This article sorts out the corporate training model, landing pattern, head layout and change trend in the United States.

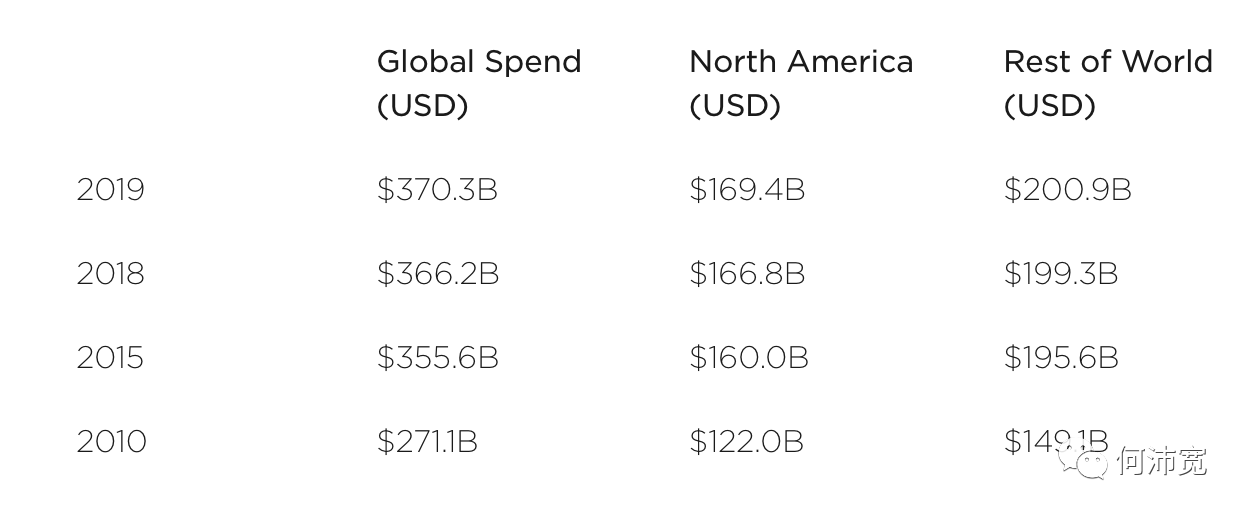

In the United States, 2019 ’s market size reaches 1694 Billions of dollars , accounting for 46% of the global market share. Technavio Research Institute forecasts, The US corporate training market will have a compound annual growth rate of more than 10% during 2019-2023 . Therefore, for the United States, the corporate training industry is still on a rising cycle. From the perspective of the primary market, several cutting-edge enterprise training (training content, services, and tool products, such as enterprise education software company lessonly and employee training company BetterUp) from 2019 to 2020 have successively obtained more than C round of financing to confirm the market growth.

How does the corporate training industry, which is a brilliant performer, land in the United States? What is the current market competition landscape (head and emerging players)? What are the industry variables and trends? For China, the statusWhat perspectives are worth learning from?

Two main functions and models of corporate training

Utility

According to Statistica research results , American companies are employees The purpose of providing enterprise training is mainly divided into two categories. One is to provide training for employees to equip them with the specific skills required to perform their duties, such as how to use the required software or manage certain types of interpersonal communication. Another category is, Learning and development includes a wider range of skills that are not necessary for employees ’workplaces.

Mode

Corresponding to utility is two modes of corporate training. One is internal training, which is provided by internal resources of the company. For external suppliers, there are more opportunities to provide tools for assisting technology and collecting feedback from students. With service support. The other is knowledge learning and training, which requires external suppliers to provide training content and services.

Training industry statistics show that in 2018, US companies are approximately 61 % Of the budget is for the first type of training, which is internal resources (including internal training personnel and other auxiliary tools and product services), 39% of the training budget is for the second type of training, namely external (outsourcing) suppliers .

