Why open China ’s stock market? This seemingly simple question is actually not simple.

China ’s opening up of the A-share market can be traced back to the birth of QFII at the end of 2002, and QDII was launched in 2006. The Shanghai-Hong Kong Stock Connect was launched in November 2014, and the Shenzhen-Hong Kong Stock Connect was also opened in December 2016. At the same time, the annual total limit for Shanghai-Shenzhen-Hong Kong Stock Connect was removed. In 2018, the daily trading limit of Shanghai-Shenzhen-Hong Kong Stock Connect will be further increased by 4 times. In 2019, Shanghai-London Stock Connect implemented and canceled the total restrictions on QFII and RQFII. In short, the opening of the A-share market is steadily expanding.

The market liberalization theory believes that opening up domestic capital markets, especially for developing countries, can bring the following benefits:

First, international capital can be obtained to make up for the shortage of domestic capital and reduce the cost of capital, thereby expanding investment and promoting economic development.

Second, international investors, especially institutional investors who focus on long-term returns, generally have more investment experience, and their participation in investment can make the domestic market more mature, Be more rational and improve the governance level of local companies.

Third, it can increase liquidity, enhance the domestic market ’s position and competitiveness in the international arena, not only attract foreign investment to the domestic market but also attract foreign companies to the domestic market Go public.

Fourth, give domestic and foreign investors more choices.

However, the above theories are mostly inconsistent with China ’s practice of opening the A-share market.

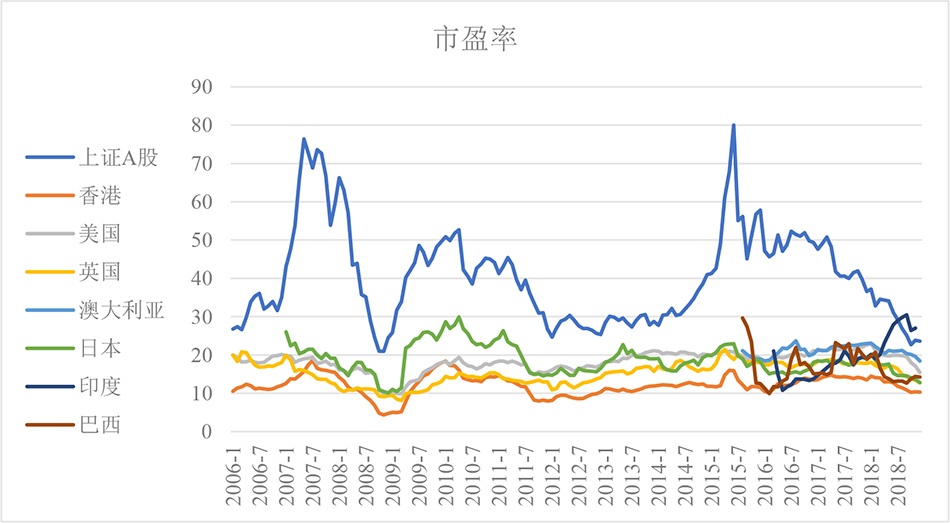

First of all, China does not lack capital after 2003. Whether it is the savings rate or the investment rate, China is the highest among major economies (see Figure 1 ), and savings are higher than investment (see Figure 2 ). China’s foreign exchange reserves have also increased rapidly since 2003 (see Figure 3 ). By 2006, it had surpassed Japan and became the world’s largest foreign exchange reserve country. The average price-earnings ratio of the Chinese stock market is also much higher than the world’s major markets (see Figure 4 ). All of this shows that China is not bad, and the cost of equity financing is relatively low. Therefore, the opening of the A-share market should not be to reduce the cost of capital and introduce foreign capital to make up for insufficient domestic investment.

Figure 1 Savings rates of major world economies

Figure 1 Savings rates of major world economies

Figure 2 China ’s savings and investment levels

Figure 2 China ’s savings and investment levels

Figure 1 Savings rates of major world economies

Figure 2 China ’s savings and investment levels

Note: The left axis represents “investment amount” and “savings amount”, and the right axis represents “savings- Investment “

Figure 3 The level of foreign exchange reserves of major world economies

Figure 3 The level of foreign exchange reserves of major world economies

Figure 4 The price-earnings ratio of major world markets Reasonable, although it may produce this effect in the process of profit-seeking. Foreign capital is no exception. If foreign capital believes that it is profitable through rational investment, long-term holding, and strengthened supervision, it is better to gain more with half the effort through speculative arbitrage. They have no reason not to do so. To date, the academic community has not found strong evidence that foreign institutional investors constitute a strongStrong constraints. In fact, most Chinese companies have controlling shareholders, and the status of institutional investors is relatively unimportant. Even if the strategic investors introduced when the five major banks reformed their shares, most of them sold their shares after the lock-up period expired. In addition, A-shares experienced a speculative frenzy between 2006 and 2007, and in 2015, it happened again shortly after the Shanghai-Hong Kong Stock Connect opened. The result of strong intervention. The level of volatility is often used to measure the strength of speculative activities. After the Shanghai-Hong Kong Stock Connect, the volatility of the A-share market has not decreased (see Figure 5 ). The most important thing is that the A-share market’s price-earnings ratio is significantly higher than that of Hong Kong, China, and the European and American markets, and higher than the corresponding B-shares, H-shares, and red-chip stocks. From the perspective of asset allocation. Foreign investors can find cheaper alternatives to A shares among the more than 1,000 Chinese stocks listed overseas. Although the quota is not high, QFII quota has never been used up since 2013, which also shows from one side that A shares are not attractive to foreign institutional investors, and most of them come from speculators.

