Known as the last billion user market with huge opportunities

Editor’s note: Entrepreneurship and investment have become an irreversible trend globally. Known as the last billion user market with huge opportunities, India has been receiving global attention. In order to better demonstrate the current actual business environment in India, we also invited the Gujarat Chinese Enterprises Association to disassemble us in detail from the business environment, tax policy, manpower policy, visa policy and other aspects. Gujarat Chinese Enterprises Association was established in January 2019. It is a non-profit organization established to adapt to the growing economic and trade exchanges between China and India.

If your institution also wants to share the business environment and policies of your region on the platform, please also contact me (email: syq@36kr.com; WeChat: 15300063873)

1. Why choose Gujarat, India?

1. Complete infrastructure

① Kupang has 41 small ports and 1 main port connecting major ports in the world, and has the largest number of operating ports and commercial freight ports.

②Developed road, bus and rail transportation systems.

• Total road length: 77,690 kilometers (95% of roads meet all climate conditions).

• Total railway length: 5 257.22 kilometers. (Occupies 8.25% of India)

• Building BRT systems and subway projects in multiple urban areas.

• Mumbai-Aha High-speed Railway Corridor project has been approved, connecting India ’s Mumbai (Maharashtra) and Ahmedabad (Gujarat), the first high-speed in India railway.

③ Kupang is the only state in India with a natural gas network covering 2,400 kilometers and covering the entire state.

④Continuous water supply ———— A statewide “water supply network” covering 120,769 kilometers, determined to provide water services for 75% of the state ’s population.

⑤The only state with surplus electricity, every town and village has realized uninterrupted power supply.

⑥Gujarat has the second largest solar power generation potential in India, about 69,000MW (megawatt) (to 31-03-2014 Installed capacity: 889 MW) and Asia’s first and largest solar park in Charanka, with a capacity of 590 MW (until May 2014: 274 MW). The “solar park” also has a 100 MW wind power capacity, making it the largest solar-wind energy hybrid park in the world.

⑦In 2009, the Special Investment Zones Act was promulgated. It is the first state in India to promulgate the Act. It has established 13 special investment zones within a range of 3,600 square kilometers and 7 special investment zones have been announced. Annex 1 is a summary of the special investment zones that have been notified and proposed.

The map below is the location of the special investment zone announced by the Bureau of Industry Promotion. Among them, Virangam, Mandal-Becharaji, Dholera, Halol-Savli and PCPIR are the first special investment zones according to the plan of the Kupang government.

2. Superior strategic location

① Gujarat has a superior geographical advantage: it has a coastline of about 1,600 kilometers, 41 small ports and 1 main port.

② For ships from Western Europe, the Middle East, Africa and other countries, Gujarat is an excellent distribution center for maritime trade.

③It is the gateway to India’s rich north and central hinterland; it is organically connected by road, rail and air, which provides huge opportunities for trade.

3. Sustainable urban development

① Forty-three percent of Gujarat’s population lives in cities, while India’s national urban population is only about 31%.

②Urban transportation: fast and convenient planning of public transportation system and subway system

③ The Indian Government’s Best Intelligent Transportation System Award in 2011 and the World’s Best Sustainable Transportation Award in 2010.

④ Kupang successfully implemented the country’s first BRT system in Aiha.

⑤ A riverside landscape project with Gubang characteristics was constructed in Sabarmati, creating a beautiful and high-quality space for cultural and entertainment activities.

⑥ In the 2013 Indian Urban System Survey (ASICS) Awards, Surat and Ahmedabad won the “Best Living City” award at ETJanaagrahaa. Ahmedabad was named by Forbes Magazine as the fastest growing city in India and the third fastest growing city in the world.

4. Convenient business environment

① Establish a single convenient window for investment promotion of industrial and infrastructure projects. Investors can submit online applications for relevant permits through the portal (www.ifpgujarat.gov. in).

② Based on the World Bank’s business environment assessment report, Gujarat is one of the states with the best business environment in all states in India.

③ The state government actively promotes industrial development.

④ The various departments of Kupang and the central government actively coordinate to support the resolution of various permits and problems in the investment process.

⑤The Government of Gujarat has implemented a series of policies and incentives in various industrial sectors to attract large amounts of investment and to promote the overall development of the economy.

5. Human capital supporting the industry

① Siemens PLM Software India will set up five talent centers in Gujarat, which will cover the market segments of automation, industrial machinery, industrial automation, aerospace, defense and shipbuilding.

② The construction planning of 49 skill upgrading centers has been completed, of which 22 have been put into operation. And plans to establish 50 new skills upgrading centers within the GIDC.

③ The Gujarat government has set up a world-class International Center for Entrepreneurship and Technology (iCREATE) covering an area of up to 34 acres. India’s future is more prosperous.

6. Delhi-Mumbai industrial corridor brings great opportunities to Gujarat

① Of the planned Delhi-Mumbai industrial corridor route, 38% (564 kilometers) pass through Gujarat (the main cities passed are: Ahmedabad, Vadodara, Surat).

② Of the 26 districts in the state, 18 are directly benefited. Of the 90 billion investments in the Delhi-Mumbai Industrial Corridor, more than 60% of the total investment may occur in Gujarat.

③ Of the 19 potential projects totaling approximately $ 4.5 billion from Japan, 7 will be invested in Gujarat.

④Estimated to create 800,000 jobs

⑤Development of supporting infrastructure: high-speed railway freight passage, six-lane expressway, 3 ports and 6 airports.

Map (GIDB”Areas in Gujarat that directly benefit from DMIC”)

⑥ Of the 24 industrial zones planned for the Delhi-Mumbai Industrial Corridor, 6 zones (2 investment zones and 4 industrial zones) have been planned for Gujarat.

The Gujarat government set up the state’s first special investment zone in Dholera. The Dholera special investment zone is the most important place in the plan of Gubang.

7. Gujarati

①Gujaratis have been skilled in trade and industry since ancient times. Compared with other regions, they understand the importance of trade and industry better.

② Gujarat sells 22% of all Indian products to different countries and regions through international trade.

③Strong economic strength

Second, India and Gujarat What are the rules for corporate taxation?

1. What are the regulations on corporate taxation?

1.1 Tax system and system

The Indian tax system is based on the provisions of the Indian Constitution. According to Article 265 of the Indian Constitution: “Without the authority of the parliament, taxes cannot be taxed administratively.” India’s tax legislative power and collection power are mainly concentrated between the federal central government and the states, and local municipal governments are responsible for a small amount of tax collection.

The taxation rights of the central government and states are clearly divided. The central government’s taxes include direct taxes and indirect taxes. Direct taxes are mainly composed of corporate income tax, personal income tax, and wealth tax. Indirect taxes It mainly includes Goods and Services Tax (GST) (levied on July 1, 2017), customs duties, etc.

The state government also mainly levies newly levied GST, stamp duty, state consumption tax, entertainment and gaming tax, land income tax, etc. In areas not covered by the GST, such as petroleum products and liquor, the original taxes such as value-added tax (sales tax for countries without VAT) will continue to be levied.

The taxes collected by local city governments mainly include property taxes, market entry taxes, and taxes on the use of public facilities such as water supply and drainage.

Although Indian federal, state, and local governments have their own taxes, the tax revenue is mainly concentrated in the federal government. Central tax revenue accounts for about 65% of total tax revenue, and state and local government revenue accounts for about 35%. The tax sources of each state include two parts: one part is the independent tax revenue of each state, and the other part is the tax revenue that is uniformly distributed by the central government and has a controlling tax revenue. The two account for 60% and 40% of each. In general, India’s tax revenue has been increasing since 2003, and its share of GDP has also increased year by year.

India’s tax year coincides with its fiscal year, starting on April 1 and ending on March 31. Most taxes are reported on a per-account basisBefore the end of the year, that is, before the end of March each year; corporate income tax needs to be paid in advance according to the expected next quarter income every quarter before the 15th day, and settled according to the actual situation of the financial year before the end of March each year: the personal income tax is withheld and paid by the employer unit on a monthly basis .

