Behind the golden age of mobile phone screens: technology change, player elimination, a new round of ranking battles!

Editor’s note: This article comes from WeChat public account “Smart stuff” (ID: zhidxcom ), The author Xuan window.

In 2019, the mobile phone screen industry has once again reached a new climax. Folding screens, waterfall screens, ring screens, surround screens, and dazzling screen forms have become a focal point of the mobile terminal war, and also a microcosm before the 5G mobile war.

As the physical carrier of video presentation, the screen industry is also ushering in a golden age. In the newly launched electronic consumer terminal products such as smart speakers and smart screens this year, the importance of screens continues to increase. The communication and terminal giants headed by Huawei have even sloganed “multi-screen collaboration”. The repair cost of a Huawei folding screen phone Mate X is as high as 7080 yuan. Due to limited supply, even the price of Huawei’s folding screen mobile phone Mate X was speculated to be 90,000 yuan by cattle.

▲ Ring screen of Huawei Mate30

Before the release of Huawei Mate 30, vivo released the vivo NEX 3 first, with a curved screen with an arc of up to 88 degrees, and named it waterfall screen.

▲ Waterfall screen of vivo NEX 3

In September this year, Xiaomi released a 100-megapixel 5G concept machine MIX Alpha, which is between curved screens and double-sided screens. The screen was launched in cooperation with domestic screen maker Visionox.

▲ Xiaomi concept machine MIXAlpha

It can be said that the competition in the smart phone industry’s screen field is intensifying, and major mobile phone manufacturers hope to make differentiated products to attract users and lead the industry development. According to the in-depth investigation of Zhixi stuff, the mobile phone screen industry is showing three major competition trends. The mobile phone giants located downstream are becoming important promoters of the research and development of new screen technologies and their promotion. A concert of vertical and horizontal killing of mobile phone manufacturers and screen manufacturers is starting!

Comprehensive screen, folding screen, waterfall screen, various mobile phone screens

In recent years, with the domestic smartphone market becoming increasingly saturated, the core technology competition has intensified under the leadership of mobile phone manufacturers. From chip to camera, from camera to screen, the upstream and downstream innovations in the mobile phone industry chain have continued.

< / p>

< / p>

▲ A weird full screen solution

Take mobile phone screens. As one of the most important core components of the mobile phone supply chain, after the wind of “full screen” in 2016, a variety of derivatives of full screens appeared, such as bangs screens, water screens, and pearls. Screens, as well as lifting camera designs and slider designs have emerged. For mobile phone manufacturers compete full screen, the intellectual stuff in the previous article ( The full screen of blooming heads has been thoroughly explored in the mobile phone company driven by madness ).

Subsequently, under the leadership of the mobile phone giant, the screen supply chain continues to “toss” new technologies. Since the end of last year, folding screens have become the industry’s latest technology vane. Mobile phone manufacturers want to show their technical strength with folding screens, and upload this pressure upstream, so that the screen supply chain started a difficult research and development journey. Production difficulties on folding screen technology, intellectual stuff before in the article ( The six deadly factors of the mass production dilemma of the mobile phone circle collectively turning around and hitting the street, folding screens at the bottom! ) have also been discussed in depth.

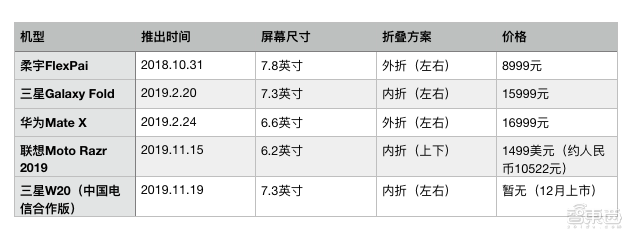

However, for the screen supply chain, this challenge is not just about meeting customer needs. If anyone can take the lead in conquering the folding screen, it also means getting more recognition from downstream mobile phone manufacturers. Interestingly, the folding screen mobile phones are currently launched by Samsung, Huawei, Lenovo and the upstream screen supply chain company Rouyujia. The screen suppliers are Samsung Display, BOE (Huawei and Lenovo folding screen suppliers) and Rouyu themselves.