Three subdivision dimensions of suppliers

A supplier that provides American companies with enterprise training products and services, currently has a relatively subdivided layout (this article will not be expanded in detail). Can follow technical courses (hard skills) and non-technical (soft skills) courses, end users (industries: manufacturing, healthcare, BFSI, IT, etc.) and learning formats (online and offline, offline And online) and other dimensions.

Among them, According to the Technavio report , in terms of form, In 2018, enterprise training combined online and offline (blended learning) leading the way, followed by offline learning and online learning (Online learning). During the forecast period, due to the lower training costs involved in the offline online learning market, it is expected that this form will maintain its dominant position in the global market and achieve the highest incremental growth-this is the same as the domestic C-end online education The trend of gradually becoming mainstream is different.

Competitive territory: major players in the market and emerging companies

Head Company

Current corporate training companies in the US include:

-

City & Guilds Group, founded in 1878 and headquartered in London (also providing services for the United States), provides professional skills certification, corporate training and electronic certification, leadership and management training services. Brand, target users include companies, government agencies and employees.

-

D2L, established in 1999, has accumulated more than 165 million US dollars in financing, providing cloud learning solutions and learning management systems for enterprise departments, governments, educational institutions, and healthcare institutions. D2L’s cloud learning solution currently has more than 700 clients (Clients) and more than 8 million learners (Users).

-

GP Strategies, which went public in 1998, provides companies with customized training, performance improvement programs, and consulting, engineering, and technical services. GP Strategies ’customized training, sales training, and performance improvement services include basic analysis of customer training needs, course design, textbook development, information technology service support, and training delivery. For the automotive, steel, oil and gas, power, chemical, electronics and technology, healthcare, food and beverage industries.

-

Skillsoft, founded in 1997, provides e-learning and training solutions for businesses, governments, and educational institutions.Skillsoft’s products include learning management platforms, virtual classroom tools, learning content centers, and courseware sets (including more than 2,000 learning topics and cases). Skillsoft was acquired for US $ 2.3 billion in 2014.

-

Wilson Learning Worldwide, established in 1965, provides learning and training solutions to improve salesperson performance and employee leadership. During its global expansion, it entered the Chinese market.

The above are relative to the head corporate training companies established before 2000 and listed. From a model point of view, there are both dedicated content training services, auxiliary tools required for internal training, or both. In a more subdivided dimension, there are those who focus on hard technology and comprehensive soft skills. In comparison, from the perspective of end customers, the industry segmentation performance is not obvious.

Senior Company

In terms of emerging companies, from the perspective of primary market financing data in recent years, worth noting include: the first mentioned in the article lessonly, BetterUp There is also the listed IT vertical training company Pluralsight. Last year, C1 and C2 rounds of financing were completed Degreed, which provides professional skills certification services for enterprises and individual learners. In addition, there is Guild Education, which has completed the D round of financing, which provides online products for enterprise employees with degree and skills training.

What is happening to American corporate training?

The head layout is the current market demand performance, the direction of change, pointing to the opportunities and adjustments of corporate training suppliers.

Enterprise training product structure: online learning tools and systems account for the highest proportion

U.S. Training magazine research shows that U.S. companies The most common purchases of corporate training products are distributed in: online learning tools and systems (41%, compared with last year ’s 40%), learning management systems (33% compared to last year ’s 39%), classroom tools and systems (with 32% compared to last year ’s 28% jumped to third place).

followed by 31% for content development, 27% for authoring tools / systems (28% last year), and 26% for certification (go(29% per year), mobile learning accounted for 24% (23% last year).

Learning mode: Microlearning (MicroLearning) is increasingly popular

Organizations are increasingly encouraging micro-learning in corporate training programs and services to ensure effective learner participation. Micro-learning is real-time content provided in the form of video and other multimedia, and employees can learn at their own speed.

There are several factors that promote the popularization of micro-learning in corporate training:

-

1) Short-term micro-learning can improve employees’ understanding of any specific concept, learning reinforcement and knowledge retention.

-

2) Micro-learning enables organizations to solve the time and resource limitations of corporate training.

