In 2019, the total installed capacity of power batteries in China was 62.2GWh, a 9% increase against the trend.

Editor’s note: This article is from WeChat public account “ Car stuff ” (ID: chedongxi ), author: Bear

In the second half of 2019, the entire new energy market is shrouded in a cloud, and the pressure brought by subsidies to decline is unprecedented.

The sales volume of the new energy vehicle market declined for the sixth consecutive year. The annual sales volume was 1.206 million units, a year-on-year decrease of 4%. This is also the first annual decline in sales of the new energy vehicle market since 2013 when China introduced a new energy vehicle subsidy policy.

Behind the declining vehicle market, upstream power batteries have continued to grow against the trend.

The latest 2019 battery data released by the China Automotive Power Battery Industry Innovation Alliance shows that in 2019, domestic power battery production reached 85.4GWh, a year-on-year increase of 21%; sales reached 75.6GWh, a year-on-year increase of 21.4%; installed capacity It reached 62.2GWh, a year-on-year increase of 9.2%.

Although the market is expanding, from an industry perspective, the degree of fierce competition is continuing to rise. The installed capacity of Ningde Times power batteries reached 31.26GWh in 2019, and its market share increased from 40.7% in 2018 to 50.5% in 2019, and the industry concentration has further increased. At the same time, the number of supporting power battery companies also dropped from 89 in 2018 to 79 in 2019, and the industry reshuffle accelerated.

The latest 2019 battery market data released by the China Automotive Power Battery Industry Innovation Alliance reveals the industry situation, technical route, and changing trends of the player structure in the upstream power battery market.

Industry fundamentals: total production and sales surged by 20% at the end of the year.

According to China Automotive Power Battery Industry Alliance data, in 2019, domestic power battery output reached 85.4GWh, a year-on-year increase of 21%; sales reached 75.6GWh, a year-on-year increase of 21.4%; installed capacity reached 62.2GWh, a 9.2% year-on-year increase.

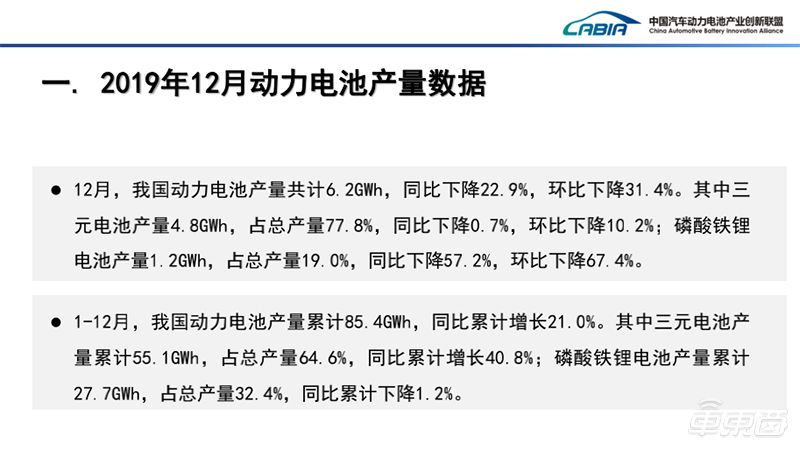

▲ Power battery production data for December 2019 and the whole year

In December 2019, domestic power battery production was 6.2GWh, a year-on-year decrease of 22.9% and a 31.4% decrease; sales volume was 7.8GWh, a year-on-year increase of 3.5%; installed capacity was 9.7GWh, a 27.4% year-on-year decrease, and a 54.4% chain increase %.

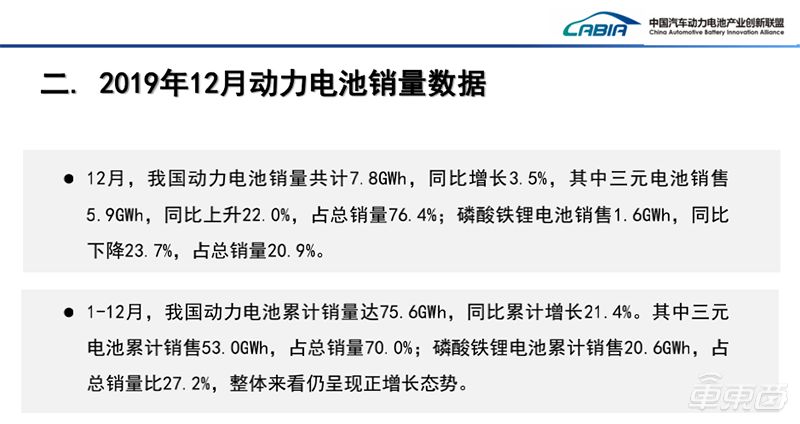

▲ Sales data of power batteries in December 2019 and the whole year

In December, the power battery industry experienced a relatively clear inventory clearance phenomenon. Production was reduced and the number of installed vehicles rose month-on-month. However, due to the slump in the new energy vehicle market in the second half of 2019, the momentum of concentrated battery loading is not as good as in previous years.

