In the face of the epidemic, Starbucks temporarily closed more than half of its stores in mainland China.

Editor’s note: This article is from WeChat public account “Deep Sound” (ID: deep-echo ) , Author rubber hero Golzan.

Although Starbucks is still unstoppable globally, its difficulties in the Chinese market may become the first stop of its coffee empire in distress.

On January 28, US time, Starbucks (NASDAQ: SBUX) announced its fourth quarter performance report as of December 29, 2019.

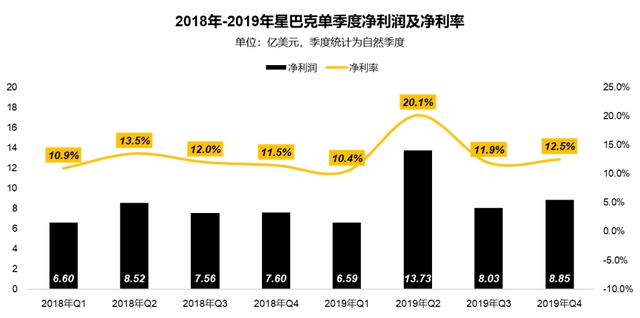

Starbucks achieved revenue of US $ 7,097 million in the quarter, an increase of 7% year-on-year; realized a net profit of US $ 885 million, and a net profit rate of 12.5%.

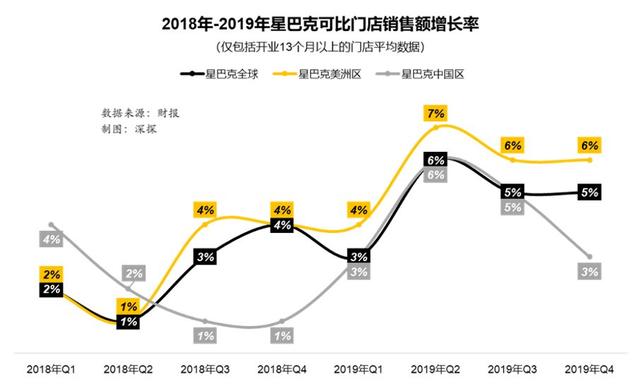

On the whole, Starbucks’ global comparable store sales growth rate maintained 5%, and in the fourth quarter, it opened 539 new stores worldwide. As of the end of 2019, Starbucks has 31,795 stores worldwide.

However, the improvement in Starbucks’ global performance has come mainly from North America. In its once-proud Chinese market, Starbucks is facing fierce competition, limited expansion, and same-store sales. In addition, the coronavirus epidemic has increased uncertainty about future performance.

In response to the new coronavirus-infected pneumonia epidemic, Starbucks temporarily closed more than half of its stores nationwide, adjusted the opening hours of some of its stores, and strengthened epidemic protection at its stores.

Proportion of global direct sales increased, business downsizing

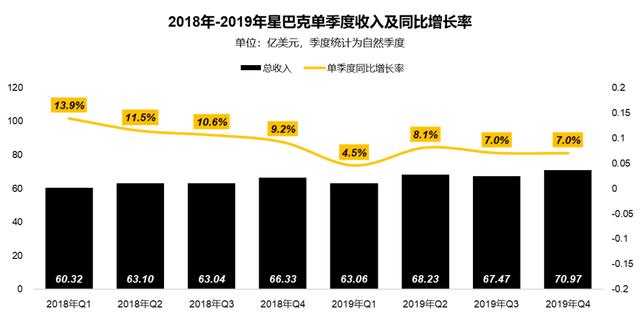

In the fourth quarter of 2019, Starbucks achieved US $ 7,097 million in revenue, an increase of 7% compared to the same period in 2018. Since the second quarter of 19, Starbucks’ revenue growth rate has basically stabilized at more than 7%, but its growth rate has slowed by half compared to the beginning of 2018.

Source: company’s financial report; collation: in-depth exploration

From the perspective of segmented revenue, the proportion of Starbucks’ self-operated revenue is constantly increasing. This quarter, direct-operated store revenue accounted for 81.5% of total revenue; other revenues continued to decline, and this quarter has fallen to 7.4%. .