< / p>

< / p>

▲ Folding screen phone released

In the second half of this year, large curved screens have become a new story that mobile phone manufacturers have begun to tell. Huawei Mate30 and vivo NEX 3 use curved screen designs with large arcs up to 88 degrees.

In addition to these mobile phone screen morphological changes, the innovation of other smart phone modules has also affected the mobile phone screen industry.

The most worth mentioning is the already mature, under-screen fingerprint technology. At present, the flagship phones of the four major domestic mobile phone manufacturers “Hua Mi OV” basically use fingerprint technology under the screen. The most common under-screen fingerprint recognition solution in the industry is to put a sensor under the screen of the mobile phone, and when the hand unlocks the fingerprint, take a picture of the user’s fingerprint and use AI technology for fingerprint recognition. At present, mobile phone manufacturers can already achieve regional fingerprint recognition.

Analog to fingerprint recognition under the screenOther technologies, in addition to the fingerprint module, affected by the full-screen “redundant”, mobile phone manufacturers and the supply chain are still struggling to overcome another solution-the screen camera.

As early as February of this year, OPPO showed a prototype of an under-screen camera at the MWC 2019 site. Zhiwu also experienced it in the field. Because of the screen and glass, the sharpness of the camera is lost. For today’s increasingly high pixel requirements for mobile phones (Xiaomi CC9 Pro is equipped with a 100 million pixel main camera), the sacrifice of pixels is obviously not acceptable to users. So far, the industry is continuing to explore under-the-camera solutions.

From the perspective of smart phone products launched by downstream mobile phone manufacturers, the articles surrounding small mobile phone screens can be described as varied. However, behind these mobile phone products with “different attitudes”, we see that the screen industry is ushering in a new period of industry oscillation.

Three major trends behind the screen industry oscillation

After an in-depth investigation of the industry chain, Zhixiong discovered three obvious trends that are hidden behind the screen industry oscillation: market share changes, technological route evolution, and some screen manufacturers being eliminated by core players.

To understand the changes in market share, let’s first look at the shipments of the mobile phone screen industry in recent years.

According to Sigmaintell data, global smartphone panel shipments in the first half of 2019 were approximately 840 million (Open Cell caliber), a decrease of approximately 5.2% year-on-year.

Let’s take a longer look and look at the market situation in the last three years.

In 2017, total global mobile phone display panel shipments reached 2.01 billion units, an increase of 3% compared to 2016. Among them, the LCD screen panel shipments were about 1.599 billion, and the AMOLED panel shipments were about 402 million.

As the full screen wind blows, the demand for AMOLED panels from smartphones has begun to increase. Since 2018, OLED screens have quickly occupied the flagship mobile phone market with their self-luminous, bendable, and good color rendering effects. In the smartphones released this year, OLED screens have almost become the mainstream of flagship phones, and only a few models still insist on using LCD screens.

< / p>

< / p>

▲ Note: The picture is from the Foresight Industry Research Institute

According to global authority in the field of displayAccording to DSCC (Display Supply Chain Consultants) data, from 2016 to the present, global OLED panel sales have maintained a rapid growth trend. In 2018, the global shipment of smart phone panels (OpenCell) was approximately 1.87 billion, which was affected by the decline in terminal demand, a decline of 6.1% compared with the previous year.

As the brand concentration in the complete machine market continues to increase, the panel supply chain market is also gradually concentrating.

In 2019, the entire mobile phone screen industry started in the state of folding screens. In the first half of 2019, global political and economic risks intensified, market volatility increased significantly, and the weak performance of the smart phone terminal market made the smart phone panel market also trend downward. According to Sigmaintell data, global smartphone panel shipments in the first half of 2019 were approximately 840 million (Open Cell caliber), a decline of approximately 5.2% year-on-year.

