Profitability cannot match the size of users, and financial performance is disappointing.

Editor’s note: This article is from the micro-channel public number “Capital deep exploration” (ID: deep_insights) , Author: Ya Lan Cai Baowang.

The impact of the epidemic on offline consumer companies is nothing new, and it has never occurred to us that online giants such as Weibo cannot withstand the storm.

According to Questmobile data from a third-party monitoring agency, due to the combined effects of the Spring Festival holiday, the new crown epidemic, and the death effect of Kobe, the daily active user scale of Weibo reached a peak of 239 million on January 27.

The increase in active users and reading volume is a good thing. Many game companies and online education companies have been blessed by capital because of the disaster. But for Weibo, it just exposes its weaknesses as a platform.

The just-released Sina Weibo earnings report gave lower-than-expected Q1 guidance. The company believes that the decline in revenue in the first quarter may be as high as 15% to 20%, compared with the market’s previous forecast of a decline of about 13%. This means that because of the “unexpected” new traffic, activity, and length of use of the epidemic, it may not be effectively converted into revenue, and Weibo’s business capabilities will inevitably face unprecedented challenges.

Take a closer look at Weibo and Weibo’s parent company Sina’s 2019 fourth quarter and full-year performance reports. Although the market already has lower expectations for Weibo and Sina’s performance, the company’s actual performance is still low. Previous market and company performance expectations.

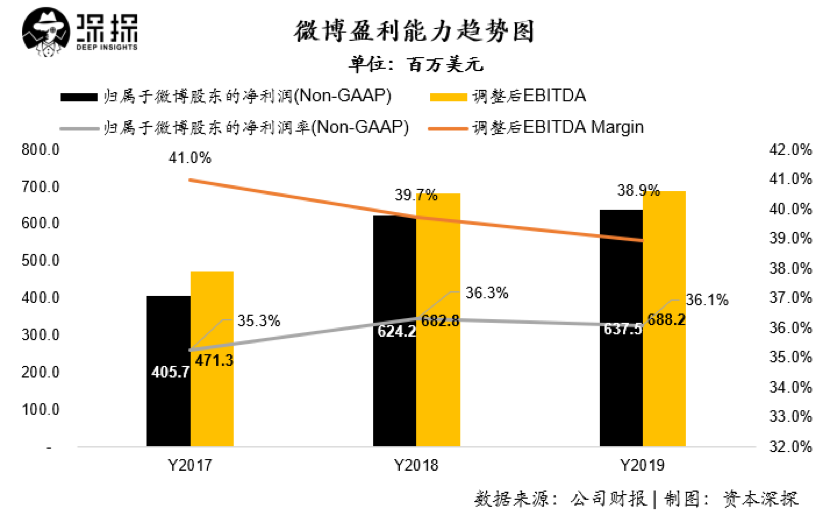

Finance reports show that Weibo achieved operating income of US $ 468 million and US $ 1.767 billion in the fourth quarter and the full year of 2019, and its fourth-quarter performance was 2.8% lower than the same period last year, lower than the company’s previous performance guidance of 0-3% Growth; Non-GAAP net profit attributable to shareholders of the parent company was 177 million and 638 million, respectively, with net profit margins of 37.7% and 36.1%.

The revenue of its parent company Sina for the fourth quarter and full year of 2019 was US $ 593 million and US $ 2,163 million, respectively, a year-on-year increase of 4% and 3%. US dollars.

Although Weibo and Sina still make money, the efficiency of their overall profitability obviously cannot match that of usersMatch the scale. With the tightening of advertiser budgets, increased competition in the advertising market, and the rise of new forces such as byte bounce, Weibo and Sina, which lack innovation and have a single source of income, are likely to face the crisis of “front waves losing on the beach”.

Advertising business is under pressure, and Weibo ’s fatigue is full

Although Sina and Weibo are two independent listed companies, as a holding subsidiary of Sina, Weibo accounts for almost 80% of the entire Sina Group’s revenue and is the absolute core of Sina’s business system.