The change in revenue composition is highly relevant to Starbucks’ global development strategy. On the one hand, in order to strengthen the company’s control over services and products, Starbucks has gradually taken back ownership of franchise stores worldwide. Since 2017Starting in the fourth quarter, Starbucks has fully recovered the operating rights of all stores in China.

On the other hand, in order to focus more on the chain cafe business, Starbucks has gradually divested its non-core business (coffee bar). In May 2018, Starbucks sold retail and dining rights outside the coffee shop to Nestlé for $ 7.15 billion, and also stopped supplying newspapers in September 2019.

Source: company’s financial report; collation: in-depth exploration

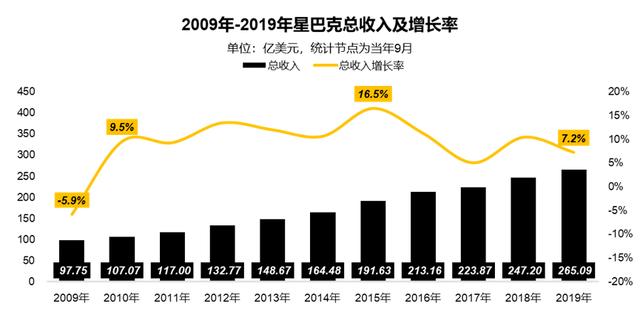

Starbucks’ revenue growth has changed from negative to positive in 2010, and has maintained an annual growth rate of more than 10% for many years, reaching a maximum of 16.5%. With the continuous expansion of business scale, the company’s current revenue growth has entered a relatively stable stage. The company’s operating income for the full year of 2019 was US $ 26.509 billion, a year-on-year increase of 7.2%.

Source: company’s financial report; collation: in-depth exploration

Focusing on core business while gaining revenue, the company’s profits have also steadily increased. This quarter, Starbucks achieved a net profit of $ 885 million and a net profit rate of 12.5%, showing a stable trend in the past two years.

Source: company’s financial report; collation: in-depth exploration

Limited expansion in China, same-store sales decline

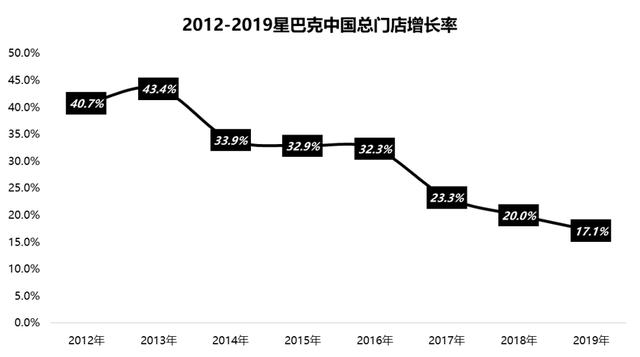

Since Starbucks opened its first mainland store in Beijing in January 1999, it has undergone three major development stages: tortuous development, rapid expansion, and full-scale expansion, which have witnessed the budding and emergence of the Chinese coffee market. As of the end of 2019, Starbucks has 4,292 stores in China, second only to 15,188 in the United States.Second largest market.

But Starbucks ’expansion in China has slowed in recent years. From 2012 to 2019, the growth rate of Starbucks stores in China has fallen from 40% to 17%.

Source: company’s financial report; collation: in-depth exploration

Because Starbucks cuts into the high-end market in China, it has high coverage and influence in first- and second-tier cities, and most of its locations are near large commercial centers or office buildings. Looking at the distribution of Starbucks stores in various provinces and cities in China, about 66% of stores nationwide are concentrated in Beijing, Shanghai, Guangdong, Zhejiang, and Jiangsu.

As far as the current distribution situation is concerned, Starbucks has basically covered the core areas of first- and second-tier cities, and this is also a “high-end constraint” that restricts Starbucks’ expansion and development.

Source: Zhongtai Securities; finishing: deep exploration

In addition to limited expansion, Starbucks also faces a decline in same-store growth in China. As the core indicator of physical retail, same-store sales (also known as comparable store sales) generally refers to the average annual sales that can be increased in each stable store, showing the chain’s operating and innovation capabilities. And retention rates.

