Open Source and Throttling

Shenyi Translation Bureau is its compilation team, focusing on technology, business, workplace, life and other fields, focusing on introducing foreign new technologies, new ideas, and new trends.

Editor’s note: If you want to increase your wealth, in addition to open source, you need to minimize expenses. This article is translated from Medium, author Carter Kilmann, the original title How I Cut My Monthly Expenses by 32%.

From January 2018 to June 2019, my average monthly expenditure was $ 3484. At the time, I worked in corporates and investment banks, working 70-80 hours a week. Since the work leaves me little free time, I do n’t have much control over my financial situation. But the point is, my monthly expenditure budget is only $ 2935. So on average, I will exceed the budget by $ 549 per month. This expenditure definitely makes you feel confident in my income, right?

Listen to me and explain why I need to reduce expenditure.

Working in an investment bank is very physical and energy intensive, but it is undeniable that the salary is high, and I can basically predict how much I can get this month. But I have to say that spending $ 3484 a month actually lowers my efficiency in making money. This is not wise at all. I hope I can save more.

Due to various reasons, I quit my job as an investment bank in July 2019 and worked full-time as a freelance writer. My income was hit hard.

This does not surprise me. I know what the departure will bring to myself. I do n’t expect to maintain my previous lifestyle, nor do I have a stable salary. Therefore, in order to reduce the impact of lower income on me, I had to adjust the budget.

At this point, I ’ve made intermittent budgets for several years, so I do n’t need to start from scratch. I opened my budget table, carefully reviewed each expenditure category, carefully considered my needs, and deleted some of the budget … In the end, I set a monthly expenditure budget of 2275 US dollars. In other words, I stipulate that I will reduce the average monthly expenditure in the future by 1209 US dollars over the past 18 months.yuan.

It is not easy to reduce expenditures. I need to check each expenditure to determine which expenditures are necessary. For me, it is the most important thing to maximize the opportunities for my professional success. To do this, I must make sacrifices.

If you want to control your financial situation, you still have to open source and cut costs, first of all you have to find ways to increase your income, and second, you can also cut costs. The steps I introduced are simple, clear, and operable, and can help you reduce your monthly expenses.

Preparation of budget table

First of all, if you want to spend less every month, you need a budget.

This is not an exciting activity, but it is a necessary step. Don’t worry, you don’t need to spend a lot of time on budgeting, and you don’t need to specify too many details.

Although I have compiled the sexiest budget table in the world, I still want to outline what your budget table should include. I have always been a fan of homemade budget tables, but you can also use digital budget apps (such as Mint, etc.).

As long as you have consumer behavior, you can easily combine expenditures into several categories. To clearly understand your consumption habits, please pay attention to your spending in the past three months.

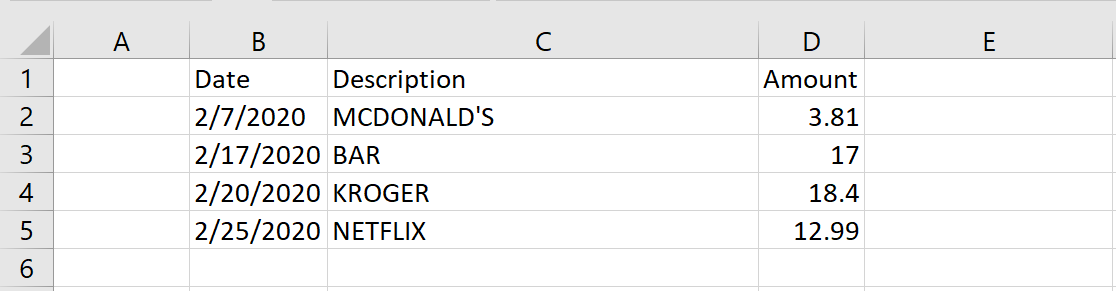

The following picture is a fairly simple example, only a few items are listed, but it shows the general situation of your expenditure.

Your expenditure list may be more detailed This is just a very simple example.

