They are the most worthy of attention in 2020.

Editor’s note: This article is from WeChat public account “Guotai Junan Securities Research” (ID: Gtjaresearch), author Guotai Junan Consumer Team. The original title “Guotai Junan nine consumer groups annual strategy: 2020, the consumer industry’s “small leading era””

The A-share market in 2019 is an industry giant in the consumer sector.

From Guizhou Maotai to Haitian Weiye, from Hengrui Medicine to Midea Group, investors no matter how to choose stocks, they are better off holding these leading stocks to obtain “stable happiness”.

After the stock has been taken for a long time, it is easy to produce feelings. It is inevitable that the “leading theory” will be more and more convincing – the most beautiful and the highest.

However, Mr. Market’s favorite is to give investors the unanimous expectation of “a big stick”. Especially when the position is adjusted at the end of the year and the beginning of the year, it is the time when the style switching is frequent.

The annual strategy of the Guotai Junan Nine Consumers Group, “The Age of the Consumer Industry”, gives its answer to the next stage of the market hotspot –

The era of the faucet is not over, but it is more necessary to carefully select the 28 small consumer companies that have been summed up. They are most worthy of attention in 2020.

01 Consumer white horse continues to strengthen,Market concerns three points

Since the beginning of this year, the share price of consumption Baima, represented by Guizhou Maotai, Wuliangye, Haitianweiye, Gree Electric Appliances and Midea Group, has hit record highs, and has gone out of a round of value return market and gained a high degree of market attention.

But the market has come to the present, the market is increasingly worried, there are three main points:

1, is the valuation too high

From the valuation point of view, the large consumer sector is relatively high in both PE and PB.

For example, the PE in the food and beverage industry is 32.17 times, reaching 68% of the historical percentage. The PB is 6.5 times, reaching the historical percentile of 81%. The price-earnings ratio of the segmented liquor sector is much higher than the historical average. The valuation of home appliances, automobiles, agriculture, forestry, animal husbandry and fishery is not cheap, PE is 22.13 times, 23.89 times, 34.22 times, reaching 58%, 56% and 41% of the historical percentile.

But we believe that from the macro, industrial and micro level, the consumer industry can no longer simply value the P/E ratio, but should change from PE to DDM model. It used to give “growth” valuation, the future. It is a valuation of “competitive advantage.”

Further reading: consumer industry “core Assets, stocks are too expensive?

2. Will the group warm up?

From the perspective of market transactions, the hotspot of the organization’s consumption of white horses reached a historical high.

In the case of public funds, the positions of public offerings in the past three years have continued to tilt toward the core assets of A-shares. The share value of the top 50 stocks has risen from 27% in 2016 to over 50% today. Breaking through the record high, the white goods in mass consumer goods and home appliances in food and beverage are also at a historically high level.

However, we believe that the consumer industry is a long-term industrial investment logic. If there is no sustained lower-than-expected or extreme external events, it is difficult to break the group.

3. “Reduce consumption, increase technology” phenomenon, consumer stocks will be cold

From the perspective of holding positions in the third quarter of 2019, the fund did appear to reduce the consumption of warehouses and technology. However, we believe that it is normal for the consumer sector to increase its holdings in the previous period. The rise of technology stocks will not cause consumer stocks to collapse, but it may affect the excess returns of consumer stocks.

02 The consumer industry enters the second half

In 2020, the investment outlook of the Chinese consumer industry can be summarized in two sentences:

Supply to see efficiency:

From the supply side, the growth of China’s consumer industry has entered a stage of squeeze growth. The competition among enterprises is more reflected in the competition between efficiency, and the efficiency is reflected in the management ability of the enterprise and the management team. competition.

Therefore, leading companies with high operational efficiency and strong competitive advantages can grow by squeezing the market share of SMEs.