Figure 4 The price-earnings ratio of major world markets Reasonable, although it may produce this effect in the process of profit-seeking. Foreign capital is no exception. If foreign capital believes that it is profitable through rational investment, long-term holding, and strengthened supervision, it is better to gain more with half the effort through speculative arbitrage. They have no reason not to do so. To date, the academic community has not found strong evidence that foreign institutional investors constitute a strongStrong constraints. In fact, most Chinese companies have controlling shareholders, and the status of institutional investors is relatively unimportant. Even if the strategic investors introduced when the five major banks reformed their shares, most of them sold their shares after the lock-up period expired. In addition, A-shares experienced a speculative frenzy between 2006 and 2007, and in 2015, it happened again shortly after the Shanghai-Hong Kong Stock Connect opened. The result of strong intervention. The level of volatility is often used to measure the strength of speculative activities. After the Shanghai-Hong Kong Stock Connect, the volatility of the A-share market has not decreased (see Figure 5 ). The most important thing is that the A-share market’s price-earnings ratio is significantly higher than that of Hong Kong, China, and the European and American markets, and higher than the corresponding B-shares, H-shares, and red-chip stocks. From the perspective of asset allocation. Foreign investors can find cheaper alternatives to A shares among the more than 1,000 Chinese stocks listed overseas. Although the quota is not high, QFII quota has never been used up since 2013, which also shows from one side that A shares are not attractive to foreign institutional investors, and most of them come from speculators.

Figure 5 The volatility level of the Shanghai stock market before and after the Shanghai-Hong Kong Stock Connect opens

Figure 5 The volatility level of the Shanghai stock market before and after the Shanghai-Hong Kong Stock Connect opens

Figure 3 The level of foreign exchange reserves of major world economies

Figure 4 The price-earnings ratio of major world markets Reasonable, although it may produce this effect in the process of profit-seeking. Foreign capital is no exception. If foreign capital believes that it is profitable through rational investment, long-term holding, and strengthened supervision, it is better to gain more with half the effort through speculative arbitrage. They have no reason not to do so. To date, the academic community has not found strong evidence that foreign institutional investors constitute a strongStrong constraints. In fact, most Chinese companies have controlling shareholders, and the status of institutional investors is relatively unimportant. Even if the strategic investors introduced when the five major banks reformed their shares, most of them sold their shares after the lock-up period expired. In addition, A-shares experienced a speculative frenzy between 2006 and 2007, and in 2015, it happened again shortly after the Shanghai-Hong Kong Stock Connect opened. The result of strong intervention. The level of volatility is often used to measure the strength of speculative activities. After the Shanghai-Hong Kong Stock Connect, the volatility of the A-share market has not decreased (see Figure 5 ). The most important thing is that the A-share market’s price-earnings ratio is significantly higher than that of Hong Kong, China, and the European and American markets, and higher than the corresponding B-shares, H-shares, and red-chip stocks. From the perspective of asset allocation. Foreign investors can find cheaper alternatives to A shares among the more than 1,000 Chinese stocks listed overseas. Although the quota is not high, QFII quota has never been used up since 2013, which also shows from one side that A shares are not attractive to foreign institutional investors, and most of them come from speculators.

Figure 5 The volatility level of the Shanghai stock market before and after the Shanghai-Hong Kong Stock Connect opens