Paste each transaction activity into Excel (using CSV format) to classify each expenditure. The five standard expenditure classification labels are listed below. Of course, advanced players can also make specific classifications according to their needs (for example, “food and entertainment” can be divided into two major categories).

Housing: rent, utilities, various maintenance fees, property fees, etc.

Transportation and travel: gas, taxi, parking, subway, and air tickets.

Food and entertainment: groceries, dining out, drinks, events / tickets, etc.

Goods and services: buy clothes, household items, Various paid subscriptions, haircuts, insurance, etc.

Miscellaneous: Any item that does not fall into the above category.

Note: Separate your business expenses from personal expenses. You should make a separate budget for business expenses and record these expenses in a separate form or document. You can also follow these steps to track your business expenses. In this way, if it involves tax calculation, you will more easily calculate the tax you should pay.

Return to your personal budget. Next, you need to classify each expenditure.

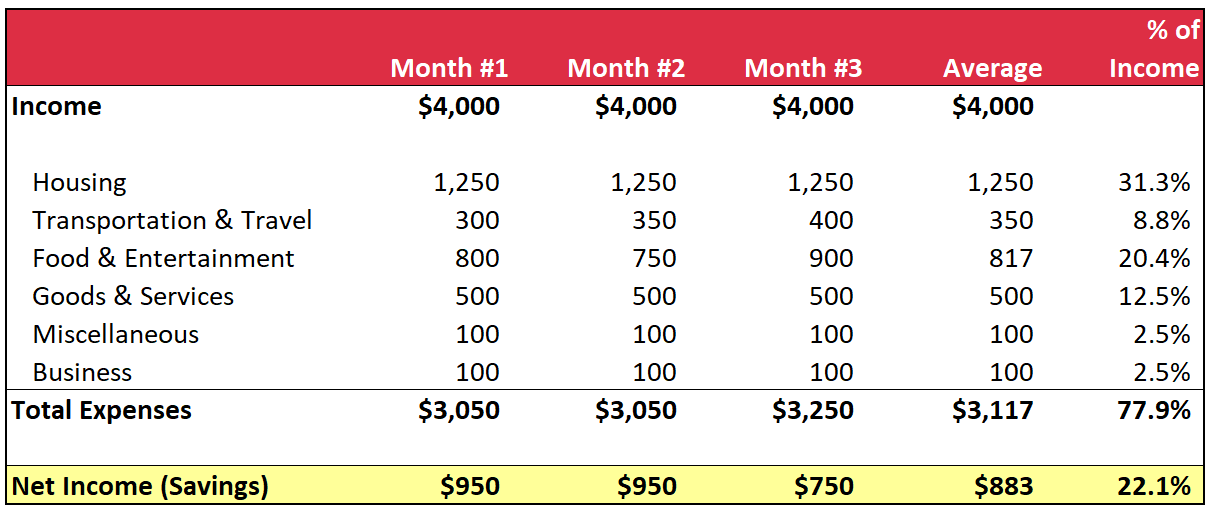

Calculate the average number of expenditures for each category within three months, and then divide the average number of each category by your monthly income. This way you can know where your income is spent. For example, suppose your monthly income is $ 4,000 and your rent / utility expenses are $ 1250. To calculate how much of your income is spent in the “housing” category, divide $ 1,250 by $ 4,000, which equals 31.3%.

After using the percentage, you will get the table as shown below, which is an example of the three-month budget table. (An explanation: because it is to calculate how much money I can save, this table covers business expenses.)

Note: I did not include debt in this budget statement. If you have a loan to repay every month, you must also include these expenses.

In this way, you can have a good understanding of your capital inflows and outflows. In this example, rent is the largest expense, and food and entertainment costs are also high. If this is my budget, I will first look at what can be reduced in food and entertainment consumption.

Identify the category of overspending

The following tells you a short story as an example.