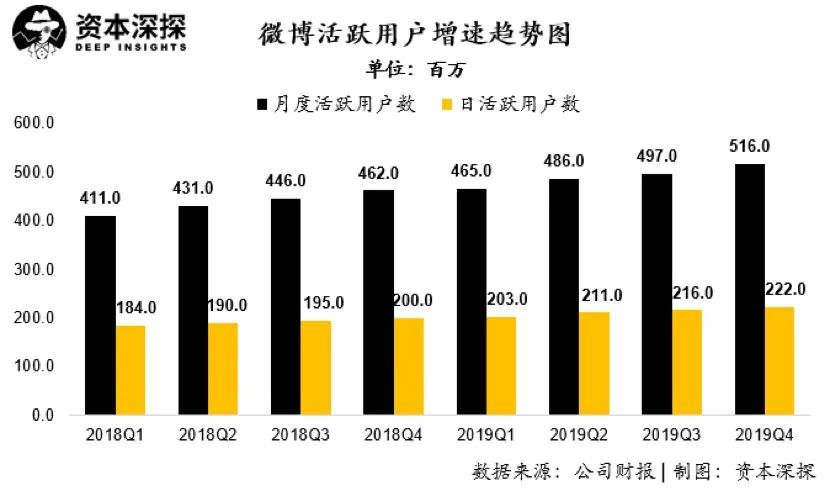

As of December 2019, Weibo ’s monthly active users entered 500 million clubs for the first time, reaching 516 million, a net increase of 54 million compared to the end of 2018. The number of daily active users reached 222 million, a net increase of 22 million compared to December last year. Affected by the new crown epidemic, it can be expected that the number of active users of Weibo in the first quarter of 2020 will still usher in a wave of growth.

In the past year, the number of active users on Weibo has grown rapidly. With such a large user base, it has still achieved an increase of more than 10%, which is not easy.

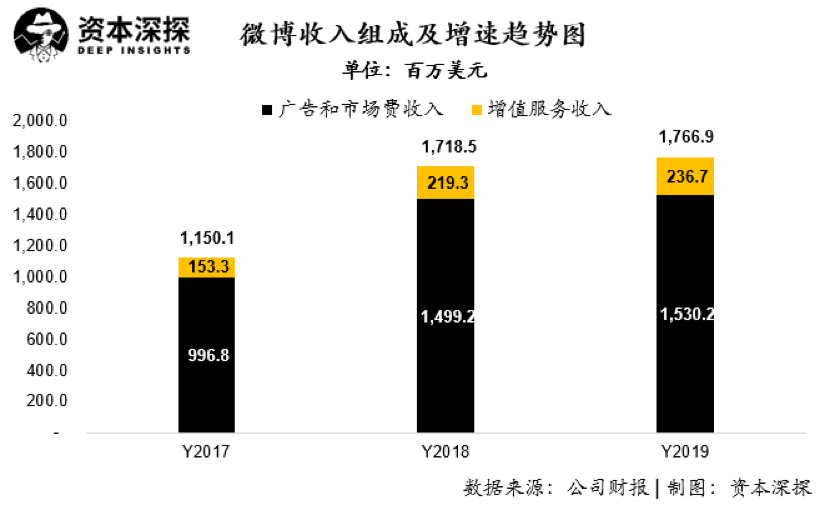

However, Weibo’s financial performance is not enough for such user growth. Weibo achieved total revenue of US $ 1.768 billion in 2019, a year-on-year increase of only 2.8%, which is much lower than the company’s active user growth rate.

The weak growth of Weibo’s revenue is largely due to the monetization model of over-reliance on advertising. The single means of monetization resulted in: In 2019, Weibo’s advertising and market fee income reached $ 1.53 billion, a year-on-year growth of only 2.1% At the same time, the company’s advertising and marketing fee income accounted for 86.6% of the total revenue, and the company’s revenue source was single.

For many companies that rely on advertising as their main source of revenue, 2019 will be very difficult.

On the one hand, advertisers ’budgets for advertising have been tightened, and the overall growth of the advertising industry has slowed. On the other hand, as more new entrants have joined and advertisers’ requirements for advertising conversion have increased, Also makes the competition between advertising platforms more intensified.

But there isThe two news that was officially stated as “untrue” also has certain reference value at this time-byte beats the annual revenue in 2019 of more than 140 billion yuan; the fast advertising revenue in 2019 exceeds 13 billion yuan. No matter what the exact numbers are, their existence will undoubtedly put great pressure on the advertising market.

