Perspective industry trend ID: Xinfinance).

In the “asset shortage” in 2020, operational experience, technical level, and ability to counter risks are becoming “hard currencies” for fintech platforms.

—— Xin Finance

Hong Yuxin, Yi Lei / Wen

The epidemic period hit the financial reporting season, and the pressure of listed companies seems to be even greater.

Recently, the stocks of FinTech have successively disclosed the fourth quarter and full year 2019 financial reports. Unsurprisingly, under the dual pressures of tightened regulation in 2019 and intensified industry competition, the performance of listed companies has once again diverged.

Among them, platforms that have accelerated their transformation to the loan-assistance model and expanded the proportion of institutional funds in the past two years have further stabilized their head positions.

Especially the two companies 360 Finance and Lexin, whose annual matching loan amount exceeded the 100 billion mark, of which the growth momentum of the former has already pointed directly to 200 billion. The rapid growth of business volume has also brought advantages in financial performance. According to the financial report, the two platforms ranked first and second in terms of revenue in 2019.

At the same time, those platforms that have always been unable to give up on P2P or have a slower transition are not so lucky. The pitiful P2P “first-share” pleasant loan and the 51 credit card that encountered the door-to-door investigation are all facing a decline in performance and even huge losses.

2019 is already a big challenge for listed companies, and the outbreak in 2020 will make the situation even more serious.

The business shutdown and overdue rise in the first quarter have been expected, but in the long run, whether the platform itself can indigest, manage risks, and adjust strategies in a timely manner to adapt to the special development environment is a huge challenge.

More importantly, rising industry risks may cause financial institutions to become more cautious in external cooperation, which will also make it more difficult for fintech companies to develop.

However, every “crisis” in the industry can always force out “opportunities”. In the special environment shaped by the epidemic, the looseness of funds and the scarcity of high-quality assets exist at the same time, which may create head institutions More space. Under the epidemic, financial institutions will increase their investment in financial technology, and some platforms with technological capabilities may also usher in a real “outbreak period.”

1

Intensified industry differentiation

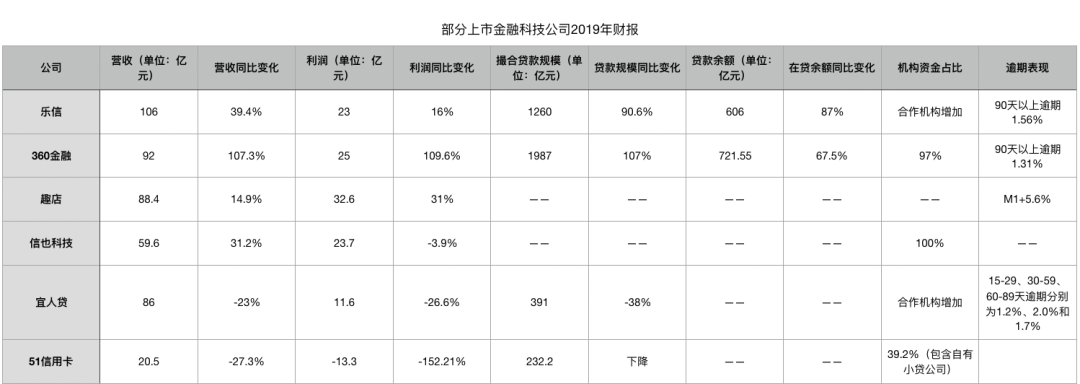

This may be one of the earnings seasons with the most obvious performance differentiation.The gap between the scale of business and the scale of income, and this time, the differentiation between growth and decline, profit and loss, and asset quality has become more distinct.

Click to view the big picture in high definition

In terms of financial performance, Lexin, 360 Finance and Qudian have maintained a large advantage. Among them, Lexin achieved the largest revenue in 2019, with a total amount of 10.6 billion yuan; and in terms of profit, Fun Store ranked first again with 3.26 billion, continuing to write the myth of “money printing machine”.

Although 360 Finance ranks second in these two terms, it is rare that this company’s revenue and profits have increased by more than 100% over the previous year, and 360 Finance is also The only company with a three-digit growth rate . In 2019, when industry pressure continues to increase, it is not easy to maintain such growth.

The changes in financial indicators reflect the trend of business changes. In comparison, 360 Finance’s matching loan scale reached 198.7 billion yuan in 2019, ranking first among all listed platforms, and its loan balance climbed to 72.155 billion yuan. These two figures increased by 107% and 67.5% respectively from the previous year.

In terms of business growth, Lexin followed closely, with a matching loan size of 126 billion yuan in 2019, an increase of 90.6% year-on-year; the loan balance increased 87% year-on-year to 60.6 billion yuan. In comparison, Qudian seems to be hesitating, especially in the fourth quarter, the open platform loan volume promoted by Qudian has decreased by 20%, and revenue has dropped by 34.6%.