Enterprises can file their own tax returns or file tax returns through a local accounting firm. When reporting tax at the end of the fiscal year, the enterprise must provide the tax authority with a statement, an audit report issued by an accounting firm, as well as documents such as the business license and tax registration number of the enterprise.

1.2 Major taxes and rates

1.2.1 [Corporate income tax]

India’s tax year is the fiscal year, from April 1st to March 31st the following year. The current tax rate is 25% + additional for newly established domestic companies, 30% + for other domestic companies; 40% + additional for foreign companies. A company incorporated in India or placing its management and control in India is considered a domestic company, and its worldwide income is subject to tax. Other companies are foreign companies and only tax their operating income in India.

1.2.2 [capital income tax]

This tax mainly refers to the taxation of income from the sale of assets. “Long-term assets” refers to those who have owned physical assets for more than 3 years or held stocks, securities, funds, etc. for more than 1 year. The tax rate for long-term physical asset sales income is generally 20%, while income from the sale of stocks, securities, funds, etc., which are also long-term assets, is exempt from taxation.

“Short-term assets” refers to those who have owned physical assets for less than 3 years or held stocks, securities, funds, etc. for less than 1 year. The income tax rate for the sale of short-term physical assets is the same as the corporate income tax rate. Income from the sale of stocks, securities, funds, etc. held for less than one year is taxed at 10%.

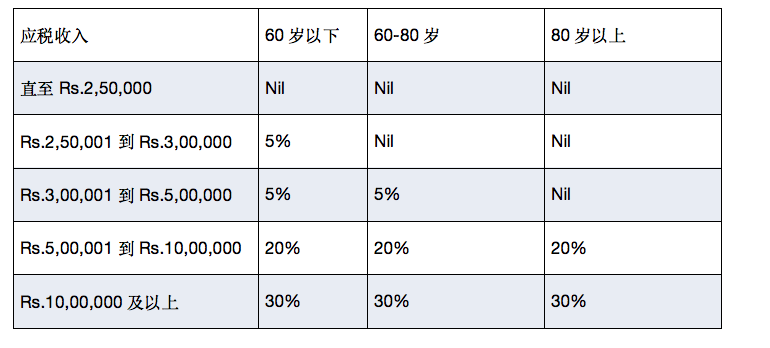

1.2.3 [Individual income tax]

The items subject to personal income tax include: (1) Wage income: including wages, subsidies, allowances, retirement benefits, etc .; (2) Real estate income: such as income from housing leases; (3) Business and skill income: Refers to Commissions from business operations and the use of your own professional skills; (4) Capital income: such as interest, securities, and stock income; (5) Other income: such as lottery, gaming, etc. The personal income tax rate in India is often adjusted. The starting tax for this tax year is Rs 250,000. In order to reflect the principle of fairness, the Indian individual tax also uses an excessive progressive tax rate, which is progressively taxed in 3 grades at a rate of 5% -30%. The details are as follows: (On this basis + additional tax)

1.2.4 [Income based on income tax]

![What is the environment for venture capital in India? Here is the most complete Gujarat business strategy guide]()

1.2.5 [Health and Education Extras]

Health and education supplements are income tax and its additional 4% (applicable to all assessees)

1.2.6 【GST】

GST is divided into four sub-taxes, namely the Central Goods and Labor Tax (CGST), the State Goods and Labor Tax (SGST), the Comprehensive Goods and Labor Tax (IGST), and the Central Territory Goods and Labor Tax (UTGST). Among them, the GST of the Central Territory is equivalent to the GST of the state and belongs to the level of local government taxation.

GST implements a “dual-track system”. The central and state governments, as tax collectors, levy their respective GSTs simultaneously, that is, the central government and the state government levy a central goods and labor tax (CGST) and State Goods and Services Tax (SGST), the “Union Territory” (levy of the Central Territory) collects the “GST” (UTGST, equivalent to SGST). For interstate transactions, the central government levies a comprehensive goods and services tax (IGST), which is the sum of CGST and SGST.

At present, the basic tax rate of the GST is four levels, namely 5%, 12%, 18% and 28%. The tax rate of each level is the combined tax rate of CGST and SGST, that is, 50% each. In addition, there are two rates of 0.25% and 3% applicable to diamonds, unprocessed gems, and small quantities of goods such as gold and silver. Therefore, if the zero tax rate applied to exports is not included, India’s GST actually has 6 tax rates. The tax rate for most products is below 18%. At the same time as the 28% tax rate applies to certain luxury and harmful products, additional taxes are also levied.

GST’s tax rate covers:

(1) Taxes on 98 and 1211 designated goods;

(2) Taxes on 36 designated services; (3) Reverses 18 designated services Tax collection mechanism; (4) Exemption of tax on 87 designated services. Specific tax items and rates include: for goods, for coal, sugar, tea and coffee, medicines and drugs.

Medication, edible oil, Indian sweets, etc. are subject to a 5% tax rate; 12% tax rate is applicable to fruit juice, vegetable juice, milk-containing beverages, biofuels, fertilizers, etc.18% tax rate applies to soap, toothpaste, etc .; 28% tax rate applies to air conditioners and refrigerators; 28% tax rate applies to cars, but subject to additional compensation tax. The compensation tax for medium-displacement cars has been adjusted from 15% to 17%; large The compensation tax rate for displacement cars is 20%; the compensation tax rate for sport utility vehicles (SUVs) is 22%.

Tax exemption for food, cereals, milk, raw sugar and salt. For labor services, a 5% tax rate applies to cargo transportation, railway tickets (excluding sleepers), economy class air tickets, taxi services, and advertising on print media; engineering contracts, business class air travel, telecommunications services, Financial services, restaurant services, hotel services between Rs 1,000 to 5,000 are subject to a tax rate of 12-18%; movie tickets, gaming, gambling, hotel services above Rs 5,000 are subject to a tax rate of 28%; education, health care Tax free for hotels, hotels, and hotel services below Rs 1,000.

In principle, GST includes all goods and services in the scope of GST collection, but there are two exceptions: the first is drinking white wine. The newly amended constitution and the various GST laws clearly stipulate that drinking liquor is not included in the scope of GST collection. In other words, after the GST reform, drinking liquor is still taxed according to the original system, that is, state value-added tax (or state sales tax) and alcohol consumption tax. Second, crude oil, high-speed diesel, gasoline, aviation fuel, and natural gas are five types of petroleum products, as well as electric power and energy products.

Simplified collection of small businesses with an annual turnover of less than 5 million rupees in the previous year (the GST Committee decided on June 11 to increase to 7.5 million rupees, and on June 18 specified a specific state of 5 million rupees) Rates vary by industry: manufacturing 2%; catering services 5%; other industries 1% (ie, CGST and SGST rates are halved to 1%, 2.5% and 0.5% respectively). This simple collection method does not apply to goods and service providers (except hotel services) and special categories of manufacturers that trade across states.

In order to protect state revenue and reduce resistance to GST reform, India adopted the 101st Constitution Amendment Act and the Goods and Services Tax (Compensation to States) Act in the design process of the GST reform program. The GST reform benefits compensation mechanism, that is, the loss of state revenue caused by the GST reform is compensated by the central government within 5 years. To this end, a “GST Compensation Fund” was set up and a “Compensation Cess” was temporarily levied by the central government as a source of funds for the fund. For some special taxable items to which a high tax rate of 28% is applicable, mainly including tobacco products, luxury goods and “unhealthy” products harmful to the society, in addition to the GST, a “compensation surcharge” is also levied. The tax rate is 1% -204% Etc., tobacco products are subject to a compound tax rate of “proportionate tax rate + fixed tax rate”, July 1, 2017On the 7th and September 21st, the GST Committee made the latest increase in cigarette and mid-displacement, large-displacement, and additional taxes on SUV cars. From this, it can be determined that the compensation tax also has a special consumption tax nature.

