Produced by Arterial Network

Editor’s Note: This article is from WeChat public account “ Artist Network ” ( ID: vcbeat), author Hao Han.

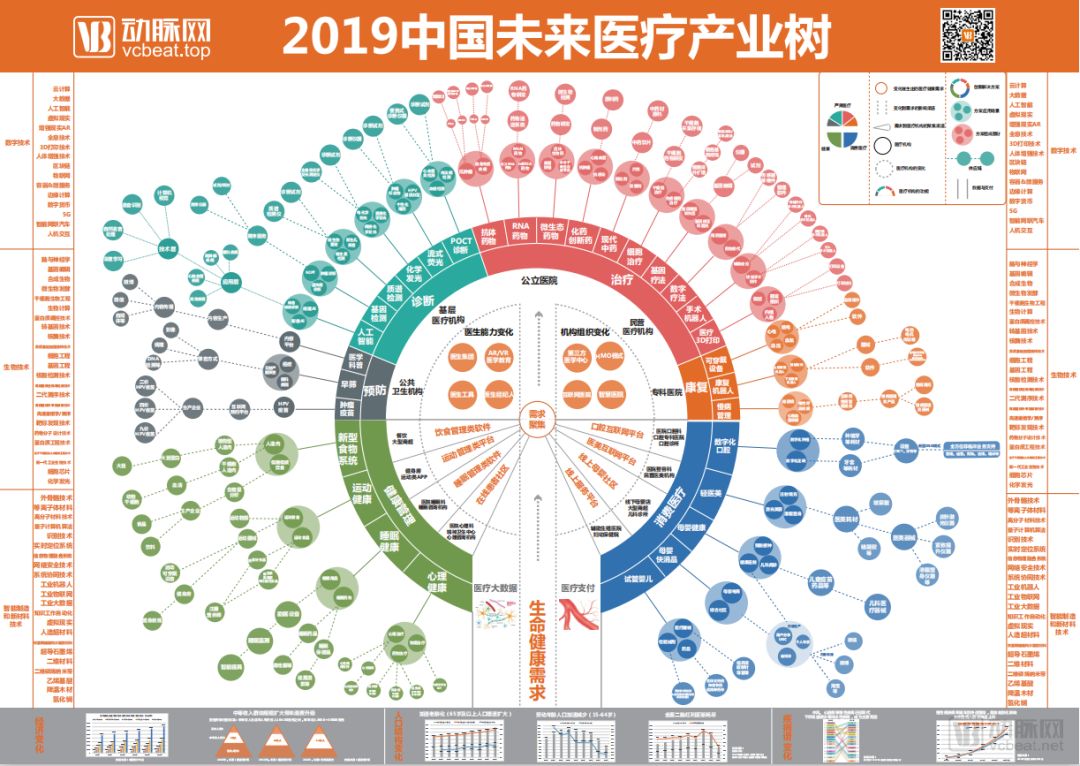

The Arterial Network Eggshell Research Institute has continuously tracked and researched new medical technologies and new models over the past five years, and summarized models such as “domain” models, medical impossible triangles, and medical big data bows. The Future Medical 100 Annual Conference released the 2019 Future Medical Industry Tree Report. This article is an excerpt from a report.

In the course of our research, we found that, subject to the traditional structural framework system with the core structure above and below the medical industry as the core, it is difficult for the innovation part to find a corresponding position and a reasonable logical framework. I hope to present some of our thoughts in this report:

①Follow the core change of demand, analyze the demand trends of medical service organizations from the four directions of society, economy, policy, ecology, etc.

② Make a map of medical and health innovation industry;

③Exploring solutions in subdivided fields, analyzing the required scenarios, tools and business cases under technological innovation and model innovation.

2019 China’s future medical industry tree (Due to the limited resolution of the compression ratio, this high-resolution big picture of the “Future Medical Industry Tree” can be obtained for free in the report area of the arterial network)

The origin of the industrial tree

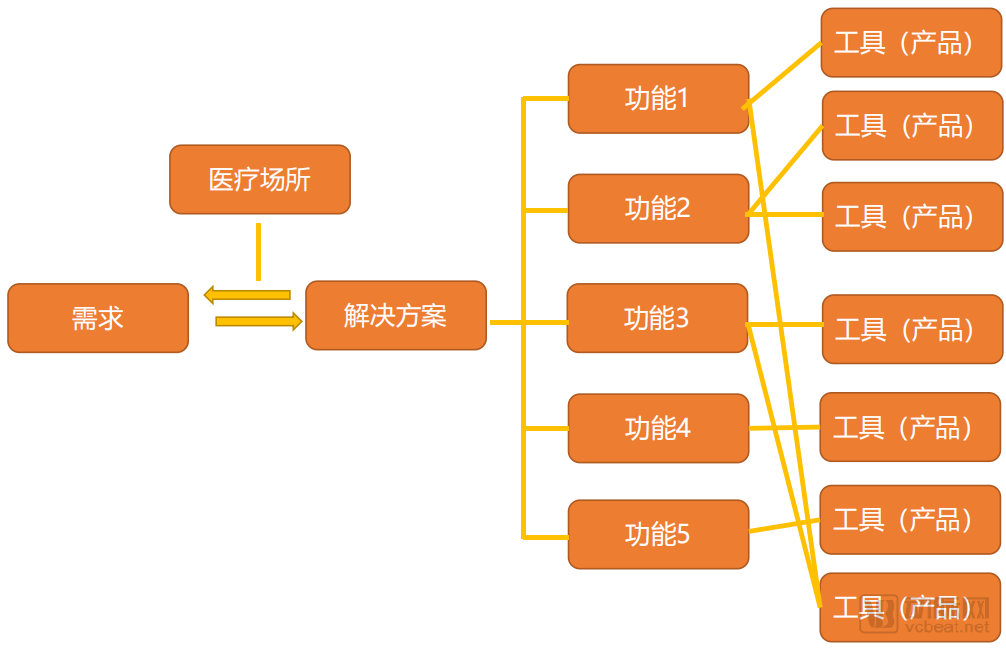

In the medical industry, we divide patient needs into treatment needs, health maintenance needs, and “better needs”. These needs are met in medical facilities that are mainly medical institutions. These medical institutions use doctors + medical functions through the use of Device as an integrated solution to meet the needs of patients; industry research is mining this setThe functional composition and enterprise situation behind the solution, through long-term tracking, insight into industry changes.

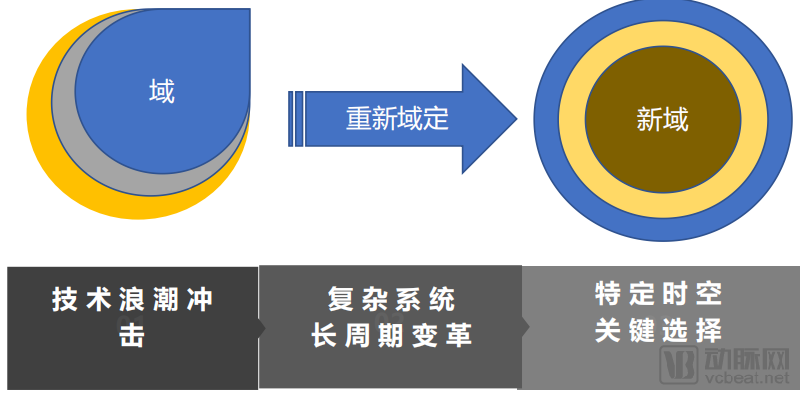

The domain model is the source model of the research on the arterial network industry. We believe that only great changes can bring about great opportunities. The dilemma of industrial development will reach a new equilibrium through reform, which is a major opportunity for all interested parties.

