This catering renewal is very “story”.

Editor’s note: This article comes from the WeChat public account “Winner Cloud Intelligence Library” (ID: sydcxy2014 ) , author: Hu Qiancong.

During the epidemic, consumers who “sucked” could only find solace from the takeaway channel. The epidemic has gradually faded. Which sub-categories can best cure consumers’ hurt hearts? In the spring breeze of consumption recovery, where is the “jumping platform” for catering?

01 Casual dining: The “net red” category has increased significantly, and high-customer price tea and low-customer price coffee are expected to “overtake in corners” < / strong>

In the epidemic, whether it is online marketing or takeaway sales, consumers have always maintained a high degree of attention to casual dining. After the epidemic, casual dining The celebrity of celebrities will continue to inspire consumers’ “impulse to punch” and promote a round of “compensatory consumption.”

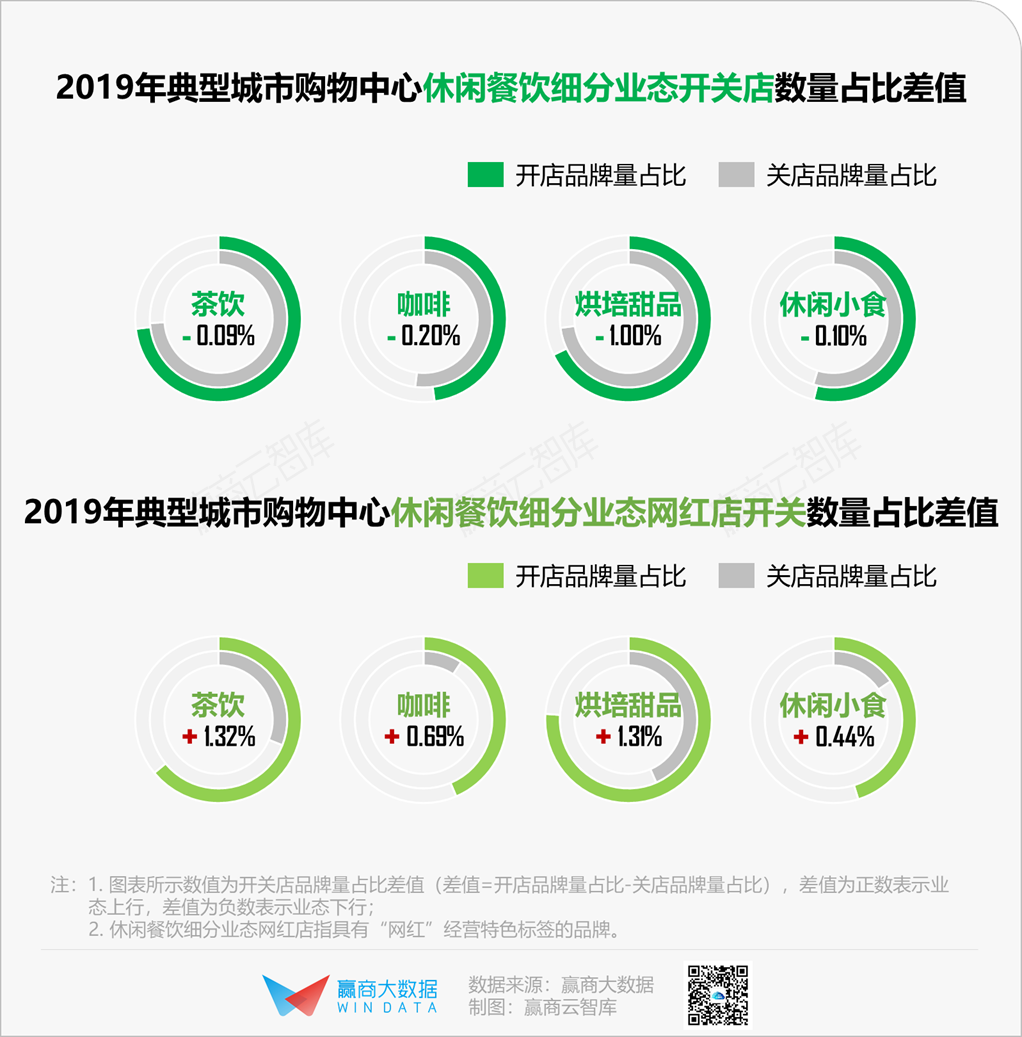

The proportion of closed store brands of tea, coffee, roasted desserts, and casual snacks is higher than the proportion of opened stores. Casual dining is a non-rigid demand format and has certain requirements for regional consumption capacity. With the saturation of the market Higher and higher, the format of the race track is narrowing.

