2020 is expected to become the inflection point of the domestic M & A market

This article comes from the WeChat public account “Hanergy Investment Group” (ID: TheHinaGroup)

On January 16, China and the United States signed the first phase agreement in the early morning, and the boots landed.

For the domestic capital market, this matter has largely eliminated the uncertainty of the external environment, and the expectations of companies and other market participants have improved, becoming the first agent to benefit the M & A market in 2020. Strong heart.

It has been three years since the last wave of mergers and acquisitions.

2019 is the third year of the “L-shaped” sideways of the domestic M & A market. The external environment is uncertain, the internal policies are uncertain, the primary market has no money, and the secondary market has no confidence.

Compared to the ups and downs of U.S. M & A history of more than 100 years, the 30-year-old Chinese capital market is like a enthusiastic young man who has gone through the history of U.S. M & A for decades in less than 20 years. In the past, we have more reasons to believe that this young and vigorous market will soon usher in its own golden age.

Three years of consolidation and dormancy, from fanaticism to panic to being forced to calm down, all participants in the M & A market have gradually matured and rationalized, hot money everywhere, price-earnings games, in-and-out arbitrage, and “market value management” The buzzword is attributed to the old paper pile. Industrial logic, as a larger internal factor, drives the development and maturity of the M & A market.

Looking back at the M & A market over the past year.

Internet giants are no longer competing as a money bag in the investment circle, regaining the vision of ambitions, focusing on the present and future of the main business, and using “focus” and “overweight” to firmly reserve new momentum for their own continuous growth .

State-owned enterprises have emerged as a compelling buyer force. In the process of buying and buying, “seeking incremental synergies” is the core driving force for “marriage” between state-owned enterprises and private listed companies.

A shares are “really fragrant”, light loading and favorable policies make us have more expectations for the development of the A share M & A market.

Looking forward to the new year, we believe that China’s M & A market will embark on a rational and stable development track after “growing pains”.

Macro market judgment

2020 is expected to become an inflection point in the domestic M & A market

2019 is the third year at the bottom of the “L-shape” in the domestic M & A market.

Approximately 2,500 M & A transactions were completed throughout the year, and the value of M & A transactions was approximately 1.4 trillion. Since 2017, M & A transactions have fallen to the level of 1.5 trillion, and have been low for two years since then.

The reason for last year’s sluggish trading is that there is no money in the primary market and no confidence in the secondary market.

The implementation of the new rules on asset management has hindered the use of high leverage methods such as prior-inferior, inferior, stock pledge, and M & A loans. Therefore, we have seen that the amount of fundraising in the primary market in 19 years has continued to decline, and market capitalization has continued Fleeing, the state-owned LP became the main investor.

In the context of domestic and foreign difficulties, A shares began to fall and fall for two years at the beginning of 18 years. The rebound has been less than 4 months. Listed companies have lost the favorable weapon of issuance and merger in a depression. dramatically drop. The poor exit channel of the secondary market spreads forward, affecting the rhythm of investment in the primary market.

We predict that the dormant period of the M & A market is about to pass, and the macro environment in 2020 has shown a trend of comprehensive recovery. It is mainly reflected in the following four points:

-

International trade has entered the second stage of negotiations, and its marginal impact on the operation of the domestic economy has continued to weaken.

-

The domestic financing cost has continued to decrease. The Central Economic Work Conference mentioned that it is necessary to continue to “reduce social financing costs.” It has lowered its quota three times in 19 years and released over trillions of stock funds.

-

The bottom of the M & A policy has already emerged. The 19-year supervision has encouraged corporate mergers and acquisitions by simplifying the review, adjusting the locking mechanism, and allowing the GEM to borrow money.

-

The smooth operation of the Science and Technology Innovation Board and the forthcoming GEM registration system will bring more diversified investment options and increase the enthusiasm of all parties in the capital market for investment and mergers and acquisitions.

So we predict that 2020 is expected to become the inflection point at the bottom of the “L-shape”, and the M & A market will gradually recover and usher in spring.

Industrial M & A is a new trend

Reviewing the five wave of mergers and acquisitions in the United States in the 20th century and the merger and acquisition phase in China in the past 20 years, One obvious finding is that the more mature the mergers and acquisitions market, the more emphasis is placed on industrylogic.

Several mergers and acquisitions in the early 20th century were mainly driven by financial logic. For example, “share issuance and mergers” set off the second wave of mergers and acquisitions, “effective frontier theory” set off the third wave of mergers and acquisitions, and “leverage acquisition” set off the fourth wave of mergers and acquisitions, in an immature market Mergers and acquisitions that target market value management or arbitrage arbitrage frequently occur.

But with the maturity of the US market, the weight of industrial mergers and acquisitions has gradually increased . It can be seen that during the fifth wave of mergers and acquisitions in the 1990s, many typical transactions have the characteristics of industrial integration. At the time, when oil prices fell, Exxon and Mobil oil companies exchanged and merged; the federal government opened the bank After the mixed operation control, JP Morgan and Chase Bank exchanged shares to merge; in the Internet tide, leading companies made a series of acquisitions to consolidate the status of the industry, pulling the future rivals to their own camp with a small price, such as Facebook for only 1 billion US dollars With the acquisition of Instagram, Google captured Youtube for only $ 1.6 billion, and according to media estimates, the independent valuation of Instagram and Youtube has now exceeded $ 100 billion.