1. Ecological composition: the underlying technology, the distribution pattern of benefits formed on this basis, the rules mechanism and regulations for coordinating social operations.

2. Domain and re-domain: When the key technologies in the domain gradually evolve and eventually change fundamentally, the old domain will transition to the new domain, and the economic operation mode will reach new stability based on this process. Become re-localized.

3. Relational time: The process from the old domain to the new domain is rarely accomplished overnight. It usually takes 20 years or more. This time is called the relational time by philosophers.

Based on the domain model, Arterial Network put forward a series of related inferences to help understand and recognize the development process of the industry.

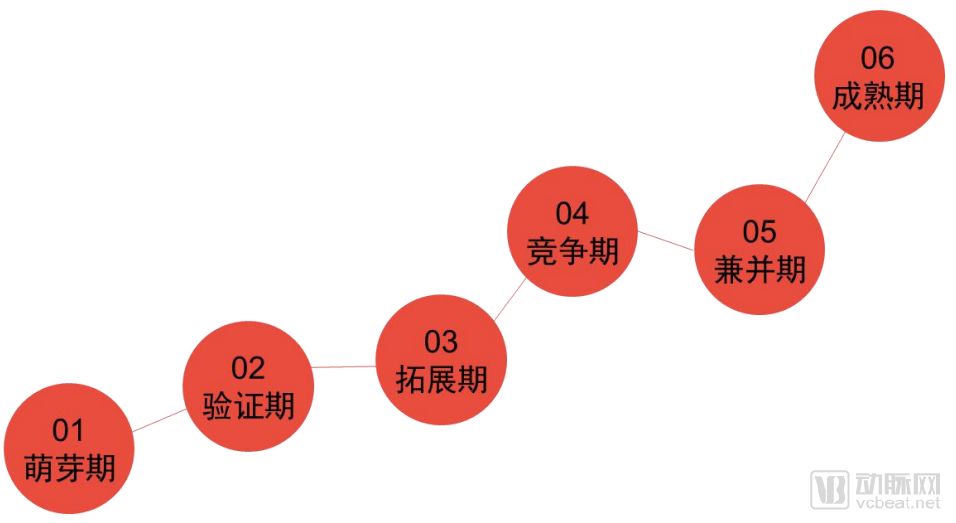

1. Inference 1: 6-stage evolution model of innovative enterprises

We divide the development of innovative companies into six stages: budding period, verification period, expansion period, competition period, merger period, and maturity period. Enterprises in different stages are faced with concept proposal, technology verification, and industrial cooperation. The core tasks of confirmation, capital verification, revenue verification, and profit feedback.

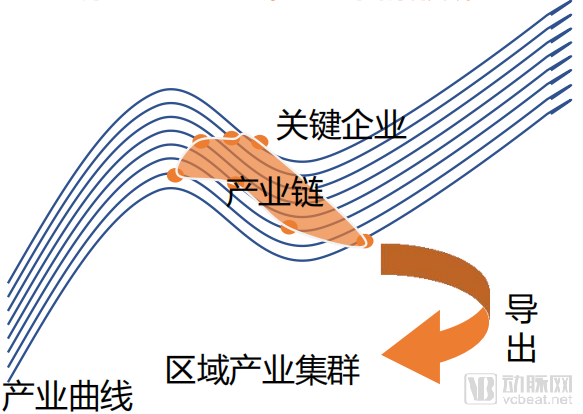

2, Corollary 2: Formation of regional industrial clusters

A large number of new enterprises are bound to be generated on the technology-driven industrial development curve. New business specificSpace carriers may be chosen consciously or unconsciously.

The industrial development driven by technology may resonate with the regional development of the carrier platform, thus creating the possibility for the birth of a future medical benchmark city.

Role relationship positioning

We re-sorted the roles and relative relationships of the seven major elements in the medical industry, and established our perspective on the medical industry. From this perspective, we build the following future medical industry tree.

Driven by the three major technology clusters, new requirements are efficiently aggregated and deeply integrated with the scene, and a new market is activated. Policy, as the only active element, is an important switch and valve of industrial evolution.

The nearly $ 400 billion in health funds invested in this area over the past six years is a driving factor. On this basis, the original industrial structure was re-explained by different logics, and the combination of production factors was broken and reorganized.

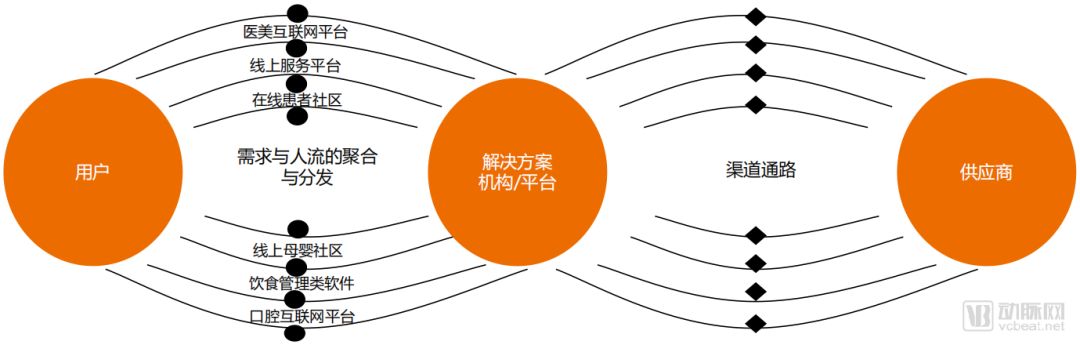

1. Coupling of requirements and solutions

In the industrial system we build, demand-solution-vendor positioning is regarded as three key nodes, which are connected by traffic channels and market channels. Next, we will analyze their changes.

2. The game between payment, data, and medical solutions

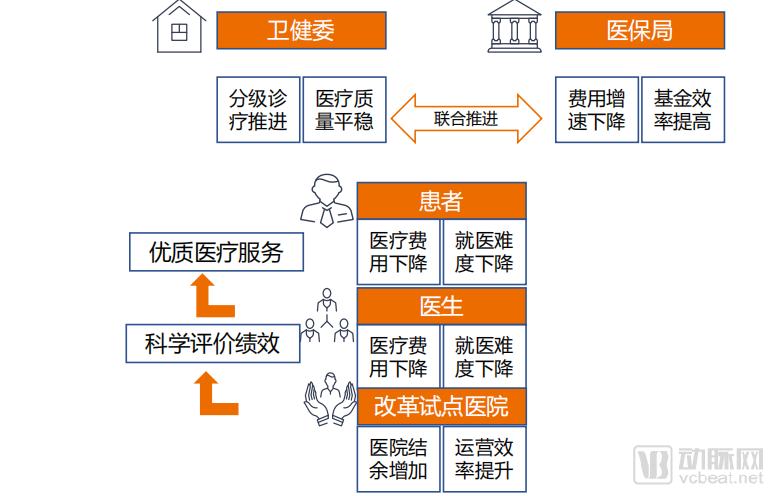

Medical payment reform has always been the primary task of medical reform. However, from pay-by-item and total prepayment system to pay per disease, various models are dazzling, and the burden of medical insurance continues to increase.