2. What are the relevant procedures for companies to file taxes in India?

2.2.1 Tax filing time

The tax reporting time for most taxes is before the end of each fiscal year, that is, before the end of March each year; corporate income tax must be paid in advance according to the expected next quarter income before the 15th of each quarter and settled according to the actual situation of the fiscal year before the end of March each year; Income tax is withheld and paid monthly by the employer.

The tax reporting time of each tax type is determined according to their respective regulations, and is divided into monthly, quarterly and annual. The corporate income tax shall be paid in advance according to the calculated quarterly income before the 15th of the next month after the end of each quarter, and shall be settled and paid according to the fiscal year before the end of September each year; the personal income tax shall be withheld and paid by the employer unit on a monthly basis.

2.2.2 Tax reporting channels

Enterprises can file their own tax returns or file tax returns through local accounting firms.

2.2. Tax declaration procedures

When reporting tax at the end of the fiscal year, the enterprise must provide the tax authority with a statement, an audit report issued by an accounting firm, as well as the business license, tax registration number, and other documents required by the tax authority.

2.2.4 Tax filing information

Enterprises must submit a Return of Income to the tax authority before September 30 of each year, even if there is no profit for the financial year. In this fiscal year, companies must fulfill their tax payment obligations by paying taxes in advance, specifically four times: June 15th, September 15th, December 15th, and March 15th. If the tax filing materials are not submitted within the prescribed time, the enterprise will be required to pay a late fee based on the amount of tax paid.

III.Human Resources Policy in India and Gujarat

1. Employee working hours

The working hours of all categories of employees / workers should comply with the provisions of the Factories Act 1948, which states that employees must not be required or permitted to work more than 48 hours in any one week, and this requirement should also be displayed on the notice board from time to time On display. Managers have the right to change the length of work, the number of shifts, the number of shifts, the number of working days per week, the weekly leave system, etc., and can decide for any reason, but must comply with the Factories Act 1948.

2. Management Code

2.1 Employee Provident Fund (PF).

According to the provisions of the Employees Provident Fund and Miscellaneous Act 1952, all employees who were under the age of 58 when they joined the company are entitled to provident fund benefits from the date of joining the company. They should provide the following documents to the company: ① When joining the company, employees must submit a declaration using Form 11 and confirm the name of the person named in Form 2 and submit it to the designated agency of the company’s personnel department. ② If the employee is already covered by the provident fund plan and if they want toIf the accumulated provident fund is transferred to a new account, they must provide Form 13.

![What is the environment for venture capital in India? Here is the most complete Gujarat business strategy guide]()

Withdrawal of Provident Fund upon separation: If an employee wants to withdraw funds from his account after leaving the company, he must provide forms 19 and 10-C together with the form SSN and submit it to the designated responsible agency within the company, and they will Submit to Provident Fund Center

2.2 Employee termination benefits

Companies shall pay termination benefits to their appropriate employees in accordance with the provisions of the End of Life Act 1972, as amended from time to time. It will be paid upon termination of employment. If the company stops working after less than 5 years of service, the company will pay ex gratia payments. If the service period is more than 5 years, it will be paid according to the amount stipulated in the Superannuation Act 1972. However, if the company suffers damage or loss as a result of the employee’s misconduct, intentional omission or negligence, the company has the right to confiscate the termination benefits payable to the employee.

2.3 bonus distribution

The company should pay bonuses to eligible employees whose salaries or wages have reached Rs 21,000 per month. Pursuant to Article 11 of the “Bonus Payment Regulations” of 1965, the company shall pay bonuses to employees in accordance with Article 10 or (as the case may be) and has the right to adjust the amount paid during the year instead of the bonus

2.4 National Insurance for Employees (where applicable)

Company shall comply with the provisions of the “Employees National Insurance Act of 1948” as amended from time to time, and eligible employees shall be insured in accordance with the “Employees National Insurance Act of 1948”. Deducted based on 1.75% of the employee’s total salary (including various allowances), the company pays 4.75%

2.5 employee compensation

A company employee who has suffered an injury during an accident during the employment of the company is entitled to compensation from the company in accordance with the provisions of Chapter 2 of the Employees Compensation Act of 1923. * [Article 53 of the “National Insurance Law of the Employees”-Prohibition of recovering damages under any other law-The insured or his family members shall not recover compensation from the insured’s employer or other person The “Employees’ Compensation Act of 1923” or the law in force at that time or implemented in other ways must be complied with as an employee’s insured artificial injury]

2.6 Prohibition of contract workers

Without proper registration, the company shall not directly or indirectly employ other persons who have been employed as contract workers.

3. Wage policy: p>

3.1 Salary:

Employees’ salaries will be paid in accordance with the salary structure specified in the offer of employment. The company will pay employees the net salary after making the necessary deductions

According to the law, the company needs to deduct the following payments from the payment:

1 Income tax levied at the current tax rate.

2 Provident Fund

3 professional tax

4 Absences without paid leave

5 ESIC

Increasing wages in 3.2 years

According to work efficiency, attendance and behavioral satisfaction, a salary increase is given to employees approved by the company once a year. The annual salary of each employee can be reviewed during the annual formal performance review and planning meetings. Such reviews could be carried out more frequently on newly created posts or based on recent transfers. The salary increase will be determined based on performance, good compliance with company policies and procedures, ability to fulfill or exceed job descriptions, and ability to achieve performance goals. Although the company’s salary will be adjusted continuously, the company has no obligation to increase the “cost of living”. Performance is the key to a pay raise in the company.

3.3 Payday

All employees shall receive a fixed monthly salary on the scheduled pay day, usually paid (verified) on the first day of the following month. If the regular payday is on a weekend or holiday, employees should receive their pay one day in advance. The company pays salaries by making payments directly to employees’ bank accounts. If the company’s bank changes, the company should notify employees. Employees who join the company after the 20th of each month shall receive the salary of the entry month next month, and employees who join the company before the 20th of each month shall receive the salary of the entry month.

3.4 Variable pay

Performance-related variable compensation is determined by management. Variable compensation is linked to the individual performance of employees and the company’s annual performance. Employees must not consider variable remuneration as a right, because it is a right that management decides based on employee performance. Employees fired for disciplinary reasons will not be entitled to variable compensation. Any employee who has filed a resignation and resignation before the company announced variable pay, regardless of his / her working hours in that year, is not entitled to such compensation.

3.5 work schedule

Employees submit work schedules (attendance sheets) on Mondays after each work week. If necessary, the employee’s line manager must approve the schedule. All timetables should be submitted by 6:00 pm on the submission day. If the submission date is a holiday, the employee should submit the timetable by 6:00 pm on the next working day. Due to time constraints in payroll management, employees who do not submit a timetable on the submission date will be deferred to the next payroll cycle to receive pay.

3.6 Mobile Phone:

There is an upper limit on the talk time of mobile phones issued by our company for certain employees. If the limit is exceeded, the excess costs will be paid by the employee himself. CorrectFor some employees, they can apply for reimbursement for mobile phone use. The maximum limit will be determined by management based on specific circumstances. Therefore, one-off reimbursement can be made within one month of receiving the bill and receipt.

3.7 Medical benefits

The company uses collective medical and accident insurance policies on behalf of all employees.

3.8 Deduction of tax from source

All employees’ tax deductions from the source will be deducted at the specified tax rate, and the company should provide employees with a copy of the income tax deduction.