Even WeChat, which has always prioritized user experience, has had to accelerate the pace of commercialization under market pressure. According to Tencent’s financial report, as of the first three quarters of 2019, Tencent’s social and other advertising revenues reached 34.51 billion yuan, an increase of 23.6% year-on-year. The main sources of growth were WeChat Guangdiantong, the circle of friends, and small program advertising revenue.

In contrast, Weibo lacks innovation and shows signs of fatigue.

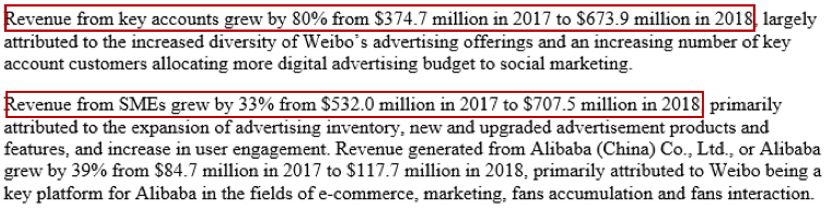

According to its 2018 annual report, its KA advertising revenues mainly for display advertising and SME revenues mainly for performance advertising accounted for almost half (49% of KA advertising), which means that it is still Nearly half of advertisers are promoted through display advertising, which has greatly reduced the value of Weibo ’s 500 million monthly active users (performance ads are also displayed for a longer time, and the frequency of display is higher).

The advertising world has changed. Manufacturers and advertisers have increasingly valued the effectiveness of advertising, which has also led to more advertising channels such as Toutiao and WeChat GuangDianTong, which are based on algorithmic recommendations, and TaoBao, KuaiShou and other live channels (with direct conversion). popular.

Source: Weibo Annual Report 2018

The fatigue of Weibo on advertisements is reflected not only in the slowdown in revenue growth, but also in the collection of receivables.

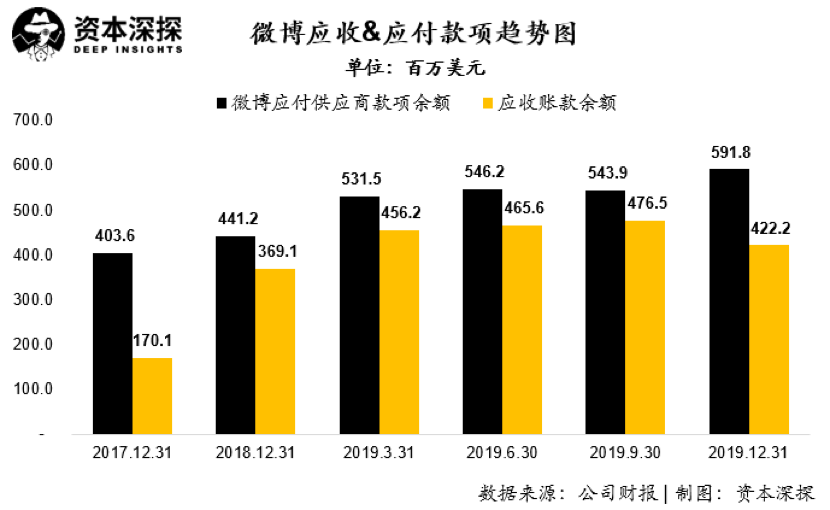

In 2019, Weibo’s accounts receivable balance increased significantly in the first quarter and remained at a high level in 19 years. As of the end of 2019, the company’s accounts receivable balance reached 422 million US dollars, an increase of 53 million US dollars compared with the end of 2018. This means that although Weibo ’s advertising revenue has not declined, advertisers have a longer account period for Weibo and it is more difficult for the company to receive payments than in previous years.

In order to reduce its own operating pressure, Weibo indirectly releases the pressure on the advertiser’s account period to its suppliers. According to Weibo’s financial report, the balance of Weibo’s payables (including accounts payable and accrued expenses, mainly payable to suppliers) as of the end of 19 years increased by US $ 151 million compared with the end of 2018. Supplier payment to reduce own risk.

However, Weibo deserves to be at the helm of “accounting”-in terms of profitability, Weibo’s net profit attributable to shareholders of the parent company under Non-GAAP in 2019 is US $ 638 million, with a net profit margin of 36.1%; adjustment Post-EBITDA was $ 688 million and EBITDA Margin was 38.9%.