Requirements to see bonuses:

From the demand side, despite the overall slowdown in macroeconomic growth, the demographic dividends of third- and fourth-tier cities continue. These cities have a large population baseThe income growth is fast and the marginal consumption tendency is high. Most of them are in the stage of mass consumption and brand consumption, which brings huge development space for liquor, snacks, beauty, tax-free, sports, recreation, outdoor sports and other sub-segments.

We can testify from the performance of the 11th Golden Week in 2019. According to Jingdong Big Data, the amount of orders placed in the 11 low-tier cities (3-6 lines) increased by an average of 20%, which is higher than that of first- and second-tier cities. In addition, service consumption has soared, and tourism, tax-free, catering, and movies have been fully presented. trend.

03 Why is the consumer faucet more dominant?

Looking forward to 2020, we believe that the investment hotspots in the consumer industry may gradually move from big taps to small leaders in some segments.

The revenue and market value of these companies may not be as big as the big ones, but the industries they are in are in a fast-growing period and have certain demand dividends. In these subdivided fields, small leading enterprises are rapidly gaining market share by virtue of their competitive advantages, and the industry competition pattern is becoming clearer.

With long enough track and enough wet snow, these small leading companies are showing the potential and style of growing into an industry giant.

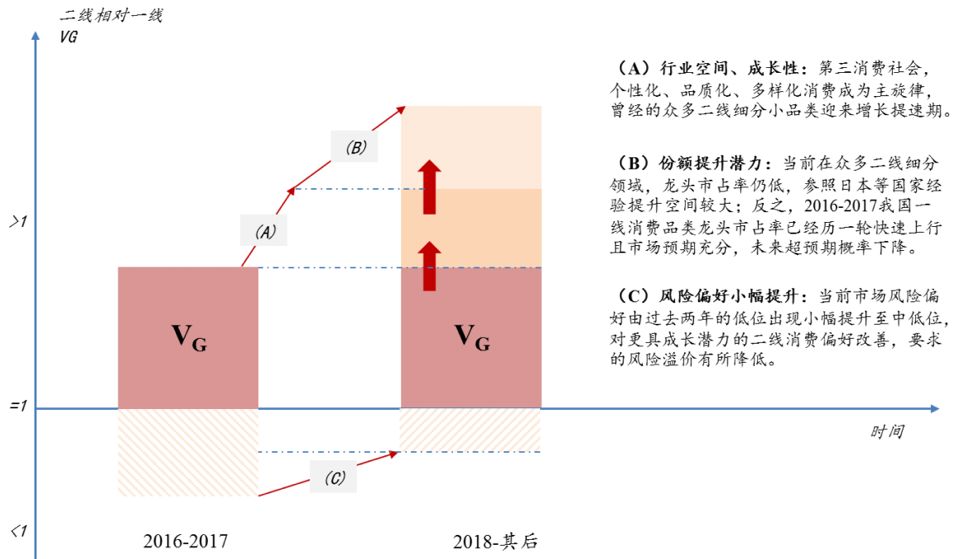

From the “trilogy” created by the value of consumer goods companies, the value of the enterprise V = the value of the asset VB + the value of the profit VF + the value of the growth VG, and the growth value of the small leader VG is better.

Further reading: Huang Yanming: consumer goods companies rely on What creates corporate value?

The reasons are as follows:

1 As China enters the third consumer society, individualized, quality and diversified consumption become the main theme, and many small-scale leaders are welcoming the growth acceleration period, which promotes the rapid improvement of the small faucet VG relative to the super faucet. ;

2 The market share of current small faucets in their respective fields is still low. With reference to the experience of countries such as Japan, there is a large room for improvement, while the market share of super faucets (such as liquor, home appliances, etc.) has experienced a rapid upward trend, and the market expects sufficient. ;

3 The current market risk appetite has slightly increased from the low level in the past two years to the middle and low level, and the preference for the growth potential leader is improved, and the required risk premium is reduced..

