5%, respectively. 8.8%, 5.0%. Regardless of the online and offline channels, Cobos has an absolute leadership position.

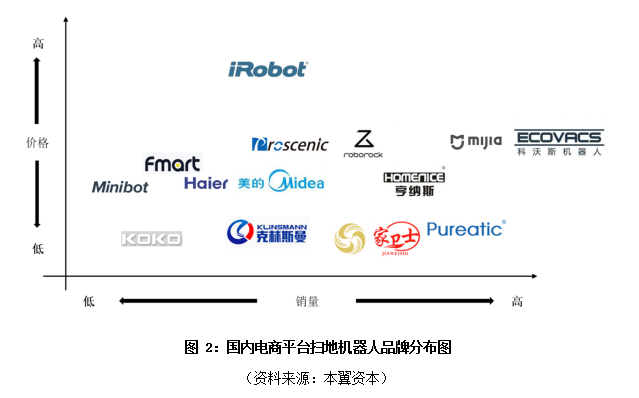

From the sales situation of Taobao, Jingdong and many sweeping robots in the main domestic e-commerce platform, the high-end sweeping robot is only a brand of iRobot. The sales price of the products is in the range of 2500-5000 yuan. At present, the cumulative sales of the whole platform is less than 6 Wantai, mainly based on Taobao and Jingdong platforms. The mid-end model price is positioned at 1000-2500 yuan, the brand competition is fierce, Cobos sales are far ahead, and DJ35, DD35 and other models have sold more than 400,000 units in the Tmall flagship store, followed by Mijia. Its flagship product, the Mijia sweeping robot, has accumulated more than 450,000 units in the Tmall platform. Other brands such as Stone Technology, Hennesss, Midea, and Pusangnik sold about 100,000 units. The low-end models are mainly active in multi-platform platforms, and the price is positioned at 200-500 yuan. The main planning-type sweeping robot products using gyroscope navigation are popular. Popular brands include Pureatic, Home Guardian, Fengrui, etc. The sales volume is 10 Ten thousand orders of magnitude.

Comprehensively, iRobot currently dominates the European and American markets. Cobos has a dominant position in the Chinese market, but the competition in the low-end and mid-end markets is still fierce, and there is no strong brand at the monopoly level. According to the above, the current cleaning robot is in the era of “functional machine”. Its cleaning ability and efficiency are not enough to completely replace the traditional broom, mop and vacuum cleaner. Now Cobos and iRobot are like Nokia and Motorola in the mobile phone industry. Whether it is possible to continue to maintain a leading position in the “smart machine” era is still unknown. From the historical experience, the “Apple” and “Huawei” of the sweeping robot industry may still be in the bud.

III. Research on leading companies at home and abroad

3.1, Cobos

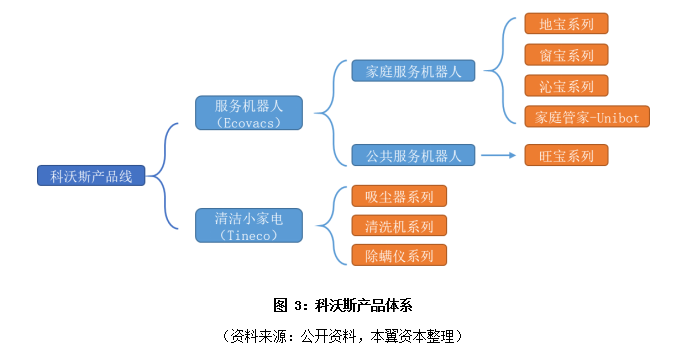

Kovos is a domestic sweeping robot, rubbingA leading company in the development, production and sales of household cleaning tools such as window robots and wireless hand-held vacuum cleaners. The company was first established in 1998. It started with the foundry service for cleaning small household appliances. It has formed a sweeping robot “land treasure”, window cleaning robot “window treasure”, air purification robot “Suibao” and clean small household appliance brand. A series of household cleaning products such as TINECO”. In May 2018, the company was listed on the A-share market with an issue price of 20.02 yuan/share. As of now, the company’s share price is 22.4 yuan and the total market value is 12.644 billion yuan.