It can be seen that Weibo is still a very profitable company. In the fierce market environment, Weibo still maintains a high profit margin consistent with previous years, and the company has an excellent performance in cost control.

The blood loss of Sina portal business makes it difficult for consumer finance to reverse the situation

Weibo’s growth is weak, but it is still very profitable. In contrast, Weibo’s parent company, Sina, had a hard time.

After excluding Weibo business, Sina’s portal business (Portal business, including portal advertising and consumer finance) suffered a huge loss.

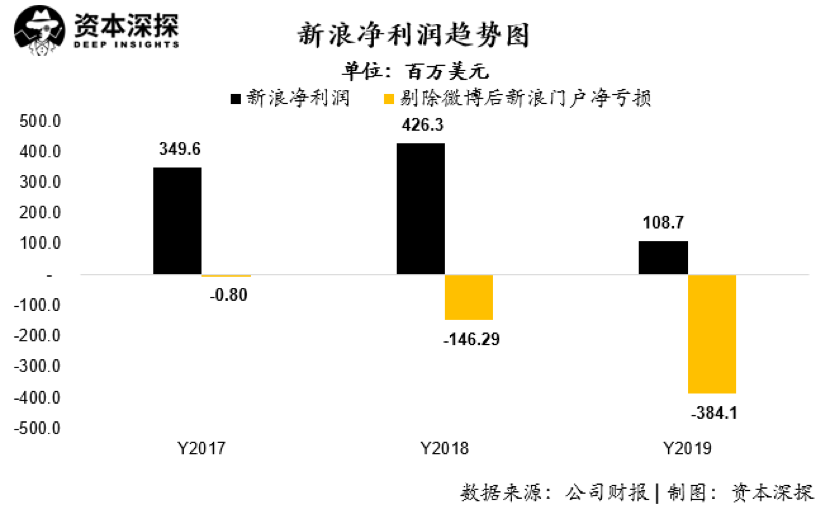

According to Sina’s 2019 report, its total revenue in 2019 was US $ 2.163 billion, and Weibo’s revenue accounted for 82% of total revenue. Excluding Weibo revenue, Sina’s portal business revenue was only US $ 423 million, an increase of only 5.4% compared to the same period last year. Since 2017, the Sina portal business has begun to show a loss, with a net loss of 800,000 US dollars, and this trend will continue to expand in 2018 and 2019. As of 2018, the loss of Sina’s portal business expanded to US $ 146 million, compared to a loss of US $ 384 million in 2019.

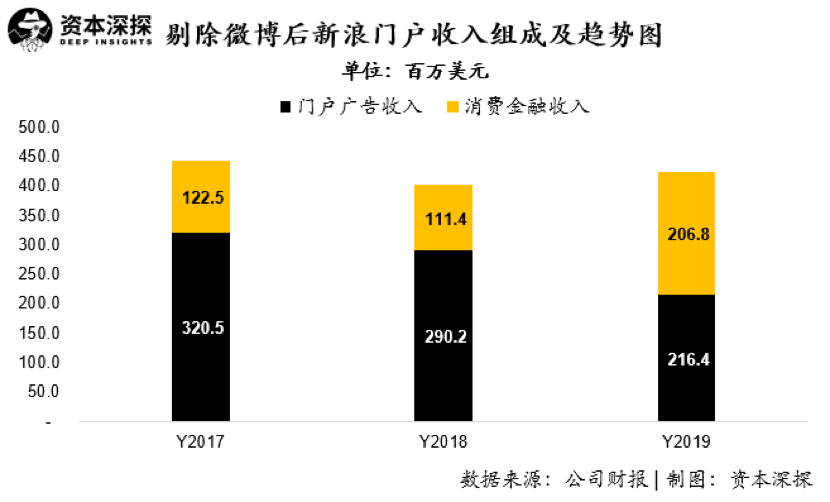

Among them, the portal advertising business continued to decline rapidly, only 216 million US dollars in 2019, a year-on-year decrease of 25.4%, and this is the second consecutive year of decline.

The overall market value of Sina is currently only around 2.5 billion US dollars. Excluding the value of controlling Weibo ’s equity, the valuation of Sina’s portal business is even negative. Control market value of about $ 4.1 billion).