▼ Consumer faucets dominate, key is the value of growth VG is faster than super faucet

Data Source: Guotai Junan Securities Research

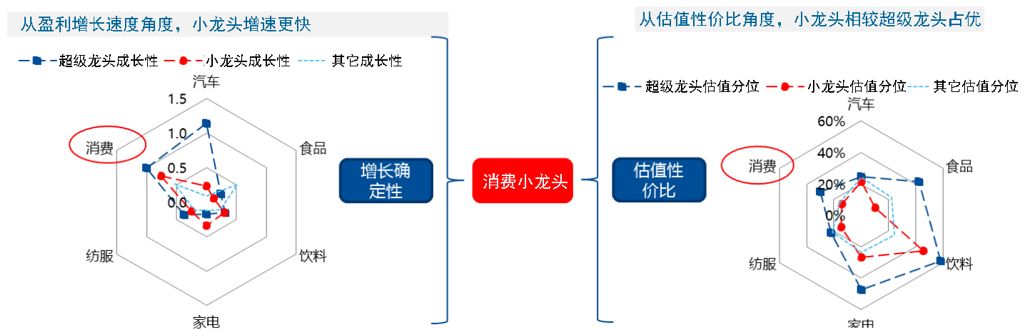

At the same time, consumer faucets have both profit growth and valuation.

Compared with the super faucet, Xiaolong’s profit growth rate is faster, fully enjoy the industry’s high growth dividend and competitive advantage to enhance the market share. Although the leading company has high profitability, the growth rate is limited, and after a round of valuation and repair, the valuation level and the small leader are not much different.

Therefore, if the valuation level is considered by PEG, the valuation of the small faucet is significantly higher.

▼ Consumers’ profit growth is faster, valuation is significantly higher than price

Data Source: Wind, GTJAS securities research

Taking the leader of the beauty and manufacturing industry as an example, while the industry is developing at a high speed, the company continues to increase its market share by relying on integrated marketing and product development advantages, and its performance is accelerating.

Further reading: explosion models Beauty Brand Behind the scenes “contributors”

Cosmetics is an early stage industry in large consumption, and the industry is still in a period of rapid growth, especiallyIn the past few years, Xiaohongshu, Vibrato has educated consumers and activated many low-line urban consumers to become Internet users. Cosmetics have accelerated penetration from the first and second lines to the third and fourth lines, and the per capita use amount has also been increasing. This brings great opportunities to domestic brands.

壹 壹 壹 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012 2012

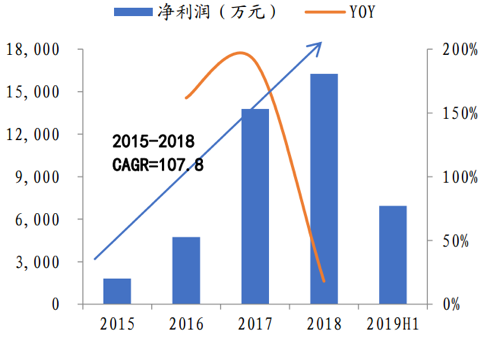

In recent years, the company has added domestic and foreign heavyweight customers such as Procter & Gamble, Neutrogena, Elizabeth Arden, Amore, Herborist, etc. The outstanding achievements highlight the company’s unique advantages in integrated marketing and product development, and after the IPO is listed, The company’s financial strength has further improved and is expected to accelerate the expansion of its customers.

