Since it is a “new” infrastructure, how can we not fall into the stereotype of “building piles”?

Editor’s note: This article comes from the WeChat public account “Smart Relativity (ID: aixdlun) author: Weiqi Yang

Looking for the stars and the moon, the charging pile industry finally got the “Shangfang Sword” from the national strategic level to promote development.

The Standing Committee of the Political Bureau of the Central Committee of the Communist Party of China clearly stated on March 4 that it is necessary to speed up the major projects and infrastructure constructions that have been identified in the national plan. New energy charging piles are listed among the seven major areas of new infrastructure that are subsequently announced. .

How encouraged are industries and capital markets?

In the five trading days after the announcement of the new infrastructure policy, the flush pile index of the Flush has increased by 7.25%.

In another dimension, the second day after the announcement of the policy, the charging head companies announced that they would receive a round of investment of about 1.35 billion yuan jointly led by the State Investment Fund, Guoxin Capital and CDH Investment. .

Undoubtedly, under the tuyere of new infrastructure, the new energy charging pile industry will undoubtedly usher in a wave of dividends, and the industry will therefore catch the express train of high-speed development. It is also because of this wave of dividends that it will also Speed up the shuffle of players in the industry.

I. The market looks big, but how many opportunities does it leave for future players?

What kind of blueprint does the charging pile industry under the new infrastructure air duct have?

Let’s take a look at a set of data published by CCID Consulting.

As of December 2019, the number of charging piles in China was 1.219 million, of which 516,000 were public charging piles and 703,000 were private charging piles, with a vehicle-to-pile ratio of about 3.4: 1. The 1: 1 requirements of the Development Guide (2015-2020) are quite different.

From the data in 2019 alone, there is still a lot of potential to be tapped in the charging pile industry. What makes the industry even more excited is that the “New Energy Vehicle Industry Development Plan ( (2021-2035) “(draft for comments), proposing that by 2025 new energy vehicles will account for about 25% of new vehicle sales.

From this calculation, if we want to achieve a 1: 1 car-to-pile ratio, there will be a gap of 63 million in the construction of charging piles in the next 10 years, and this is a trillion-scale infrastructure construction market.

Data source: CCID consultants

In fact, the tuyere of the charging station is always there.

In July 2012, the State Council issued the “Development Plan for Energy Conservation and New Energy Vehicle Industry”, announcing that it will be driven by pure electric power as the main strategic direction for the development of new energy vehicles and the transformation of the automotive industry. With the drive of new energy vehicle industry, charging The pile industry flooded a large number of players at that time.

According to incomplete statistics, in the first half of 2017, the number of charging pile companies in China reached a peak, exceeding 1,000. However, because charging piles are an asset-heavy industry, before the penetration rate of new energy vehicles is low and the utilization rate of charging piles has not reached a certain level, all companies in the industry will face living pressure from the financial level, so most of them Enterprises did not wait for the dividends distributed by the new infrastructure to “fall down” halfway.

As of the end of 2019, there are only more than 100 surviving charging pile companies in the country today, and the elimination rate is as high as 90%.

Generally speaking, the higher the risk, the greater the return. Does this mean that as long as you have enough courage and determination to “live to death”, you can still get a dividend in the charging pile market?

In terms of the current market structure, the charging pile market has not yet been finalized, but like the industry competition in gas stations, the charging pile market has begun to show a trend of oligopoly concentration.

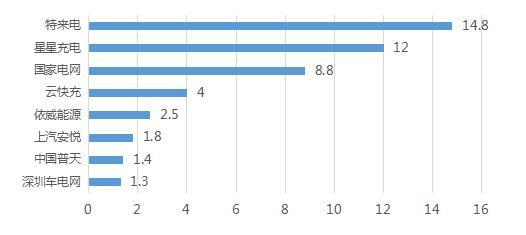

It is also the data from CCID Consulting. As of December 2019, the top 8 charging operation companies accounted for more than 90% of the current total charging piles. In particular, the three enterprises, namely special telephone, Xingxing Charging and State Grid, have established certain competitive advantages and barriers in market enclosure.

The scale of charging operation companies with a total of more than 10,000 units (Unit: 10,000 units) Data source: CCID Consulting

It must be clear that, in addition to the characteristics of the industry mentioned above, as part of the energy sector, the charging pile industry must also be connected to the grid. Therefore, at the national level, it must have very strong control over the charging pile. It also promoted the industry to a certain extent.

Look at the top three companies in terms of market shareThe background of the industry can be seen.

The two companies led by the A round of investment are state-adjusted funds and Guoxin Capital. The former is supported by the State-owned Assets Supervision and Administration Commission of the State Council, which mainly supports central enterprises and state-owned backbone enterprises in industrial layout optimization, transformation and upgrading, and specialization Integration, international operation and other projects; the latter is performed by the State-owned Assets Supervision and Administration Commission of the State Council as investor, and also has a very strong official background.

