In the short term, the profit margin of logistics companies may face further narrowing; long-term head companies are expected to gain more capital favor and market share will further increase.

Editor’s note: This article is from WeChat public account “ Ocean Capital ” ( ID: Sino-oceancapital), author Ocean Capital

The macroeconomic level , the impact of the new crown epidemic on GDP may be greater than that of SARS in that year. Given that 2020 is the end of China ’s 13th Five-Year Plan, the government will hedge its economic downturn with a large number of fiscal, tax, and monetary policies. It is conservatively expected that GDP growth in 2020 will remain at 5.5-6%.

Logistics industry The overall correlation with the economy is high, short-term revenue of logistics companies is under pressure, and costs are rising, the profit space may face further narrowing . However, due to the epidemic situation, the industry’s backward production capacity will be further cleared, and leading companies are expected to gain more capital favor and achieve a further increase in market share.

In the medium and long term, we are still optimistic about investment opportunities in the following segments:

Less-than-truck and fast-moving industry : Large-size express delivery market with household appliances and household appliances as main transportation objects ;

Warehouse distribution industry : Online consumption penetration is accelerating, especially the consumer education cycle of fresh food and online education services is greatly shortened, which will promote the rapid growth of warehouse distribution industry;

Express industry : The gradual formation of a monopoly pattern will promote the rise of industry prices, the rise in profitability of head companies will drive valuation repairs, or it will create excess returns, with due attention to fixed growth and strategic investment opportunities.

I. The impact of the new crown epidemic on the economy may be greater than that of SARS, but it will not change the long-term economic development trend

(1) The impact of SARS in 2003 on the short-term economy was greater, but the medium- and long-term impact was smaller.

Overall, the outbreak of SARS in early 2003 caused China’s economy to fall significantly in the second quarter of 2003. The main sectors affected by SARS are the transportation industry, catering, and tourism industries of the tertiary industry, while the necessities industry, such as food, remains “firm.”The SARS epidemic has a short-term impact on the economy, but the mid- and long-term impact is small. In the second half of 2003, China’s macro economy returned to the rising channel.

(II) The economic impact of New Coronary Pneumonia in 2020 (especially the tertiary industry) will be greater than SARS.

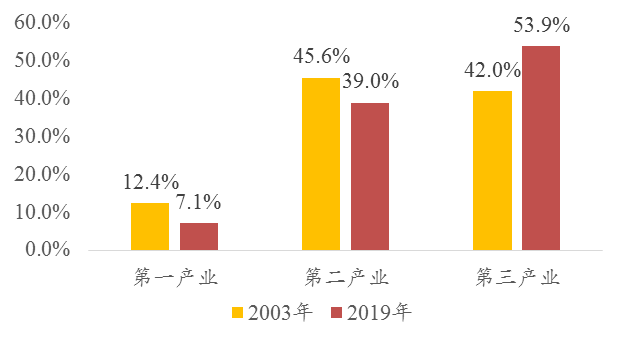

Compared to SARS, this new crown epidemic is more contagious and has a wider radiation range. The tertiary industry, which has been more affected by the epidemic, accounts for a higher proportion of current GDP than during SARS. In the current Chinese economic context, we expect the impact of the new crown epidemic on the economy to be greater than that of SARS.

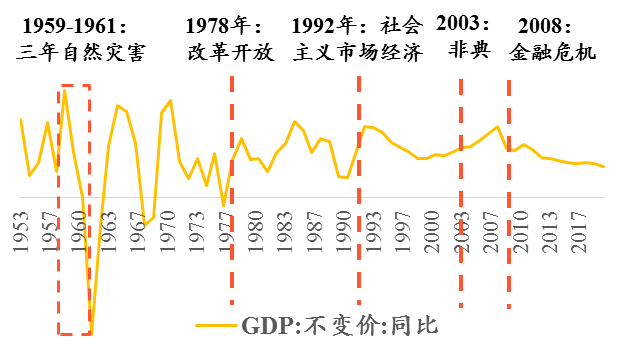

After entering the 21st century, the fluctuation of the impact of a single major event on China’s economy has flattened, and we judge that this epidemic will not change the medium and long-term development trend of our economy.