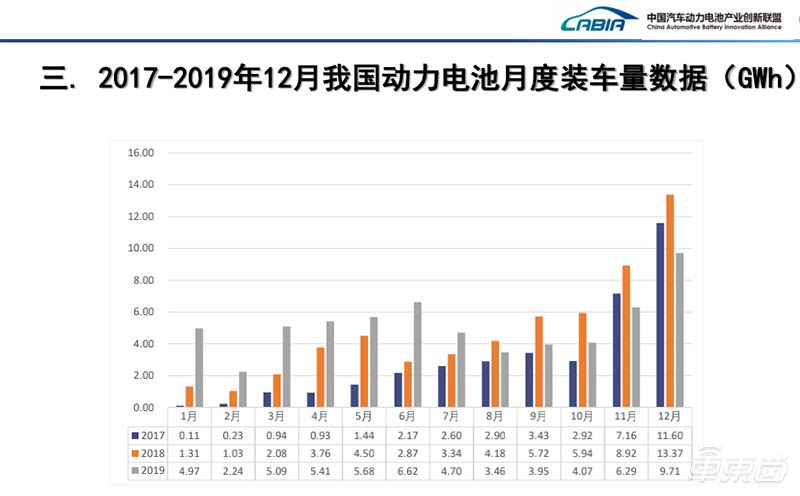

▲ December 2019 and full year power battery loading data

From the monthly power battery loading data below, you can more clearly see the gap between the power battery loading in 2019 and previous years:

▲ 2017-2019 Power Battery Loading Data

The figure shows that from January to July 2019, the installed capacity of domestic power batteries is higher than the same period. This is mainly because the production and sales of new energy vehicles in 2018 are too dazzling, and the installation boom has continued into 2019. July.

After July 2019, the sales of new energy vehicles plummeted by more than 50% that month, and the OEMs tended to calm down and began to adjust the installed capacity of power batteries. After July, the installed capacity of power batteries was not as good as in the same period of previous years.

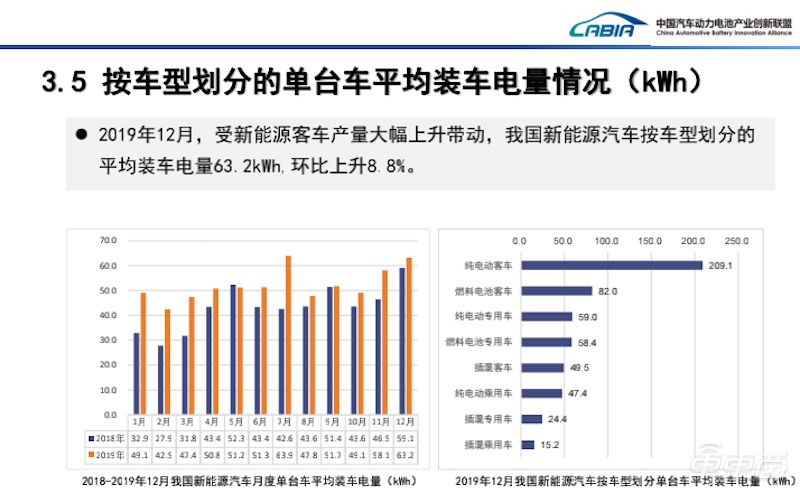

Another major reason for the increase in the installed capacity of power batteries in 2019 is the increase in the average charge of new energy vehicles, driven by the increase in output of new energy buses. It is understood that in December 2019, the installed capacity of new energy vehicle bicycle power batteries in China reached 63.2kWh, an increase of 8.8% from the previous month.

