To defend your own interests, it is urgent to

Editor’s note: This article comes from the WeChat public account ” beast Finance “(ID: mengshoucaijing) , author: Dong Law Act.

This article is slightly longer and is divided into two parts. The first part is to restore the crude oil treasure thunder incident from a professional financial perspective; Ten issues were raised from the perspective of financial law, and the rights and responsibilities of both parties were clarified from a legal perspective, demonstrating that investors can claim compensation from BOC. Only by pursuing the doubtful points of crude oil products can we find the direction of the claim. Looking at all the articles on the market, there is no article like this article that clearly and professionally explains the bugs in this product, which is worth a closer look.

Beast Finance is not a bystander. If you are an investor in BOC crude oil products and need rights protection and claims, you can add a WeChat editor (mengshoucaijing001). Mengshou Finance will bring you into the rights protection group. Professional financial litigation lawyers will help you. Interoperability, help each other.

First, behind the thunder of BOC crude oil products

Let ’s first talk about the deep-seated reasons behind the huge loss of crude oil. Readers who are not interested in this part or just want to make a claim can jump directly to the second part of this article.

Since the beginning of the year, Brent crude oil futures have fallen by about 60%, while U.S. crude oil futures have fallen by about 130%. U.S. crude oil futures plummeted on Monday, falling to the negative region for the first time. The crude oil contract closed at a jaw-dropping US $ 37.63 per barrel.

(Source: Investing)

This plunge fell by 306%, and once hit a historical low of $ 40.32 per barrel. Brent crude oil futures fell 2.51 US dollars, the settlement price reported 25.57 US dollars per barrel, a decrease of 9%.

The reason for the plunge in oil prices is still that traders who are long May contracts are eager to close their positions.

The production and operation of American companies were suspended due to the epidemic, and the oil market was seriously oversupplied. According to data released by the US Energy Information Administration last week, as of the week of April 10, U.S. crude oil inventories (excluding strategic oil reserves) increased by 19.25 million barrels from the previous week, recording growth for 12 consecutive weeks, and the increase continued to hit a record high. The storage tanks in Cushing, Oklahoma alone, have reached 69%, up from 49% four weeks ago. At the same time, the epidemic caused problems such as poor infrastructure, transportation and logistics, and crude oil was difficult to export or store. If the storage capacity of the storage tank is insufficient or the storage cost is too high, the trader has to accept the negative oil price.

To sum up, there are five steps in the process of “cashing out” the crude oil real position this time:

1 The oil price fell sharply in the early period, causing a large number of speculators to bargain-hunting for crude oil futures, forming a state of massive accumulation of long bulls

2 The production reduction agreement will be implemented from May, so the period from late April to May becomes a garbage period for crude oil trading

3 There are too many speculative orders, and there is no real delivery demand. When faced with delivery, long positions or liquidation or rollovers

4 The bears see the timing and hit the contract price in recent months, causing the bulls to face losses regardless of the liquidation or rollover

5 The bulls staged “Run Fast”. The previous friends became opponents, and the ant cave collapsed and robbed the road.

On the evening of April 21, the U.S. oil contract delivered in June fell by nearly 70% during the session, and the WTI June crude oil futures settlement price closed at 11.57 US dollars per barrel on the same day, a decrease of 43.37%, the lowest since February 1999.

On April 22, the main contract of domestic crude oil futures opened at a daily limit, oil and gas funds collectively jumped at a high altitude, and even crude oil ETFs plunged 47% during the day.

According to wind news, the plunge in oil prices has forced the largest oil ETF in the market, the United States Petroleum Fund (USO), to apply for a change in the position structure and begin to clear the near-month contracts, moving directly to August.

Because the price of US crude oil is in the negative range, this means that the seller of crude oil futures must pay the buyer, which is the first time in history.

Investors who have bottomed out not only want to cry without tears, but also have worsened.

BOC ’s official website shows that crude oil treasure is a pegged domestic and overseas crude oil futures contract issued by the Bank of China to individual customersThe trading products of the contract are different according to the reference object of the quotation, including US crude oil products and British crude oil products, and US oil and British oil are divided into two types: USD and RMB. The product does not have leverage, and contracts are issued on a regular basis.