▼ The company provides a generation of operational services for multiple beauty brands

Data Source: Company Prospectus, Guotai Junan Securities Research

▼ Company performance maintains rapid growth

Data Source: Company Prospectus, Guotai Junan Securities Research

04 What other industry leaders?

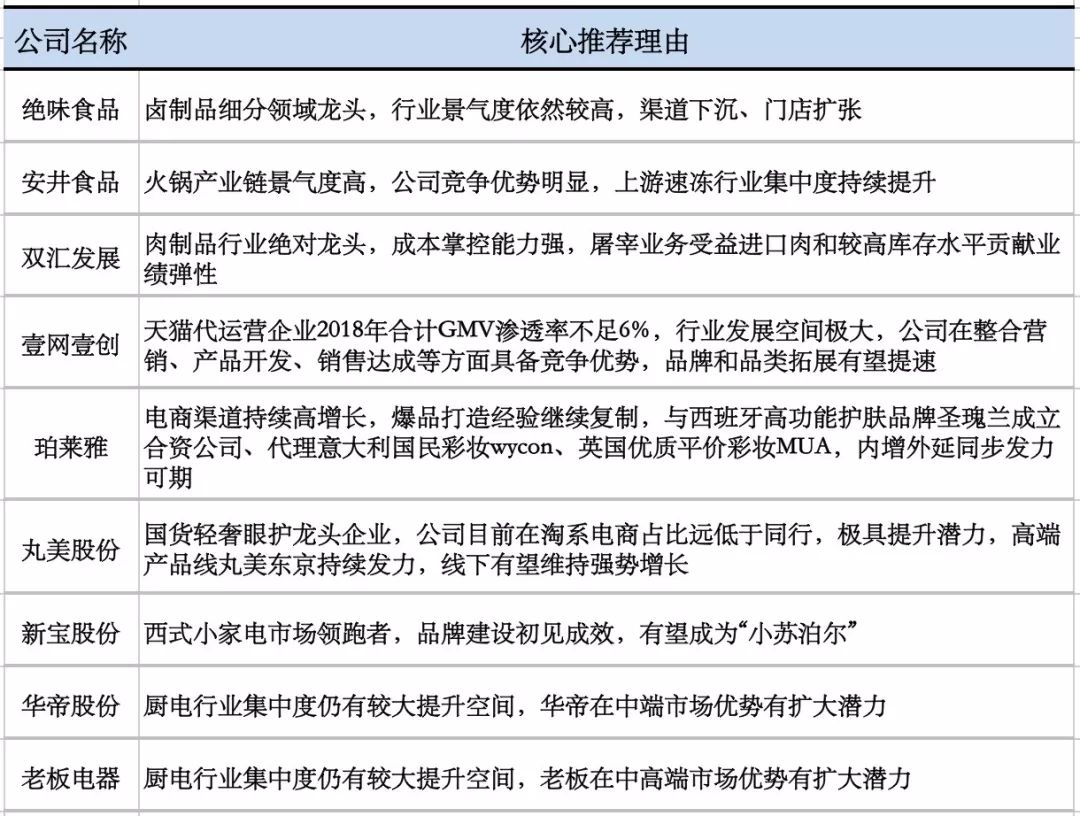

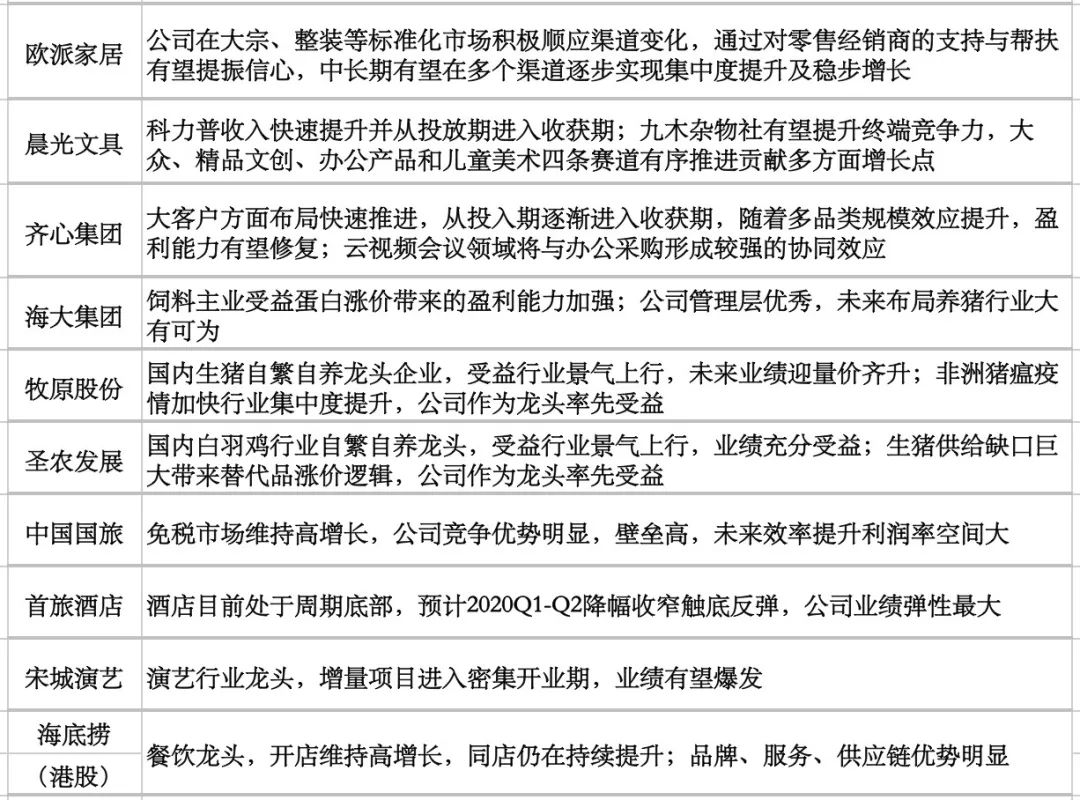

Guotai Junan’s nine consumer industry research teams (food and beverage, commercial retail, home appliances, agriculture, light industry, social services, automotive, textiles, media) selected 28 consumer goods small leading enterprises, the core recommendation reasons are as follows Show.

▼ Guotai Junan selects 28 consumer taps

Data Source: Guotai Junan Securities Research Institute

In terms of industry:

Commercial retail: mandatory consumption is still strong, domestic products rise to cosmetics boom