On the other hand, the competition in the Red Sea has forced the brand to continuously upgrade to “survival”, striving for cross-border, face value, and marketing, which has become a game for casual dining. Brands with “Internet celebrity” labels in the four sub-segments have a significantly higher proportion of store brandsProportion of closed stores , online red shops are still the core driving force for the growth of the format.

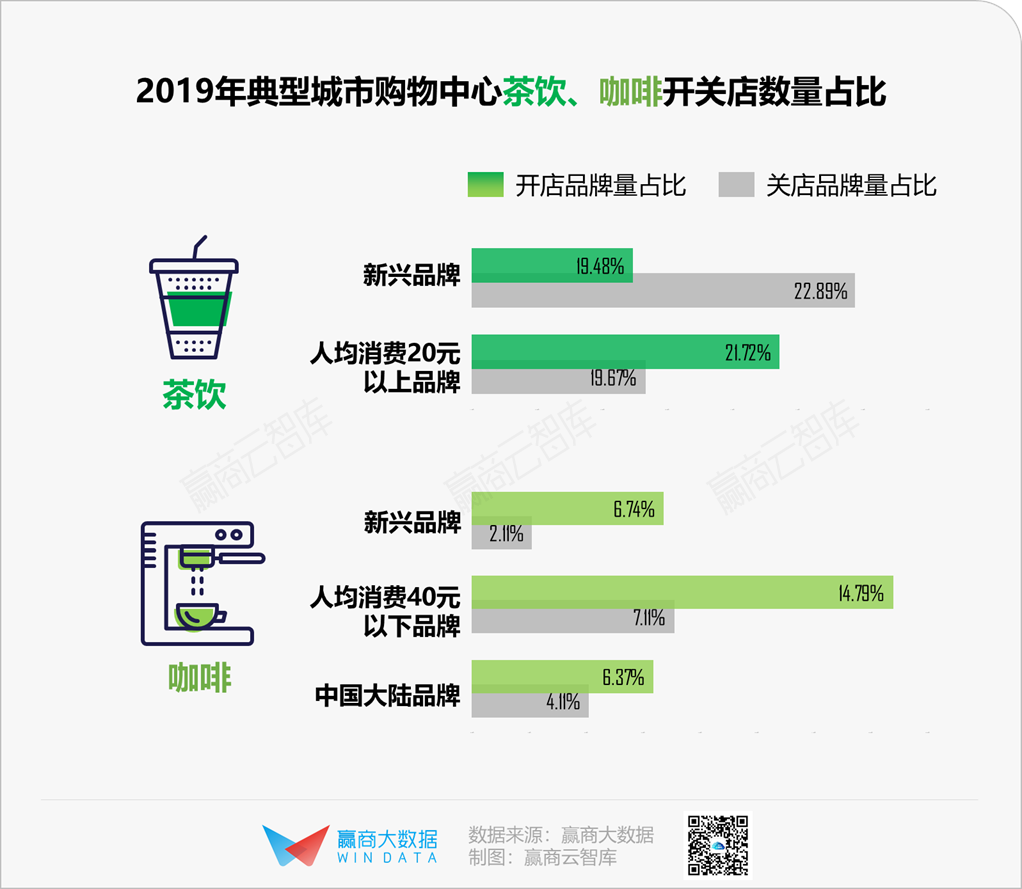

Among them, the hottest tea and coffee tracks have taken different paths.

In the past year, the emerging brands of tea beverages have shown a downward trend, indicating that the industry concentration is constantly improving; at the same time, under the leadership of the head brands, the industry standards and consumption quality in the tea beverage sector have been further improved. strong> For brands with a per capita consumption of more than 20 yuan, the proportion of open store brands is higher than that of closed stores 2.06% .

For some established brands, consumers are more willing to pay an equivalent premium for this; for example, the recently popular “Xicha”, which was promoted by the “price hike” on the public comment Of the 11 commented high-frequency words, “product price” is the feature with the fewest mentions.

The increase in emerging coffee brands is significant. The annual consumption growth rate of the Chinese coffee market has reached 15%, attracting many new brands to enter the market. Among them, Mainland China brands and brands with per capita consumption below 40 yuan have outstanding growth power . At present, coffee consumption is still in the rising stage in China. After 90s, the group is more willing to try new brands and pay more attention to the quality, price and convenience of coffee.

The catering giant taking Yum as an example, also launched the coffee trendy brand [COFFii & JOY] targeting young people in 2018, which will “hand-fashion” hand-made specialty coffees. 26 stores have been opened in 8 cities across the country.

Image source: COFFii & JOY

02 Social dining: Sichuan style hot pot “quality”, Cantonese / Hong Kong style hot pot “Shang Hot Search”