3.9 professional tax

Under the tax plan based on total wages, professional tax will be deducted and remitted, which applies to different locations in the country where employees are employed

3.10 Payment of workers’ wages

Company shall pay wages to workers in accordance with the provisions of the “Worker Wage Payment Act of 1936” applicable from time to time

4. Vacation policies and benefits:

Determine the number of vacations and uniform rules for vacations. Human Resources and Administration to ensure that appropriate documentation and records are maintained. This policy applies to all employees in the company. Apprentices under the “Apprenticeship Act” are not included. During the one-year training period, trainees will be entitled to leave every 26 days. All vacations are performed for one calendar year, for example from January to December.

4.1 days of vacation

According to Section 35 of the Gujarat Shops and Institutions Act 1948, each employee is entitled to a maximum of 24 days of paid leave if he or she works for at least 240 days in a year. According to the above regulations, if an employee is employed for not less than three months in any one year, he is entitled to 5 days of paid leave every 60 days

Note: Laborers should be managed by service companies, and labor holiday policies should also be formulated by service companies. According to the law, laborers should have one paid holiday every 20 days.

4.2 Extra paid leave (EL): (mentioned above)

Employees are entitled to 24 additional days of paid leave per year, but in the case of 240 days of actual attendance in a calendar year. Or if the employee joined in the middle of a calendar year, it should be calculated as a percentage of the actual number of working days. From the date of employee’s joining, the leave account shall be added up on a quarterly basis every 2 days. Paid leave for all employees can accumulate up to 90 days, more than 90 days,The company will pay him cash based on the base salary, and each calendar year, employees are encouraged to use at least 50% of additional paid leave

4. 3 Temporary leave (CL):

Employees can use the temporary leave CL on a pro-rata basis from the date they join the company. It will be credited to the employee’s leave account at the beginning of each quarter or, if the employee joined the company in the middle of a calendar year, it will be credited to the employee’s leave account at the time of joining. Except in unforeseen circumstances, prior approval from HOD must be obtained. At any given point in time, temporary leave can be used for a maximum of 2 days. Temporary leave cannot be superimposed with any other leave. Employees can use half-day temporary leave. Unused temporary leave will not be carried forward and will lapse. It cannot be exchanged for cash.

4.4 Sick leave (SL)

When employees are unwell, they can use sick leave, which is calculated in proportion to the time when they joined the company. It will be credited pro rata to the employee leave account at the beginning of each quarter or, if joining the company in the middle of a calendar year, on a pro rata day. If 3 or more sick days are used, support from a doctor is required. Sick leave cannot be superimposed with any other leave.

Employees can use half-day sick leave. Unused sick leave can be accumulated and carried forward up to 30 days.

4.5 Unpaid Holidays (LWP):

When all available holidays are exhausted or not counted into the leave account, unpaid leave is at the discretion of the department head. It will be used in very critical or emergency situations.

4.6 Maternity leave: (under the Maternity Benefits Act 1961)

Eligible female employees are entitled to maternity leave benefits for 26 weeks with their first two children. Under the Maternity Benefits Act 1961, female employees continue to enjoy 12 weeks of maternity leave benefits if they have more than two children. In the case of miscarriage or termination of pregnancy, a woman employee is entitled to 6 weeks of paid maternity leave benefits immediately after the date of her abortion upon presentation of evidence

4.7 Paternity leave: (check)

Extend paternity leave to male employees if the following conditions are met: only the first 2 children were born with paternity leave-up to 5 days off (one-time vacation, or up to two vacations)-check whether you To this point-the law is not mandatory.

4.8 General corporate policies on vacation:

(a) If a day of vacation was originally unpaid, but any company announced company vacation / weekly vacation during that period, that vacation will also be counted as part of the vacation.

(b) Vacations are not a right, and supervisors have the right to refuse, postpone or reduce vacations based on the urgency of the work.

(c) All leave applications must be approved in advance by the department head.

(d) All leave applications must arrive at the Human Resources Department seven days in advance, with the responsible person in charge.Formally approved. However, in the event of an illness or emergency, the application should reach the Personnel Department within three days of leaving.

(e) For department heads (AGM and above), leave should be approved by MD.

(f) All senior staff and above employees requesting leave for more than 7 days must be approved by the managing director.

(g) The management / manager may at any time without notice Over one or more time periods

Stop all or part of the work of any machine, department, or department,

(h) Workers affected by the above-mentioned suspension should be deemed to have been laid off temporarily. This situation is within the scope of the relevant provisions of the Labor Disputes Act 1947, and the company should accordingly Make compensation

(i) The following should be considered necessary / confidential and / or emergency personnel.

(J) On duty or security staff.

(k) Maintenance personnel

(l) Staff working in the power and water sector

(m) Maintenance staff

(n) Personnel / Human Resources staff

(o) Workers necessary for loading and unloading, transporting materials and finished products, and workers driving cars, trucks or employee buses.

How to apply for a work visa to India?

1. Competent authority for work visas

Receiving departments for Indian work visas are Indian embassies (consulates) abroad; the examining and approving departments for Indian work visas are Indian embassies (consulates) and Indian Ministry of Home Affairs. After entering the country, foreigners must apply for a residence permit and apply for an extension from the foreign registration office (FRRO or FRO) where their residence is located.

2. Work permit system

Foreigners working in India must obtain an Employment Visa or a Project Visa newly established for power and metallurgy projects.

Applicants for work visas must be professionally qualified high-tech / high-skilled professionals engaged in routine affairs, secretarial or clerical work, clerks and other relevant personnel who do not require professional skills or high-skills. Within the scope of acceptance. The foreign citizen sponsored by the Indian company must have an annual income of more than $ 25,000 in the Indian company. This requirement does not apply to personnel working in the following areas: Chinese food chefs, language teachers (English language teachers must meet the annual income requirement of more than $ 25,000), translators, and personnel working for the embassies and consulates of the relevant country in India.

2.1 [Persons to issue work visas]

(1)Foreign citizens who are going to India to work in a company or organization (registered in India), or foreign citizens who are engaged in related work in a project operated by a foreign company / organization.

(2) According to the contract for the supply of equipment / machines / tools and other equipment signed by the two parties, foreign engineers or technicians who install and debug machines, equipment or tools and equipment in India

(3) Foreigners who are authorized to travel to India to provide technical support, technical services, transfer of skills, or provide various services to Indian companies that have paid user fees and other fees.

(4) According to the contract, a foreign person who travels to India to work as a consultant and is paid a fixed remuneration (not a monthly salary) by an Indian company.

(5) According to contracts signed with Indian hotels, restaurants, clubs or other units / organizations, foreign artists who regularly perform in the above units during the contract period.

(6) Foreign citizens who are coaching in Indian national or state sports teams or well-known sports clubs.

(7) Foreign athletes who have signed fixed-term contracts with Indian sports clubs or sports organizations.

(8) Self-employed foreigners who travel to India to perform high-skilled services in engineering, medical, financial, legal or other fields as independent technical consultants. If Indian law does not allow it, foreigners cannot work in the field in India.

(9) Teachers or interpreters in Chinese and other languages.

(10) Professional chefs in Chinese cuisine, professional chefs in other countries. According to the memorandum of understanding between China and India on simplification of visa procedures signed in June 2003, p.

The types of work visas that can be issued to Chinese citizens are as follows: 13-month single-round work visa (applicable to opening an office in India, working in India, including work contracting for a certain project); 23-month staff accompanying Single-entry visa for family members; 33-month non-staff travelling spouse / children / relatives single-entry tourist visa. (Tip: Business visas or any other type of visa are not allowed to be converted to work visas. Foreign citizens wishing to obtain a work visa must return to the country where they have permanent residency, apply for a work visa from the Indian embassy / consulate, and provide a visa office All relevant documents needed.)