Looking at the continued shrinking of the portal advertising business, Sina is also constantly looking for new breakthrough opportunities. Its hope of saving lives may be pinned on consumer finance. Its total consumer finance revenue in 2019 reached US $ 207 million, a significant increase of 85.6% year-on-year. In the foreseeable future, Sina, one of the largest portals in the past, will likely become an Internet financial company.

But consumer finance is not a panacea.

As early as 2015, Sina began to actively deploy its financial sector business, launching products such as “Sina Instalment”, but limited to its own e-commerce business, which can form a natural closed loop, and there is no WeChat red envelope ” There is a flash of light, “and progress in its financial business has been difficult.

In 2017, Sina Finance launched Weibo to borrow money for diversion through Weibo and Weibo wallet.

It should be noted here that although it is called “Weibo borrowing money”, its entire income is recorded in the Sina portal business. Weibo and Weibo wallets only borrow money from Sina as a diversion entrance. Weibo borrowing money is directly controlled by Sina Group, and its actual controllers are Liu Yunli, vice president of Sina Investment, and Zhang Lijing, investment director.

Although consumer finance has obvious advantages in terms of security, there are also a number of consumer finance companies, including Lexin and Qudian, which are listed on US stocks. The industry has a high degree of transparency and standardization. But as a “high-interest loan”, it still has its natural insurmountable problems. Usury loan and huge profit collection are common problems that plague consumer finance companies, and it is difficult to avoid borrowing money on Weibo.

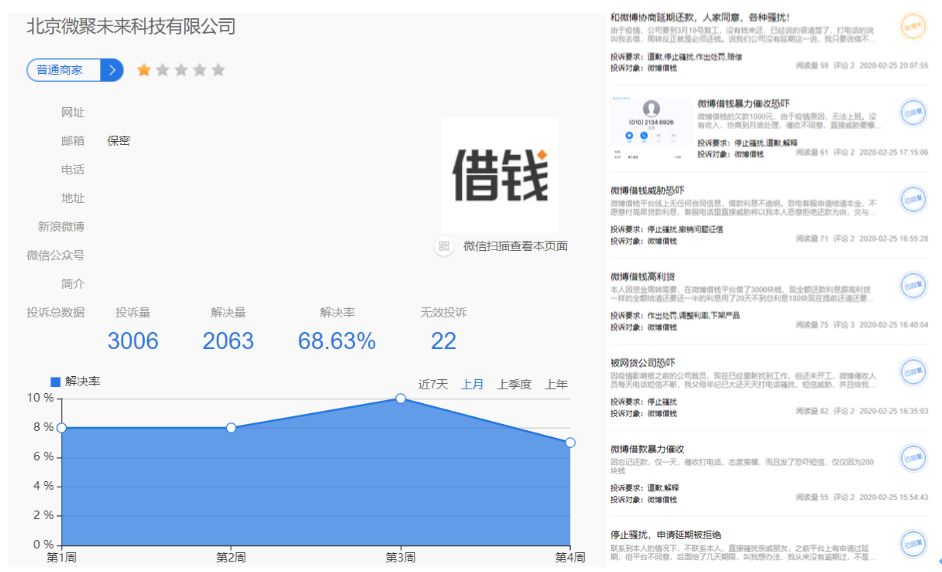

According to the public data of Ju Complaint Platform, as of now, the total number of complaints received by Beijing Wei Ju Future Technology Co., Ltd., the microblog borrowing operation entity, has exceeded 3,000, of which, the proportion of complaints about usury and high profit collection is relatively high.

The reason why a large number of users question the existence of usury on Weibo borrowing money is mainly because when Weibo borrows money from customers, it calculates interest in the form of simple interest, but the user is actually in the process of repayment. Since the principal and interest are paid in installments, its actual compound interest rate is much higher than its simple interest accounting amount.