On the whole, the mobile phone screen market changes with the shipment of smartphones.

< / p>

< / p>

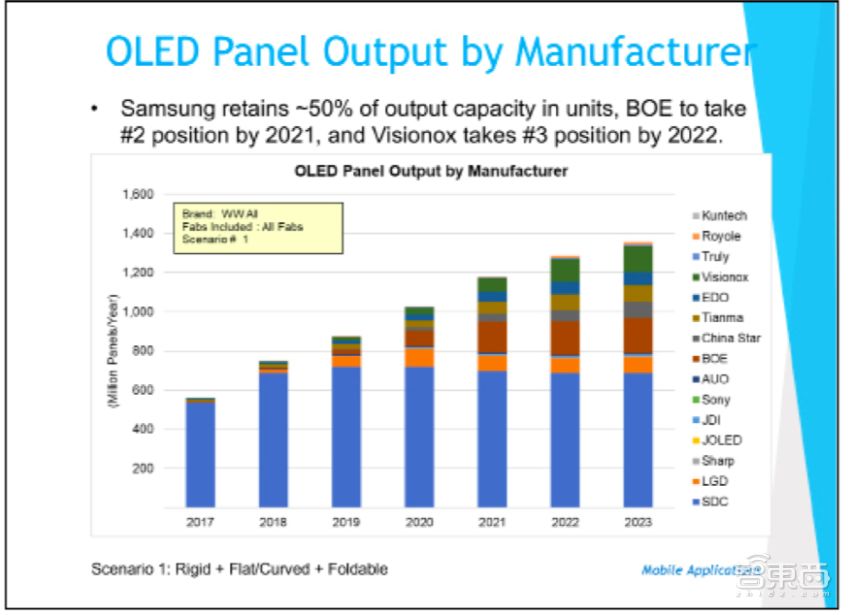

Panel research agency Display Supply Chain Consultants (DSCC for short) predicts in the 2019 LCD panel research report that by 2023, Samsung will still maintain a market share of more than 50% in the OLED field, and BOE will maintain its market share in 2021. Occupying the second position, another Chinese screen maker Visionox will occupy the third position in the market in 2022.

On the other hand, the screen technology route is undergoing changes.

The most obvious feeling is that OLED is squeezing the LCD market further.

On November 28, foreign media reported that Apple expects to launch three iPhone 12 models next year, all of which will use OLED screens instead of LCD screens.

< / p>

< / p>

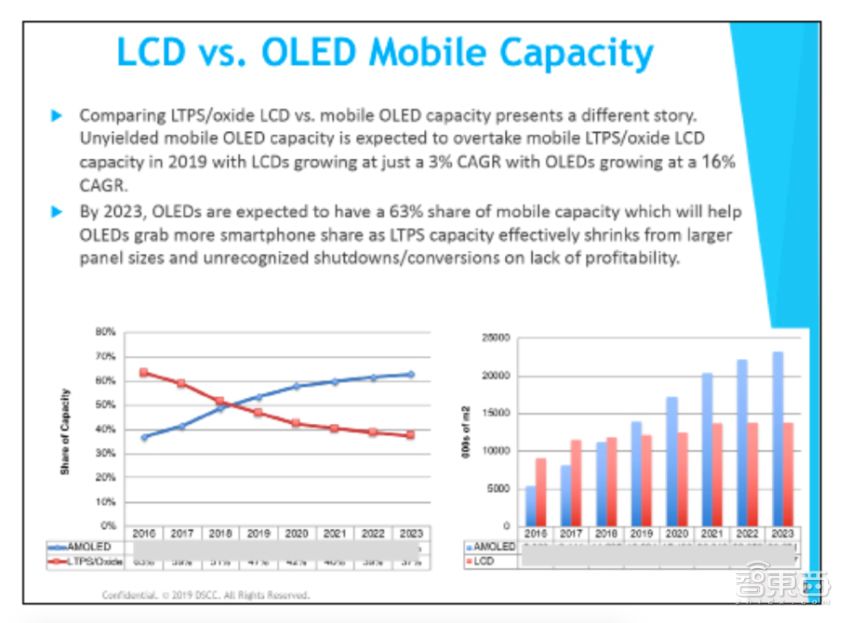

DSCC forecasts that in the field of mobile products, LCD compound annual growth in 2019The rate is expected to be 3%, and the compound annual growth rate of OLED is expected to be 16%. DSCC believes that by 2023, OLED will occupy 63% of the market.