This quarter, same-store sales growth in China was only 3%, while global and North American stores maintained growth of 5% and 6% year-on-year, which also reflects that Starbucks ’growth rate in the Chinese market is lower than global As well as North American levels.

Source: company’s financial report; collation: in-depth exploration

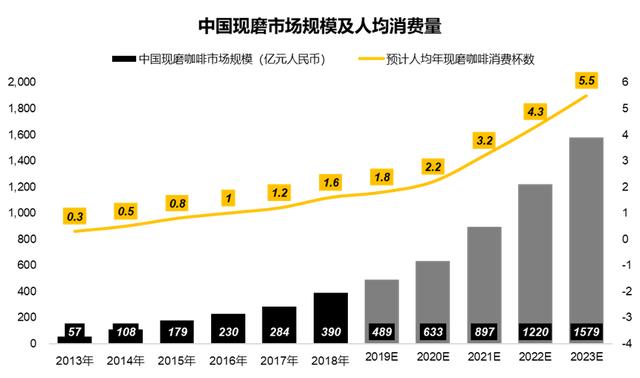

However, corresponding to the slowdown of Starbucks’ expansion in China and the weak growth of store revenue, the Chinese coffee market still has proven potentialfoot.

According to Euromonitor data, per capita coffee consumption in mainland China in 2018 was 4.7 cups, while Taiwan was 4.9 times that of mainland China, Hong Kong was 31.6 times that of mainland China, and the United States was 55.6 times that of mainland China. Among them, the penetration rate of freshly ground coffee in mainland China is even lower, which was only 1.6 cups per capita in 2018.

According to Frost & Sullivan data, China’s fresh ground coffee market reached 39 billion yuan in 2018, and it is expected to reach 157.9 billion yuan in 2023. Even more gratifying is that even if the market has reached 150 billion yuan, the penetration rate of freshly ground coffee is only 5.5 cups per capita, which is still far lower than that of European and American countries.

According to the revenue of Starbucks and Ruixing, the two leading coffee chains in China in 2019, the two companies account for more than 50% of the total market revenue. Ruixing, as an emerging coffee chain brand, quickly occupied the market through agile and aggressive strategies, which also confirmed the huge potential of the Chinese coffee market from the side.

Source: Frost & Sullivan; Finishing: Deep Dive

Ruixing vs Starbucks: Cheetah is better than elephant, who is better?

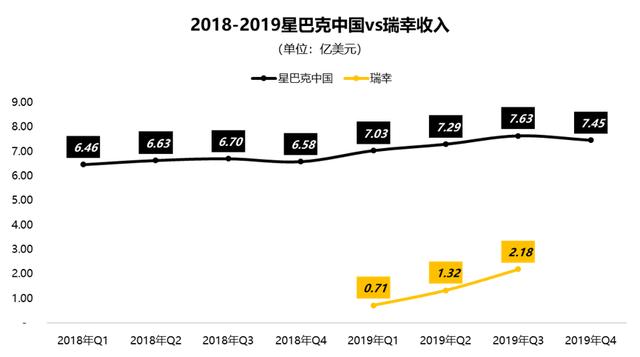

In 2019, the revenues of Ruixing and Starbucks have exceeded 50% of the total revenue of the ground coffee market in mainland China, and this is just over two years from the establishment of Ruixing.

With strong capital support and efficient operating capabilities, Ruixing has quickly opened up in the Chinese market. Its domestic stores have surpassed Starbucks China by the end of 2019, becoming the most popular coffee brand in China.

According to the data of Ruixing’s official website, as of the end of 2019, the total number of Ruixing’s stores has reached 4,507; and the fourth quarter financial report shows that Starbucks has 4292 stores in China, and Ruixing has successfully overtaken.

Source: Starbucks, Ruixing’s financial report, Ruixing’s official website; Reorganization: Deep dive into Research

In terms of revenue, Starbucks China’s revenue for the quarter was US $ 745 million, and Ruixing’s fourth quarter revenue will likely be close to US $ 300 million. Starbucks China still has obvious advantages in terms of revenue scale, and this is mainly reflected in the customer unit price, the stickiness of core consumer users, and loyalty.