In addition, another data also confirmed the difference in the growth rate of the business of the head platforms.

In terms of registered users, the registered users of 360 Finance increased from 95.08 million in the first quarter of last year to 135 million at the end of the year, an increase of 71.3% year-on-year; during the same period, the number of registered users of Lexin increased from 42.2 million to 7330 Ten thousand people also maintained a double-digit growth rate. Qudian’s total number of users grew less than 8 million in the past year, and the number of registered users in the fourth quarter dropped to 1.48% year-on-year.

Although the growth performance is different, the characteristics of the three head platforms are that they started the transition to the loan-assistance model earlier or started with the loan-assistance model themselves. In a turbulent industry environment, no matter Both the business model and the source of funds were kept stable.

Among them, 360 Finance disclosed in the financial report that as of the fourth quarter of 2019, the platform ’s institutional fundsThe proportion reached 97%.

In addition, last year ’s decision to completely abandon P2P and decide to change its name, “Xin Ye Technology” also mentioned in the financial report that its institutional funds as of the fourth quarter of 2019 have reached 100%. The data shows that Xinye Technology achieved a net profit of 2.37 billion yuan in 2019. Although it has declined from the previous year, it has maintained stable development in a volatile industry environment.

In comparison, the other two platforms that are still fighting with P2P in 2019 are not performing well. As the “P2P first share” of Yirendai, after undergoing business integration in the past year, it will I hope that the wealth management business will not turn around.

The 51 credit card ushered in the first loss-making financial year after listing after the “1021” incident (Note: 51 credit card was investigated for violations of outsourcing collection business)-due to the reduction in loan size and rising default risk, the loss during the year exceeded 1.3 billion. It is worth noting that, after announcing the withdrawal from the P2P business, 51 Credit Card also announced that it will be overweighted as a financial management business, which will guide the bank’s financial management.

2

Funding ability “breakout”

It is worth noting that although we have previously discussed the issue of the source of institutional funds, especially the increase in the “quantity” of institutional funds, more of it stayed in the circumvention of P2P industry risks and business stability.

However, in 2019, Institutional capital cooperation in terms of “quality” improvement, may bring greater advantages to the head platform.

For example, as a company that has always used institutional funds as its main source, as of now, the proportion of institutional funds for 360 financial cooperation has reached 97%, and the number of cooperative institutions has exceeded 90, including large commercial banks and joint-stock banks. , City commercial banks, trust companies and consumer finance companies, cooperative institutions covering most of the provinces in China.

In other words, 360 Finance has established an absolute advantage in the “quantity” of institutional cooperation, and the significance of further improvement is actually not significant.

However, Citi Securities mentioned in a recent research report on 360 Finance that the capital cost of 360 Finance fell from 8.4% to 8.0% in the third quarter to the fourth quarter of 2019, and before In the first quarter of this year, its capital cost was as high as 9.3%. In 2020, this data is expected to be further reduced to 7.5%.

For the entire lending industry, under such a large volume, each bp (basis point, equivalent to 0.01 percentage point) of capital cost fluctuations will have a huge impact on the final income and profit of the platform. This explains from another dimension why 360 Finance is able to achieve peak revenue and profit growth in 2019.

More importantly, the reduction in capital costs can further enhance its competition on the user sideCompetitiveness, based on its huge customer base, provides differentiated pricing services.

Citigroup mentioned in the aforementioned research report that there are three key points to further reduce the cost of 360 financial funds in 2020. One is the lack of high-quality assets in financial institutions during the credit down cycle; the second is the further increase in the scale of ABS issuance; Monetary policy.

This is actually not difficult to understand. Under the influence of the epidemic, the world has entered a cycle of interest rate cuts, the domestic market is relatively loose, and funds are rushing into the market eagerly. However, the epidemic in the first quarter prevented most banking financial institutions from achieving a “starter” and the pressure on performance further increased.

On the other hand, the rising risk of the industry from 2019 has made financial institutions more cautious. A case that can be corroborated is that the recent financial report disclosed by PICC P & C revealed that its 2019 credit guarantee insurance business suffered a loss of 2.884 billion yuan, which is still the case for the leading domestic property insurance company. The pressure on the entire industry can be imagined .

Under such a background, high-quality assets become more scarce and precious in 2020, Whether it is the direct credit of the institution or the purchase of ABS products, financial institutions are willing to further reduce the price of funds, which is insufficient. It’s strange.