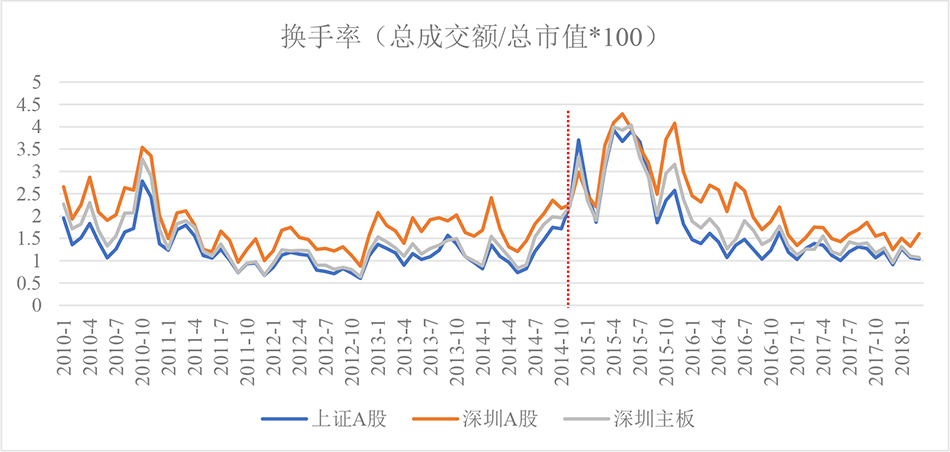

Once again, after the opening of the Shanghai-Hong Kong Stock Connect, the proportion of foreign capital in the daily trading volume of the Shanghai stock market is less than 5% on average, and the highest is less than 8% (the Shenzhen market is even lower). Therefore, foreign capital has a limited impact on the liquidity of the A-share market. If the Shanghai-Hong Kong Stock Connect enhances liquidity, then its impact on the underlying stocks should be greater than that of non-standard stocks. Similarly, Shanghai-Hong Kong Stock Connect’s impact on the Shanghai stock market should be greater than that of the Shenzhen stock market. However, Figure 6 shows that after the opening of the Shanghai-Hong Kong Stock Connect, the turnover rate of its underlying A shares (SHC) has not increased significantly compared to non-standard A shares (non-SHC) (except for the first three months). Figure 7 further shows that there is no significant difference in the turnover rate between Shanghai and Shenzhen, and they fluctuate roughly simultaneously. In fact, the average turnover rate of stocks in the Shanghai stock market in the two years after the opening of the Shanghai-Hong Kong Stock Connect was significantly lower than the turnover rate of non-standard stocks, which also coincides with the fact that capital going south is larger than capital going north. An important sign of the exchange ’s international competitiveness is that it can attract a large number of foreign companies to list, such as the London Stock Exchange, the New York Stock Exchange and the NASDAQ. The Shanghai and Shenzhen markets have a high price-earnings ratio, and should have a role in attracting foreign companies to list and tradeSome comparative advantages.

Figure 6 The turnover rate of standard A shares and non-standard A shares of Shanghai stock market before and after the opening of Shanghai-Hong Kong Stock Connect

Figure 6 The turnover rate of standard A shares and non-standard A shares of Shanghai stock market before and after the opening of Shanghai-Hong Kong Stock Connect

Figure 7 Shanghai Stock Exchange turnover rate before and after the opening of the Shanghai-Hong Kong Stock Connect

Figure 7 Shanghai Stock Exchange turnover rate before and after the opening of the Shanghai-Hong Kong Stock Connect

Figure 6 The turnover rate of standard A shares and non-standard A shares of Shanghai stock market before and after the opening of Shanghai-Hong Kong Stock Connect

Figure 7 Shanghai Stock Exchange turnover rate before and after the opening of the Shanghai-Hong Kong Stock Connect

Finally, the opening of the A-share market has indeed given domestic and foreign investors More choices, but due to the limitation of open scale, its marginal effect is not very great. For foreign investors, there are more restrictions before 2018. In addition, the high price-earnings ratio of A-shares and widely existing substitutes have also reduced the demand for A-shares by foreign investors. For mainland investors, there are more restrictions. First, QDII and Shanghai-Shenzhen-Hong Kong Stock Connect still have daily quota restrictions. Furthermore, most of the investment targets are Hong Kong stocks, and only some Hong Kong stocks. Finally, there are qualification restrictions for mainland investors. Individual investors must have financial assets of more than 500,000 yuan to invest in Hong Kong stocks. Even so, the capital going south is greater than the capital going north, indicating that the Shanghai-Shenzhen-Hong Kong Stock Connect still provides benefits for mainland investors. It is inferred from this that further relaxation of restrictions on overseas stock investment by domestic investors will help curb speculation in the domestic market and will of course increase the risk of capital flight. In addition, RQFII and Shanghai-Shenzhen-Hong Kong Stock Connect do provide more investment options for overseas RMB holders, but the scale is limited and most are invested in the bond market. Whether these RMB holders invest in A shares depends mainly on the company’s quality and cost performance. Instead of letting them vote, they must vote.

To sum up, the opening of the A-share market does not reduce the cost of capital, increase net capital inflows, increase liquidity, and make the market more rational as expected by traditional theory. Opening the A-share market does give domestic investors more choices, but their marginal utility is limited. Of course, Shanghai-Shenzhen-Hong Kong Stock Connect has increased the demand for Hong Kong stocks and activated the Hong Kong market,It helps to consolidate and enhance Hong Kong’s status as an international financial center, but this should not be the main purpose of opening up the A-share market.

So, why open China ’s A-share market? As far as the current situation is concerned, it basically provides more choices for domestic and foreign investors. In the long run, it should be part of China’s overall financial internationalization strategy, which is to fully liberalize capital controls and realize RMB internationalization. Full opening means that the stock market may be hit by international hot money and capital flight. The current opening can be seen as a limited stress test. At the same time, opening up the A-share market is also preparing for the Chinese stock market to participate in global competition.

(Author Sun Qian is a professor at Fudan University School of Management, Sun Xiangyu is a PhD student at Fudan University School of Management)