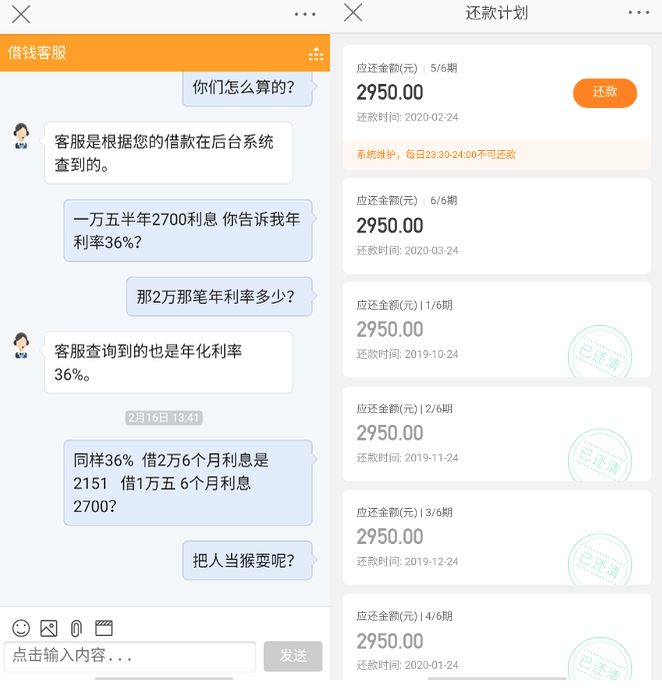

For example, a user borrows 15,000 yuan from Weibo and borrows 2700 yuan for half a year. If the total annual interest is calculated to be 5,400 yuan divided by 15,000 yuan, the interest rate is indeed 36%. However, because the user does not repay the principal and interest at one time when it is due in half a year, but pays the principal and interest every month, its annual compound interest rate is actually close to 60%.

However, national regulations only stipulate that the annual interest rate of borrowings exceeding 36% is usury, but there is no mention of simple interest, compound interest, etc., so it is difficult to determine whether Weibo borrowing money is higher than the legal requirements.

Screenshot of users’ complaints on Jucom platform

In addition to making articles on interest rates, Weibo borrowing money also provides “double insurance” for high-interest loans through “reasonable” contractual arrangements. In fact, the high annualized interest of Weibo borrowing money is composed of two parts of fees, namely the “interest fee” and the “service fee”.

During the borrowing process, the borrower will select two agreements, namely the “Loan Agreement” and the “User Agreement”. In the “Loan Agreement”, the counterparty that the borrower signs the agreement with is the financial institution that actually conducts the lending. Of the total expenses paid by the borrower, the part paid to the lender is the “interest expense on borrowing”.

In the “User Agreement”, the counterparty to the agreement signed by the borrower is “Beijing Weiju Future Technology Co., Ltd.”, which is the operator that borrows money from Weibo, and the payment part of it is the “service fee”. The service content is “help the borrower find the lender to establish a loan relationship, and provide technical and channel support.”

Usually the service fee charged by Weibo is much higher than the interest on borrowings, so in this case, the situation of usury will never exist.

Deep Capital has consulted lawyers in related fields for this purpose. Lawyers said that this approach of charging low interest by lenders and high service fees by platformers is a popular way of online loan platforms. As the “service fee” follows market pricing principles, while avoiding legal risks, the platform charges high fees to borrowers.

No matter what kind of arrangement, for the borrower, the loan obtained by borrowing money through Weibo is indeed used in the process of use.High cost of capital paid. Whether or not there is a risk at the legal level, borrowing money from Weibo faces huge risks in terms of credibility.

In addition to being suspected of “usury loans”, related to “profiteering” are more manifestations of the borrowing platform’s shortcomings in risk control capabilities and user identification capabilities. The core reason for the huge profit collection is that the platform cannot identify the user’s credit rating and repayment ability when borrowing, so that after the overdue, the end user can only collect money through informal means.

Weibo, as one of the largest social platforms in China, has a large number of users and excellent diversion ability. However, since the user does not have any consumption behavior on the Weibo platform, it is difficult to obtain the actual user’s actual information through only limited real-name authentication. Credit rating.

Compared with professional consumer finance companies such as Lexin and 360 Finance, they invested a lot of resources to build a professional risk control team to develop risk control tools (the number of 360 financial risk control personnel accounts for more than half of the company’s total employees). It is obviously difficult for money to invest in such a large amount of resources.

Weibo ’s lack of risk control capabilities is also reflected in its choice of cooperative financial institutions. When Weibo borrowed money in the early development of consumer finance business, due to the company’s small overall volume and low market share, it was difficult to cooperate with large licensed financial institutions to develop loan business cooperation.

According to Beijing Youth Daily, Jiujiang Yunke Network Microfinance Co., Ltd. is a licensed financial institution that cooperated with Weibo in borrowing money in the early stage. Subsidiary. Li Luyi, the founder and former chairman of the board of directors of Yunyou Holdings, is under police investigation for P2P online loan platform issues, while Li Luyi is currently in a state of loss of contact.