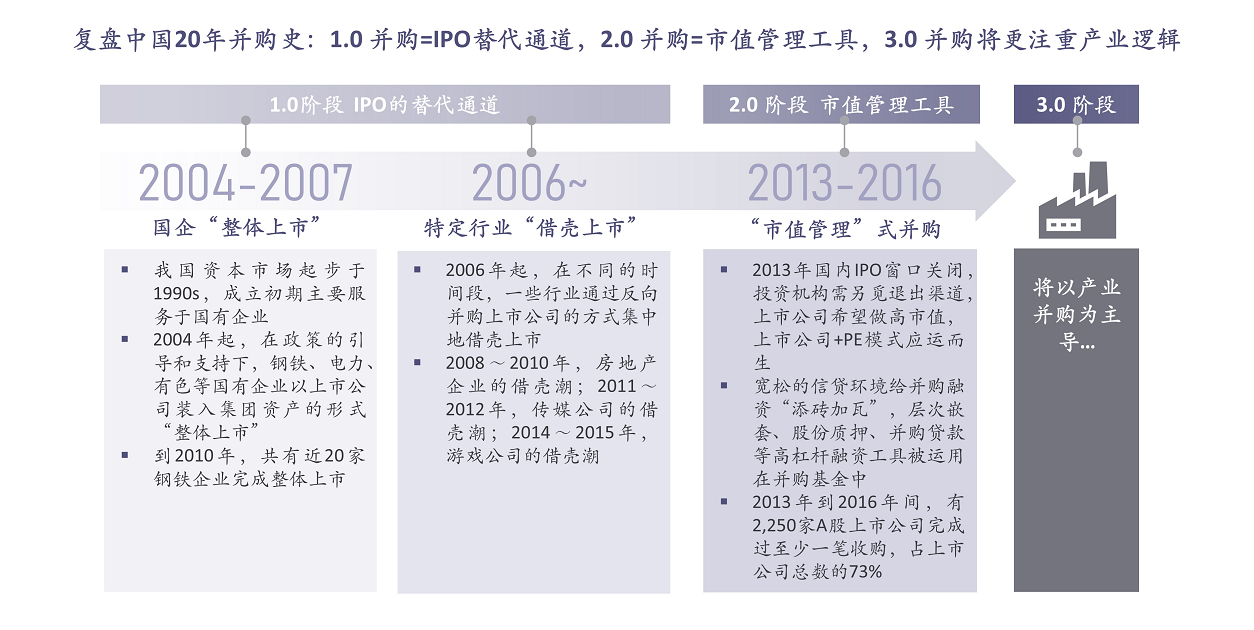

The history of China’s mergers and acquisitions is relatively short. In 2002, the Securities Regulatory Commission issued the first edition of the “Administrative Measures for the Acquisition of Listed Companies”, which marked the beginning of China’s mergers and acquisitions market.

The first stage of China’s mergers and acquisitions only serves as a substitute for IPOs : Since 2004, state-owned enterprises such as iron and steel, power, and nonferrous metals have achieved “overall listing” in the form of listed companies’ mergers and acquisitions of group assets, 2006 Since the beginning of the year, the real estate, media and other industries have focused on backdoor listing through reverse mergers and acquisitions of listed companies.

The second stage of China ’s mergers and acquisitions is a market value management tool for listed companies. Between 2013 and 2016, driven by domestic IPO barrier lakes, loose credit environment, long-term bull market and other factors, the company went public. Companies tend to operate M & A funds and earn valuation differences in the primary and secondary markets. According to Wind data, during the “M & A boom” from 2013 to 2016, more than 70% of listed companies in the A-share market had external acquisitions.

China’s M & A market has experienced more than 20 years of development and has become more and more mature. In the third stage of M & A in the future, it will become more industrial and rational.