In the first half of this year, BOE’s smart phone panel shipments exceeded 190 million pieces, a year-on-year increase of 23.1%. LCD panel shipments soared in March, with shipments of approximately 180 million units, a year-on-year increase of approximately 16.7%, and still the world’s largest LCD panel supplier.

Samsung ’s screen shipments were relatively weak in the first quarter. According to Sigmaintell data, its total smartphone panel shipments in the first half of 2019 were basically the same as BOE’s, also about 190 million pieces, an increase of about 9.6% year-on-year, but still occupy an absolute advantage in the AMOLED field.

Tianma ’s smartphone panel shipments in the first half of the year were approximately 100 million pieces, of which LTPS shipments exceeded 80 million pieces, ranking first in the global LTPS LCD shipments. In the first half of 2019, Tianma’s “punched screens” shipped close to 20 million pieces, occupying about 61.0% of the market in the LCD punched screen market, and is the main supplier of LCD punched screens.

However, the industry generally believes that OLED and LCD have their own advantages, and OLED will not completely replace LCD. Although OLEDs have gradually become the choice of more mobile phone products due to better contrast in mobile products such as mobile phones, in the field of TVs, LCDs have higher brightness and more competitive prices.

Look at the situation in the OLED market again.

According to the data from Qunzhi Consulting, the global smartphone OLED panel shipments in the first half of 2019 were approximately 220 million pieces, accounting for approximately 26% of the overall smartphone panel market, a year-on-year increase of approximately 18.6%. It is estimated that the shipment of OLED mobile phone panels will be about 490 million pieces.

No surprise in the market’s throne, it is still firmly occupied by Samsung. In the first half of this year, Samsung ’s AMOLED panel shipments were approximately 190 million, an increase of approximately 11.4% year-on-year, of which hard-screen shipments accounted for more than 60%. With the strong demand for OLED under the screen fingerprints and Samsung’s active promotion strategy, Samsung’s hard screen production line is still in short supply.

The domestic screen manufacturer BOE ranks second in the global smart phone OLED panel market, shipping about 10 million pieces, accounting for about 5% of the global market share, and is currently a panel manufacturer that can stably supply flexible AMOLED in addition to Samsung. .

During this turmoil, some manufacturers stand out, while others are on the verge of elimination and are entering a difficult situation.

The most typical example is Japanese screen maker JDI. Zhixi has previously published a detailed analysis of the situation of the JDI crisis ( < / p>

▲ Global smartphone market share in the third quarter of 2019

A few days ago, the analysis agency canalys released the latest smartphone market share report. The top five are Samsung, Huawei, Apple, Xiaomi and OPPO, which occupy a total of the world.67% of market share.

And more interestingly, in the context of the weak growth of the global smartphone market, mobile phone giants, on the one hand, have a large amount of banknotes, on the other hand, they want to continue to win in the market and choose to extend their tentacles to the depth of the industrial chain. , And screen manufacturers to launch technological changes.

Let’s take a look at Samsung, the “almighty” giant.

Samsung is the world ’s largest mobile phone maker by market share. It can also be called the “leading player” in the field of OLED screens. Among the OLED small-size panel manufacturers in the fourth quarter of 2018, Samsung ’s display sector accounted for 93.3% of the market, and flexible OLEDs accounted for 94.2%.

Especially in the field of OLED, Samsung has taken the lead in betting and monopolized the industry by buying out upstream materials and equipment. Smart stuff used to be in ().