The Chinese cosmetics industry is still in a long-term accelerated growth stage, especially the rise of domestic brands will be the future trend.

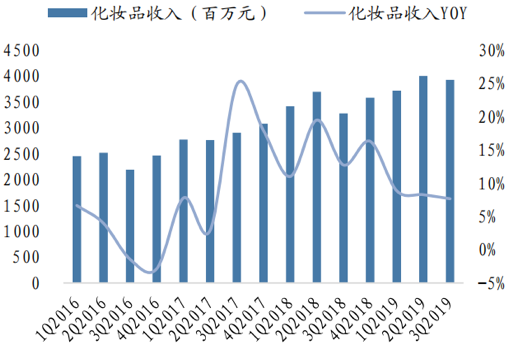

Industry data continued to improve. The retail sales of cosmetics above the zero limit were +12.8% from January to September, ranking the highest among consumer goods. Throughout the optional consumption, the cosmetics crossing cycle attributes have become more and more recognized by the market.

▼The cosmetics industry’s revenue has grown steadily

Data Source: Wind, GTJAS securities research

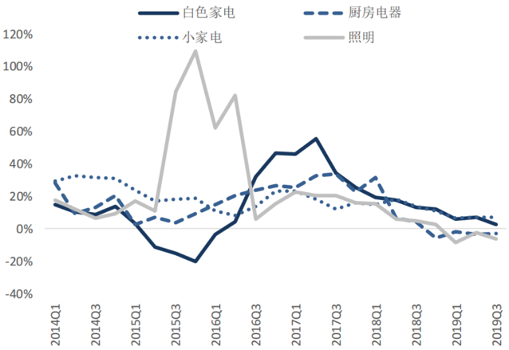

Home Appliances: From risk discount to deterministic premium, 2020 market can be

Industry valuation from risk discount to deterministic premium will become the main theme of the market at the end of the year. In 2020, the home appliance industry will become one of the most eye-catching sectors.