As early asWhen I was still working in an investment bank, I was very reluctant whenever I had to make a budget every month. I am very tired every week, and during precious rest time, I have absolutely no desire to manage money. Actually, I only make budgets every two or three months. After a month without any budget, (suddenly poor) I finally made up my mind to update my budget every month. It’s a bit like drunkenly swiping yourself in the bar the night before, only to find that the balance on your card is only single digits the next day.

I give this example not because I am an alcoholic. In fact, in the past few months, I have consumed a lot of alcohol.

It ’s not buying food, it ’s not gas money, it ’s not a taxi.

Is buying milk tea.

I used to drink $ 145 milk tea a month, a month! In four months, I drank a total of $ 302 milk tea. I know what you are thinking, “Milk tea? So much money? What cat disease do you have?”

First of all, milk tea is the source of my sin. Secondly, I didn’t realize that I was buying milk tea. Maybe this description is not exact. In fact, I did n’t move to a milk tea shop like a zombie, but I bought it consciously. I just did not realize that this behavior has become a habitual behavior.

A cup of milk tea can be enjoyed for seven or eight dollars, but it is also a lot to add every day. Once this thing becomes uncontrollable customary behavior, it becomes a problem. In the afternoon, casually drinking a cup of milk tea to refresh is an inevitable daily activity.

If I do n’t make a budget, I may lose more. Guess how much money I have spent on milk tea in the past few months after I set the budget?

$ 132.

The total amount is about one cup of milk tea per month, I am very satisfied with this situation. You don’t need to give up what you like, all we have to do is temperance.

Change your lifestyle

With a budget, it wo n’t take long before you can determine where most of your income is going. Take a look at the cost of each category and see what is your biggest cost?

Unless you live with your parents or have special living conditions, your housing expenses will be the largest sum in your budget. This is normal and expected. Not everyone can move immediately. However, if you have the conditions, you may consider moving to a cheaper apartment / house or choosing to share a house. This can definitely reduce your monthly expenses and maximize your chances of success in your career. Just before I resigned, I moved to a cheaper apartment. My rent has been reduced from $ 1275 (excluding utilities) to $ 850.

The following are some of the biggest savings for me after I changed my lifestyle:

Moving has saved me $ 425 a month.

Let ’s go to the restaurant less and save me $ 160 a month.

Replacement of car insurance saved me $ 120 per month.

Drinking less alcohol saved me $ 80 per month.

Buying less clothes saved me $ 74 a month.

Reducing paid subscriptions saved me $ 70 per month.

Buying cheaper food (such as buying less steak) saved me $ 65 a month.

Not going to Starbucks saved me $ 40 a month.

There are many other ways to save, but these are the money saved on the blade. I moved from a high-rise apartment in downtown Atlanta to a lower-priced area. Of course, the surrounding scenery cannot be compared with the former, but it is more comfortable and cheaper.

I reduced my food cost by (a) going to a cheaper restaurant and (b) buying cheaper food at the grocery store. When my life was still luxurious, in most cases I would still cook for myself, but I would buy more expensive ingredients. And when I go out to eat, of course, I only go to luxury restaurants, after all, the income is there.

I still drink coffee today (I ca n’t imagine a life without coffee), but I will rely on free coffee in the rental office in my apartment. Over time, these small overheads add up to a real difference.

Everyone’s consumption habits are different, so your consumption habits may be different from mine, but there are several aspects that need to be focused on here.

Eating out. I speculate that 90% of people will spend more on meals than they think.

Grocery store. In most cases, cooking by yourself is cheaper than eating out. But shopping at the grocery store is still very likely to overspend.

Liquor. It is entirely up to the individual, but drinking is very expensive.

Shopping. Fortunately and unfortunately, shopping is as convenient as ever, and you can complete shopping with just a few taps on your phone.

Paid subscription. The subscription fees add up too much. Cable TV (if you still have it), Amazon Prime, Netflix, Hulu, Netflix, Spotify, HBO …

Again, moderation is the key. I ’m not saying you ca n’t go to the restaurant anymore,