Although Samsung is a large screen manufacturer, it has to rely on Japanese material suppliers in the upstream material field, and this year Samsung ’s screen has encountered unprecedented huge obstacles-Japan-South Korea trade friction. In July this year, the Ministry of Economy, Trade and Industry of Japan announced that starting from July 4, it will restrict the export of core upstream raw materials for Japanese semiconductors, core materials for displays such as smartphones and televisions to South Korea. This includes fluorinated polyimide, an OLED display component material used in the manufacture of foldable screens. Affected by the trade war between South Korea and Japan, Samsung’s OLED production line researchDevelopment progress has caused some impact.

Huawei rushed to the second place in the global mobile phone market. Despite facing force majeure, its market share maintained a rapid growth trend. In the choice of screen supply chain, Huawei has also suffered a big loss of Samsung ’s supply cut. With the rise of domestic screen manufacturers, Huawei now tends to choose multiple screen supply chains. With the increase of market share in recent years, Huawei is also continuously expanding the list of screen supply chain partners. For example, the mobile phone screen giant BOE is an important partner of Huawei, and this year ZTE and Xiaomi’s screen supplier Visionox also joined Huawei’s partner camp.

Apple defines the basic form of smart phones and is known as the vane of the smart phone industry. Apple has been gradually building its own supply chain system. In the field of screens, Apple chose to strongly bind with the major screen manufacturer Samsung to jointly promote the popularity of OLED. However, now Apple is also trying to develop new screens. Rather than being the first to be installed on mobile phones, Apple is first testing the water on smart watches. In the Apple Watch Series 5 launched in August this year, Apple officially used an LTPO-based OLED screen. According to Apple, the advantage of this screen is that it saves more power.

< / p>

< / p>

▲ LTPO-based OLED screen for Apple Watch Series 5

In addition to the top three giants, Xiaomi, OPPO, vivo and other head mobile phone manufacturers, on the one hand, are keeping up with the trend of OLED screens, on the other hand, they are also trying different screen innovations. Several classic schemes in the full screen battle were proposed by them. For example, Xiaomi MIX 3’s slider design, vivo NEX’s lifting camera and OPPO Find X’s dual-track perimeter lifting camera design.

So, what role will the screen play in competition in the smartphone market? After the 5G era, how will the relationship between screen manufacturers and mobile phone manufacturers change?

Boao Vice President Yuan Zhi told Zhixi that the screen will become increasingly important for mobile phones in the future. The evolution of the screen is mainly reflected in two aspects: one is the change in form, such as the folding screen that is popular this year, this product form can enhance product appeal and consumer experience. In the future, the form will be the direction of product technology research and development. By changing the current form of mobile phone products, there will be more and more products.

The second is increased functional integration. All current mobile phone manufacturers

< / p> < / p>After an in-depth investigation of the industry chain, Zhixiong discovered three obvious trends that are hidden behind the screen industry oscillation: market share changes, technological route evolution, and some screen manufacturers being eliminated by core players.

To understand the changes in market share, let’s first look at the shipments of the mobile phone screen industry in recent years.

According to Sigmaintell data, global smartphone panel shipments in the first half of 2019 were approximately 840 million (Open Cell caliber), a decrease of approximately 5.2% year-on-year.

Let’s take a longer look and look at the market situation in the last three years.

In 2017, total global mobile phone display panel shipments reached 2.01 billion units, an increase of 3% compared to 2016. Among them, the LCD screen panel shipments were about 1.599 billion, and the AMOLED panel shipments were about 402 million.

As the full screen wind blows, the demand for AMOLED panels from smartphones has begun to increase. Since 2018, OLED screens have quickly occupied the flagship mobile phone market with their self-luminous, bendable, and good color rendering effects. In the smartphones released this year, OLED screens have almost become the mainstream of flagship phones, and only a few models still insist on using LCD screens.