At present, data is complex, illogical, and non-standard.point. The health insurance bureau conducts performance games on behalf of all medical demanders and medical solution providers.

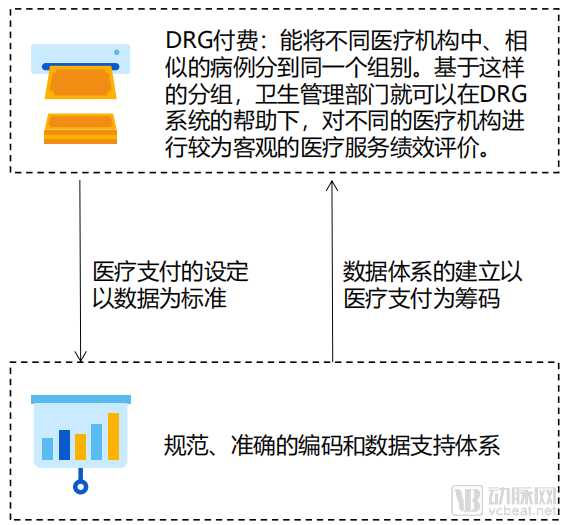

With the launch of the comprehensive advancement of DRG payment policies, big data-driven hospitals ’lean operation upgrades will surely become an important strategic direction for hospital development, as well as the basic guarantee for value medical upgrades.

The establishment of CDR and ODR data centers in hospitals will further promote the hospital’s entry into a new era of science-based clinical pathways that guide the decision-making based on the value of patient and disease services and cost management.

3. Voting rights for policies and capital

Policy is a flow valve that controls the process of the industry. It is the only active element that industry promoters can master.

Industrial policy is the sum of various policies in which the government intervenes in the formation and development of industries in order to achieve certain economic and social goals. The functions of industrial policies are mainly to make up for market defects and effectively allocate resources; to protect the growth of small national industries; to iron out economic shocks; to give full play to the advantages of latecomers and to enhance their ability to adapt.

In the operation of the market economy, industrial policy plays a guiding role. This guiding role is mainly: it can adjust the supply and demand structure of commodities to help achieve a balance between supply and demand of commodities in the market; it can adjust the capital market through credit tilt policies such as differential interest rates, which helps to rationalize the flow of funds and optimize the allocation; Regional blockades and market segmentation promote the development and formation of regional markets and domestic unified markets.

Industrial policies can regulate the economic structure, that is, regulate the industrial structure, industrial organization structure, and industrial area layout structure, so that social resources can be reasonably allocated among various industries, industries, enterprises, and regions, and gradually optimize the industrial structure; It can also regulate supply, that is, by promoting or restricting the development of certain industries, transforming the industrial structure, adjusting the interrelationships between industries, so that the total supply and structure can meet demand, and the total supply and demand, structure balance.

However, industrial policy has its own lag in its formulation. New industries come from innovation. Innovation is often unpredictable, so industrial policies are always formulated after innovation occurs.

At the same time, the formulation of industrial policies needs to be investigated, piloted, and promoted. The entire series of processes has a certain time lag. Therefore, industrial policies are often launched only after the industry has tried multiple paths, gained certain lessons, and has the corresponding undertaking capabilities.

In the development of industry, capital acts more as a catalyst, pushingThe subdivided fields with development potential have developed faster.

Usually we divide the field of health care into three major categories: medical services, medicine and medical devices.

In the investment of medical service enterprises, as a knowledge-intensive investment industry, medical personnel must be the top priority of their operations. How to attract, develop and retain talent, and how to formulate a talent incentive mechanism are the core of medical service investment.

In the investment of pharmaceutical companies, intellectual property rights and independent innovation are hot spots for capital.

In the investment of medical device companies, Capital pays more attention to the R & D capabilities of medical device companies. From a long-term perspective, in the future, its products can have core competitiveness globally.

In addition to independent research and development capabilities, capital has paid more attention to the company’s product capabilities, channel capabilities, and resource integration capabilities.

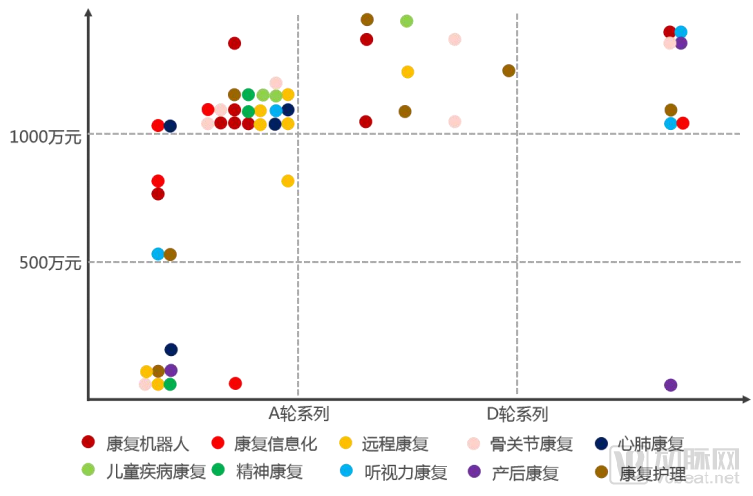

By analyzing the investment trajectory of capital, we have identified six major fields of rehabilitation robots, remote rehabilitation, rehabilitation informatization, bone and joint rehabilitation, rehabilitation care and cardiopulmonary rehabilitation as the golden track for the future of rehabilitation.

Change observation

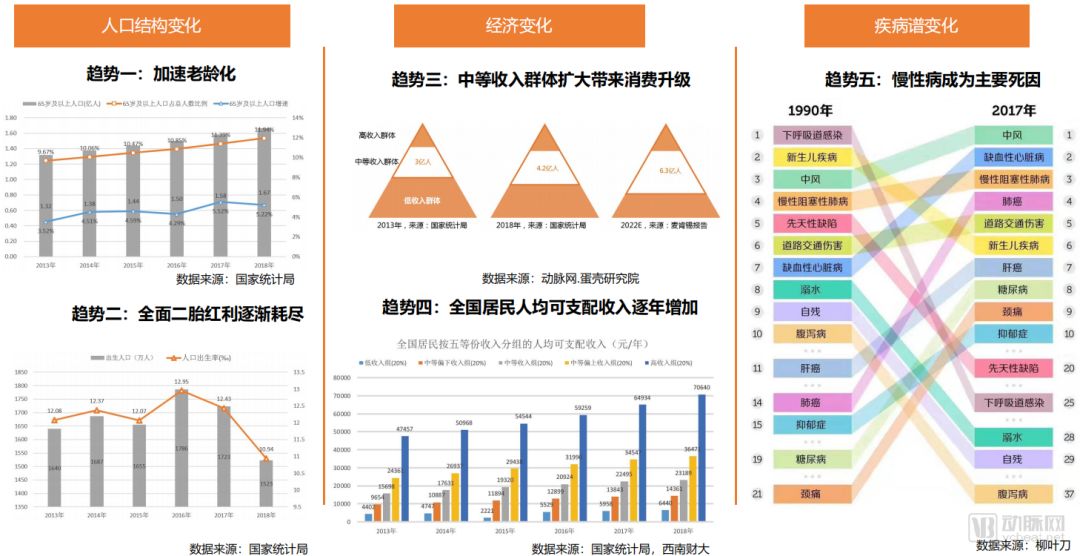

The source of changes in the medical industry lies in the rapid evolution of the economy, population, and disease spectrum. Changes in the economic situation directly affect people’s ability to pay; the evolution of the population and disease spectrum represents changes in the main patient population and medical needs.

Besides the origin, changes in technology, medical organization, and social ideology also affect the development of the medical industry.

From the perspective of technology evolution, the development of technology will cause changes in other factors related to technology, which will promote the consolidation of productivity.

When technology improvesTherefore, when the quality of labor force, labor tools and labor objects are improved, the productivity will rise to a higher level. Therefore, technology restricts the development of productivity. In the current era, the development of technology is the growth point of productivity.

In modern society, the invention of the steam engine has brought about changes in the transportation, textile, and smelting industries. Modern productivity has originated on the basis of the steam engine.

The development of medical technology has promoted the upgrading of generations of biomedicine and medical equipment, and has become the growth point of medical productivity.

Medical organization is an open subsystem in the entire social system, which is affected by the social environment. Therefore, the medical organization must adopt the corresponding organizational form according to the changes of the productivity and production relations in the social system to maintain the adaptability to the environment.

The activities of medical organizations are the process of moving towards organizational goals in the form of feedback under changing conditions. Therefore, it is necessary to act according to the current and long-term goals of the medical organization and the conditions at the time. The demand for medical services is endless. In addition to the need to cure diseases, patients also need to improve their health.

Therefore, the hospital organization must become an open system, maintain agility, stand on the patient’s perspective, and integrate the changes in productivity brought by technology into the needs of patients.

With the development of technology, innovation of productivity, reorganization and adjustment of medical organizations, patient-centered medical awareness has begun to take shape. Patient-centered medical awareness is an important part of high-quality medical care.

The core is to recognize patients and their families as important members and protagonists of the treatment team according to different environments, cultures, and medical systems, and integrate patient values, personal preferences and special needs into their treatment plans.

The impact of the technology wave, the era of a new universal technology is coming

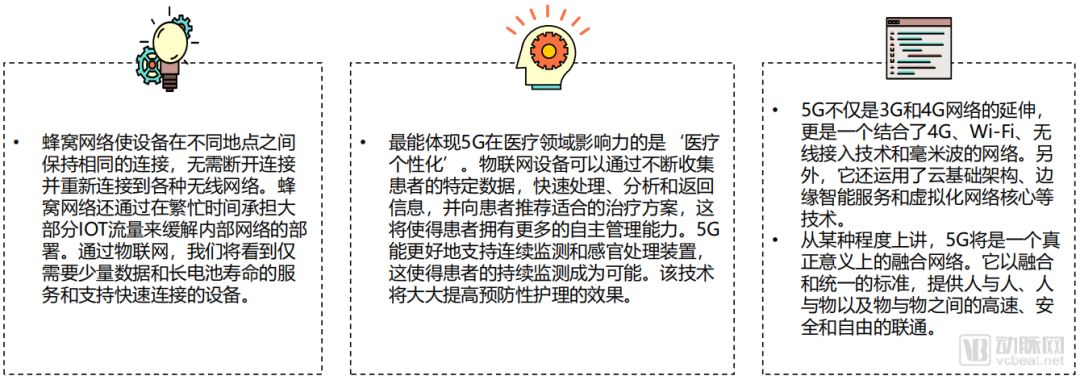

The emergence of digital technology, biotechnology, intelligent manufacturing and new material technologies in the era has jointly shaped the long-term future of linkage. Relying on common technologies such as the Internet of Things, 5G, gene sequencing, and big data, it marks the uninterrupted perception and the intelligent era of seamless computing is coming.

Medical technology innovation has begun to emerge in the fields of prevention, testing, treatment, rehabilitation, such as HPV vaccine, cell therapy, artificial intelligence medical testing and robotics.

1. Digital technology becomes the underlying foundation for disease treatment

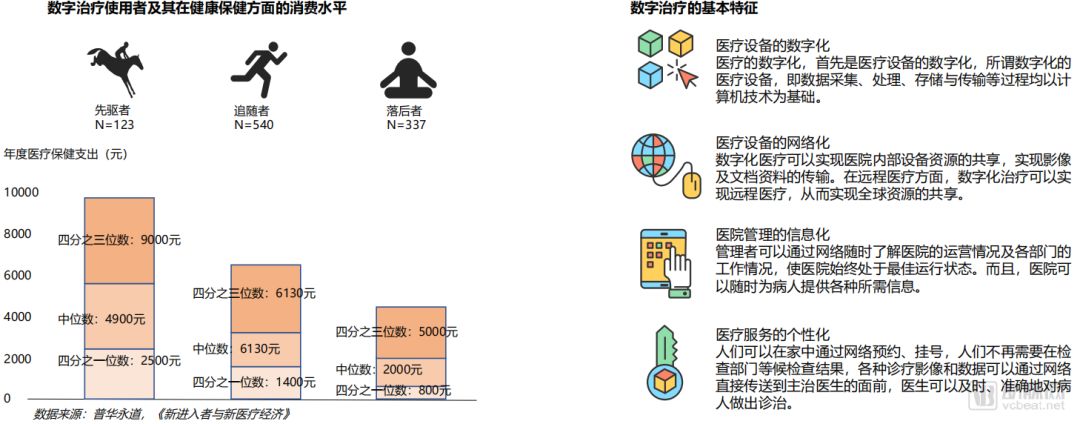

Digital therapy is a new type of modern medical method that applies modern computer technology and information technology to the entire medical process. It is the development direction and management goal of public medical treatment. According to BCG’s forecast, the digital treatment market in China will usher in rapid development in the next 5 years, and it is expected that the value will reach 110 billion US dollars by 2020.

Digital therapy is more than a simple collection of digital medical equipment. It is a new modern medical method that applies contemporary computer technology and information technology to the entire medical process.

In digital treatment, patients can complete consultations with minimal procedures, doctors ’diagnostic accuracy is greatly improved, and patient medical records contain all current and historical patient health information, which can greatly facilitate doctors’ diagnosis and patient self-examination, It can truly realize the comprehensive data transfer of patients needed by remote conference clinics, and realize fast and effective services. Digital medicine also has a great advantage that it can realize the sharing of resources between medical equipment and medical experts.

For medical institutions, a database with comprehensive health information is more authoritative. The establishment of a health information system can greatly enhance competitiveness.

From the medical logic, disease treatment is a slow process that requires long-term tracking and behavioral intervention, involving the operation and transmission of a large amount of information. Digital treatment is a trend that is being promoted by technological advancement. Taking AI technology as an example, it is precisely because of the development of AI technology that the scope of digital therapy has expanded to AI-related fields.

No matter how the digital medicine develops in the future, it will be based on the existing technology. No matter how powerful the function of the hospital in the future, it will be implemented on a basic structure. This structure can be summarized simply as Each part-digital medical equipment, network of digital equipment, digital medical system on the network and services based on digital medical system.

The wave of digital treatment will bring ecological and interactive changes to the medical treatment process, causing changes in three major trends: “Service as a Product” medical solutions, the cloud becoming the core platform for cross-industry cooperation, and large technology companies will gain high Benefit.

2, 5G + IoT will promote real-time sportsSignificant development of surveillance monitoring

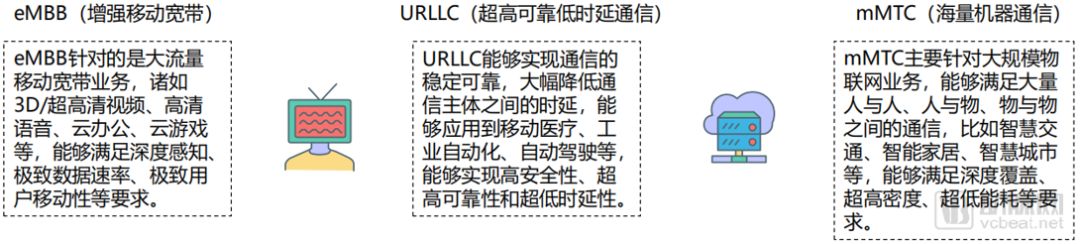

5G integrates a series of advanced communication technologies such as millimeter wave, micro base station, network slicing, and beamforming. Industry applications provide mobile network support to promote the entire socio-economic transition to digitalization.

5G can provide mobile communication support for high-definition video, the Internet of Things, VR / AR, robots, etc., and it will be widely used in smart transportation, mobile medical, cloud gaming, smart home, industrial automation and other industries. The amount of data it generates It will show exponential growth, and the peak user rate can reach 10Gbps, which will be a big era of data explosion.

The reason why 5G can provide communication guarantee for technical applications in various industries is due to the support of a series of key technologies behind it. For example, the high-frequency millimeter wave has a high bandwidth and a large amount of transmitted information.

Network slicing can set up multiple independent or shared communication networks according to the requirements of different application scenarios. There is also end-to-end technology, which can directly implement data transmission between devices without using a third-party base station, thereby reducing latency.

Therefore, no matter from the new features of 5G or the key technologies on which it is based, the performance indicators it exhibits are unmatched by previous generations of mobile communication systems. Then, what kind of architecture does 5G realize its application value?

Cellular, Wi-Fi, and Bluetooth enable the Internet of Things to work across platforms, and 5G is the link that connects these things. IoT devices have different functions and data requirements, and 5G networks can fully support them.

The difference between 5G and its predecessors is connected devices, fast intelligent networks, back-end services, and extremely low latency. These qualities make a fully connected world possible.

By 2020, the 5G network will support more than 20 billion connected devices, 21.2 billion connected sensors, and be able to access 44 megabytes of data collected from various devices, from smartphones to remote monitoring devices. This ecosystem will make real senseBig data in meaning is possible.

In the medical and health field, not all scenarios require 5G, and 5G is not perfect enough to support all application scenarios. Based on previous surveys and related literature, we found that only those medical scenarios involving large amounts of data transmission, requiring high-definition video, and short information transmission delays, can 5G fully take advantage of its advantages.

Wireless monitoring refers to real-time, continuous monitoring of patients’ blood pressure, blood glucose, heart rate, etc. through vital sign monitors or wearable smart devices, and transmits these sign data to medical staff through wireless communication.

Wireless monitoring needs to continuously, real-time and dynamically reflect the vital signs of the monitored person. It can transmit the analyzed and processed data to the display terminal of the medical staff in order to control the situation in real time. Especially for patients with sudden illness, the alarm time of wireless monitoring directly affects the corresponding rescue time of patients.

In addition to monitoring equipment and patient vital signs, it can also control some equipment. For example, in wireless infusion monitoring, a 5G network-based wireless infusion management system can monitor the patient’s infusion progress in real time through an IoT device such as an infusion monitor. At the end, the nurse can be alerted quickly, and the nurse can come to deal with it as soon as possible to avoid medical accidents.

The large-scale Internet of Things involves the Medical Internet of Things (IoMT) ecosystem, which will contain millions or even billions of low-energy, low-bit-rate medical health monitoring devices, clinical wearable devices, and remote sensors.

Doctors rely on these instruments to continuously collect patient medical data, such as vital signs and physical activity. This data will be received by healthcare providers in real time and will allow them to effectively manage or adjust treatment plans.

In addition, these data support predictive analysis, allowing doctors to detect the health pattern of the measured person more quickly, thereby improving the accuracy of the diagnosis.

Technical upgrading of the medical industry provides telecommunications operators with a lot of opportunities to help them penetrate the new value chain, which is beneficial to the cooperation of the entire IoT ecosystem. It is estimated that in 2026, operators with a turnover of 76 billion U.S. dollars will transition to 5G healthcare.

In order to successfully transform, cooperation between different players in the industry chain will be crucial. Ericsson’s ConsumerLab report “Medical to Home Care” states that 86% of cross-industry decision makers believe that in addition to being a network provider, operators can also provide system integration and application and service development.

In order to change the way patient applications are processed, patient data needs to be stored centrally. Eventually, the hospital will be transformed into a data center, and doctors will be transformed into medical data experts at the same time. This allows patients to access medical databases online, helping them easily manage the quality and efficiency of care.

45% of cross-industry experts believe that this will be a revolutionary breakthrough in medical services; and 47% of telecommunications decision-makers believe that secure access will be a key challenge.

An expert said: “With these monitoring technologies, 5G will undoubtedly provide doctors with the ability to keep in touch with patients, whether outside the ambulance or at the patient’s home.”

At present, 5G technology is not yet mature. But by 2019, the first suppliers plan to maximize this technology.

IHS market reports show that by 2035, 5G technology sales will reach 1.1 trillion U.S. dollars, accounting for more than 9% of the global 5G economy, or 12.3 trillion U.S. dollars.

This impact is roughly equivalent to expanding India’s economy to the current global economy. In addition, the value chain related to 5G will reach an output value of 3.5 trillion US dollars, and 22 million new jobs will be created worldwide.

Achieving this goal will be achieved by more than just leveraging technology. The industry has begun to shift to a results-based model, and government policy changes will help speed up the process: stimulating suppliers through taxes and policies, for example. Policies need to provide protection for innovation and intellectual property to ensure that 5G developers can be compensated accordingly.

3. Gene testing, cell therapy, and immunotherapy will open a new ecology of precision medicine

CAR-T therapy is not a new word. Since the approval of two CAR-T products from Novartis and Kite in 2017, the global enthusiasm for cellular immunotherapy has rapidly increased. The field is No. 1 in the field, and immunotherapy is also regarded as the fourth anti-cancer method after radiotherapy, surgery and targeted therapy.

According to the “Nature Reviews Drug Discovery” report, as of March this year, there were 1011 cellular immunotherapies approved or under development worldwide, an increase of 258 compared to the same period last year; CAR-T therapy exceeded Fifty percent, there are 568 models, an increase of 164 as compared to March 2018, reflecting the industry’s great enthusiasm for CAR-T therapy.

Among them, the United States and China have more than 400 and 300 cellular immunotherapy products approved and under investigation, respectively, accounting for about three-quarters of the total.

In addition to the enthusiasm of the industry, the medical insurance systems of various countries have also shown acceptance and recognition of CAR-T therapy. After the UK and the United States included it in medical insurance, in May this year, Japan also announced that it would be included in medical insurance.

On October 30, Novartis’ Kymriah, the world’s first CAR-T therapy, also obtained an implied license for clinical trials in China. These developments mean that not only the demand for it in the European and American markets will continue to increase, but China may also introduce the drug for clinical use in the future.

According to Coherent Market Insights forecast, during 2018-2028, the global CAR-T cell therapy market value will grow at an average compound annual growth rate of up to 46.1%.

For some time to come, North America will still occupy more than 50% of the global CAR-T cell therapy market share, and the European market will take second place.

But with the advancement of China ’s CAR-T related policies and the strengthening of R & D, more and more companies are pouring into the CAR-T industry market. China is expected to overtake the curve in a short period of time in the future, occupying a large part of the world market share.

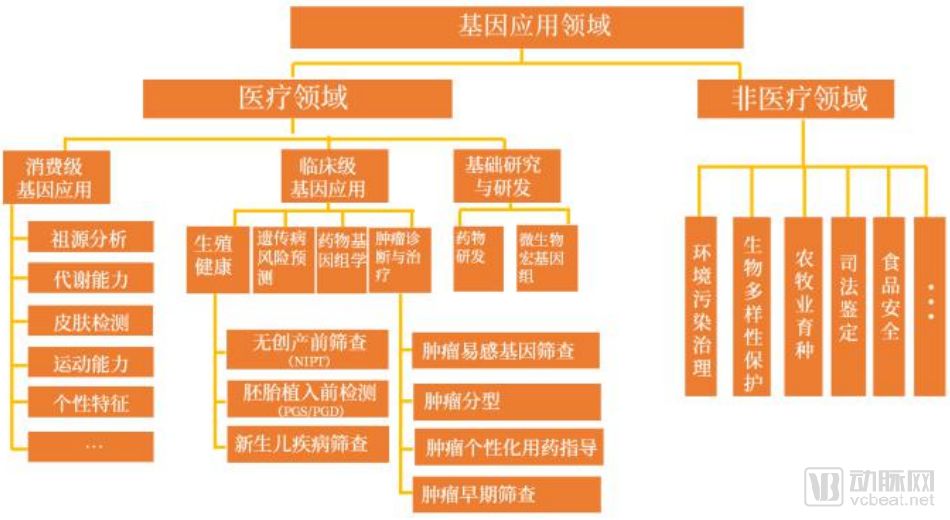

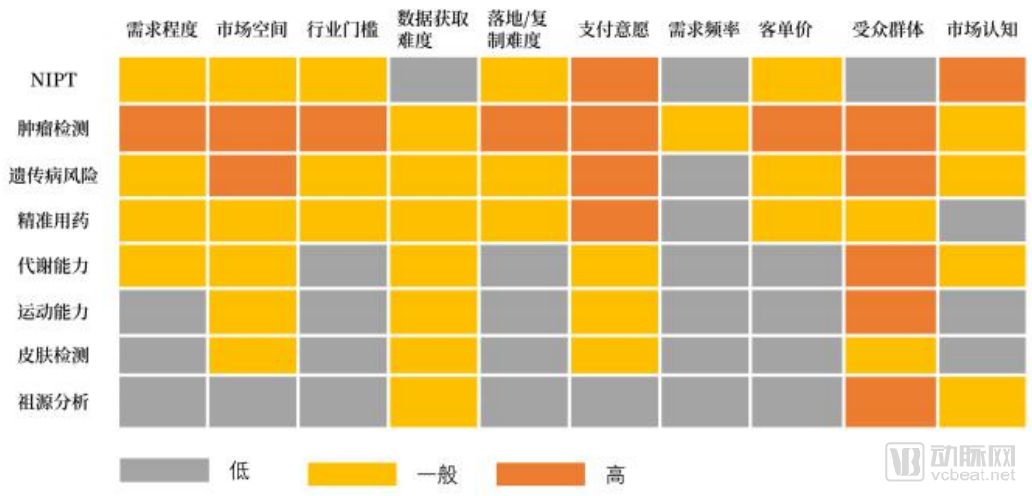

The application of genetic testing is mainly concentrated in the medical field, and the most commercialized field will have the best development momentum in the future. With the development of gene sequencing technology, people have the opportunity to see their origins. Gene interpretation and gene editing technologies have made everyone see the dawn of active management of health.

At present, genetic technology is mainly used in the medical and non-medical fields. We have designed a series of evaluation indicators for genetic technology in the medical field, carried out commercial evaluation, and selected several areas with the best development momentum in the future.

According to the current research direction of genetic testing, the application of genetic testing can generally be divided into medical and non-medical fields. The medical field mainly includes consumer-level genetic applications, clinical-level genetic applications, and basic research and development.

According to the index system of the Arterial Network. Eggshell Research Institute, we can evaluate the application of genes. The application of high probability tumor detection, genetic disease risk prediction, accurate medication, and metabolic capacity will become the best development momentum in the future field.

Reform of industrial organization system

1. Third-party medical institutions enter the growth stage

Third-party medical service organizations, also known as “independent medical service organizations”, refer to organizations established outside the traditional hospital system and focused on providing a certain diagnostic, test, or specialty medical service.

In October 2013, the government issuedSeveral Opinions on Promoting the Development of the Health Service Industry, vigorously develop third-party services, and guide the development of professional medical test centers and imaging centers.

On February 21, 2017, the National Health and Family Planning Commission added five categories of medical institutions: “Medical Testing Laboratory, Pathological Diagnosis Center, Medical Imaging Diagnosis Center, Hemodialysis Center, Anning Care Center”.

In August 2017, the National Health and Family Planning Commission added five categories of independent medical institutions, including: rehabilitation medical centers, nursing centers, disinfection supply centers, small and medium-sized eye hospitals, and health check-up centers.