Review of annual market highlights

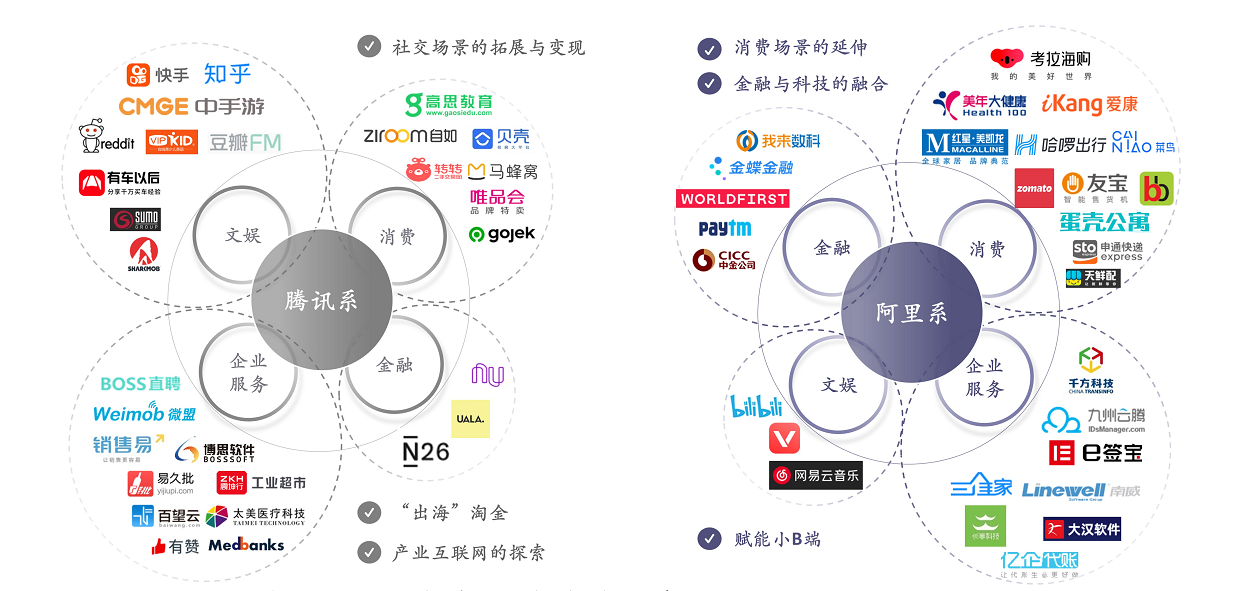

In the “Winter”, Internet giants are ploughing

1. “Focus” and “continuous coding” are keywords

Look first at Focus . Let’s take the Tencent Department as an example to see several key directions in 2019:

-

Large entertainment, big consumption The expansion and realization of the social scene is the long-term focus of the Tencent Department, and it will naturally continue in 2019.

-

Industrial Internet is in the early stages of the layout. By incorporating various types of to B companies into the investment portfolio, you can quickly achieve online / offline, large, medium and small types Indirect coverage of corporate customers. For example, BOSS has directly recruited a large number of diversified B-end customers, such as direct employment, sales, and Weimeng, while Yi Jiu Pian and Zhen Kun Xing have focused on online / offline linkage scenarios. Therefore, strategic investment as a medium can effectively expand the “range” of the Tencent-based industrial Internet.

-

“Going out and going to the sea” is the consensus of the Internet community in the past two years. The Tencent Department has also made a layout around areas such as technology and finance.

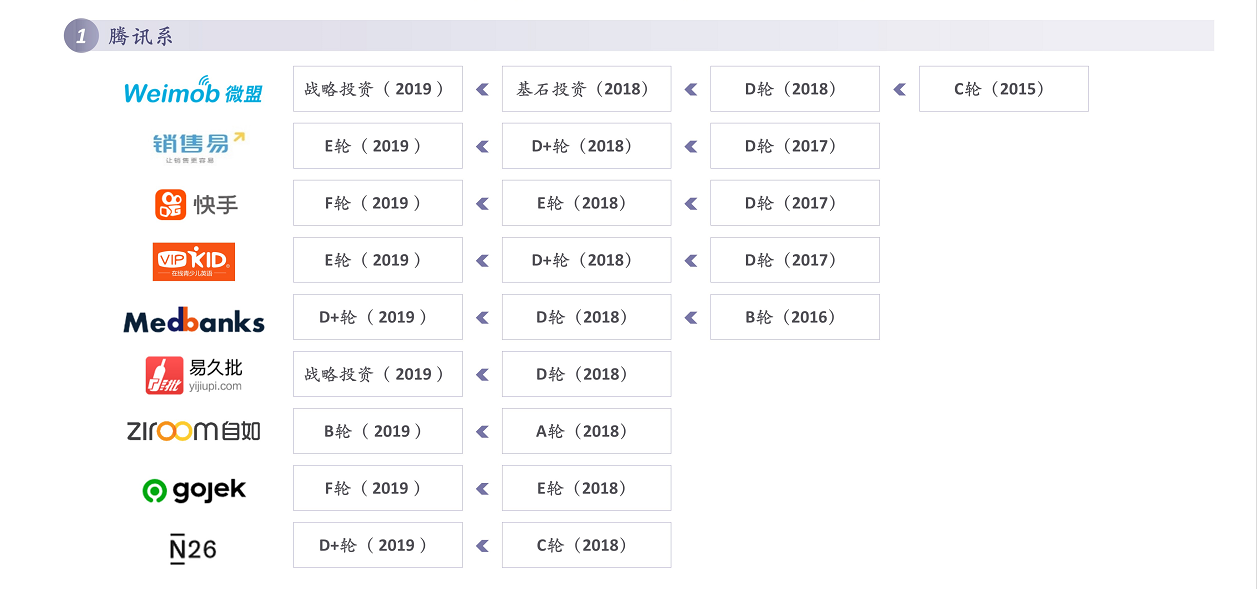

SecondCheck out “Continuous Overweight” . There are two reasons for the projects that the giants can follow up and love deeply:

-

These companies are located in the direction of the giants’ heavy bets, which is in line with their “appetite”.

-

As these companies continue to grow, they have also become “small giants” in the segmented field. Continued follow-up will help these “little giants” continue to expand their competitive advantages, making the giants effectively form indirect influence and control in the segmented areas. For example, Tencent has continuously raised Weimeng before and after listing, and Weimeng has grown into a leading provider of cloud commerce and marketing solutions for SMEs and a leading provider of precision marketing services for SMEs on Tencent’s social network service platform.

2. What is the inspiration for us?

2. What is the inspiration for us?

Finally, we can see that dancing with the giants is essential for doing what you want. A deep understanding of the fit between the business direction and the strategic layout of the giants, and the synergies between existing businesses are the key points to get bets and re-bets from the giants.

State-owned enterprises buy buy buy, “scanning goods” A-share listed companies

When we look at another market with a larger amount and more active trading, that is, the control trading market of A-share listed companies, we can see that state-owned enterprises have emerged as a remarkable buyer force.

1. What is the logic behind it?

We understand that the formation of a win-win situation through transactions, that is, seeking for incremental synergies is the core driving force for the “marriage” of state-owned and private listed companies.

In general, this includes:

-

OppositeCity companies’ relief and relief.

-

State-owned background support. The Oriental Garden, which will be analyzed later, fully enjoys the support of various resources from finance to industry.

-

Integration of the industry chain.

2. What are the characteristics of 2019?

Complex and diversified transaction methods, and more mature and refined business arrangements, are the common characteristics of related transactions in 2019.

-

First look at Transaction methods . In the “eighteen weapons” of A-share control transactions, in addition to the most mainstream purchase of old stocks, the use of “auxiliary weapons” (such as entrustment and abandonment of voting rights) is not uncommon. At the same time, there are also “cold weapons” (such as part of the offer, that is, to issue an offer to all shareholders to acquire some shares to acquire / consolidate control) and once again “out of the river.”

-

Look at Commercial arrangements . Compared with the original thick-line arrangements, which are mainstream, paying attention to post-trade arrangements has become a “basic operation.”

3. What are the salient features of typical cases?

We have selected two distinctive cases for a brief analysis. One is that Chaoyang State-owned Assets Center “owns” the Oriental Garden and helps it “solve concerns”, and the other is Shanghai Electric ’s subdivision of the industry in its strategic layout. The leading company wins technology.

-

The outstanding feature of the Oriental Garden case is the support effectiveness of the Chaoyang State-owned Assets Center after it became a master, including: (1) In terms of financing, the cost has been reduced from about 10% to the newly signed The average part does not exceed 6%, the debt period has been extended, and the financing channels have also been expanded. (2) Oriental Garden has actively explored related businesses in Chaoyang District and Beijing.

-

The prominent feature of the case of Yinghe Technology is the binding with the original actual controller / management : (1) The original actual controller made a performance commitment and agreed not to Compensation when the target is reached, and share pledge as the corresponding “insurance measure”; (2) Corresponding to performance commitments, the original actual controller and management can also enjoy excess performance rewards after reaching certain performance indicators.

A shares: Looking back, Begonia still remains

1. The core source of attraction: valuation or valuation

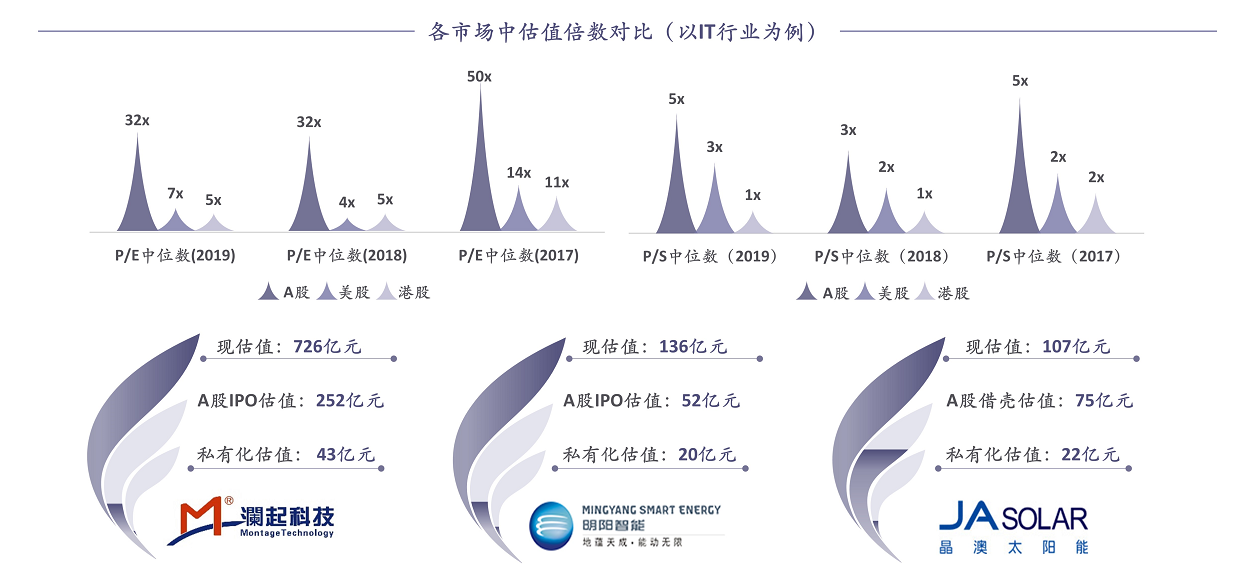

We take the IT industry as an example and compareIn the past three years, the median P / S and P / E multiples of A shares, U.S. stocks, and Hong Kong stocks can be seen. A shares have obvious advantages in valuation multiples. For example, P / S multiples are about 2-5 in other markets in the same period. Times.

From another perspective, we reviewed the valuation performance comparisons of companies listed, privatized, and re-listed on A shares in other markets. Taking Lanqi Technology as an example, the valuation at the end of 2019 has reached about 17 times the valuation of privatization, which fully illustrates the core motivation of the return of Yan: valuation difference.