-

3) The compatibility of micro-learning modules across multiple platforms and digital networks has improved knowledge sharing and peer-to-peer connections among employees.

Training form: online and offline integration into the mainstream

In terms of learning form, the hours of American employees receiving corporate training are mainly concentrated on the online and offline mixed mode, and the pure online training time is reduced.

-

About 69.3% of the company ’s employees use online learning (Blended learning) for learning hours, a significant increase from 34.7% last year. Among them, small and medium-sized companies rely on a mixed delivery method (79% and 86%, respectively) in a considerable portion of training, while large companies account for 43%.

-

25.6% of the time it was provided via online or computer technology, down from 28.6% last year.

-

1.7% of training time was provided through mobile devices, down from 3.6% in 2017.

5 trends of corporate training in the US

Over the past decade, the pattern of corporate training has changed dramatically. The next-generation enterprise management system requires employees to learn new skills. Technavio judges that enterprise training will present the following 5 trends in the future:

-

1) Artificial intelligence + corporate training, personalized learning path development

American corporate training experts are always looking for the best training materials. They are looking for learning resources such as articles, books, videos, and podcasts that have their own advantages. In the new era of personalized learning experience, enterprises

According to Statistica research results , American companies are employees The purpose of providing enterprise training is mainly divided into two categories. One is to provide training for employees to equip them with the specific skills required to perform their duties, such as how to use the required software or manage certain types of interpersonal communication. Another category is, Learning and development includes a wider range of skills that are not necessary for employees ’workplaces.

Mode

Corresponding to utility is two modes of corporate training. One is internal training, which is provided by internal resources of the company. For external suppliers, there are more opportunities to provide tools for assisting technology and collecting feedback from students. With service support. The other is knowledge learning and training, which requires external suppliers to provide training content and services.

Training industry statistics show that in 2018, US companies are approximately 61 % Of the budget is for the first type of training, which is internal resources (including internal training personnel and other auxiliary tools and product services), 39% of the training budget is for the second type of training, namely external (outsourcing) suppliers .

Three subdivision dimensions of suppliers

A supplier that provides American companies with enterprise training products and services, currently has a relatively subdivided layout (this article will not be expanded in detail). Can follow technical courses (hard skills) and non-technical (soft skills) courses, end users (industries: manufacturing, healthcare, BFSI, IT, etc.) and learning formats (online and offline, offline And online) and other dimensions.

Among them, According to the Technavio report , in terms of form, In 2018, enterprise training combined online and offline (blended learning) leading the way, followed by offline learning and online learning (Online learning). During the forecast period, due to the lower training costs involved in the offline online learning market, it is expected that this form will maintain its dominant position in the global market and achieve the highest incremental growth-this is the same as the domestic C-end online education The trend of gradually becoming mainstream is different.

Competitive territory: major players in the market and emerging companies

Head Company

Current corporate training companies in the US include:

-

City & Guilds Group, founded in 1878 and headquartered in London (also providing services for the United States), provides professional skills certification, corporate training and electronic certification, leadership and management training services. Brand, target users include companies, government agencies and employees.

-

D2L, established in 1999, has accumulated more than 165 million US dollars in financing, providing cloud learning solutions and learning management systems for enterprise departments, governments, educational institutions, and healthcare institutions. D2L’s cloud learning solution currently has more than 700 clients (Clients) and more than 8 million learners (Users).

-

GP Strategies, which went public in 1998, provides companies with customized training, performance improvement programs, and consulting, engineering, and technical services. GP Strategies ’customized training, sales training, and performance improvement services include basic analysis of customer training needs, course design, textbook development, information technology service support, and training delivery. For the automotive, steel, oil and gas, power, chemical, electronics and technology, healthcare, food and beverage industries.

-

Skillsoft, founded in 1997, provides e-learning and training solutions for businesses, governments, and educational institutions.Skillsoft’s products include learning management platforms, virtual classroom tools, learning content centers, and courseware sets (including more than 2,000 learning topics and cases). Skillsoft was acquired for US $ 2.3 billion in 2014.