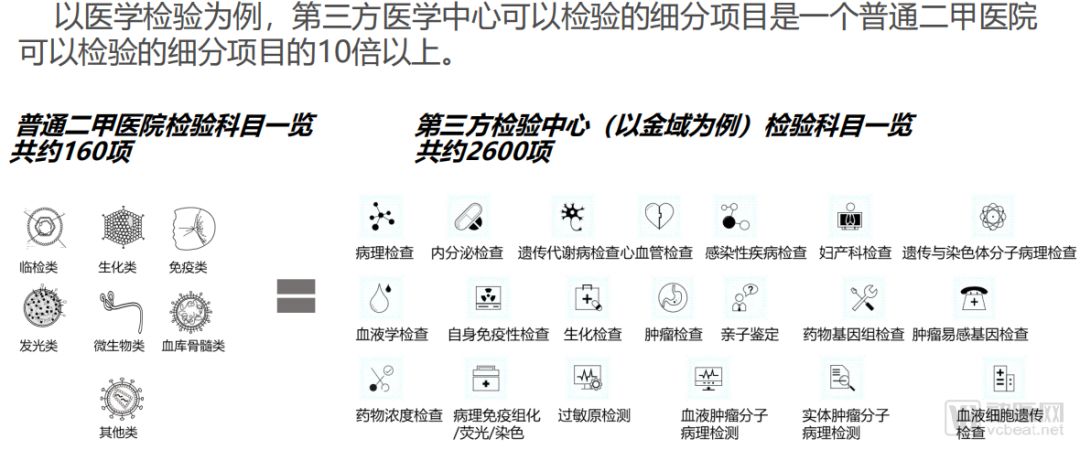

According to the data of the 2018 China Health and Family Planning Statistical Yearbook, there are currently more than 29,000 hospitals across the country and the number of medical and health institutions is close to 1 million. If basic-level medical and health institutions are required to set up inspection, imaging, and pathology departments, there will be a large gap in practitioners. Centralized setting up of third-party medical institutions and opening up to primary-level medical institutions. While ensuring quality, it is conducive to concentrating limited medical resources and achieving regional resource sharing.

At the same time, the development of medical device technology has made some medical behaviors a standardized process and provided feasible support for out-of-hospital development. Some high-end technologies do not carry much business in a hospital and are not cost-effective. If a third party can provide services independently and use contractual management, it will help quality control and ensure medical quality and safety.

Thus, under the guidance of the tiered diagnosis and treatment policy, the status of third-party medical institutions is recognized to achieve greater regional resource sharing.

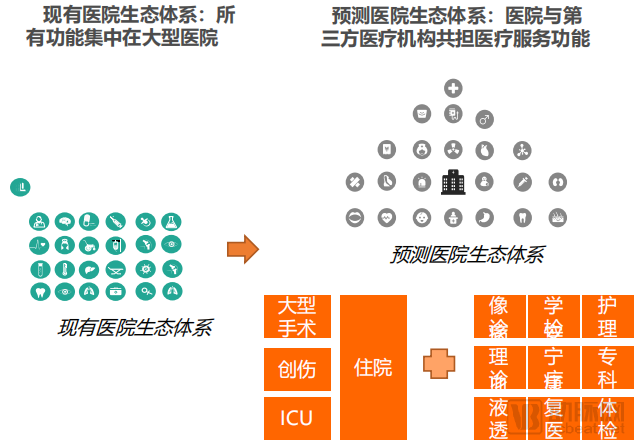

Under the development trend of third-party medical institutions, we predict that in the future, hospitals will shift their functions, forming an ecosystem in which hospitals and third-party medical institutions share medical service functions.

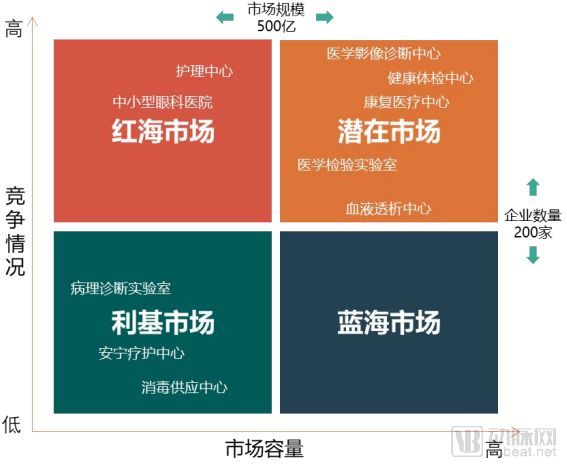

According to the knowledge accumulation of the industry network and eggshell research institute, we will divide the third-party medical service institutions according to the market capacity (the market size is 50 billion yuan as a watershed) and the competition situation (the number of related companies is 200 (Watershed) is roughly divided into four different markets: As the market structure and business model gradually become clear, the entry of potential markets and niche markets into the growth stage.

Third-party medical service organizations are essentially in the category of asset-heavy service industry. It is characterized by being difficult to grow, but once it has developed on a large scale, its “Matthew Effect” will become more obvious and the potential returns will be huge.

A key competitive element of the third-party medical service industry is the ability to finance, because third-party medical service organizations can only continue to grow and form the possibility of chain and group development only if they continue to receive capital support; the second is operation Capabilities, because third-party medical service organizations involve various aspects and requirements of different functions. Only by fully coordinating and integrating various resources can operators ensure that the company has been in a steady state of growth.

Of the two elements, we believe that the management team’s operational ability is the key to obtaining capital support, so the latter is more important.

Industry standards and operating specifications have been issued. Relatively free health checkups, ophthalmology, and other industries have killed the red eye, and imaging centers and pathology centers that serve the clinic have an important observation point in the process: the state has these stocks The direction of resource redistribution.

For example, the update cycle of imaging department equipment is 10-15 years, and now it is very close to the next wave of equipment update cycle. We only need to observe the state’s support for imaging equipment in secondary and primary hospitals.

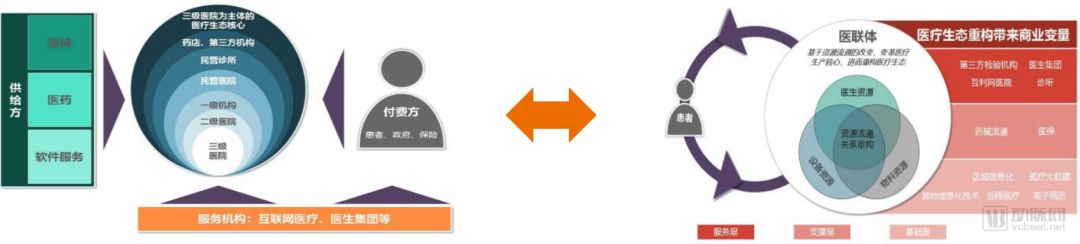

2. Deconstruction and integration of medical institutions

Traditional medical institutions are geographically divided. The medical consortium is based on advanced information technology and redefines the boundaries of traditional medical institutions. The medical union has built multiple medical institutions in a certain area into functional departments within the medical union through functional division and division of labor according to its own capabilities and advantages.

Medical Federation has become a larger medical institution, its geographical influence has weakened, and the boundaries of traditional medical institutions have been redefined.

The major changes in medical institutions themselves, especially in their internal relations, will inevitably affect the suppliers, payers, and service organizations of all parties around the institution.

Formally, the medical association policy is the most important business relationship of medical institutions.New definition; from a commercial perspective, the reform of medical institutions and medical associations will inevitably cause the collapse of the traditional medical chain. For market participants, there are a lot of changes and risks hidden behind them, as well as a lot of business opportunities.

The medical ecosystem core is changing the internal link of the medical ecosystem through the medical consortium, which in turn affects the interrelationships between external payers, suppliers, service agencies and the core of the medical ecosystem, resulting in the reconstruction of the value distribution system and a new Business opportunity.

