Has established partnerships

and the country more than fifty small and medium banks Author: Wing-yee, bear pure Yi

It is learnt that the family members of the family recently announced the completion of the 120 million yuan Pre-A round of financing, led by Panda Capital. This round of funds will be used to deepen technology, expand the team of experts, and expand business.

The credit field can be simply understood as the connection between the capital side and the asset side. There are various forms of third-party institutions in the middle to help the two parties connect, such as loan assistance institutions. In recent years, despite the emergence of institutions such as P2P platforms and flow platforms, the financial lending sector is under a strong regulatory environment, and the supply and demand relationship is seriously unbalanced. It is still difficult to achieve a reasonable match between the capital and asset sides.

Taking banks as an example, as of the end of 2018, there were 2,260 rural financial institutions, 1,562 rural banks, and many small and medium-sized banks in China. For example, the flower-like and lending businesses carried out by the head e-commerce platform (asset side) usually have long-term cooperation with head banks and trust institutions, and it is difficult for small and medium-sized banks to cut in. But at the same time, small and medium-sized banks are also very keen to develop similar online consumer finance business, so there is a strong demand for high-quality and sub-optimal assets.

The family member of the family that I contacted recently was established in August 2018. Its core business is to provide quality and sub-optimal capital (such as small and medium-sized banks, trusts, etc.) companies that provide docking services with asset parties. In-house Mathematics uses cloud computing, AI, data insight, anti-fraud and other technologies to provide both parties with new financial business transformation and construction solutions.

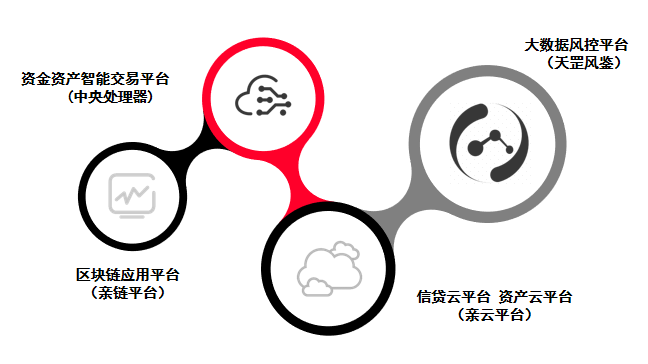

In-House Mathematics Products

Song Junwei, the founder and chairman of Family Mathematics, said that in the field of loan assistance, there are currently three mainstream models, mainly fund output, technology risk control output and flow output. The route taken by the in-person mathematics department is a more comprehensive route, and all three types have outputs. The central processor, big data risk control laboratory and intelligent recommendation engine in the background of the in-house math department constitute its core barriers.

Based on this, at the front end, the family has established four business segments: fund-asset intelligent matching, scene client group connection, supply chain finance and technology consulting: