Is the old cave filled up?

Editor’s note: This article comes from WeChat public account: Zhiqu Finance and Economics (ID: zhiqucjs) a>, author: Fun little sister, authorized reprint

Greentown’s house is a timeless legend on rivers and lakes, and Greentown’s stock price is also an eternal topic on rivers and lakes.

That’s the answer: buy a house in Greentown, don’t buy Greentown stock!

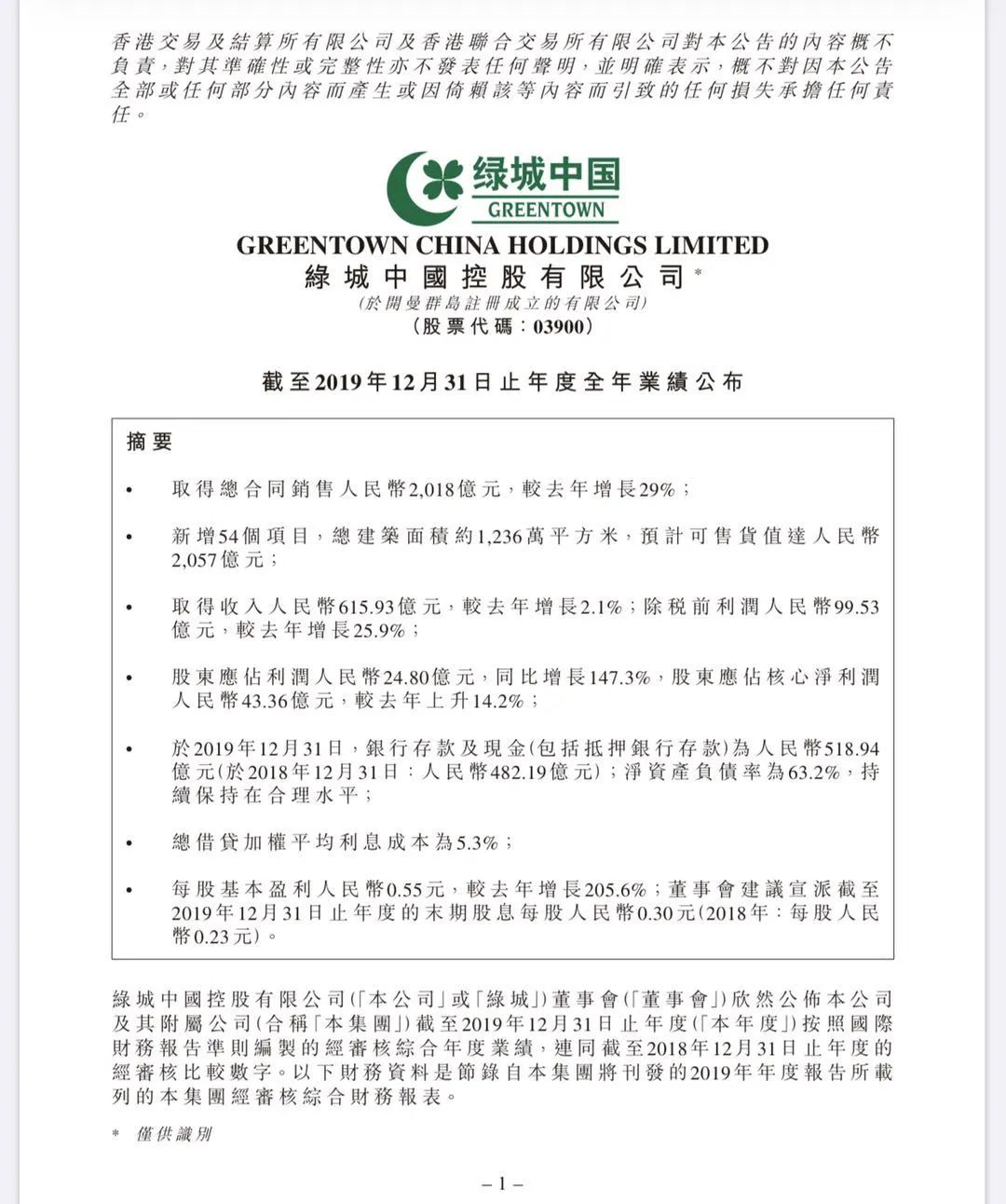

On the morning of March 23, Greentown announced its 2019 results announcement. In 2019, it achieved revenue of 61.59 billion yuan, an increase of 2.1% year-on-year. The total contracted sales area was approximately 10.27 million square meters, and the total contracted sales amount was approximately RMB 201.8 billion, an increase of 29% year-on-year. The sales scale reached a record high. Profit attributable to shareholders increased by 147.3% year-on-year to RMB 2.480 billion.