Tianyancha’s information shows that the main investor of Xingxing Charging is CDB Development Fund, which is a policy investment entity registered and set up by the China Development Bank and mainly supports the construction of key areas identified by the state. As for the national grid, it is a proper “national team.”

Apart from the above-mentioned companies, the ranking of the first echelon is relatively stable, and the competition of the second echelon that can be on the list is much fiercer. In 2018, players such as BYD, China Southern Power Grid, Zhejiang Wanma, and Spruce Wisdom have also been included in the list. After 2019, the players in the second echelon have almost changed.

Another noteworthy data. After Tesla entered China, it began to deploy supercharging piles before the Shanghai factory was completed. As of January 2019, the number of Tesla’s public charging piles reached 1,540. At that time, It has already surpassed BYD to become the second largest car charging operator in China after SAIC Anyue.

If you carefully consider domestic charging pile players, you can divide them into three forces: one is a private private enterprise group with official capital support, which is composed of special calls and star charging; the other is national power grid, China Putian, and South China State-owned electric power companies represented by the power grid; third, auto companies that sell new energy vehicles such as SAIC, BYD, and Tesla.

Is this picture of the competition in the charging pile industry under the new infrastructure tuyere very similar to the pattern of gas stations? A few giant “national font” players occupy the vast majority of market share, and a few strong private enterprises serve as “embellishments”.

Second, since it is a “new” infrastructure, how can it not fall into the habit of just “building piles”?

Put aside complex commercial competition, and look at the “new infrastructure” of charging piles from the perspective of meeting the needs of the development of new energy vehicles. How should they be built?

If you continue to use traditional infrastructure thinking, it is nothing more than seeing stitches and building piles in enclosures. It is expected that in the future, the state’s new energy subsidy policy or the gradual shift from new energy vehicles to the field of charging piles. If local governments do not have accurate insights and predictions, the construction of charging piles with the name of “new infrastructure” will fall again The “old infrastructure” stereotype.

Many experts believe that the new infrastructure of charging piles is mainly “new” in the evolution from a single independent charging pile to an interconnected charging network. There are three aspects that need to be refreshed at the cognitive level.

First, the value of charging piles is not in building piles, but in industrial ecology and operations.

Although all of them provide charging services, what the gas station presents to us is a three-dimensional and rich industrial ecology. Gas stations are usually equipped with convenience stores, car maintenance stations, entertainment facilities, and even outdoor billboards. It can be said that every contact in car life can be found in gas stations.

Compared to the value that can be generated by the one-time investment of building piles, the direction of charging piles is obviously to establish a vibrant industrial ecology. In addition to the daily entertainment and entertainment activities in the process of waiting for charging, we can even imagine that through charging In addition to charging the vehicle, the pile’s energy storage equipment sells electricity to the grid under the regulation of the market at the peak of electricity consumption.

To achieve the above, it will test the operating ability of charging pile companies, that is, to increase the utilization rate of charging piles in various ways and grasp the big heads in the industrial chain.

In fact, the industry has already done something here.

In November last year, head charging companies such as State Grid, China Southern Power Grid, Special Caller, and Wanbang New Energy jointly established Lianhe Technology and launched the Lianyi Yichong App. In addition to more than 100 charging pile operators such as Chengwanchong and Zhuhai Yilian, they have also established cooperation with new energy OEMs such as GAC New Energy, Byton, BAIC New Energy, BYD, Weimar, and Nezha Automobile. .

According to the announcement, at that time, the total number of charging piles connected to the Unibank Yichong App reached 390,000, accounting for 85% of the country’s total charging piles.

Secondly, the operation of the charging pile is a table, and the value of mining data is miles.

In the Internet industry, those who get data win the world.

Following this thinking, although the charging pile is not the Internet industry, due to the large amount of charging data generated in the charging pile, this has also become an extremely valuable asset for charging pile enterprises.

Imagine if the charging behavior of new energy vehicles makes it easy to obtain the battery information and data of new energy vehicles, the user ’s car habits, and further, you can even grasp the distribution of the vehicles. If you analyze these data in depth, And excavation, in the evaluation of used cars, battery and new energy vehicle technology upgrades, consumer consumer portraits, commercial layout and other after-market services are promising, which will also provide new value for the charging pile industry.

Finally, we must attach importance to software thinking in the operation and maintenance of the charging pile network.

Different from the operation mode of gas stations, most of the charging piles are unattended, and users use it on their own. Therefore, this puts higher requirements on the operation and maintenance of charging piles.

Manual inspection mode may be able to cope when the number of charging piles is small. When the number of charging piles reaches one million or even ten million, a charging network needs to be managed remotely using the cloud platform. This is not only a method to improve operation and maintenance efficiency, but also a necessary means to ensure that the charging network can operate normally. Especially the cloudThe combination of the platform and daily operations can better bring out the overall value of the charging network.