Figure 1: Proportion of economy and tertiary industry in two outbreaks

Figure 2: After the founding of the People’s Republic, the impact of major events on GDP

Source: wind, such as the Financial Research Institute, Ocean Capital Logistics Team

Second, the logistics sector has been greatly affected by the epidemic in the short term, and it will continue to keep pace with GDP growth in the medium and long term

(I) Short-term impact: income, cost, and capital endurance

The modern logistics system is closely connected. Express delivery, express transportation, complete vehicles, warehouse distribution, etc. are all part of the logistics supply chain. The impact of the epidemic on enterprises in different areas of logistics is basically the same. The impact of this epidemic on logistics companies includes: 1. Revenue decline: Affected by the epidemic, downstream B-end companies delayed construction, upstream and downstream companies have not resumed work, and the overall revenue of the logistics industry will decline.2. Increasing costs: On the one hand, the return to work rate has been greatly reduced, and the shortage of manpower has caused the cost to rise; on the other hand, inspection and disinfection stations have been set up in various places, the logistics lines have been blocked, and the time in transit has been increased, which has ultimately led to insufficient production capacity, reduced efficiency, and transportation costs Rising; 3. Funding pressure: affected by factors such as the decline in the speed of repayment and the delay in a new round of financing, the working capital turnover was tight, and the company experienced a temporary funding gap.

(II) The medium and long-term logistics industry will continue to keep pace with GDP and grow steadily.

The logistics industry is an important part of the national economy, and the logistics sector maintains a high correlation with the national economy. After the outbreak, the government supported logistics companies in various aspects such as tax incentives and loan subsidies. The new crown epidemic will not cause fundamental changes to the logistics industry, nor will it change the long-term development trend of the logistics market.

III. The sluggish performance of the logistics sector in 2019 may bring mid-to-long-term investment opportunities

From the perspective of the secondary market, The general trend of the logistics sector and the market began to diverge in the second half of 2019 , the logistics sector market trend continues to underperform Shanghai The Shenzhen 300 Index is mainly due to the overall decline in performance of the logistics industry due to macroeconomic impacts in 2019. At the same time, various express delivery companies have adopted price war strategies to affect the company’s financial data and further affect market prices. The valuation level of leading express delivery companies has continued to be lower than the valuation hub of the past two years. With the rapid development of China’s e-commerce industry, competition in the express delivery market remains fierce. Second-tier express delivery companies are increasingly under pressure to survive, and incidents such as mergers and acquisitions, bankruptcy and liquidation occur from time to time. As the rate continues to increase, it is expected that there will be opportunities for medium and long-term layout.

![The epidemic is a double-edged sword, which is more optimistic about the rapid development of head enterprises in the medium and long term.]()

Figure 3: H2 logistics sector deviates from the market trend in 2019

(I) Short-term impact: income, cost, and capital endurance

The modern logistics system is closely connected. Express delivery, express transportation, complete vehicles, warehouse distribution, etc. are all part of the logistics supply chain. The impact of the epidemic on enterprises in different areas of logistics is basically the same. The impact of this epidemic on logistics companies includes: 1. Revenue decline: Affected by the epidemic, downstream B-end companies delayed construction, upstream and downstream companies have not resumed work, and the overall revenue of the logistics industry will decline.2. Increasing costs: On the one hand, the return to work rate has been greatly reduced, and the shortage of manpower has caused the cost to rise; on the other hand, inspection and disinfection stations have been set up in various places, the logistics lines have been blocked, and the time in transit has been increased, which has ultimately led to insufficient production capacity, reduced efficiency, and transportation costs Rising; 3. Funding pressure: affected by factors such as the decline in the speed of repayment and the delay in a new round of financing, the working capital turnover was tight, and the company experienced a temporary funding gap.

(II) The medium and long-term logistics industry will continue to keep pace with GDP and grow steadily.

The logistics industry is an important part of the national economy, and the logistics sector maintains a high correlation with the national economy. After the outbreak, the government supported logistics companies in various aspects such as tax incentives and loan subsidies. The new crown epidemic will not cause fundamental changes to the logistics industry, nor will it change the long-term development trend of the logistics market.

III. The sluggish performance of the logistics sector in 2019 may bring mid-to-long-term investment opportunities

From the perspective of the secondary market, The general trend of the logistics sector and the market began to diverge in the second half of 2019 , the logistics sector market trend continues to underperform Shanghai The Shenzhen 300 Index is mainly due to the overall decline in performance of the logistics industry due to macroeconomic impacts in 2019. At the same time, various express delivery companies have adopted price war strategies to affect the company’s financial data and further affect market prices. The valuation level of leading express delivery companies has continued to be lower than the valuation hub of the past two years. With the rapid development of China’s e-commerce industry, competition in the express delivery market remains fierce. Second-tier express delivery companies are increasingly under pressure to survive, and incidents such as mergers and acquisitions, bankruptcy and liquidation occur from time to time. As the rate continues to increase, it is expected that there will be opportunities for medium and long-term layout.

![The epidemic is a double-edged sword, which is more optimistic about the rapid development of head enterprises in the medium and long term.]()

Figure 3: H2 logistics sector deviates from the market trend in 2019