2.2 [Subject of project visa]

[Subject of project visa] is a foreign citizen who travels to India to work on power or metallurgical projects. Specific requirements include:

(1) Issuing objects are only senior technicians or skilled technicians, semi-skilled and unskilled technicians are not within the scope of issuance;

(2) Project visa holders can only work on the project in India during the validity period of the visa, and may not participate in other project projects of the same company, or participate in project projects of other companies;

(3) Project visa holdersThe scope of activities is limited to the location of the project;

(4) The validity period of the visa is the same as the contract period of the project, but the longest is 1 year with multiple round trips;

(5) Each foreign citizen must have been engaged in the same project for an Indian company for no more than 2 years (counting from the date the project started);

(6) Project visa applicants must submit relevant application materials to prove that an Indian company or organization has signed a project contract with a foreign company;

(7) Only a maximum of two chefs and two translators are allowed per project;

(8) An Indian company must guarantee that foreign personnel who go to the company for project work will leave India before the expiry of their visa;

(9) Project visa holders whose visas are valid for more than 180 days must go to the local foreigner registration office (FRO / FRRO) to complete the registration procedures within 14 days of arrival.

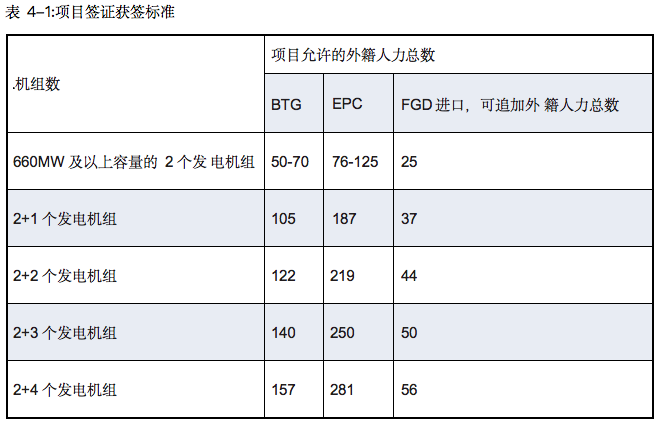

2.2.1 [Electricity Project] Visa

Note: 1 The Indian Electric Power Corporation imported FGD flue gas desulfurization system-related equipment must apply in accordance with the number of additional persons required in the table above. 2 If multiple generating units are newly built at the same location as an independent project, the contract period of the two contracts must be at least one year apart.

Source: Ministry of Home Affairs, India

2.2.2 [Metallurgical Project] Visa

For new construction projects, the number of project visas per million tons of steel output is 10% of the total number of workers, and the maximum number is not more than 300. For the expansion and expansion projects of existing plants, the project visas are granted per million tons of steel output The number is 5% of the total employment, and the maximum number is 150.

3. Application Process

The work visa must be directly applied by the applicant or the applicant’s organization to the Indian Embassy (Consulate) in China.

The Indian embassy (consulate) in India must first report to the Ministry of the Interior, the Ministry of Labor and other departments for approval. Approved by the Indian government approved in India

, or an appointment letter from the Indian company provided by the Chinese employee and a confirmation letter issued by the Indian engineering department on the project and the need to hire Chinese personnel, etc., can generally be processed once every 3 months. Entry work visa. Accompanying family members providing proof of kinship and employmentAfter the main invitation letter, you can get a single entry visa valid for 3 months. The aforesaid personnel should register with the local FRRO or FRO, apply for residence permit and visa extension in sequence within 14 days after entry and 60 days before their visa expires. Once the extension application has been approved, the entry visa can be extended to 1 for 1 month. Multiple entry visas for the year. The application period for each extension of a foreigner’s residence permit and multiple-entry visas does not exceed one year, and the total length of work allowed for one work permit cannot exceed five years. Applicants who have worked in India for more than 5 years will need to reapply for a new work permit. It usually takes 8 weeks or more to apply for a work visa, and 4 weeks or more to extend the approval of a work visa.

At present, India has very strict control over Chinese citizens working in India. It is extremely difficult for general managers and engineering and technical personnel to obtain work visas, and ordinary workers are even unable to obtain related work visas.

4. Provide materials

4.1 [Work Visa Application] Documents to be submitted:

(1) A copy of the employment letter of the Indian company and the contract signed by the two parties; (2) the applicant’s resume; (3) the education / professional experience certificate; (4) the professional skills certificate; (5) the Indian company in accordance with the “Company Law 》 Registration registration license, or the company’s certificate of registration in the Indian state’s industrial department or the Export Promotion Board; (6) Certificate issued by the Public Security Bureau, notarized by the Notary Office, and a record of no criminal record; (7) In the visa review form Other documents required.

4.2 [Project visa application] Documents to be submitted:

(1) A certificate (original or fax) issued by an Indian company that has signed a construction contract or project contract with a Chinese company or agency, which should include the following Information:

1 full name of Chinese company;

2 registered address of Chinese company;

3 project / project name;

4 detailed address of the project in India: state, district, town, village;

> 5 project contract duration (total days); 6 separately list the number of the following Chinese staff who travel to India to work on the project: senior technical staff; proficient technology with a bachelor’s degree in science or engineering or a diploma in science and engineering > Staff;

Skilled workers with secondary professional qualifications.

(2) Letter (original or fax) from the Indian company to the relevant Indian embassies / consulates abroad

The following information must be clearly listed:

1The Indian company guarantees all the acts of the Chinese company and Chinese staff who go to the company to engage in engineering and project work in India;

2The Indian company fully guarantees that the Chinese staff will comply with Indian laws and regulations in India The name, passport number, and date of birth of the relevant Chinese person); 3 the Indian company guarantees that the Chinese staff who went to the Indian company to engage in engineering and project work will leave India before the visa expires;

(3) The certification document issued by the Chinese company must briefly describe the nature of the Indian project or project and the work content of the relevant Chinese staff in the project;

(4) Resume of the applicant;

(5) Education qualification certificate;

(6) Professional and technical qualification certificate;

(7) Registration license issued by an Indian company in accordance with the provisions of the Indian Company Law, or the company’s industrial sector in a state Or the export promotion committee has been registered;

(8) Notarized certificate of no crime issued by the Public Security Bureau / Police Station; and (9) Fill in an additional form and promptly electronically copy the form (using Word format) to email: fsvisa@indianembassy.org.cn

Fifth, How is India’s financial environment?

At present, India ’s foreign exchange management system is still relatively strict. There are many restrictions on foreign currency exchange, remittance, and account opening. Once violated, it may involve economic punishment and even criminal punishment.

1. Local currency

India’s currency is the rupee and the exchange rate structure is a single exchange rate. The exchange rate of the Indian rupee is determined by the interbank market. The Reserve Bank of India (RBI) conducts spot and forward USD transactions with authorized dealers on this market at market exchange rates.

As of March 31, 2018, the exchange rate of the rupee to the US dollar was 1.53 US dollars / 100 rupees, and the exchange rate of the rupee to the euro was 1.24 euros / 100 rupees. In the past three years, the exchange rate of the rupee has shown a general depreciation trend. The exchange rate of the rupee against the US dollar has fallen from 1.83 US dollars / 100 rupees at the beginning of 2012 to 1.45 US dollars / 100 rupees on November 24, 2016. The exchange rate of the rupee against the US dollar has fallen by 17.5% in the past three years. Recently, due to the instability of the world economy, the downward pressure on the exchange rate of the rupee against the US dollar has been greater.

At present, the RMB and Indian Rupee cannot be settled directly, and RMB payments or exchanges are only informally accepted in some markets.

2. Foreign exchange management

The Reserve Bank of India (RBI, Central Bank) is the competent authority in charge of foreign exchange management in India. Its foreign exchange administration is the department responsible for foreign exchange transactions and control.

The Foreign Exchange Management Act (1999) is the main law governing foreign exchange management in India. The law was promulgated by Parliament in 1999 and entered into force on June 1, 2000. It applies to institutions in India and institutions outside India that are owned or controlled by Indian residents. In addition, under the framework of the “Foreign Exchange Management Law (1999)”, there are also a large number of management rules related to specific areas of foreign exchange management, such as the “Foreign Exchange Management (Establishing a Branch, OfficeBusiness place) rules (2000) “and so on.

According to relevant regulations, the Indian government has liberalized foreign exchange controls and the rupees under the current account can be freely converted. The non-resident’s capital account can also be almost fully converted into rupees. However, in practice, the government has many specific regulations and restrictions on capital flows.

For foreign investors investing directly in India, they need to report to the Reserve Bank within 30 days on the transfer of shares and the amount of remittances.

Non-resident individuals investing in shares can remit through normal channels of banks, while foreign institutional investors need to open a non-resident special rupee account and deposit their money into that account.

Except for the investment lock-up period for construction engineering, development projects, and defense projects, all foreign investment principals and profits can be repatriated freely to the home country. Profits, dividends, and sales proceeds from foreign direct investment can be Remittance in full. Among them, the repatriation of securities sales income and liquidation income shall obtain the tax payment certificate of the Income Tax Division of the Ministry of Finance of India and conduct it through a designated bank (AD Category-I bank).

According to relevant Indian customs regulations, there is no limit on the amount of foreign currency in and out of foreign currency. However, if you carry more than US $ 5,000 in cash or traveler’s check exceeds US $ 10,000, you must declare.

In addition, India ’s foreign exchange management system also requires the following regulations:

(1) Non-resident rupee account. Foreigners residing in India, overseas legal entities, other legal entities with at least 60% of which are directly or indirectly owned by Indian non-residents, and overseas trusts with at least 60% of which are irrevocably owned by Indian non-residents, may open Establish non-resident rupee accounts (also known as external accounts). The balance of these external accounts can be freely converted into foreign currencies.

(2) Non-resident foreign currency accounts. As a non-resident Indian citizen, a person born in India, and an overseas company with at least 60% of the property owned by a non-resident, you can open a non-resident foreign currency time deposit account in euros, yen, pounds, and dollars. The account balance can be remitted abroad at will, without the need to ask the central bank.

(3) Foreigners residing in India can open interest-free, current wage income foreign currency accounts in banks. Foreign currency wage income can be remitted freely in full after tax payment, and can also be freely converted and withdrawn in rupees.

[Requirements for foreign exchange management of foreign-invested enterprises] Depending on the type of foreign exchange transaction, foreign exchange laws also differ when applicable. The requirements of the Foreign Exchange Control Law for different types of transactions are summarized as follows:

(1) Equity investment. Foreign equity investment is subject to the foreign exchange law, which mainly includes the Foreign Exchange Control Act (Issuance or Transfer of Securities by Non-Indian Residents), its amendments and related regulations, and the Foreign Direct Investment Policy. Foreign equity investments include (common stocks) fully compulsory convertible preference shares, fully compulsory transferable bonds, and share certificates. Legislation under foreign exchange lawIt is intended that any optional convertible financial instrument is not included in the scope of “equity” investment, but is regulated by relevant foreign commercial borrowing rules (see below for details). At present, foreign equity investment is made in the form of foreign direct investment or foreign portfolio investment.

①Foreign direct investment. Angel investments (investments by foreign venture capitalists), foreign private equity and venture capital investments are the main sources of foreign direct investment in India. The “Foreign Exchange Control Law” is very lenient for foreign direct investment, and only stipulates the minimum conditions (if any) of the investment subject. Except for the pure real estate industry, insurance business, gaming industry, mutual funds, atomic energy, certain railway operations, transferable development rights transactions, and the tobacco industry, business entities in almost all industries can be the object of foreign direct investment. However, under the condition of obtaining an automatic license, these business entities must set up a company or a limited liability partnership to receive foreign equity investments. Foreign investments in trusts, partnerships, or other registered and unregistered business entities are not allowed unless they are non-Indian or Indian-foreign foreigners residing in partnerships or trusts registered with the Indian Securities and Exchange Commission Investments made by the company.

There are still certain restrictions in certain industries, such as insurance, retail, defense, print media, etc. Except for foreign venture capital investments, the Foreign Exchange Control Law regulates the pricing rules for all foreign direct investment and merger and acquisition transactions. The Foreign Exchange Control Law also provides for certain reporting systems. In addition, the legal framework applicable to foreign direct investment is quite loose and flexible to help attract foreign investment.

② Foreign portfolio investment. Foreign portfolio investment is led by qualified investors registered with the Indian Securities and Exchange Commission. Foreign portfolio investors may include asset management companies, pension funds, mutual funds, investment trusts, corporate or institutional portfolio managers or their lawyers’ agents, school funds, endowment funds, charities, and charitable trusts. Investments by foreign portfolio investors cannot exceed 10% of the paid-up capital of Indian companies. The sum of investments made by foreign portfolio investors, financial institution investors or qualified foreign investors cannot exceed 24% of the paid-in capital of Indian companies.

(2) Foreign commercial loans. Foreign debt transactions are subject to the foreign exchange loan rules in the Foreign Exchange Control Law. Compared with foreign exchange laws that regulate equity investment, foreign exchange lending rules are relatively strict. Foreign exchange loan rules classify foreign exchange loans based on borrowing terms and risk forecasts, and foreign debt is correspondingly divided into long-term foreign debt and short-term foreign debt. The foreign exchange lending rules stipulate various conditions that should be met for lenders and borrowers in order to make foreign debt transactions eligible for automatic licensing. The rules also restrict the use of external debt and strengthen the regulatory process. Therefore, foreign commercial borrowing is not the most desirable form of investment. The Reserve Bank of India has begun to take measures to further relax restrictions on foreign commercial borrowing, and foreign commercial borrowing will increase in the future. Zh

(3) Other transactions. In addition to investment, foreign exchange laws also apply to other transactions involving foreign exchange, including:

① export, import or hold money or banknotes;

② transfer and acquisition of real estate located outside India;

③ Provide guarantees or guarantees for any loans, obligations or other obligations performed by Indian residents to non-Indian residents. The Foreign Exchange Control Act further stipulates that Indian residents must ensure that the foreign exchange they receive or deserve must be repatriated to India within a certain period of time in accordance with the provisions of the Reserve Bank of India. The foreign exchange law also stipulates that, except for “authorized persons”, any individual is prohibited from trading or transporting any foreign currency or foreign exchange securities in India. “Authorized persons” include authorized dealers, money changers, overseas banking units, or other individuals and units authorized by the Reserve Bank of India.

Severe penalties will be imposed for violations of foreign exchange laws. If the amount of violations can be determined, the penalty may be three times the illegal income. If the amount of the violation cannot be determined, the maximum penalty amounted to Rs 200,000. Penalties can also be calculated based on the number of days of continuing violations.

3. Banks and insurance agencies

As of the end of March 2013, the Indian banking system includes 1 central bank, 26 state-owned commercial banks, 20 private commercial banks, 43 foreign commercial banks, 64 regional rural commercial banks, and 4 regional commercial banks. , 1,606 urban cooperative banks, 93,551 rural cooperative banks. State-owned banks account for about 74% of the total assets of Indian banks, while private banks and foreign banks account for 19% and 7%, respectively.

[Central Bank] The Reserve Bank of India is the Central Bank of India. Its functions include currency issuance, formulating and implementing monetary policies, managing foreign exchange reserves, maintaining currency stability, and supervising the banking system.

[Commercial Banks] The main local commercial banks in India are: State Bank of India (the largest state-owned commercial bank), ICICI Bank (the largest private bank, the second largest commercial bank), Punjab National Bank ( Punjab National Bank (third largest bank), Canara Bank, Indian Industrial Development Bank (IDBI), HDFC Bank (private), etc.

[Foreign banks] India’s major foreign banks include Standard Chartered Bank, HSBC, Citibank, and others.

[Chinese Bank] In September 2011, the Industrial and Commercial Bank of China set up a branch in Mumbai. The Industrial and Commercial Bank of China Mumbai Branch can provide a variety of services for Chinese-funded enterprises in India, including deposits, loans, trade financing, international settlement, and guarantees. The contact telephone number is 0091-22-33155999, and the correspondence address is Level 1, East Wing, Wockhardt Tower, C-2, G Block, Bandra Kurla Complex, Bandra (East), Mumbai, Maharashtra, India, 400051. China Development Bank has a working group in India and is preparing to establish a branch in India.

For a foreign company to open an account with a local bank, in addition to all the materials needed for an ordinary local company to open an account, it also needs a certificate of approval from the Reserve Bank of India. Therefore, to open an account in India, a foreign company must first apply to the Indian central bank to open an account. After approval, it can open a company account in a domestic bank in India.

[Insurance companies] As of the end of 2015, India had a total of 53 insurance companies, including 24 life insurance companies and 29 non-life insurance companies (including reinsurance companies). India’s main insurance companies are: Life Insurance Corporation (India’s largest insurance company), Export Credit Guarantee Corporation (India), GIC Insurance Company (India’s only reinsurance company).

4. Financing services

On October 5, 2018, the Central Bank of India maintained the repo rate at 6.5%. The benchmark interest rate for bank loans is approximately 9.5%, and the overnight lending rate for banks is approximately 6.9%; the interest rate on demand deposits is 4%, and the interest rate on time deposits of more than one year is approximately 6.5%.

Indian law does not allow Indian financial institutions to make rupee loans to foreign companies. Therefore, foreign companies must seek financial assistance at the place of registration. The Reserve Bank of India prohibits such loans from being remitted outside India. However, this provision is reasonable if one considers the difficulty of seeking relief when a foreign company that does not actually operate in India has a default.

However, Indian companies that are owned or controlled by foreign countries are still considered “Indigenous companies in India” under Indian law. Therefore, all foreign company subsidiaries, joint ventures, or invested companies of such foreign companies can still obtain loans from Indian financial institutions. The interest rate of foreign bank loans in India is generally higher than that of local banks in India, but the service quality is better. Foreign companies mostly choose foreign banks as partners.

The use of the loan requires approval from Indian financial institutions. Therefore, in any case, these Indian companies (portfolios, joint ventures or subsidiaries of these foreign companies) must declare the purpose of the loan. Typical financing requirements include:

(1) restrictions on the end use of total loans; (2) restrictions on creating burdens on Indian corporate assets;(3) examination and approval of changes in business or management of Indian enterprises; (4) examination and approval of any divestment, merger or other corporate actions including dividend distribution; (5) restrictions on continued loans by Indian enterprises;

(6) Create a burden on the securities involved.

It should be noted that Indian law does not allow financial support when acquiring equity in Indian local companies. Therefore, even for local Indian companies, domestic loans are hardly a good option for financing during investment and acquisition.

Regarding the issuance of guarantees and reopening of guarantees, there are two cases for foreign companies. The first case is that a foreign company has already established a company in India and established an operating entity. In this case, the procedure for foreign companies to apply for relevant materials from local banks is the same as for local companies. The second case is that a foreign company has not established an operating entity in India, and it needs to seek a bank in its home country to issue a counter-guarantee letter, and then apply for relevant materials to the local bank in India with the counter-guarantee letter.

6. What are the benefits of India for foreign investment?

The Indian government does not have special preferential policies for foreign investment. Enterprises established by foreign investors in India are regarded as local enterprises and must comply with the industrial policies formulated by the Indian government just like Indian enterprises. Only by investing in industrial areas or regions encouraged by the government can foreign capital enjoy the same preferential policies as local Indian companies.

1. Preferential Policy Framework

The preferential policies for foreign investment in India are mainly reflected in regional preferences, export preferences and special economic zone preferences.

2. Industry encouragement policies

The Indian government has implemented the following support measures for specific industries:

(1) “Made in India” investment policy in the manufacturing sector: Foreign direct investment in Indian manufacturing can be licensed without approval. In addition, according to foreign exchange laws and foreign direct investment rules, manufacturers can either wholesale or retail products produced in India, including sales through e-commerce (e-commerce does not require government approval). This coincides with the “Made in India” investment policy formulated by the Indian government to promote the country’s economic development.

(2) “Entrepreneurship in India” policy: Driven by the “Entrepreneurship in India” policy, the Indian government plans to relax various compliance standards. Start-ups can issue hard-earned shares at 50% of paid-in capital within 5 years from the date of their incorporation. Unlisted start-ups can directly or indirectly (through their relatives or any other corporate entity) hold more than 10% of the company’s issued shares to the core employees of the company (must belong to the company’s sponsor or one of the company’s sponsors) Directors implement equity incentive policies. In addition, the Reserve Bank of India allows startups with overseas subsidiaries to open foreign exchange accounts with foreign banks. Startups and their overseas subsidiaries can obtain foreign exchange borrowings through import and export earnings and accounts receivable. Foreign currency account due to outgoing from IndiaThe balance obtained from the export shall be repatriated to India within the prescribed period. In addition, the Indian government also provides the following tax incentives for start-ups: 1 Exemption from income tax on capital gains obtained by investing in funds recognized by the government to provide funds to start-ups; 2 Within 3 years of its establishment, non-distribution Dividend start-ups are exempt from income tax; 3 Exemption from startups that are above fair value for investments.

(3) Air transportation service industry: India automatically permits foreign countries to directly invest in 49% ownership of scheduled air transportation services or domestic scheduled passenger air services, and 100% ownership of air transportation services in regional routes. 100% of the investment objects under the automatic permit path can only be non-scheduled air transport services and helicopter services. However, a few projects should be approved in advance by the Civil Aviation Commission, such as seaplane services.

(4) Construction and development-towns, housing, and combined infrastructure: The Indian government automatically permits foreign countries to make 100% investment in the following construction and development projects when they meet the relevant provisions of the foreign exchange law, including urban construction, Residential or commercial residential construction, roads or bridges, hotels, holiday villages, hospitals, educational institutions, recreational facilities, urban or regional infrastructure.

(5) E-commerce: The Indian government automatically permits foreign countries to invest 100% in B2B e-commerce enterprises.

(6) Railway infrastructure: Foreign investment can participate in the construction of Indian suburban channel projects in the PPP (public-private partnership) mode, such as high-speed rail projects and freight lines. However, these investors must comply with industry guidelines set by the Ministry of Railways and other conditions set out in foreign exchange laws.

(7) National defense: India has expanded its opening up and actively introduced foreign direct investment in the field of defense. As we all know, the Indian government allows foreign countries to invest 100% directly in the field of defense. Before June 2016, the maximum foreign investment in defense enterprises under the auto-licensing path was limited to 49%. In addition, more than 49% of foreign direct investment requires the permission of the Indian Cabinet Security Council, which is limited to the introduction of the latest modern technology and must be reviewed on a case-by-case basis. Now if the investment allows India to access modern technology, the Indian government allows more than 49% of foreign investment to be implemented after government approval. The Indian government has also relaxed foreign investment restrictions on the small arms and ammunition manufacturing industry under the Armed Services Act (1959).

At the same time, in order to streamline the current tax and management system and relax financing restrictions, many related policies are being drafted and will be announced in the near future.

3. Regional encouragement policies

(1) Investing in the northeast Indian states, Kashmir (India Control) and other backward areas can enjoy 10 years of tax exemption, 50% -90% freight subsidy, and equipment import tax exemption depending on the state. The investment amount is 250 million. Projects above rupees enjoy investment subsidies of up to 6 million rupees and interest subsidies of 3% -5%; etc.

(2) Investment in Uttaranchal and Himachal Pradesh is 100% tax-free for the first 5 years, and 25% tax-reduced for the next 5 years.

4. Export encouragement policy

Enterprises that export all products, domestic and foreign enterprises in export processing zones and free trade zones are exempted from income tax for 5 years; companies are exempt from customs duties on imports of machinery and equipment parts and raw materials used to produce export goods; joint ventures in backward regions10 Income tax is reduced by 25% during the year.