Summary: Although in the construction and operation of charging piles, the current trend is that the market is gradually concentrated, eventually the remaining players will be only a few leading companies, and small and medium players seem to be able to share a small amount of dividends. However, in fact, from the perspective of industrial ecology, any enterprise cannot complete the entire industrial chain. Therefore, whether it is the upstream charging pile equipment manufacturing, the midstream construction and operation ecology, or the downstream cloud control platform and offline maintenance There are still many opportunities for operation. There is only one problem for small and medium-sized enterprises and entrepreneurs-how to get stuck.

Put aside complex commercial competition, and look at the “new infrastructure” of charging piles from the perspective of meeting the needs of the development of new energy vehicles. How should they be built?

If you continue to use traditional infrastructure thinking, it is nothing more than seeing stitches and building piles in enclosures. It is expected that in the future, the state’s new energy subsidy policy or the gradual shift from new energy vehicles to the field of charging piles. If local governments do not have accurate insights and predictions, the construction of charging piles with the name of “new infrastructure” will fall again The “old infrastructure” stereotype.

Many experts believe that the new infrastructure of charging piles is mainly “new” in the evolution from a single independent charging pile to an interconnected charging network. There are three aspects that need to be refreshed at the cognitive level.

First, the value of charging piles is not in building piles, but in industrial ecology and operations.

Although all of them provide charging services, what the gas station presents to us is a three-dimensional and rich industrial ecology. Gas stations are usually equipped with convenience stores, car maintenance stations, entertainment facilities, and even outdoor billboards. It can be said that every contact in car life can be found in gas stations.

Compared to the value that can be generated by the one-time investment of building piles, the direction of charging piles is obviously to establish a vibrant industrial ecology. In addition to the daily entertainment and entertainment activities in the process of waiting for charging, we can even imagine that through charging In addition to charging the vehicle, the pile’s energy storage equipment sells electricity to the grid under the regulation of the market at the peak of electricity consumption.

To achieve the above, it will test the operating ability of charging pile companies, that is, to increase the utilization rate of charging piles in various ways and grasp the big heads in the industrial chain.

In fact, the industry has already done something here.

In November last year, head charging companies such as State Grid, China Southern Power Grid, Special Caller, and Wanbang New Energy jointly established Lianhe Technology and launched the Lianyi Yichong App. In addition to more than 100 charging pile operators such as Chengwanchong and Zhuhai Yilian, they have also established cooperation with new energy OEMs such as GAC New Energy, Byton, BAIC New Energy, BYD, Weimar, and Nezha Automobile. .

According to the announcement, at that time, the total number of charging piles connected to the Unibank Yichong App reached 390,000, accounting for 85% of the country’s total charging piles.

Secondly, the operation of the charging pile is a table, and the value of mining data is miles.

In the Internet industry, those who get data win the world.

Following this thinking, although the charging pile is not the Internet industry, due to the large amount of charging data generated in the charging pile, this has also become an extremely valuable asset for charging pile enterprises.

Imagine if the charging behavior of new energy vehicles makes it easy to obtain the battery information and data of new energy vehicles, the user ’s car habits, and further, you can even grasp the distribution of the vehicles. If you analyze these data in depth, And excavation, in the evaluation of used cars, battery and new energy vehicle technology upgrades, consumer consumer portraits, commercial layout and other after-market services are promising, which will also provide new value for the charging pile industry.

Finally, we must attach importance to software thinking in the operation and maintenance of the charging pile network.

Different from the operation mode of gas stations, most of the charging piles are unattended, and users use it on their own. Therefore, this puts higher requirements on the operation and maintenance of charging piles.

Manual inspection mode may be able to cope when the number of charging piles is small. When the number of charging piles reaches one million or even ten million, a charging network needs to be managed remotely using the cloud platform. This is not only a method to improve operation and maintenance efficiency, but also a necessary means to ensure that the charging network can operate normally. Especially the cloudThe combination of the platform and daily operations can better bring out the overall value of the charging network.

Summary: Although in the construction and operation of charging piles, the current trend is that the market is gradually concentrated, eventually the remaining players will be only a few leading companies, and small and medium players seem to be able to share a small amount of dividends. However, in fact, from the perspective of industrial ecology, any enterprise cannot complete the entire industrial chain. Therefore, whether it is the upstream charging pile equipment manufacturing, the midstream construction and operation ecology, or the downstream cloud control platform and offline maintenance There are still many opportunities for operation. There is only one problem for small and medium-sized enterprises and entrepreneurs-how to get stuck.

In the Internet industry, those who get data win the world.

Following this thinking, although the charging pile is not the Internet industry, due to the large amount of charging data generated in the charging pile, this has also become an extremely valuable asset for charging pile enterprises.

Imagine if the charging behavior of new energy vehicles makes it easy to obtain the battery information and data of new energy vehicles, the user ’s car habits, and further, you can even grasp the distribution of the vehicles. If you analyze these data in depth, And excavation, in the evaluation of used cars, battery and new energy vehicle technology upgrades, consumer consumer portraits, commercial layout and other after-market services are promising, which will also provide new value for the charging pile industry.