Development history:

According to the company’s development history, its business layout can be divided into three phases:

The first phase was 1998-2006, which was the company’s original accumulation period. At this stage, the company mainly focuses on the OEM business of household cleaning small household appliances such as vacuum cleaners. From the beginning of the unknown brand to the founding of famous brands such as Philips, Panasonic and Electrolux, the company became a labor-intensive OEM in Suzhou. Representatives, and during this period, accumulated foreign patents and core technologies that cracked many high-end household vacuum cleaners.

The second phase was 2006-2016, which was the company’s cleaning product business. Under the influence of companies such as Electrolux and IRobot, the company has been investing in the development of household cleaning robots based on sweeping robots since 2006. In 2009, 2010 and 2011, the company launched the “Ground Treasure” series and air purification robots respectively. The “Suibao” series and the window cleaning robot “Window Po” series products have completed the overall layout of the household cleaning robot.

According to the data of Zhongyikang Market Research Institute, Cobos sweeping robot has occupied the dominant position in the domestic market since its launch. In 2012-2013, the domestic market share of Cobos sweeping robot retail sales was 60.8% and 63.7 respectively. %, while the second-ranked Fomat retail sales accounted for only 19.5% and 12.1%. In the international market, the company has set up branches in Germany, the United States and Japan since 2012, and has successfully developed Spain, France, Canada, Malaysia and other countries and regions, forming an international marketing centered on Europe, the United States and Japan. Service Network. On the other hand, based on the original accumulation of the company’s vacuum cleaner OEM business, the company’s clean small appliance brand TEK launched the first generation of fully intellectual property wireless handheld vacuum cleaner AK47 in 2013, and was named “The Best Vacuum Cleaner of the Year” by China Household Electric Appliance Research Institute. . Since then, the company has launched two products, wireless floor washers and wireless mites, which form a direct confrontation with the famous British brand Dyson.

The third phase, from 2016 to the present, is the transition period for the company to expand its complete product line for mid- to high-end products and service robots. As the clean robot market continues to heat up, competition is becoming more intense. In 2013-2017, Cobos sweeping robots have a comprehensive market share in China by 63.7% fell to nearly 50%, iRobot, Pusannik, Laike Electric, Midea, Xiaomi and other companies took turns to seize the market. In this industry background, the company invested in a number of software and hardware companies based on artificial intelligence technology, and on the other hand established the Cobos (Nanjing) Artificial Intelligence Institute in 2018 to carry out machine vision and depth. Learn and develop a number of AI technologies, upgrade the added value of their cleaning robots and small home appliances, and upgrade to the mid-to-high end. In 2016, the company launched the butler robot Unibot, which integrates home appliance control, security, patrol and cleaning. It evolved from a single-function cleaning tool to an integrated multi-functional family intelligence “housekeeper”. In addition, the company began to enter the public service field, launched the commercial service robot Wangbao, achieved landing in the banking, judicial, retail and other scenarios, and improved the overall product layout of its service robot.

Developed to this day, Cobos has experienced two business transformations from vacuum cleaner OEM to self-developed cleaning robots and small appliances to extended service robots. The home robot scene products are gradually integrated into one, with a single cleaning tool. Upgrade to intelligent central control housekeepers, public service scenarios, and launch commercial service robots based on the technology of cleaning robots to lay out the potential toB service market in the future.

Product:

As of now, after two business transformations, the company has formed two series of product lines: service robot brand “Corvos” and clean small appliance brand “TINECO”. Among them, service robots include home service robots and public service robots. Home robots are mainly clean, including Dibao series, window treasure series, Sic Bo series and butler robot Unibot, which cover sweeping, window cleaning and air. Purification; public service robots are mainly based on the Wangbao series, with various functions such as face recognition, voice interaction, and security patrol. The clean small appliance brand “TINECO” is a sub-brand of Cobos. It was derived from the vacuum cleaner OEM business during its startup period. It now has three product lines: vacuum cleaner series, washing machine series and sputum series.