Sales and all aspects met expectations, but then Greentown China’s stock price fell in the early morning, as of 9:44, down 16.04%, quoted at 6.96 Hong Kong dollars, the market value is less than 14 billion yuan.

The crowd opened their eyes and thought that they were on the wrong set and ran to Evergrande’s room for profit warning. Shareholders are even more mournful.

In fact, after CCCC became a major shareholder of Greentown, Greentown has indeed changed a lot in the past two years. Operation management is improving, financial costs are reduced, and the company is back on the growth track. But the biggest problem of Greentown China is that the financial report is too unpredictable and shareholders’ profits are too poor.

The annual report shows that Greentown China’s perpetual debt has risen from 18.5 billion yuan in a half year to a total of 21,229 million yuan. The net profit of shareholders should be reduced by 1.287 billion in dividends from perpetual bonds, which means that the net profit attributable to mothers is only 1.193 billion yuan.

The operating income of more than 60 billion yuan reaches 1.1 billion yuan, and the net profit margin is less than 2 percentage points. Industry countdown!

You know, the average sales price of Greentown projects has reached 25,936 yuan, which is in the forefront of the industry. This is really the most expensive house to sell and earn the lowest net interest rate!

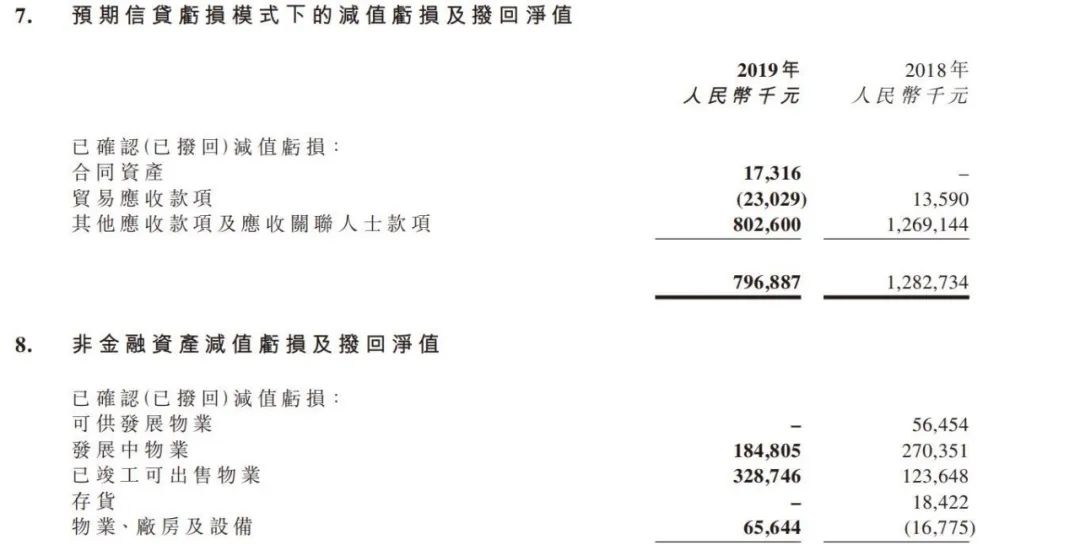

In addition, in the 2019 annual report, an additional 1.5 billion yuan in asset impairment was made. Greentown has been depreciating assets for three consecutive years. The external expectation is that asset impairment is basically complete. Moreover, in the first half of 2019, no large-scale asset impairment was performed, and all of it suddenly exploded in the second half of the year.

