Ali’s revenue and profit continued to grow steadily this quarter. Affected by the epidemic, the next quarter will face a greater test.

On February 13, Alibaba Group (NYSE: BABA) announced the third quarter of fiscal 2020 before the US stock market.

According to the financial report, as of December 31, 2019, Alibaba’s revenue in the third quarter of fiscal 2020 reached 161.46 billion yuan, a year-on-year increase of 38%, which was higher than market expectations of 159.21 billion yuan. The net profit attributable to shareholders was 52.309 billion yuan, far higher than the market expectation of 30.335 billion yuan, and 33.052 billion yuan in the same period last year, a year-on-year increase of 58.4%.

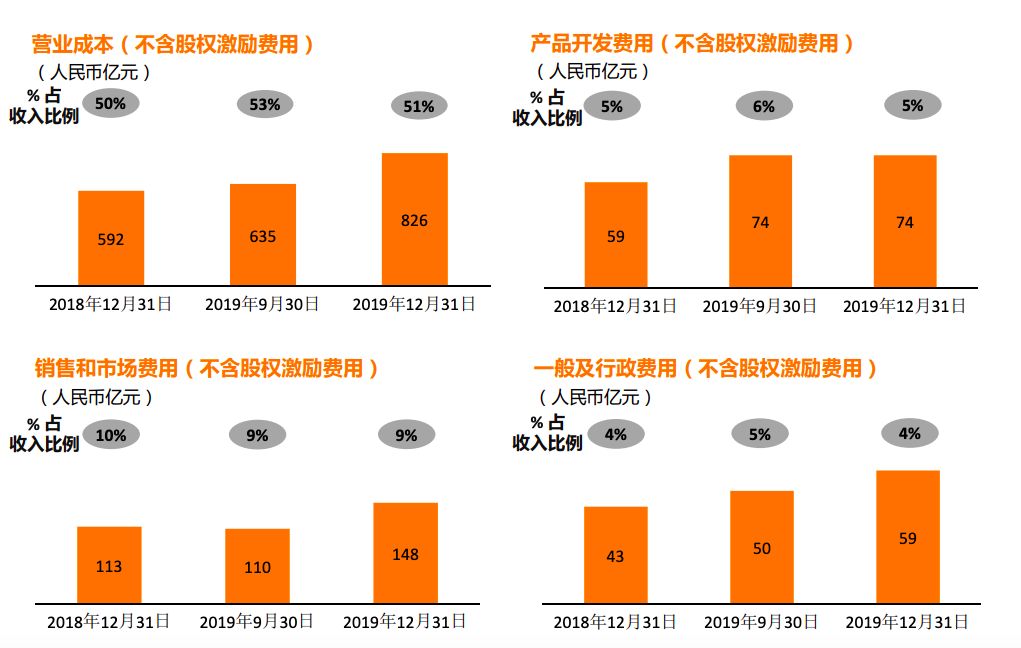

In the past eight quarters, Alibaba’s earnings per share have met or exceeded analyst expectations. The large increase in net profit YoY may be related to Ali’s contraction of expenses. It can be known from the financial report that Ali’s expense growth rate in this quarter was not obvious year-on-year. Under the situation of revenue growth and expense control well, net profit maintained a high growth.

Image source: Ali Financial Report

In addition, Ali This month, China ’s retail market has 824 million mobile monthly active users, with a single quarter growth of 39 million. “ Core business in the next three years The target of increasing the number of target users to 900 million “is close at hand. Among them, The annual consumer of the Chinese retail market reached 711 million, and more than 60% of the increase came from sinking markets.

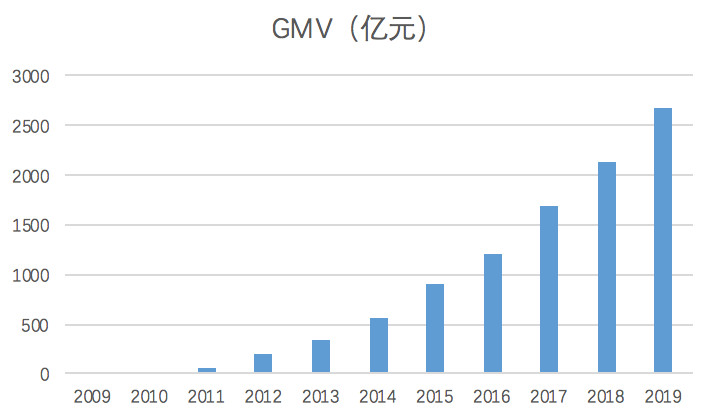

Double Eleventh promotion has become a great opportunity for brands to achieve sinking. Of the total GMV of Double 11, 54% comes from consumers in the sinking market. In addition, the GMV and monthly active users generated by Taobao Live in December both increased by more than double from the same period last year.

In the new quarter, Alibaba’s revenue has maintained a strong growth. On the one hand, core e-commerce business revenue has steadily increased, and the annual Tmall Double Eleven has become an important engine of quarterly revenue growth: the cost-effective offensive sinking market not only pulls over 60% of new revenue, but also doubles for Eleven increaseGrower to make a greater contribution.

In addition, the content service Taobao Live, which has risen in the past two years, broke 10 billion yuan within 9 hours of Double Eleven, and the GMV of the whole day was nearly 20 billion. After settlement by Alipay, the Tmall Double Eleven full-day GMV in 2019 reached 268.4 billion yuan, a year-on-year increase of 25%. Among them, 15 brands entered the 1 billion yuan club, and 299 brands entered the 100 million yuan club.

2009-2019 Tmall Double Eleven Day Revenue Data, Mapping:

On the other hand, although cloud business, local life, new retail business, digital media business, and logistics business have low profit margin contributions, they still maintain good revenue growth. Take the cloud business as an example, the first single quarter revenue exceeded 10 billion yuan, reaching 10.7 billion yuan. According to Canalys data, although Tencent Cloud’s market expansion has reached 15% in 2019, Alibaba has resisted the artillery fire from Tencent, with a market share of 47%. In addition, new retail business revenue also maintained a high growth year-on-year, exceeding 128%.

However, after 11 consecutive months of revenue growth of more than 40%, Ali’s quarterly revenue growth rate slightly declined. Next, factors such as the epidemic will lead to severe economic pressure, coupled with the fact that the first quarter has always been an off-season for e-commerce, these factors may lead to more significant seasonal weakness, and revenue and profits may be affected to some extent.

But the good news is that because of the epidemic, The nails based on PaaS and SaaS platforms, and Hema and Alibaba Cloud brought more new users and also expanded to include online education And remote office applications. In the long run, CICC expects that these businesses are expected to become Alibaba’s new valuation growth engine.