Source: Financial reports of Starbucks and Ruixing; finishing: deep exploration

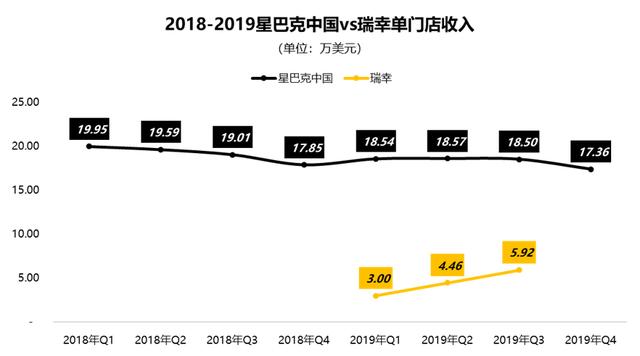

From the perspective of store revenue, Starbucks China’s single store revenue is about three times that of Ruixing, and this is basically reflected in the difference in the average price of single products between Starbucks and Ruixing (after subsidy).

Source: Starbucks and Ruixing’s financial reports; Reorganization: Deep research

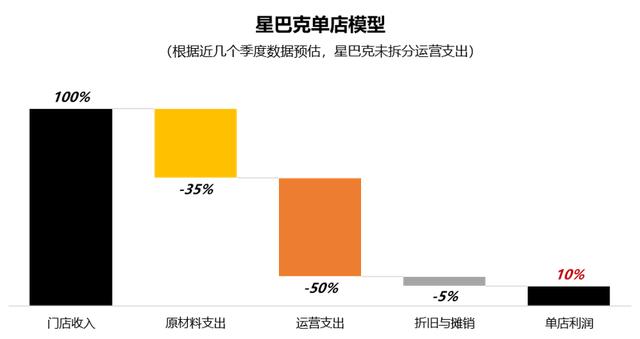

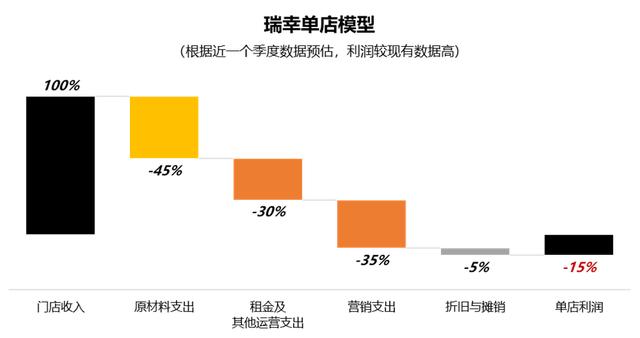

In the third quarter, Ruixing disclosed in its financial report that its overall store level has achieved profitability, and if Ruixing and Starbucks are restored to the same caliber, the two companies will still have significant differences.

It can be seen that Ruixing ’s overall store-level model disclosed does not include marketing expenses, which means that the daily consumption of coffee coupons and various advertisements is calculated at the headquarters level. Fortunately, the cost of the store only includes raw materials, rents, utilities, depreciation of fixed assets, and staff salaries.

In contrast, Starbucks does not include marketing expenses at the reporting level, but instead allocates marketing expenses to the store level as part of its operating expenses. Therefore, if Ruixing and Starbucks are compared at the single store level model, Ruixing’s promotion expenditure should also be decentralized to the store level.

It can be seen that under the current operating conditions, Starbucks can still maintain a 10% profit in a single store on the basis of including marketing expenses, while Ruixing has lost about 15% at the store level. The difference is mainly in the cost of raw materials and operating expenses (including promotion costs).

Source: Financial reports of Starbucks and Ruixing; finishing: deep exploration

Although Ruixing has continued to reduce expenditures and expense ratios through scale; it has reduced rents and improved bargaining power through brand influence, but its profitability is still far from Starbucks. In contrast, Starbucks supports its long-term profitability through its stable, strong supply chain, and its strong brand premium ability.