If last year Greentown’s financial report was ugly and understandable because of some historical problems, this year’s financial report is very clear. The interest on perpetual bonds has not been played out. Impairment is accrued year after year, and most of the profits are eroded every year.

Before everyone was betting that the high-priced landmines in Greentown were over, and the performance was reversed, but this time they let everyone down. Uncertainty is the biggest crime, and it is impossible to kill the market.

Of course, we must look at everything in two. The sales of Greentown’s 2019 performance settlement are the projects of 2017 and 2018. These projects are the land of 2016 and can be regarded as Song Weiping’s pot. Only the annual report performance in 2021 and 2022 can reflect Zhang Weidong’s management level and performance.

Greentown China ’s expectations depend on more than 2019 results.

Since the beginning of this year, Greentown has actively expanded its land market, with land investment in Hangzhou, Beijing, Wenzhou, and Zhejiang exceeding 20 billion yuan. At the same time, the company proactively issued debts and raised sufficient funds.

At the online performance meeting on the afternoon of March 23, Chairman of the Board of Directors of Greentown China Zhang Yadong revealed that the sales scale in the next five years will exceed 500 billion yuan.

But this is not necessarily a clever way. Real estate has passed the era of large-scale expansion, and Greentown itself is not good at low-cost scale.

But no matter what, the value of Greentown’s brand is still there, and the popularity of the product and the agency construction listing still give it future expectations. Let ’s look forward to what kind of transcripts will be produced by Greentown China in the Zhang Yadong era in the future?

01

Actually, there was a wave of sales growth for Greentown in 2016.

In 2017 and 2018, the sales of investment projects exceeded 100 billion yuan.

According to the normal carryover, most of the projects carried forward in 2019 were projects in 2016 and 2017. The performance of Greentown in 2019 should be good.

Actually, the good news of Greentown China’s annual report is indeed obvious.

Sales performance has increased sharply, and Greentown China is accelerating to cover short positions in 2019.

According to the annual report, the Group has 54 new projects in 2019 with a total construction area of approximately 12.36 million square meters; the total land cost / acquisition amount is 69.1 billion yuan; the estimated new saleable amount is 205.7 billion yuan, creating Greentown China New historical record value of new investment, which is attributable toGroup equity is about 108.6 billion yuan.

The core net profit attributable to the parent is RMB 4.336 billion, with a dividend of RMB 0.3 per share, or approximately HKD 0.33.

The net asset-liability ratio is 63%, and the weighted average interest cost of total borrowings is 5.3%.

There has also been significant progress in cost control and efficiency improvement, with a significant increase in per capita efficiency. Selling expenses are controlled at 1.8%. The target of 1.6% this year is already high in the industry.

Revenue, land reserves, and total assets are increasing. It is rare to trade and remove products. Rarely, cost control has begun to emerge.

This shows that in terms of operation and management, Greentown has begun to go on track.

But perpetual debt eats up a lot of profits. Greentown’s income is increased but not increased. The core net profit and shareholders’ net profit are very different. The land price is higher later, but I am afraid that the profit will not be seen.

Perpetual bonds are nominally “debts”, but they can be included in equity instead of liabilities. This feature makes housing enterprises keen to issue such bonds, which can modify the financial statements of the enterprise to a certain extent and reduce the asset-liability ratio.

But in fact, perpetual debt has caused the real estate enterprises’ leverage to rise to a certain extent. Including equity, perpetual debt can continue to share the profits of the enterprise, becoming a “black hole” that eats up the profits of the housing enterprises.

Greentown’s perpetual debt is a thorn in the minds of small and medium shareholders.

Greentown issued USD 500 million perpetual bonds in 2014; issued USD 400 million perpetual bonds on April 22, 2016; issued USD 450 million perpetual bonds on July 19, 2017, and issued December 28, 2018 500 Million USD Perpetual Bonds ……… p

In 2019, Greentown’s perpetual debt liabilities totaled 21.23 billion yuan, of which 1.286 billion yuan was the interest expense on perpetual bonds.

It is this 1.286 billion yuan perpetual debt interest support that has swallowed the profit attributable to shareholders. Shareholder profits of 2.48 billion yuan ended up with only 1.193 billion yuan.