▲ The average charge of domestic new energy vehicles in December 2019

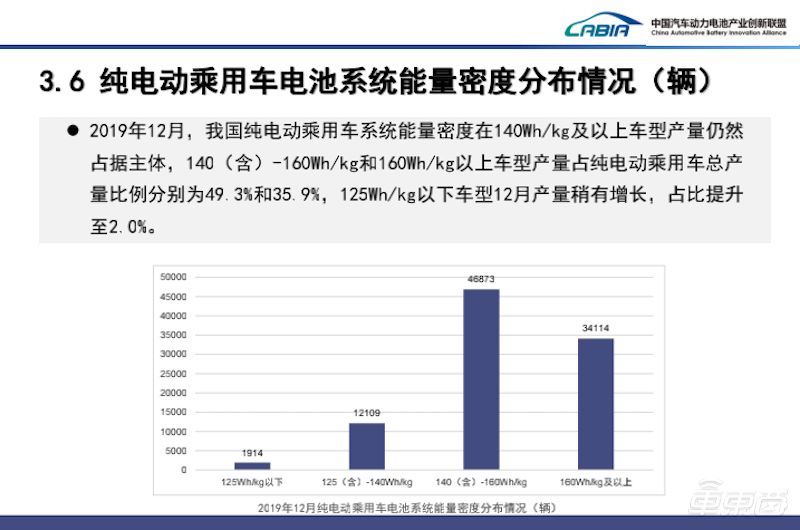

In terms of pure electric passenger vehicles, in December 2019, the average energy density of power battery systems in domestic models was mainly concentrated at 140Wh / kg-160Wh / kg, accounting for 49.3%, and the system energy density was above 160Wh / kg. The market share of pure electric passenger car models is 35.9%, and the number of models with system energy density below 125Wh / kg accounts for 2%. The average energy density of pure electric passenger car power battery systems has also increased compared to the same period in 2018.

▲ Energy density distribution of pure electric passenger car systems in December 2019

Technical line dispute: Ternary lithium is firmly in the mainstream. Lithium iron phosphate temporarily counterattacks

Under the broader market, the performance of power batteries for various technical routes this year also varies.

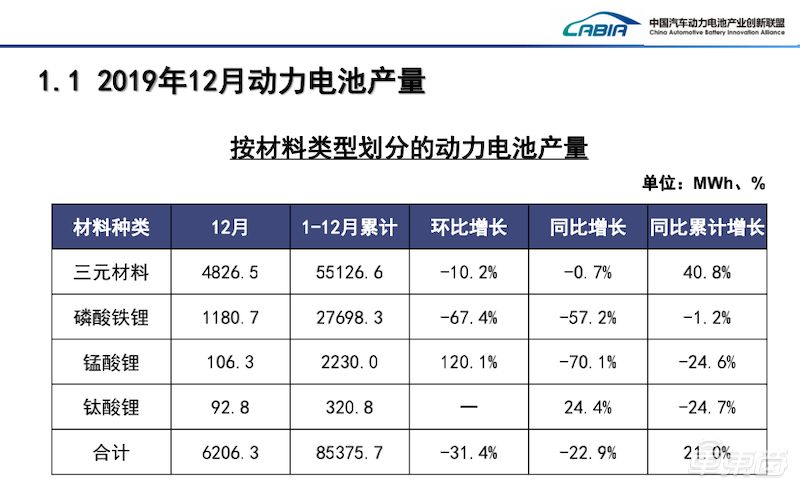

In 2019, the output of ternary lithium batteries was 55.1GWh, accounting for 64.6% of the total output, an increase of 40.8% year-on-year; the sales volume was 53.0GWh, accounting for 70% of the total sales volume; The installed capacity is 40.5GWh, accounting for 65.2% of the total installed capacity, an increase of 22.5% year-on-year.

▲ Power battery production data for December and the whole year (by material)

The output of lithium iron phosphate batteries in 2019 was 27.7GWh, accounting for 32.4% of the total output, a decrease of 1.2% year-on-year; sales were 20.6GWh, accounting for 27.2% of total sales; installed capacity was 20.2GWh, accounting for total The volume was 32.5%, a year-on-year decrease of 9%.

▲ Power battery production data for December and the whole year (by material)

Throughout the year, ternary lithium batteries and lithium iron phosphate batteries are still the mainstream technology route, and because ternary lithium batteries have higher energy density, they are widely used in the field of new energy passenger cars, so their growth is good. It is used in lithium iron phosphate batteries with a small application range.

▲ Data on the installed capacity of power batteries in December and the whole year (by materials)

But in December, the installed capacity of lithium iron phosphate battery was 4.7GWh, and the installed capacity of ternary lithium battery was 4.8GWh, which was almost the same. New energy vehicle matching price is more affordable lithium iron phosphate battery.

But from the history of power battery technology iterations, lithium iron phosphate batteries will eventually be eliminated by ternary lithium batteries, which are even higher.The energy density determines that it is more suitable for new energy vehicles.