3. Digitalization helps the medical industry enter the era of data management

“Smart hospital” is a concept derived based on technology and results. It is not a single technology accumulation, nor is it synonymous with a certain function. Smart hospital is a hospital with characteristics of information, intelligence and internet.

Informatization means that the hospital has established data systems of different dimensions and integrated systems of data in each dimension; intelligent means that the hospital uses big data, cloud computing, Internet of Things technology, automation equipment, robots, and intelligent workflow And operation management system; the Internet means that the hospital has launched mobile applications to provide medical staff and patients with data input and output before, during and after the consultation.

Smart hospitals can achieve interconnection between patients, medical staff, medical institutions, and medical equipment, improve the level of hospital operations, and optimize the experience of medical services before, during, and after consultation.

In August 2014, the National Development and Reform Commission, together with eight ministries and commissions including the Ministry of Industry and Information Technology, issued the “Guiding Opinions on Promoting the Healthy Development of Smart Cities,” and proposed the construction of smart hospitals and telemedicine. This is the first time that the construction of a “smart hospital” has been proposed. Since then, the central and local governments have issued a series of policies to push the construction of a “smart hospital” to a climax.

From the top-level design to local policies, from technical guidance to evaluation indicators, the release of a series of policies has promoted new technologies such as artificial intelligence, information technology, Internet of Things technology, big data and cloud computing to empower hospitals and promoted Smart hospitals with higher efficiency and better service have been set up.

It is expected that in the near future, clear smart hospital definitions and specific smart hospital construction support policies will be released one after another.

The medical treatment process has shaped the patient’s all-round experience in the hospital. For a long time, the hospital has queued up, registered, waited for, paid, checked, re-visited, re-paid, treated, taken medicine, left the hospital, etc. The cumbersome process of making the service Inefficiency leads to decreased patient satisfaction.

At present, many hospitals are reforming their medical procedures, taking outpatients as an example.

The outpatient clinic is a window for hospital services. The outpatient clinic uses information technology as a platform to make appointments. It seeks doctors by time, arranges the patient consultation process rationally, and reduces waiting time. It can improve the optimization of patient treatment, simplify the service link, and reduce the invalidity of patients in the hospital Mobility and waiting times improve the quality of services and make it easier for patients to see a doctor.

The construction of smart hospitals in the future will face ten major needs:

-

Improving the quality of medical care and avoiding medical errors requires effective data and necessary human support.

-

Medical safety, such as quantifying the effects of medicines through the Internet of Things technology and intelligent technology, and continuously monitoring patient signs.

-

Reducing the labor intensity of doctors, improving the efficiency of doctors, automating standardized and standardized operations, and improving the work efficiency of medical staff.

-

Improve the experience of patients and doctors, build patient service platforms, optimize doctors’ work platforms and other Internet application systems.

-

Optimize processes and simplify tedious business processes through mobile.

-

Improve the utilization rate of resources, realize intelligent utilization of hospital resources through IoT technology, intelligent technology, and interconnected technology, and improve the effective utilization of expert resources, equipment resources, and ward resources.

-

Reduction of medical costs, including the establishment of corresponding systems to optimize hospital management, and to achieve cost control.

-

Improve the level of scientific decision-making and support this demand through artificial intelligence systems.

-

Improve the level of scientific and technological research, and use big data technology to assist hospital research.

-

Improving the level of medical collaboration, different specialties in the hospital achieve synergy, medical collaboration between hospitals, and the interconnection and interconnection of various systems.

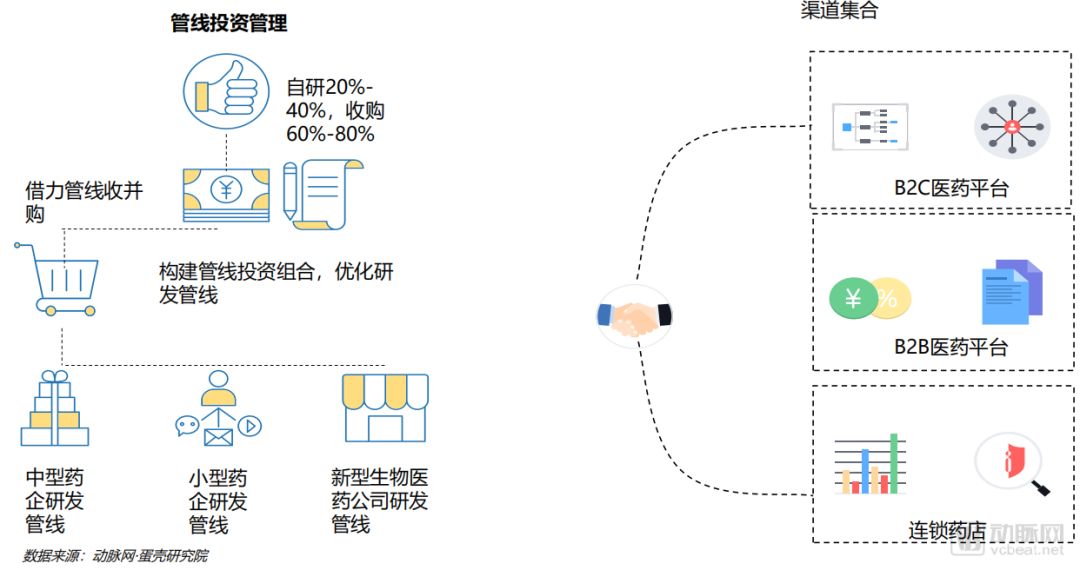

4. The value of large pharmaceutical companies is shifting to pipeline investment management and channel integration and integrated solutions.

Among the 59 new drugs approved in the United States in 2018, less than half of the drugs submitted by large pharmaceutical companies. Moreover, 64% of the approved drugs were originally developed by emerging biopharma (EBP) companies.

Emerging biopharmaceutical companies have achieved annual global sales of less than US $ 500 million and R & D investment of less than US $ 200 million in the last year. These EBP companies have not only initiated most of the R & D activities of approved new drugs, but also can push 66% of the products under development to the stage of submitting new drug applications.

This means that these EBP companies have not only made important contributions to launching innovative research and development, but also have the willingness and ability to drive product development to submit new drug applications.

The value chain of pharmaceutical companies is migrating. From the perspective of ecosystem construction, change their business models from the perspective of processes, services, and stakeholders, and provide patients with digital integrated solutions based on products.

From the data of pipelines of drug research and development in the late stage of clinical research, the late-stage R & D projects carried out by new-type biomedical companies accounted for 72% of all late-stage R & D projects in 2018, while large-scale pharmaceutical companies accounted for only 20%, and large-scale pharmaceutical companies Relying on pipeline investment methods such as mergers and acquisitions to strengthen research and development pipelines.

Strengthening the R & D pipeline, investing in blockbuster drugs that are under research or coming to market, and achieving complementary product portfolios and synergistic scale effects have become the basic logic of pipeline management for many large pharmaceutical companies.

With the gradual implementation of the “4 + 7” taped procurement policy, the pharmaceutical procurement model has changed. In addition to striving to win the bid for the in-hospital market, pharmaceutical companies are also taking advantage of the trend to develop new marketing channels with the help of pharmaceutical e-commerce platforms. , Entered the market outside the hospital.