In fact, looking back on 2019, there are only six ABS internet platforms that issue cash instalment assets, all concentrated in the head institutions-Ant, JD, Du Xiaoman, Xiaomi, Meituan, and 360 Finance, which itself is also The result of market selection.

In addition, 360 Finance mentioned in its financial report that in the fourth quarter of last year, the proportion of its “capital-light” (light asset model) in matched loans has risen from 0.8% in the first quarter of 2019 to four 22% of the quarter. 360 is expected that in 2020, this proportion will be further increased to 30-40%.

The so-called “capital-light” model means that the platform does not take risks at all, but earns the cost of providing customers with services such as customer acquisition and risk control. This is to some extent an evolution of the fintech to B model. Fintech companies truly provide technical services to institutions to help them build capabilities.

From a certain perspective, the epidemic may promote the development of this part of the business.

The root cause is that the special industry environment brought by the epidemic makes banks more urgently realize the importance of becoming a “contactless bank” and developing financial technology. Whether from the perspective of acquiring scarce assets or building capabilities, the epidemic is “Forcing” financial institutions and fintech companies to establish a closer and deeper connection.

It is worth noting that although we have previously discussed the issue of the source of institutional funds, especially the increase in the “quantity” of institutional funds, more of it stayed in the circumvention of P2P industry risks and business stability.

However, in 2019, Institutional capital cooperation in terms of “quality” improvement, may bring greater advantages to the head platform.

For example, as a company that has always used institutional funds as its main source, as of now, the proportion of institutional funds for 360 financial cooperation has reached 97%, and the number of cooperative institutions has exceeded 90, including large commercial banks and joint-stock banks. , City commercial banks, trust companies and consumer finance companies, cooperative institutions covering most of the provinces in China.

In other words, 360 Finance has established an absolute advantage in the “quantity” of institutional cooperation, and the significance of further improvement is actually not significant.

However, Citi Securities mentioned in a recent research report on 360 Finance that the capital cost of 360 Finance fell from 8.4% to 8.0% in the third quarter to the fourth quarter of 2019, and before In the first quarter of this year, its capital cost was as high as 9.3%. In 2020, this data is expected to be further reduced to 7.5%.

For the entire lending industry, under such a large volume, each bp (basis point, equivalent to 0.01 percentage point) of capital cost fluctuations will have a huge impact on the final income and profit of the platform. This explains from another dimension why 360 Finance is able to achieve peak revenue and profit growth in 2019.

More importantly, the reduction in capital costs can further enhance its competition on the user sideCompetitiveness, based on its huge customer base, provides differentiated pricing services.

Citigroup mentioned in the aforementioned research report that there are three key points to further reduce the cost of 360 financial funds in 2020. One is the lack of high-quality assets in financial institutions during the credit down cycle; the second is the further increase in the scale of ABS issuance; Monetary policy.

This is actually not difficult to understand. Under the influence of the epidemic, the world has entered a cycle of interest rate cuts, the domestic market is relatively loose, and funds are rushing into the market eagerly. However, the epidemic in the first quarter prevented most banking financial institutions from achieving a “starter” and the pressure on performance further increased.

On the other hand, the rising risk of the industry from 2019 has made financial institutions more cautious. A case that can be corroborated is that the recent financial report disclosed by PICC P & C revealed that its 2019 credit guarantee insurance business suffered a loss of 2.884 billion yuan, which is still the case for the leading domestic property insurance company. The pressure on the entire industry can be imagined .

Under such a background, high-quality assets become more scarce and precious in 2020, Whether it is the direct credit of the institution or the purchase of ABS products, financial institutions are willing to further reduce the price of funds, which is insufficient. It’s strange.

In fact, looking back on 2019, there are only six ABS internet platforms that issue cash instalment assets, all concentrated in the head institutions-Ant, JD, Du Xiaoman, Xiaomi, Meituan, and 360 Finance, which itself is also The result of market selection.

In addition, 360 Finance mentioned in its financial report that in the fourth quarter of last year, the proportion of its “capital-light” (light asset model) in matched loans has risen from 0.8% in the first quarter of 2019 to four 22% of the quarter. 360 is expected that in 2020, this proportion will be further increased to 30-40%.

The so-called “capital-light” model means that the platform does not take risks at all, but earns the cost of providing customers with services such as customer acquisition and risk control. This is to some extent an evolution of the fintech to B model. Fintech companies truly provide technical services to institutions to help them build capabilities.

From a certain perspective, the epidemic may promote the development of this part of the business.

The root cause is that the special industry environment brought by the epidemic makes banks more urgently realize the importance of becoming a “contactless bank” and developing financial technology. Whether from the perspective of acquiring scarce assets or building capabilities, the epidemic is “Forcing” financial institutions and fintech companies to establish a closer and deeper connection.