-

Wilson Learning Worldwide, established in 1965, provides learning and training solutions to improve salesperson performance and employee leadership. During its global expansion, it entered the Chinese market.

The above are relative to the head corporate training companies established before 2000 and listed. From a model point of view, there are both dedicated content training services, auxiliary tools required for internal training, or both. In a more subdivided dimension, there are those who focus on hard technology and comprehensive soft skills. In comparison, from the perspective of end customers, the industry segmentation performance is not obvious.

Senior Company

In terms of emerging companies, from the perspective of primary market financing data in recent years, worth noting include: the first mentioned in the article lessonly, BetterUp There is also the listed IT vertical training company Pluralsight. Last year, C1 and C2 rounds of financing were completed Degreed, which provides professional skills certification services for enterprises and individual learners. In addition, there is Guild Education, which has completed the D round of financing, which provides online products for enterprise employees with degree and skills training.

What is happening to American corporate training?

The head layout is the current market demand performance, the direction of change, pointing to the opportunities and adjustments of corporate training suppliers.

Enterprise training product structure: online learning tools and systems account for the highest proportion

U.S. Training magazine research shows that U.S. companies The most common purchases of corporate training products are distributed in: online learning tools and systems (41%, compared with last year ’s 40%), learning management systems (33% compared to last year ’s 39%), classroom tools and systems (with 32% compared to last year ’s 28% jumped to third place).

followed by 31% for content development, 27% for authoring tools / systems (28% last year), and 26% for certification (go(29% per year), mobile learning accounted for 24% (23% last year).

Learning mode: Microlearning (MicroLearning) is increasingly popular

Organizations are increasingly encouraging micro-learning in corporate training programs and services to ensure effective learner participation. Micro-learning is real-time content provided in the form of video and other multimedia, and employees can learn at their own speed.

There are several factors that promote the popularization of micro-learning in corporate training:

-

1) Short-term micro-learning can improve employees’ understanding of any specific concept, learning reinforcement and knowledge retention.

-

2) Micro-learning enables organizations to solve the time and resource limitations of corporate training.

-

3) The compatibility of micro-learning modules across multiple platforms and digital networks has improved knowledge sharing and peer-to-peer connections among employees.

Training form: online and offline integration into the mainstream

In terms of learning form, the hours of American employees receiving corporate training are mainly concentrated on the online and offline mixed mode, and the pure online training time is reduced.

-

About 69.3% of the company ’s employees use online learning (Blended learning) for learning hours, a significant increase from 34.7% last year. Among them, small and medium-sized companies rely on a mixed delivery method (79% and 86%, respectively) in a considerable portion of training, while large companies account for 43%.

-

25.6% of the time it was provided via online or computer technology, down from 28.6% last year.

-

1.7% of training time was provided through mobile devices, down from 3.6% in 2017.

5 trends of corporate training in the US

Over the past decade, the pattern of corporate training has changed dramatically. The next-generation enterprise management system requires employees to learn new skills. Technavio judges that enterprise training will present the following 5 trends in the future:

-

1) Artificial intelligence + corporate training, personalized learning path development

American corporate training experts are always looking for the best training materials. They are looking for learning resources such as articles, books, videos, and podcasts that have their own advantages. In the new era of personalized learning experience, enterprises

Head Company

Current corporate training companies in the US include:

-

City & Guilds Group, founded in 1878 and headquartered in London (also providing services for the United States), provides professional skills certification, corporate training and electronic certification, leadership and management training services. Brand, target users include companies, government agencies and employees.

-

D2L, established in 1999, has accumulated more than 165 million US dollars in financing, providing cloud learning solutions and learning management systems for enterprise departments, governments, educational institutions, and healthcare institutions. D2L’s cloud learning solution currently has more than 700 clients (Clients) and more than 8 million learners (Users).