2. Impairment of goodwill creates conditions for listed companies to “go light”

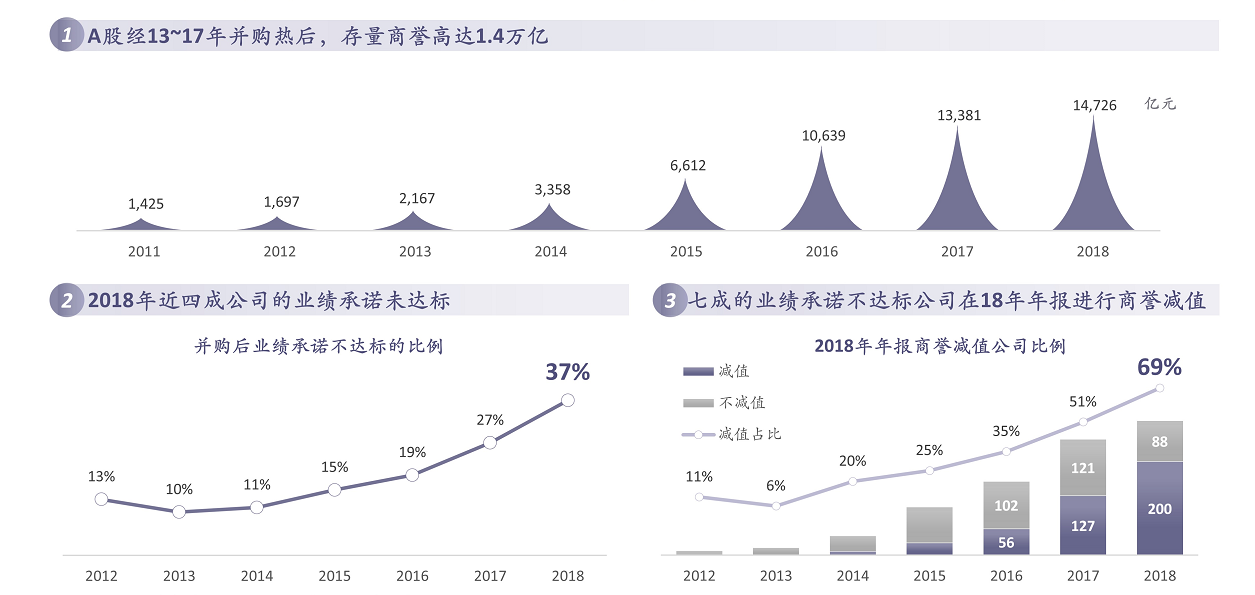

After 13 to 17 years of accumulation, the stock of goodwill in the 18-year annual report of the A-share market has reached 1.4 trillion. Behind the high goodwill is the “Haikou” that listed companies once boasted. Every company can realize its original beautiful vision-the proportion of companies that have failed to meet the A-share performance promise in 2018 has reached 37%.

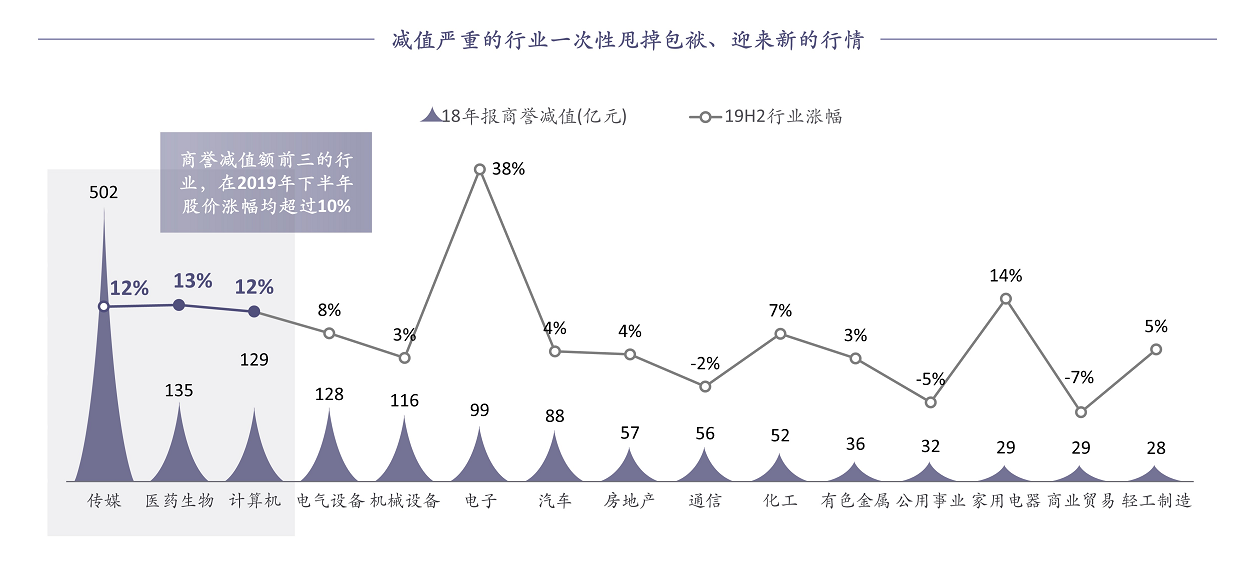

Under such pressure, 70% of companies that have failed to meet performance standards choose to conduct goodwill impairment in the 18-year annual report, and the capital market has also responded positively to this. The computer industry, in the second half of 19, the sector rose by more than 10%. Impairment of goodwill has helped these “high” companies throw away their burdens and usher in a new life.

3. The mature regulatory environment continues to add charm to A shares

Reviewing the regulatory logic in recent years, we can be roughly divided into the following three stages.