The so-called US oil is the WTI (West Texas Intermediate) crude oil traded on the US exchange, West Texas Intermediate crude oil. British oil is Brent crude oil traded on the British exchange. WTI2005 crude oil refers to crude oil delivered on April 21, 2020.

(picture source: Bank of China)

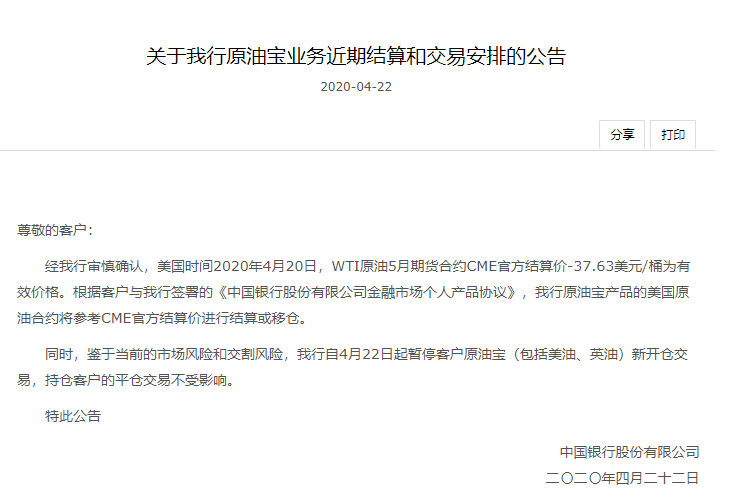

BOC stated that after careful confirmation, on April 20, 2020, the US time CTI official settlement price of the WTI crude oil May futures contract was -37.63 US dollars per barrel as the effective price, and the US crude oil contract for crude oil products will refer to the CME official settlement Price or settlement. In view of the current market risk and delivery risk, the new open trades of customers Crude Oil (including American Oil and British Oil) will be suspended from April 22, and the closed trades of open clients will not be affected.

That is to say, these crude oil clients will bear all the losses caused by the oil price falling to a “negative value” and owe the bank three times the principal.

According to reports that a customer has received a text message from the bank, a 3 times deposit is required. The investor questioned: “The bank’s 50% reminder and 20% liquidation risk control have no hint at all,” and “the insurance money for jumping a building can’t afford it.”

Some investors also said that the Bank of China Crude Oil Agreement agreed to be flat when it fell to 20% of the margin. Why did it not be flat when it fell to 20%?

Bank of China customer service responded that if the Bank of China crude oil treasure is the last trading day of the contract, the trading time will be 8: 00-22: 00. If it exceeds 22:00, the bank will not carry out the liquidation operation. After the point fell to below 20%.

An investor said that if the product design of BOC Crude Oil is the last trading day of the contract, the trading time is 8: 00-22: 00. Why is there no shifting of positions for the month at 10 pm? If BOC moves positions according to trading hours, investor losses can be reduced.

Bank of China customer service responded that stopping trading at 10 pm does not mean that it will start to shift positions at 10 pm. The delivery price refers to the official settlement price of the futures contract of the exchange on that day. , But the specific time for crude oil treasure to move the warehouse is not registered.

It is reported that due to huge fluctuations in crude oil products linked to domestic banks (including crude oil treasure), major banks have conducted self-examinations under regulatory requirements and have requested to submit self-examination reports. It is said that due to market instability, many banks have stopped recommending related products or stopped doing long.

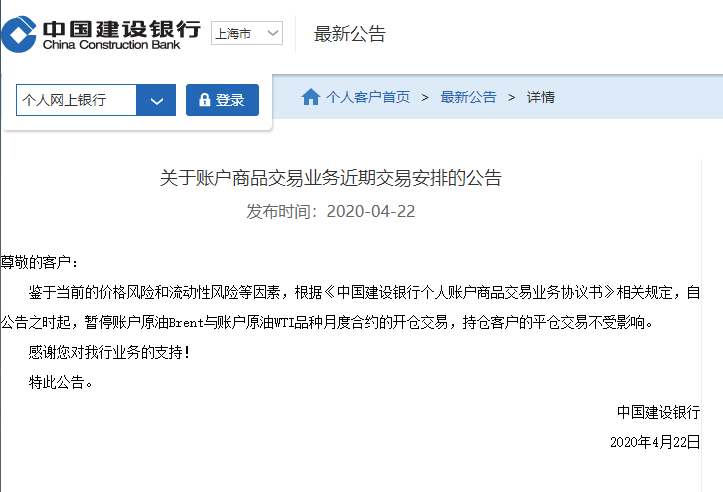

On the evening of the 22nd, CCB announced that, in view of the current price risk and liquidity risk and other factors, from the time of the announcement, the opening of the monthly contract of the account crude Brent and the account crude WTI variety monthly contract was suspended, and the position client ’s Position trading is not affected.