-

GP Strategies, which went public in 1998, provides companies with customized training, performance improvement programs, and consulting, engineering, and technical services. GP Strategies ’customized training, sales training, and performance improvement services include basic analysis of customer training needs, course design, textbook development, information technology service support, and training delivery. For the automotive, steel, oil and gas, power, chemical, electronics and technology, healthcare, food and beverage industries.

-

Skillsoft, founded in 1997, provides e-learning and training solutions for businesses, governments, and educational institutions.Skillsoft’s products include learning management platforms, virtual classroom tools, learning content centers, and courseware sets (including more than 2,000 learning topics and cases). Skillsoft was acquired for US $ 2.3 billion in 2014.

-

Wilson Learning Worldwide, established in 1965, provides learning and training solutions to improve salesperson performance and employee leadership. During its global expansion, it entered the Chinese market.

The above are relative to the head corporate training companies established before 2000 and listed. From a model point of view, there are both dedicated content training services, auxiliary tools required for internal training, or both. In a more subdivided dimension, there are those who focus on hard technology and comprehensive soft skills. In comparison, from the perspective of end customers, the industry segmentation performance is not obvious.

Senior Company

In terms of emerging companies, from the perspective of primary market financing data in recent years, worth noting include: the first mentioned in the article lessonly, BetterUp There is also the listed IT vertical training company Pluralsight. Last year, C1 and C2 rounds of financing were completed Degreed, which provides professional skills certification services for enterprises and individual learners. In addition, there is Guild Education, which has completed the D round of financing, which provides online products for enterprise employees with degree and skills training.

What is happening to American corporate training?

The head layout is the current market demand performance, the direction of change, pointing to the opportunities and adjustments of corporate training suppliers.

Enterprise training product structure: online learning tools and systems account for the highest proportion

U.S. Training magazine research shows that U.S. companies The most common purchases of corporate training products are distributed in: online learning tools and systems (41%, compared with last year ’s 40%), learning management systems (33% compared to last year ’s 39%), classroom tools and systems (with 32% compared to last year ’s 28% jumped to third place).

followed by 31% for content development, 27% for authoring tools / systems (28% last year), and 26% for certification (go(29% per year), mobile learning accounted for 24% (23% last year).

Learning mode: Microlearning (MicroLearning) is increasingly popular

Organizations are increasingly encouraging micro-learning in corporate training programs and services to ensure effective learner participation. Micro-learning is real-time content provided in the form of video and other multimedia, and employees can learn at their own speed.

There are several factors that promote the popularization of micro-learning in corporate training:

-

1) Short-term micro-learning can improve employees’ understanding of any specific concept, learning reinforcement and knowledge retention.

-

2) Micro-learning enables organizations to solve the time and resource limitations of corporate training.

-

3) The compatibility of micro-learning modules across multiple platforms and digital networks has improved knowledge sharing and peer-to-peer connections among employees.

Training form: online and offline integration into the mainstream

In terms of learning form, the hours of American employees receiving corporate training are mainly concentrated on the online and offline mixed mode, and the pure online training time is reduced.

-

About 69.3% of the company ’s employees use online learning (Blended learning) for learning hours, a significant increase from 34.7% last year. Among them, small and medium-sized companies rely on a mixed delivery method (79% and 86%, respectively) in a considerable portion of training, while large companies account for 43%.

-

25.6% of the time it was provided via online or computer technology, down from 28.6% last year.

-

1.7% of training time was provided through mobile devices, down from 3.6% in 2017.

5 trends of corporate training in the US

Over the past decade, the pattern of corporate training has changed dramatically. The next-generation enterprise management system requires employees to learn new skills. Technavio judges that enterprise training will present the following 5 trends in the future:

-

1) Artificial intelligence + corporate training, personalized learning path development

American corporate training experts are always looking for the best training materials. They are looking for learning resources such as articles, books, videos, and podcasts that have their own advantages. In the new era of personalized learning experience, enterprises

-

-

-