-

2013-2015, a relatively early stage of great development of the M & A market. The prominent feature of this stage is that the environment is very conducive to the development of the A-share M & A market, and the awakening of market value management awareness and the budding of M & A tools have further contributed to this stage. Finally, the multi-factor resonance, formed a period of rapid development, the blooming of flowers in this period is as striking as the various problems shown.

-

From 2016 to 2018, starting with the 2016 edition of the “Management Measures for Major Asset Reorganizations”, the regulatory direction has undergone a profound change. Generally speaking, it can be divided into two aspects: (1) the supervision and supervision system is further improved . For example, the “sharp” and professional exchange inquiry letters and media briefings that are gradually becoming familiar to the public have formed an important part of the supervision and supervision system at this stage; (2) The regulatory situation is becoming stricter. In particular, the negative attitude towards market chaos and the introduction of new regulations have had a profound impact on the market. Taken as a whole, this period constitutes a tightening phase aimed at clearing the source .

-

In 2019, we see two very important trends: (1) Appropriate relaxation of the regulatory situation , such as the “Regulations on the Management of Major Assets Reorganization”, Revisions, etc., fully reflect the balance between the regulatory concept and market demand; (2) The icebreaking of the science and technology board and the revision of the Securities Law have become a landmark event for further marketization of the A-share market . As a result, it not only attracted more companies to log in to A shares, but also further enriched buyer resources in M & A transactions.

As a whole, the regulatory environment is gradually maturing with the current market conditions and market needs, and a more mature and advancing regulatory environment will naturally help A shares The market is developing steadily upwards, attracting the landing of high-quality companies.

New year, new expectations: who will benefit from a mature M & A market?

Looking back, maturation and rationalization are trends and keywords

From a macro perspective, the overall environment related to domestic mergers and acquisitions is becoming more mature and rational. Looking back at the history of Sino-US mergers and acquisitions, they have all gone from boom to rationality, from explosive development to maturity. Returning to the original intention of the industry and taking into account financial logic is the only way for M & A and reorganization.

Medium and micro perspective, market participationThe participants are moving towards maturity and rationality. This is whether it is the dynamic balance that is gradually formed between the regulatory philosophy and market demands, or the changes that the transaction party has experienced after passing through the “gold rush” era and accumulating rich experience and lessons. Vivid manifestation.

Looking forward to 2020, expect mature, rational and professional participants to benefit from the times and market opportunities

There is no doubt that the irrational era of hot money and “price-earnings ratio games” has gone, and the new era is also breeding new opportunities. We believe that the following three types of participants will become a new era in the Chinese M & A market:

-

Mature, rational industrial integrator. When the market is in the doldrums, it provides buyers with real industrial integration capabilities with excellent entry opportunities, abundant alternative spaces, and other favorable conditions, which are just good for them to earn real gold. Therefore, through the organic unification of industrial logic and financial logic, it is not surprising to achieve a double harvest of industry and finance.

-

Funds with professional post-investment management capabilities . The era of extensive and “stocking” post-investment management is over. More and more investment institutions are paying attention to actively improving the operational and commercial capabilities of the investees. Whether they have the initiative to exit and complete the transaction has become an active exit New standards for measuring fund professionalism.

-

Professional intermediaries. A M & A transaction needs the services of a professional investment bank from idea, because the professional investment bank will coordinate all aspects of the transaction. The full-process, high-value services provided by professional investment banks are one of the main conditions for improving the success rate of transactions. In addition, proper handling of legal affairs, taxation and other issues can not be separated from the professional work of lawyers, tax accountants, accountants and so on.

We look forward to working with mature, rational and professional market participants to seize the new opportunities brought by the new era.

International trade has entered the second stage of negotiations, and its marginal impact on the operation of the domestic economy has continued to weaken.

The domestic financing cost has continued to decrease. The Central Economic Work Conference mentioned that it is necessary to continue to “reduce social financing costs.” It has lowered its quota three times in 19 years and released over trillions of stock funds.

The bottom of the M & A policy has already emerged. The 19-year supervision has encouraged corporate mergers and acquisitions by simplifying the review, adjusting the locking mechanism, and allowing the GEM to borrow money.

The smooth operation of the Science and Technology Innovation Board and the forthcoming GEM registration system will bring more diversified investment options and increase the enthusiasm of all parties in the capital market for investment and mergers and acquisitions.

So we predict that 2020 is expected to become the inflection point at the bottom of the “L-shape”, and the M & A market will gradually recover and usher in spring.

Industrial M & A is a new trend

Reviewing the five wave of mergers and acquisitions in the United States in the 20th century and the merger and acquisition phase in China in the past 20 years, One obvious finding is that the more mature the mergers and acquisitions market, the more emphasis is placed on industrylogic.

Several mergers and acquisitions in the early 20th century were mainly driven by financial logic. For example, “share issuance and mergers” set off the second wave of mergers and acquisitions, “effective frontier theory” set off the third wave of mergers and acquisitions, and “leverage acquisition” set off the fourth wave of mergers and acquisitions, in an immature market Mergers and acquisitions that target market value management or arbitrage arbitrage frequently occur.