Jiujiang Yunke Network Microfinance Co., Ltd. is one of the early shareholders of Beijing Weiju Future Technology Co., Ltd., holding 10% of the shares

Sina, founded in 1998, has gone through more than 20 spring and autumn, and Weibo, established in 2009, has also gone through ten years. They have experienced the ups and downs of the Internet and mobile Internet, and they have been highly valued.

Mo Yan CEO Tang Yan once thought in an interview that if he changed to Weibo, he would integrate the functions of Face Book and Twitter as soon as possible, and vigorously promote the IM (instant messaging) function. “Weibo has that imagination.”

Tencent Ma Huateng has publicly stated at the Tsinghua Management Forum that Tencent has encountered the biggestThe crisis was the rise of “Sina Weibo”. When I heard that a university had established a Weibo group, I was nervous.

Weibo and Sina will disappoint everyone?

Weibo’s growth is weak, but it is still very profitable. In contrast, Weibo’s parent company, Sina, had a hard time.

After excluding Weibo business, Sina’s portal business (Portal business, including portal advertising and consumer finance) suffered a huge loss.

According to Sina’s 2019 report, its total revenue in 2019 was US $ 2.163 billion, and Weibo’s revenue accounted for 82% of total revenue. Excluding Weibo revenue, Sina’s portal business revenue was only US $ 423 million, an increase of only 5.4% compared to the same period last year. Since 2017, the Sina portal business has begun to show a loss, with a net loss of 800,000 US dollars, and this trend will continue to expand in 2018 and 2019. As of 2018, the loss of Sina’s portal business expanded to US $ 146 million, compared to a loss of US $ 384 million in 2019.

Among them, the portal advertising business continued to decline rapidly, only 216 million US dollars in 2019, a year-on-year decrease of 25.4%, and this is the second consecutive year of decline.

The overall market value of Sina is currently only around 2.5 billion US dollars. Excluding the value of controlling Weibo ’s equity, the valuation of Sina’s portal business is even negative. Control market value of about $ 4.1 billion).

Looking at the continued shrinking of the portal advertising business, Sina is also constantly looking for new breakthrough opportunities. Its hope of saving lives may be pinned on consumer finance. Its total consumer finance revenue in 2019 reached US $ 207 million, a significant increase of 85.6% year-on-year. In the foreseeable future, Sina, one of the largest portals in the past, will likely become an Internet financial company.

But consumer finance is not a panacea.

As early as 2015, Sina began to actively deploy its financial sector business, launching products such as “Sina Instalment”, but limited to its own e-commerce business, which can form a natural closed loop, and there is no WeChat red envelope ” There is a flash of light, “and progress in its financial business has been difficult.

In 2017, Sina Finance launched Weibo to borrow money for diversion through Weibo and Weibo wallet.

It should be noted here that although it is called “Weibo borrowing money”, its entire income is recorded in the Sina portal business. Weibo and Weibo wallets only borrow money from Sina as a diversion entrance. Weibo borrowing money is directly controlled by Sina Group, and its actual controllers are Liu Yunli, vice president of Sina Investment, and Zhang Lijing, investment director.

Although consumer finance has obvious advantages in terms of security, there are also a number of consumer finance companies, including Lexin and Qudian, which are listed on US stocks. The industry has a high degree of transparency and standardization. But as a “high-interest loan”, it still has its natural insurmountable problems. Usury loan and huge profit collection are common problems that plague consumer finance companies, and it is difficult to avoid borrowing money on Weibo.

According to the public data of Ju Complaint Platform, as of now, the total number of complaints received by Beijing Wei Ju Future Technology Co., Ltd., the microblog borrowing operation entity, has exceeded 3,000, of which, the proportion of complaints about usury and high profit collection is relatively high.

The reason why a large number of users question the existence of usury on Weibo borrowing money is mainly because when Weibo borrows money from customers, it calculates interest in the form of simple interest, but the user is actually in the process of repayment. Since the principal and interest are paid in installments, its actual compound interest rate is much higher than its simple interest accounting amount.