Knowing that the poison is still insisting on eating, Greentown’s perpetual debt expansion has puzzled investors.

“Why isn’t a company good at expanding and aggressive? Why do you have so many perpetual bonds? Isn’t it flexible to add debt?” The investor complained quite puzzled.

Only from the land acquisition dynamics of Greentown at the beginning of this year, Greentown, which is not indifferent, is afraid that it has already started an aggressive mode. Just how to deal with perpetual debt in the process of scale expansion? How to better handle the non-conflicts between the growth of scale and the interests of shareholders? For Greentown, this is not a trivial matter.

02

For many investors, seeing the impairment of Greentown’s 2019 annual report is another thunder.

To accrue asset impairment, it means that from a prudent perspective, these things need to assess possible losses, and calculate the possible losses, and then treat them as losses, which is a hypotheticalThe loss may or may not be realized, but careful consideration must be prepared.

This time, the asset impairment of various projects of Greentown’s one-off loss was close to 1.4 billion, plus a hotel with nearly 1.5 billion asset impairment.

For many investors, the main reason for asset impairment is more, at least this year should not be asset impairment. Assets have been impaired for three consecutive years, and outside expectations are that asset impairment is basically complete.

For many investors, the Wuhan and Foshan areas of the new project are expensive, and it is understandable that they can’t buy the value and lose value. In Tianjin Quanyun Village and Shenyang Quanyun Village, the old project is still impaired at this stage. The holes in the old project should have been impaired now, and it is really a test of patience.

If it is the three previous asset impairments, Greentown can be said to have not released its profits. This year, it may be difficult to convince the public. Just three things will only make people worry about whether the profits can be released as scheduled.

Moreover, it doesn’t matter if you make a little more provision when the situation is good, and you increase it when the situation is bad.

At the performance meeting in the afternoon, the management’s response to the question about “storm and thunder” in asset impairment losses was in accordance with the policy of the meeting, which was compliant and conservative.

Regarding whether the impairment will continue to be accrued in the future, it is only said that it will continue to follow up and evaluate based on market changes. Some people interpret this subtext to estimate that it is likely to continue to accrue losses next time.

But Zhang Yadong also emphasized a point at the performance meeting that he must grasp profits in 2020. It is optimistic that this may mean that the impairment should be reduced, and profits will start to be released in 2020.

Whether the situation of Greentown’s income increase or not can be changed, wait and see.

03

At the performance meeting, Zhang Yadong proposed that “the sales scale will reach 500 billion yuan by 2025.”

According to Zhang Yadong, the goal of 500 billion yuan is broken down into two parts: the heavy asset part of traditional real estate development will achieve 350 billion yuan, and the asset light construction part will achieve 150 billion yuan.

Zhang Yadong thinks it is a very conservative goal, and you must control the speed not too fast in the later stage. Agent construction has begun to make efforts, and Green City has confirmed that it will do capital agent construction.

There are no special circumstances, and this performance is no problem.

This year, Greentown’s land purchases have confirmed the management’s determination on a large scale.

In 2011, the pace of Greentown was too big, and it was digested for several years. Later, too pessimistic, Greentown slowed down completely. Other housing companies are desperately taking land, and when they are expanding wildly, from 2011 to 2017, Greentown’s land data actually decreased.

In the first half of 2019, Greentown often even sold out of stock.

In the first two months of 2020, Greentown China acquired a total of 13 plots in 10 cities including Beijing, Hangzhou, Chengdu, Dalian, Wenzhou, and Tianjin, with a cumulative equity construction area of 1.84 million square meters and equity investment of 26.77 billion yuan. The estimated value is 58.56 billion yuan.

In addition, people familiar with the matter said that today Greentown is still eager to look around and replenish the soil.

Obviously, the logic of the new management is to make Greentown bigger in order to break through.

Green City, which is a state-owned enterprise, is now facing a good window of financing, and it can be used to get land with cheaper funds.

At the 2019 interim results meeting, Zhang Yadong once said, “Give us three years, we will definitely adjust the indicators to become the industry’s top students.”

It is worth mentioning that in order to be a top student, it is not only the scale, the income, but also the true net profit rate.