(picture source: China Construction Bank)

The storm has not subsided. The Bank of China issued a statement on the crude oil treasure business, saying that crude oil treasure products are linked to overseas crude oil futures. Similar to futures trading operations, according to the agreement, the contract will expire on the contract expiration processing date, according to the customer In the way specified in advance, carry out shifting or expiry. CorrectFor crude oil products, when the market price is not negative, the long position will not trigger a forced liquidation. For those who have determined to enter the position shift or due to the settlement of the difference, the client will complete the due treatment at the settlement price, and will no longer mark the market or liquidate. In the early hours of April 21st, Beijing time, the WTI crude oil futures May contract price fell sharply, and the settlement price announced on the day was -37.63 US dollars. In order to exclude the situation where the settlement price on the day is negative due to abnormalities such as failures in the exchange system, BOC actively contacted the Chicago Mercantile Exchange and market participants for verification, so the trading of crude oil products linked to the US oil contract was suspended for one day , Without affecting customer rights. At present, the main participants will still settle with reference to the settlement price according to the exchange rules. The Bank of China has completed the expiry of the May contract based on prior agreement.

Analysis in the industry believes that BOC should settle at the price of 11.7 USD quoted at the time node where trading stopped at 22:00 on April 20, instead of -37.63 USD. Because, after 22:00 that day, the customer has no transaction. The Bank of China did not renew in advance and encountered major liquidity problems, which led to huge losses for investors.

For the crude oil treasure product itself, some people think that “BOC’s crude oil treasure product design has a big problem. If there is no product design problem, some things may not happen.”

Later news said that the Bank of China believes that the crude oil treasure has been posted upside down, and that the leadership of a branch of a city branch of the Bank has been interviewed by the regulator.

It is reported that the Intercontinental Exchange (ICE) is preparing for the Brent crude oil contract transaction price to be negative. CME Group will allow oil options with negative quotes to be listed starting April 22.

Institutional analysis believes that as more data shows that US crude oil inventories are approaching the limit, and the demand shock caused by the epidemic continues, there is room for oil prices to continue to decline. Analysts warned that the June contract was reiterated at the end of May.

The initial loss under final liquidation is calculated based on CME data. Assuming 1,000 barrels per contract, this time up to 77,076,000 barrels of crude oil were traded near the settlement price. If the average price for opening a position is $ 20 / barrel, the total settlement loss will be as high as $ 4.466 billion, or about 31.5 billion peoplecurrency.

Second, what do lawyers say? Ten Doubts about Crude Oil Treasure Thunder Event

After the resumption of the crude oil treasure thunder event, we will analyze ten doubtful points from the two dimensions of finance and law:

1. What product is BOC crude oil treasure? Is it financial management, fixed investment, futures or ETF?

We first clarify the question, what type of product is BOC Crude Oil? From the customer’s point of view, the nature of this product is a “personal financial management” product. Many people think that this is an unleveraged crude oil financial management, which is basically a risk-free arbitrage. Or fixed income fixed investment, although the investment is crude oil futures, derivatives, but the risk is controllable.

But according to the product description of Crude Oil Bao, “Crude Oil Bao” is a “paper crude oil” product, and paper crude oil refers to investors buying and selling “virtual” crude oil on the books according to bank quotes. According to the product introduction, Crude Oil Bao is a tracking international crude oil futures contract issued for individual customers, which does not have a leverage effect. Product quotations are linked to international crude oil futures prices, and the corresponding benchmarks are “European Futures Exchange (ICE) North Sea Brent Crude Oil Futures Contract” and “New York Mercantile Exchange (CME) WTI Crude Oil Futures Contract”. Only the share is counted, and the physical crude oil is not extracted. Isn’t this the crude oil futures linked to US oil and British oil? But it also indicates that personal financial products are not a standardized futures contract in essence, and even have certain characteristics of stocks. They deliberately changed the definition deliberately and confused the concept. One is not like the product.