▲ Note: The picture is from the Foresight Industry Research Institute

According to global authority in the field of displayAccording to DSCC (Display Supply Chain Consultants) data, from 2016 to the present, global OLED panel sales have maintained a rapid growth trend. In 2018, the global shipment of smart phone panels (OpenCell) was approximately 1.87 billion, which was affected by the decline in terminal demand, a decline of 6.1% compared with the previous year.

As the brand concentration in the complete machine market continues to increase, the panel supply chain market is also gradually concentrating.

In 2019, the entire mobile phone screen industry started in the state of folding screens. In the first half of 2019, global political and economic risks intensified, market volatility increased significantly, and the weak performance of the smart phone terminal market made the smart phone panel market also trend downward. According to Sigmaintell data, global smartphone panel shipments in the first half of 2019 were approximately 840 million (Open Cell caliber), a decline of approximately 5.2% year-on-year.

On the whole, the mobile phone screen market changes with the shipment of smartphones.

Panel research agency Display Supply Chain Consultants (DSCC for short) predicts in the 2019 LCD panel research report that by 2023, Samsung will still maintain a market share of more than 50% in the OLED field, and BOE will maintain its market share in 2021. Occupying the second position, another Chinese screen maker Visionox will occupy the third position in the market in 2022.

On the other hand, the screen technology route is undergoing changes.

The most obvious feeling is that OLED is squeezing the LCD market further.

On November 28, foreign media reported that Apple expects to launch three iPhone 12 models next year, all of which will use OLED screens instead of LCD screens.

DSCC forecasts that in the field of mobile products, LCD compound annual growth in 2019The rate is expected to be 3%, and the compound annual growth rate of OLED is expected to be 16%. DSCC believes that by 2023, OLED will occupy 63% of the market.

In the first half of this year, BOE’s smart phone panel shipments exceeded 190 million pieces, a year-on-year increase of 23.1%. LCD panel shipments soared in March, with shipments of approximately 180 million units, a year-on-year increase of approximately 16.7%, and still the world’s largest LCD panel supplier.

Samsung ’s screen shipments were relatively weak in the first quarter. According to Sigmaintell data, its total smartphone panel shipments in the first half of 2019 were basically the same as BOE’s, also about 190 million pieces, an increase of about 9.6% year-on-year, but still occupy an absolute advantage in the AMOLED field.

Tianma ’s smartphone panel shipments in the first half of the year were approximately 100 million pieces, of which LTPS shipments exceeded 80 million pieces, ranking first in the global LTPS LCD shipments. In the first half of 2019, Tianma’s “punched screens” shipped close to 20 million pieces, occupying about 61.0% of the market in the LCD punched screen market, and is the main supplier of LCD punched screens.

However, the industry generally believes that OLED and LCD have their own advantages, and OLED will not completely replace LCD. Although OLEDs have gradually become the choice of more mobile phone products due to better contrast in mobile products such as mobile phones, in the field of TVs, LCDs have higher brightness and more competitive prices.

Look at the situation in the OLED market again.

According to the data from Qunzhi Consulting, the global smartphone OLED panel shipments in the first half of 2019 were approximately 220 million pieces, accounting for approximately 26% of the overall smartphone panel market, a year-on-year increase of approximately 18.6%. It is estimated that the shipment of OLED mobile phone panels will be about 490 million pieces.

No surprise in the market’s throne, it is still firmly occupied by Samsung. In the first half of this year, Samsung ’s AMOLED panel shipments were approximately 190 million, an increase of approximately 11.4% year-on-year, of which hard-screen shipments accounted for more than 60%. With the strong demand for OLED under the screen fingerprints and Samsung’s active promotion strategy, Samsung’s hard screen production line is still in short supply.

The domestic screen manufacturer BOE ranks second in the global smart phone OLED panel market, shipping about 10 million pieces, accounting for about 5% of the global market share, and is currently a panel manufacturer that can stably supply flexible AMOLED in addition to Samsung. .