(End)

Note: the title of this article is from Pexels

(1) Taxes on 98 and 1211 designated goods;

(2) Taxes on 36 designated services; (3) Reverses 18 designated services Tax collection mechanism; (4) Exemption of tax on 87 designated services. Specific tax items and rates include: for goods, for coal, sugar, tea and coffee, medicines and drugs.

1. Competent authority for work visas

Receiving departments for Indian work visas are Indian embassies (consulates) abroad; the examining and approving departments for Indian work visas are Indian embassies (consulates) and Indian Ministry of Home Affairs. After entering the country, foreigners must apply for a residence permit and apply for an extension from the foreign registration office (FRRO or FRO) where their residence is located.

2. Work permit system

Foreigners working in India must obtain an Employment Visa or a Project Visa newly established for power and metallurgy projects.

Applicants for work visas must be professionally qualified high-tech / high-skilled professionals engaged in routine affairs, secretarial or clerical work, clerks and other relevant personnel who do not require professional skills or high-skills. Within the scope of acceptance. The foreign citizen sponsored by the Indian company must have an annual income of more than $ 25,000 in the Indian company. This requirement does not apply to personnel working in the following areas: Chinese food chefs, language teachers (English language teachers must meet the annual income requirement of more than $ 25,000), translators, and personnel working for the embassies and consulates of the relevant country in India.

2.1 [Persons to issue work visas]

(1)Foreign citizens who are going to India to work in a company or organization (registered in India), or foreign citizens who are engaged in related work in a project operated by a foreign company / organization.

(2) According to the contract for the supply of equipment / machines / tools and other equipment signed by the two parties, foreign engineers or technicians who install and debug machines, equipment or tools and equipment in India

(3) Foreigners who are authorized to travel to India to provide technical support, technical services, transfer of skills, or provide various services to Indian companies that have paid user fees and other fees.

(4) According to the contract, a foreign person who travels to India to work as a consultant and is paid a fixed remuneration (not a monthly salary) by an Indian company.

(5) According to contracts signed with Indian hotels, restaurants, clubs or other units / organizations, foreign artists who regularly perform in the above units during the contract period.

(6) Foreign citizens who are coaching in Indian national or state sports teams or well-known sports clubs.

(7) Foreign athletes who have signed fixed-term contracts with Indian sports clubs or sports organizations.

(8) Self-employed foreigners who travel to India to perform high-skilled services in engineering, medical, financial, legal or other fields as independent technical consultants. If Indian law does not allow it, foreigners cannot work in the field in India.

(9) Teachers or interpreters in Chinese and other languages.

(10) Professional chefs in Chinese cuisine, professional chefs in other countries. According to the memorandum of understanding between China and India on simplification of visa procedures signed in June 2003, p.

The types of work visas that can be issued to Chinese citizens are as follows: 13-month single-round work visa (applicable to opening an office in India, working in India, including work contracting for a certain project); 23-month staff accompanying Single-entry visa for family members; 33-month non-staff travelling spouse / children / relatives single-entry tourist visa. (Tip: Business visas or any other type of visa are not allowed to be converted to work visas. Foreign citizens wishing to obtain a work visa must return to the country where they have permanent residency, apply for a work visa from the Indian embassy / consulate, and provide a visa office All relevant documents needed.)

2.2 [Subject of project visa]

[Subject of project visa] is a foreign citizen who travels to India to work on power or metallurgical projects. Specific requirements include:

(1) Issuing objects are only senior technicians or skilled technicians, semi-skilled and unskilled technicians are not within the scope of issuance;

(2) Project visa holders can only work on the project in India during the validity period of the visa, and may not participate in other project projects of the same company, or participate in project projects of other companies;

(3) Project visa holdersThe scope of activities is limited to the location of the project;

(4) The validity period of the visa is the same as the contract period of the project, but the longest is 1 year with multiple round trips;

(5) Each foreign citizen must have been engaged in the same project for an Indian company for no more than 2 years (counting from the date the project started);

(6) Project visa applicants must submit relevant application materials to prove that an Indian company or organization has signed a project contract with a foreign company;

(7) Only a maximum of two chefs and two translators are allowed per project;

(8) An Indian company must guarantee that foreign personnel who go to the company for project work will leave India before the expiry of their visa;

(9) Project visa holders whose visas are valid for more than 180 days must go to the local foreigner registration office (FRO / FRRO) to complete the registration procedures within 14 days of arrival.

2.2.1 [Electricity Project] Visa

Note: 1 The Indian Electric Power Corporation imported FGD flue gas desulfurization system-related equipment must apply in accordance with the number of additional persons required in the table above. 2 If multiple generating units are newly built at the same location as an independent project, the contract period of the two contracts must be at least one year apart.

Source: Ministry of Home Affairs, India

2.2.2 [Metallurgical Project] Visa

For new construction projects, the number of project visas per million tons of steel output is 10% of the total number of workers, and the maximum number is not more than 300. For the expansion and expansion projects of existing plants, the project visas are granted per million tons of steel output The number is 5% of the total employment, and the maximum number is 150.

3. Application Process

The work visa must be directly applied by the applicant or the applicant’s organization to the Indian Embassy (Consulate) in China.

The Indian embassy (consulate) in India must first report to the Ministry of the Interior, the Ministry of Labor and other departments for approval. Approved by the Indian government approved in India

, or an appointment letter from the Indian company provided by the Chinese employee and a confirmation letter issued by the Indian engineering department on the project and the need to hire Chinese personnel, etc., can generally be processed once every 3 months. Entry work visa. Accompanying family members providing proof of kinship and employmentAfter the main invitation letter, you can get a single entry visa valid for 3 months. The aforesaid personnel should register with the local FRRO or FRO, apply for residence permit and visa extension in sequence within 14 days after entry and 60 days before their visa expires. Once the extension application has been approved, the entry visa can be extended to 1 for 1 month. Multiple entry visas for the year. The application period for each extension of a foreigner’s residence permit and multiple-entry visas does not exceed one year, and the total length of work allowed for one work permit cannot exceed five years. Applicants who have worked in India for more than 5 years will need to reapply for a new work permit. It usually takes 8 weeks or more to apply for a work visa, and 4 weeks or more to extend the approval of a work visa.

At present, India has very strict control over Chinese citizens working in India. It is extremely difficult for general managers and engineering and technical personnel to obtain work visas, and ordinary workers are even unable to obtain related work visas.

4. Provide materials

4.1 [Work Visa Application] Documents to be submitted:

(1) A copy of the employment letter of the Indian company and the contract signed by the two parties; (2) the applicant’s resume; (3) the education / professional experience certificate; (4) the professional skills certificate; (5) the Indian company in accordance with the “Company Law 》 Registration registration license, or the company’s certificate of registration in the Indian state’s industrial department or the Export Promotion Board; (6) Certificate issued by the Public Security Bureau, notarized by the Notary Office, and a record of no criminal record; (7) In the visa review form Other documents required.

4.2 [Project visa application] Documents to be submitted:

(1) A certificate (original or fax) issued by an Indian company that has signed a construction contract or project contract with a Chinese company or agency, which should include the following Information:

1 full name of Chinese company;

2 registered address of Chinese company;

3 project / project name;

4 detailed address of the project in India: state, district, town, village;

> 5 project contract duration (total days); 6 separately list the number of the following Chinese staff who travel to India to work on the project: senior technical staff; proficient technology with a bachelor’s degree in science or engineering or a diploma in science and engineering > Staff;

Skilled workers with secondary professional qualifications.

(2) Letter (original or fax) from the Indian company to the relevant Indian embassies / consulates abroad

The following information must be clearly listed:

1The Indian company guarantees all the acts of the Chinese company and Chinese staff who go to the company to engage in engineering and project work in India;