But with the maturity of the US market, the weight of industrial mergers and acquisitions has gradually increased . It can be seen that during the fifth wave of mergers and acquisitions in the 1990s, many typical transactions have the characteristics of industrial integration. At the time, when oil prices fell, Exxon and Mobil oil companies exchanged and merged; the federal government opened the bank After the mixed operation control, JP Morgan and Chase Bank exchanged shares to merge; in the Internet tide, leading companies made a series of acquisitions to consolidate the status of the industry, pulling the future rivals to their own camp with a small price, such as Facebook for only 1 billion US dollars With the acquisition of Instagram, Google captured Youtube for only $ 1.6 billion, and according to media estimates, the independent valuation of Instagram and Youtube has now exceeded $ 100 billion.

The history of China’s mergers and acquisitions is relatively short. In 2002, the Securities Regulatory Commission issued the first edition of the “Administrative Measures for the Acquisition of Listed Companies”, which marked the beginning of China’s mergers and acquisitions market.

The first stage of China’s mergers and acquisitions only serves as a substitute for IPOs : Since 2004, state-owned enterprises such as iron and steel, power, and nonferrous metals have achieved “overall listing” in the form of listed companies’ mergers and acquisitions of group assets, 2006 Since the beginning of the year, the real estate, media and other industries have focused on backdoor listing through reverse mergers and acquisitions of listed companies.

The second stage of China ’s mergers and acquisitions is a market value management tool for listed companies. Between 2013 and 2016, driven by domestic IPO barrier lakes, loose credit environment, long-term bull market and other factors, the company went public. Companies tend to operate M & A funds and earn valuation differences in the primary and secondary markets. According to Wind data, during the “M & A boom” from 2013 to 2016, more than 70% of listed companies in the A-share market had external acquisitions.

China’s M & A market has experienced more than 20 years of development and has become more and more mature. In the third stage of M & A in the future, it will become more industrial and rational.

Review of annual market highlights

In the “Winter”, Internet giants are ploughing

1. “Focus” and “continuous coding” are keywords

Look first at Focus . Let’s take the Tencent Department as an example to see several key directions in 2019:

-

Large entertainment, big consumption The expansion and realization of the social scene is the long-term focus of the Tencent Department, and it will naturally continue in 2019.

-

Industrial Internet is in the early stages of the layout. By incorporating various types of to B companies into the investment portfolio, you can quickly achieve online / offline, large, medium and small types Indirect coverage of corporate customers. For example, BOSS has directly recruited a large number of diversified B-end customers, such as direct employment, sales, and Weimeng, while Yi Jiu Pian and Zhen Kun Xing have focused on online / offline linkage scenarios. Therefore, strategic investment as a medium can effectively expand the “range” of the Tencent-based industrial Internet.

-

“Going out and going to the sea” is the consensus of the Internet community in the past two years. The Tencent Department has also made a layout around areas such as technology and finance.

SecondCheck out “Continuous Overweight” . There are two reasons for the projects that the giants can follow up and love deeply:

-

These companies are located in the direction of the giants’ heavy bets, which is in line with their “appetite”.

-

As these companies continue to grow, they have also become “small giants” in the segmented field. Continued follow-up will help these “little giants” continue to expand their competitive advantages, making the giants effectively form indirect influence and control in the segmented areas. For example, Tencent has continuously raised Weimeng before and after listing, and Weimeng has grown into a leading provider of cloud commerce and marketing solutions for SMEs and a leading provider of precision marketing services for SMEs on Tencent’s social network service platform.

Finally, we can see that dancing with the giants is essential for doing what you want. A deep understanding of the fit between the business direction and the strategic layout of the giants, and the synergies between existing businesses are the key points to get bets and re-bets from the giants.

State-owned enterprises buy buy buy, “scanning goods” A-share listed companies

When we look at another market with a larger amount and more active trading, that is, the control trading market of A-share listed companies, we can see that state-owned enterprises have emerged as a remarkable buyer force.

1. What is the logic behind it?

We understand that the formation of a win-win situation through transactions, that is, seeking for incremental synergies is the core driving force for the “marriage” of state-owned and private listed companies.

In general, this includes:

-

OppositeCity companies’ relief and relief.

-

State-owned background support. The Oriental Garden, which will be analyzed later, fully enjoys the support of various resources from finance to industry.

-

Integration of the industry chain.

2. What are the characteristics of 2019?

Complex and diversified transaction methods, and more mature and refined business arrangements, are the common characteristics of related transactions in 2019.

-

First look at Transaction methods . In the “eighteen weapons” of A-share control transactions, in addition to the most mainstream purchase of old stocks, the use of “auxiliary weapons” (such as entrustment and abandonment of voting rights) is not uncommon. At the same time, there are also “cold weapons” (such as part of the offer, that is, to issue an offer to all shareholders to acquire some shares to acquire / consolidate control) and once again “out of the river.”

-

Look at Commercial arrangements . Compared with the original thick-line arrangements, which are mainstream, paying attention to post-trade arrangements has become a “basic operation.”

3. What are the salient features of typical cases?

We have selected two distinctive cases for a brief analysis. One is that Chaoyang State-owned Assets Center “owns” the Oriental Garden and helps it “solve concerns”, and the other is Shanghai Electric ’s subdivision of the industry in its strategic layout. The leading company wins technology.

-

The outstanding feature of the Oriental Garden case is the support effectiveness of the Chaoyang State-owned Assets Center after it became a master, including: (1) In terms of financing, the cost has been reduced from about 10% to the newly signed The average part does not exceed 6%, the debt period has been extended, and the financing channels have also been expanded. (2) Oriental Garden has actively explored related businesses in Chaoyang District and Beijing.