The technical stability of the two power battery routes discussed by the public is, in the industry’s opinion, the current chemical engineering still has room for breakthrough technology. From the perspective of engineering development, the ternary lithium battery’s Thermal stability can be controlled within a safe range.

Thus, judging from the current market share, the ternary lithium battery is equivalent to the throne of the mainstream line of power batteries. The industry predicts that this situation will continue beyond 2025. Until the all-solid-state battery begins to be applied on a large scale, the status of ternary lithium batteries will be threatened.

Player structure: industry concentration increases Ningde era wins over half of the market

I’ve seen the evolution of the industry fundamentals and technology line, and then look at the changes in the player landscape in the industry.

The changing trend of the power battery player pattern in 2019 can be summarized in one sentence-the stronger the stronger, the industry reshuffles faster.

According to the loading data for the whole year of 2019, a total of 79 power battery companies have achieved loading support this year. The top three, top five, and top ten power battery companies have installed power batteries of 45.6GWh and 49.2 respectively. GWh and 54.7GWh, with market shares of 73.4%, 79.1%, and 87.9%, respectively.

▲ 2019 ranking of domestic power battery companies’ installed capacity

Among them, Ningde Times topped the market with a loading capacity of 31.46GWh, with a market share of more than 50%; BYD ’s annual loading capacity was 10.75GWh, followed closely by it, winning 17.3% of the market; Gaoke’s installed capacity is 3.43GWh, with a market share of 5.5%, ranking third; the remaining players’ installed capacity does not exceed 2GWh.

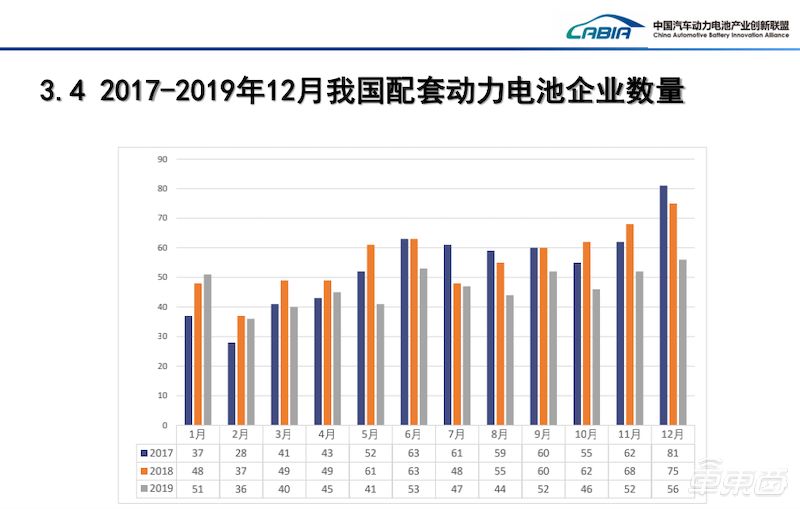

▲ Changes in the number of supporting power battery companies in 2017-2019

From this feelingIt can be seen that the status of the head player in the Ningde era has further consolidated, and its market share has increased from 40.7% in 2018 to 50.5% in 2019. However, the number of companies supporting power battery installations has dropped from 89 last year to 79 this year, and the reshuffle of the industry has accelerated.

Conclusion: The overall situation of the power battery market is still improving

The new energy vehicle market has stopped growing in 2019, and the outlook for 2020 is still not optimistic. Fortunately, the contrarian growth of the power battery market has restored a little face for the entire new energy market. In 2019, the production and sales of the power battery market increased by more than 20% year-on-year, and the installed capacity increased by more than 9%.

But it cannot be ignored that the growth of the power battery market in 2019 is largely due to the first half of the year, which subsidized the tide of installation before the decline, and after the subsidy of the decline, the installed capacity of power batteries from August to December was low. In the same period of previous years.

Continuing the development in this situation, the installed capacity of the power battery industry will not be effectively stimulated in 2020, and it will inevitably be lower than the same period in 2019. By then, the power battery market will be unable to maintain the momentum of continued growth. Overall, the growth situation of the power battery market in 2020 is worrying.

But as Jian Jianhua, deputy secretary general of the China Automobile Association, said, it is not objective and comprehensive to judge a market based on data and growth. We need to recognize that the power battery market is also in a critical period of change.

During this period, the country introduced foreign capital and activated full competition in the market. Within the market, companies are also continuously improving the core parameter indicators of power batteries, and the market for power batteries is still generally good.