The uncertainty of the overseas market caused by the epidemic or the recent divergence of views on Xiaomi’s growth prospects.

Since 2019, the European market has become the core driving force for the continued growth of Xiaomi’s overseas shipments. But this momentum may face challenges in 2020.

From February 18 to March 10, 21 days before and after, JP Morgan (JP Morgan Chase) downgraded the stock of Xiaomi Group (1810.HK, hereinafter referred to as “Xiaomi”) from “Hold” To “sell”, but raise the target price to HK $ 9.

JP Morgan said in a March 10 report that Xiaomi has risen 12% year-to-date, reflecting the strong growth of the domestic 5G market and overseas business. However, JP Morgan still believes that Xiaomi’s market share of domestic 5G mobile phones and MAU (monthly active users) are unlikely to increase significantly, mainly due to fierce competition from competitors such as Huawei, OPPO and vivo.

In addition, JP Morgan pointed out that the key downside risk for Xiaomi is the longer-than-expected duration of the global epidemic, which may lead to weak sales in domestic and foreign markets and potential risks to China’s Internet service business. The bank mentioned in the report that if the European epidemic worsens, smartphone demand may be negatively affected. In the past few quarters, the European market has been the main growth driver for Xiaomi’s smartphone business.

The recent changes in the European epidemic are one of the direct reasons for JP Morgan’s downgrade of Xiaomi stock. In the February 18th report, JP Morgan did not mention the impact of the epidemic on the overseas market of Xiaomi mobile phones in the downside risk. In fact, , the overseas mobile phone market at that time was still the millet that JP Morgan believed. Surprised Upside Space .

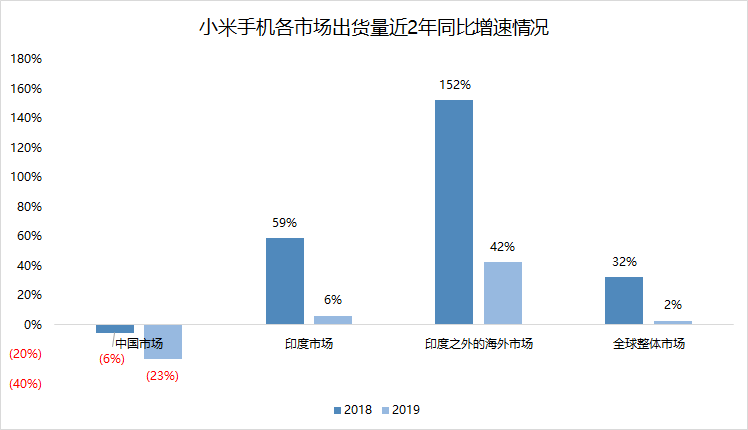

Mapping, data source: according to IDC data

It can also be seen from the IDC data that after the shipment of Xiaomi ’s mobile phone in the Indian market is close to the ceiling, the rapid growth from the European market is provoking the beam of the growth of Xiaomi ’s overseas market, thereby driving Xiaomi ’s global market shipment Volume continues to grow.

But the uncertainty brought about by the global epidemic will make the outside world’s forecast of Xiaomi’s growth prospects diverge in the near future.

CCB International also downgraded Xiaomi’s stock rating from “buy” to “hold” in its research report on March 12. The bank said that it maintains its profit forecast for Xiaomi in 2019 unchanged, but cut its profit forecast for 2020-2021 by 14% -24% to reflect higher research and development costs and the impact of the epidemic.

Apart from the two brokers mentioned above, most brokers remain optimistic about Xiaomi’s growth prospects.

CICC said in a report released on March 5 that Xiaomi ’s shipments in 2020 are expected to increase to 141 million. Market share in China, India, Western Europe and other regions Will be further improved.

China CITIC Securities said in its March 9 report that the domestic epidemic has a short-term impact on production and sales, but Xiaomi mainly sells online in China, and the other 2/3 shipments Overseas, so the relative impact will be small. However, CITIC Securities did not explicitly mention the potential impact of the overseas epidemic.

As of press time, Bloomberg data shows that Xiaomi shares have a total of 26 “buy” ratings, nine “hold” ratings and four “sell” ratings, with a 12-month average target price of HK $ 13.23 .

(The cover picture was taken by the author)