-

The prominent feature of the case of Yinghe Technology is the binding with the original actual controller / management : (1) The original actual controller made a performance commitment and agreed not to Compensation when the target is reached, and share pledge as the corresponding “insurance measure”; (2) Corresponding to performance commitments, the original actual controller and management can also enjoy excess performance rewards after reaching certain performance indicators.

A shares: Looking back, Begonia still remains

1. The core source of attraction: valuation or valuation

We take the IT industry as an example and compareIn the past three years, the median P / S and P / E multiples of A shares, U.S. stocks, and Hong Kong stocks can be seen. A shares have obvious advantages in valuation multiples. For example, P / S multiples are about 2-5 in other markets in the same period. Times.

From another perspective, we reviewed the valuation performance comparisons of companies listed, privatized, and re-listed on A shares in other markets. Taking Lanqi Technology as an example, the valuation at the end of 2019 has reached about 17 times the valuation of privatization, which fully illustrates the core motivation of the return of Yan: valuation difference.

2. Impairment of goodwill creates conditions for listed companies to “go light”

After 13 to 17 years of accumulation, the stock of goodwill in the 18-year annual report of the A-share market has reached 1.4 trillion. Behind the high goodwill is the “Haikou” that listed companies once boasted. Every company can realize its original beautiful vision-the proportion of companies that have failed to meet the A-share performance promise in 2018 has reached 37%.

Under such pressure, 70% of companies that have failed to meet performance standards choose to conduct goodwill impairment in the 18-year annual report, and the capital market has also responded positively to this. The computer industry, in the second half of 19, the sector rose by more than 10%. Impairment of goodwill has helped these “high” companies throw away their burdens and usher in a new life.

3. The mature regulatory environment continues to add charm to A shares

Reviewing the regulatory logic in recent years, we can be roughly divided into the following three stages.

-

2013-2015, a relatively early stage of great development of the M & A market. The prominent feature of this stage is that the environment is very conducive to the development of the A-share M & A market, and the awakening of market value management awareness and the budding of M & A tools have further contributed to this stage. Finally, the multi-factor resonance, formed a period of rapid development, the blooming of flowers in this period is as striking as the various problems shown.

-

From 2016 to 2018, starting with the 2016 edition of the “Management Measures for Major Asset Reorganizations”, the regulatory direction has undergone a profound change. Generally speaking, it can be divided into two aspects: (1) the supervision and supervision system is further improved . For example, the “sharp” and professional exchange inquiry letters and media briefings that are gradually becoming familiar to the public have formed an important part of the supervision and supervision system at this stage; (2) The regulatory situation is becoming stricter. In particular, the negative attitude towards market chaos and the introduction of new regulations have had a profound impact on the market. Taken as a whole, this period constitutes a tightening phase aimed at clearing the source .

-

In 2019, we see two very important trends: (1) Appropriate relaxation of the regulatory situation , such as the “Regulations on the Management of Major Assets Reorganization”, Revisions, etc., fully reflect the balance between the regulatory concept and market demand; (2) The icebreaking of the science and technology board and the revision of the Securities Law have become a landmark event for further marketization of the A-share market . As a result, it not only attracted more companies to log in to A shares, but also further enriched buyer resources in M & A transactions.

As a whole, the regulatory environment is gradually maturing with the current market conditions and market needs, and a more mature and advancing regulatory environment will naturally help A shares The market is developing steadily upwards, attracting the landing of high-quality companies.

New year, new expectations: who will benefit from a mature M & A market?

Looking back, maturation and rationalization are trends and keywords

From a macro perspective, the overall environment related to domestic mergers and acquisitions is becoming more mature and rational. Looking back at the history of Sino-US mergers and acquisitions, they have all gone from boom to rationality, from explosive development to maturity. Returning to the original intention of the industry and taking into account financial logic is the only way for M & A and reorganization.

Medium and micro perspective, market participationThe participants are moving towards maturity and rationality. This is whether it is the dynamic balance that is gradually formed between the regulatory philosophy and market demands, or the changes that the transaction party has experienced after passing through the “gold rush” era and accumulating rich experience and lessons. Vivid manifestation.

Looking forward to 2020, expect mature, rational and professional participants to benefit from the times and market opportunities

There is no doubt that the irrational era of hot money and “price-earnings ratio games” has gone, and the new era is also breeding new opportunities. We believe that the following three types of participants will become a new era in the Chinese M & A market:

-

Mature, rational industrial integrator. When the market is in the doldrums, it provides buyers with real industrial integration capabilities with excellent entry opportunities, abundant alternative spaces, and other favorable conditions, which are just good for them to earn real gold. Therefore, through the organic unification of industrial logic and financial logic, it is not surprising to achieve a double harvest of industry and finance.

-

Funds with professional post-investment management capabilities . The era of extensive and “stocking” post-investment management is over. More and more investment institutions are paying attention to actively improving the operational and commercial capabilities of the investees. Whether they have the initiative to exit and complete the transaction has become an active exit New standards for measuring fund professionalism.

-

Professional intermediaries. A M & A transaction needs the services of a professional investment bank from idea, because the professional investment bank will coordinate all aspects of the transaction. The full-process, high-value services provided by professional investment banks are one of the main conditions for improving the success rate of transactions. In addition, proper handling of legal affairs, taxation and other issues can not be separated from the professional work of lawyers, tax accountants, accountants and so on.

We look forward to working with mature, rational and professional market participants to seize the new opportunities brought by the new era.

-

-

-

-

-

-