We believe that the key to the current home appliance market is three certainty:

1. Industry growth will not be further determined by a significant downside.

2. The competitive landscape is stable to a good certainty.

3. The certainty of the further expansion of the competitive advantage of leading enterprises.

▼ White TV, small household appliances revenue growth is better than kitchen appliances, lighting

The bottom line of the whole vehicle brings two results. One is that the profit pressure is transmitted to the parts to accelerate its growth, and the other is the domestic replacement acceleration. The segmentation leader with high bicycle value and significant cost advantage will grow rapidly. In addition, the gradual commissioning of Tesla’s Shanghai Volkswagen MEB platform will become an important catalyst for the new energy vehicle industry chain. It will increase the demand for cruising range and the promotion of new technologies such as car networking and automatic driving, and reduce the weight and electricization of auto parts. New energy and intelligence will be the main marginal increase in the industry.

Wovenwear: Continue to recommend stable, low-value, high-distribution faucets in 2020

The recent double 11 came to a close, sales, sports, children’s wear and down jackets, local brands perform well.

Sports field Anta launched IP and e-commerce special contributions, which were loved by consumers. The water consumption increased by 61.95% year-on-year to 1.83 billion yuan, continuing the high growth over the years. Balabala, the local brand in the field of children’s wear, won the first place in the list, and its leading position is stable. The downhole sales of the down jacket faucet Bosideng double 11 online exceeded 1 billion yuan, a year-on-year increase of 37%, of which Tmall flagship store revenue increased by 58% to 650 million yuan, becoming the first place in China’s clothing brand single store sales, indicating product optimization The effect is remarkable.

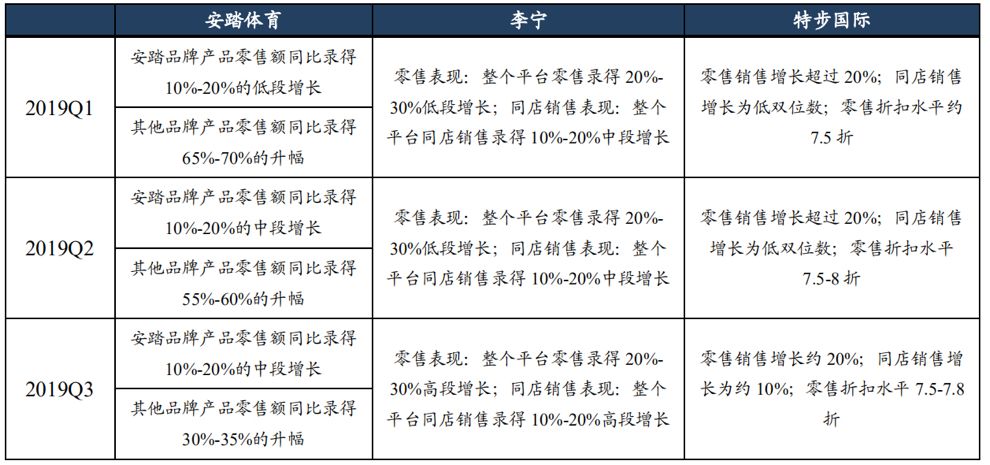

▼ 2019Q3 major sportswear companies, quarterly retail water maintains high growth rate

Data Source: Company Announcement, Guotai Junan Securities Research

Media: The marginal warming trend of the sector is expected to continue, and the opportunity will be 2020

Benefiting the National Day and “Youth”, the quality of the film is excellent. In October, the country achieved a box office of 8.16 billion, a record of innovation. On the other hand, the competition pattern of the Lunar New Year and the 20-year Spring Festival is gradually clear. The improvement in the mood of watching movies is expected to continue at least until the Spring Festival next year.

▼ Growth of CR5 concentration in cinemasEnhanced income-generating capacity of quality companies