During this turmoil, some manufacturers stand out, while others are on the verge of elimination and are entering a difficult situation.

The most typical example is Japanese screen maker JDI. Zhixi has previously published a detailed analysis of the situation of the JDI crisis ( < / p>

▲ Global smartphone market share in the third quarter of 2019

A few days ago, the analysis agency canalys released the latest smartphone market share report. The top five are Samsung, Huawei, Apple, Xiaomi and OPPO, which occupy a total of the world.67% of market share.

And more interestingly, in the context of the weak growth of the global smartphone market, mobile phone giants, on the one hand, have a large amount of banknotes, on the other hand, they want to continue to win in the market and choose to extend their tentacles to the depth of the industrial chain. , And screen manufacturers to launch technological changes.

Let’s take a look at Samsung, the “almighty” giant.

Samsung is the world ’s largest mobile phone maker by market share. It can also be called the “leading player” in the field of OLED screens. Among the OLED small-size panel manufacturers in the fourth quarter of 2018, Samsung ’s display sector accounted for 93.3% of the market, and flexible OLEDs accounted for 94.2%.

Especially in the field of OLED, Samsung has taken the lead in betting and monopolized the industry by buying out upstream materials and equipment. Smart stuff used to be in ().

Although Samsung is a large screen manufacturer, it has to rely on Japanese material suppliers in the upstream material field, and this year Samsung ’s screen has encountered unprecedented huge obstacles-Japan-South Korea trade friction. In July this year, the Ministry of Economy, Trade and Industry of Japan announced that starting from July 4, it will restrict the export of core upstream raw materials for Japanese semiconductors, core materials for displays such as smartphones and televisions to South Korea. This includes fluorinated polyimide, an OLED display component material used in the manufacture of foldable screens. Affected by the trade war between South Korea and Japan, Samsung’s OLED production line researchDevelopment progress has caused some impact.

Huawei rushed to the second place in the global mobile phone market. Despite facing force majeure, its market share maintained a rapid growth trend. In the choice of screen supply chain, Huawei has also suffered a big loss of Samsung ’s supply cut. With the rise of domestic screen manufacturers, Huawei now tends to choose multiple screen supply chains. With the increase of market share in recent years, Huawei is also continuously expanding the list of screen supply chain partners. For example, the mobile phone screen giant BOE is an important partner of Huawei, and this year ZTE and Xiaomi’s screen supplier Visionox also joined Huawei’s partner camp.

Apple defines the basic form of smart phones and is known as the vane of the smart phone industry. Apple has been gradually building its own supply chain system. In the field of screens, Apple chose to strongly bind with the major screen manufacturer Samsung to jointly promote the popularity of OLED. However, now Apple is also trying to develop new screens. Rather than being the first to be installed on mobile phones, Apple is first testing the water on smart watches. In the Apple Watch Series 5 launched in August this year, Apple officially used an LTPO-based OLED screen. According to Apple, the advantage of this screen is that it saves more power.

▲ LTPO-based OLED screen for Apple Watch Series 5

In addition to the top three giants, Xiaomi, OPPO, vivo and other head mobile phone manufacturers, on the one hand, are keeping up with the trend of OLED screens, on the other hand, they are also trying different screen innovations. Several classic schemes in the full screen battle were proposed by them. For example, Xiaomi MIX 3’s slider design, vivo NEX’s lifting camera and OPPO Find X’s dual-track perimeter lifting camera design.

So, what role will the screen play in competition in the smartphone market? After the 5G era, how will the relationship between screen manufacturers and mobile phone manufacturers change?

Boao Vice President Yuan Zhi told Zhixi that the screen will become increasingly important for mobile phones in the future. The evolution of the screen is mainly reflected in two aspects: one is the change in form, such as the folding screen that is popular this year, this product form can enhance product appeal and consumer experience. In the future, the form will be the direction of product technology research and development. By changing the current form of mobile phone products, there will be more and more products.

The second is increased functional integration. All current mobile phone manufacturers