For example, a user borrows 15,000 yuan from Weibo and borrows 2700 yuan for half a year. If the total annual interest is calculated to be 5,400 yuan divided by 15,000 yuan, the interest rate is indeed 36%. However, because the user does not repay the principal and interest at one time when it is due in half a year, but pays the principal and interest every month, its annual compound interest rate is actually close to 60%.

However, national regulations only stipulate that the annual interest rate of borrowings exceeding 36% is usury, but there is no mention of simple interest, compound interest, etc., so it is difficult to determine whether Weibo borrowing money is higher than the legal requirements.

Screenshot of users’ complaints on Jucom platform

In addition to making articles on interest rates, Weibo borrowing money also provides “double insurance” for high-interest loans through “reasonable” contractual arrangements. In fact, the high annualized interest of Weibo borrowing money is composed of two parts of fees, namely the “interest fee” and the “service fee”.

During the borrowing process, the borrower will select two agreements, namely the “Loan Agreement” and the “User Agreement”. In the “Loan Agreement”, the counterparty that the borrower signs the agreement with is the financial institution that actually conducts the lending. Of the total expenses paid by the borrower, the part paid to the lender is the “interest expense on borrowing”.

In the “User Agreement”, the counterparty to the agreement signed by the borrower is “Beijing Weiju Future Technology Co., Ltd.”, which is the operator that borrows money from Weibo, and the payment part of it is the “service fee”. The service content is “help the borrower find the lender to establish a loan relationship, and provide technical and channel support.”

Usually the service fee charged by Weibo is much higher than the interest on borrowings, so in this case, the situation of usury will never exist.

Deep Capital has consulted lawyers in related fields for this purpose. Lawyers said that this approach of charging low interest by lenders and high service fees by platformers is a popular way of online loan platforms. As the “service fee” follows market pricing principles, while avoiding legal risks, the platform charges high fees to borrowers.

No matter what kind of arrangement, for the borrower, the loan obtained by borrowing money through Weibo is indeed used in the process of use.High cost of capital paid. Whether or not there is a risk at the legal level, borrowing money from Weibo faces huge risks in terms of credibility.

In addition to being suspected of “usury loans”, related to “profiteering” are more manifestations of the borrowing platform’s shortcomings in risk control capabilities and user identification capabilities. The core reason for the huge profit collection is that the platform cannot identify the user’s credit rating and repayment ability when borrowing, so that after the overdue, the end user can only collect money through informal means.

Weibo, as one of the largest social platforms in China, has a large number of users and excellent diversion ability. However, since the user does not have any consumption behavior on the Weibo platform, it is difficult to obtain the actual user’s actual information through only limited real-name authentication. Credit rating.

Compared with professional consumer finance companies such as Lexin and 360 Finance, they invested a lot of resources to build a professional risk control team to develop risk control tools (the number of 360 financial risk control personnel accounts for more than half of the company’s total employees). It is obviously difficult for money to invest in such a large amount of resources.

Weibo ’s lack of risk control capabilities is also reflected in its choice of cooperative financial institutions. When Weibo borrowed money in the early development of consumer finance business, due to the company’s small overall volume and low market share, it was difficult to cooperate with large licensed financial institutions to develop loan business cooperation.

According to Beijing Youth Daily, Jiujiang Yunke Network Microfinance Co., Ltd. is a licensed financial institution that cooperated with Weibo in borrowing money in the early stage. Subsidiary. Li Luyi, the founder and former chairman of the board of directors of Yunyou Holdings, is under police investigation for P2P online loan platform issues, while Li Luyi is currently in a state of loss of contact.

Jiujiang Yunke Network Microfinance Co., Ltd. is one of the early shareholders of Beijing Weiju Future Technology Co., Ltd., holding 10% of the shares

Sina, founded in 1998, has gone through more than 20 spring and autumn, and Weibo, established in 2009, has also gone through ten years. They have experienced the ups and downs of the Internet and mobile Internet, and they have been highly valued.

Mo Yan CEO Tang Yan once thought in an interview that if he changed to Weibo, he would integrate the functions of Face Book and Twitter as soon as possible, and vigorously promote the IM (instant messaging) function. “Weibo has that imagination.”

Tencent Ma Huateng has publicly stated at the Tsinghua Management Forum that Tencent has encountered the biggestThe crisis was the rise of “Sina Weibo”. When I heard that a university had established a Weibo group, I was nervous.

Weibo and Sina will disappoint everyone?