We have studied with industry experts, crude oil treasure is similar to crude oil ETF, similar to wealth management, a non-standardized exotic product.

And today there is news in the market that regulators have suspended the declaration of early-stage popular industry ETF products such as semiconductors, 5G, and new energy vehicles, and also halted commodities ETFs such as crude oil with poor liquidity. Some institutions have also returned crude oil ETF declarations.

2. What role did BOC play? Is it a broker or a market maker?

Another key issue is that the Bank of China contract, which is similar to margin trading, needs to be exchanged for months. Then the product must be of a futures nature. In this transaction, his role is either a broker or a market maker.

If it is a broker, BOC will put all investors ’transactions on the international market-overseas futures exchanges, and conduct a transfer transaction. If he is a market maker, he is hedging his position after he rolls it out-hedging gap, big international banks are more willing to follow the market maker model, because the difference in the middle of the rolled position is the bank, But the problem is that the core is that no matter how many positions you hold, you will face the liquidity of the international market. This time, there will be liquidity problems in crude oil futures, and they may not be traded in the futures exchange, because there is no such big opponent.

And this time on April 20, ChinaThe bank held more than 20,000 long positions on the WTI crude oil futures May contract. At that time, the contract held more than 100,000 positions, which is equivalent to the Bank of China accounted for 20%. There must be a problem here.

In summary, in the account crude oil business, in order to respond to customer transactions in a timely manner, BOC also assumes the role of broker and market maker, and the net positions generated by customer trading, BOC will go to relevant overseas exchanges and use its foreign exchange funds to go Perform hedging. The Bank of China mainly played the role of a market maker, but there is no clear definition of power and responsibility, which also laid a major hidden danger of this thunderstorm.

3. A key question, does Crude Oil really have no leverage?

BOC’s “paper crude oil” business has always emphasized the 100% margin system and does not support leveraged trading.

Actually, the “crude oil treasure” differs greatly from the US futures trading methods. “Crude Oil Treasure” is similar to China’s stock trading. At a fixed amount, how many shares can be bought depends on the current quotation of the target. For example, when the crude oil price is USD 0.01 / barrel, a deposit of USD 10,000 can be traded at 1 million barrels, and according to the rule of 1,000 barrels per lot, you can hold 1,000 lots. However, the CME futures trading margin system in the United States does not depend on the market price. No matter how much the market price is, it is determined by the fixed amount of hands that can be bought.

For example, the CME official website shows that the crude oil May contract margin is $ 7,500, which means that no matter what the market price is, investors want to hold 1 contract of the contract, the account must have at least $ 7,500, two hands There must be $ 15,000, and so on. It can be seen from this that the same deposit is 10,000 US dollars. Under the CME futures trading system, only one lot can be traded, but the “crude oil treasure” can trade 1,000 lots.

In this case, the so-called “no leverage” paper crude oil has become a “thousand times leverage”. When the price drops to -30 US dollars / barrel, CME’s futures trading system only loses 30,000 US dollars under the condition of no forced liquidation, but it can lose 30 million US dollars under the rule of “Crude Oil”.

Crude oil treasure-“1000 times leverage” under the name of no leverage

4. Why does Crude Oil Bao not participate in physical delivery of crude oil?

In the previous analysis of the product structure of Crude Oil Bao, as well as the role of BOC in the transaction, BOC does not directly participate in physical delivery, and it is even less likely to receive oil and then sell it in June to achieve risk-free arbitrage. Futures trading is divided into investment contracts and delivery contracts. The delivery contract requires the buyer to have the relevant qualifications, and it cannot be applied on the last trading day. Therefore, at this time, they could not be delivered, and could only be slain.

CME crude oil trading rules, buyers involved in the delivery must carry out on any pipeline or oil storage equipment in Cushing, Oklahom, Okla. Use EnterprisePipelines of Cushing oil storage equipment or Enbridge Cushing oil storage equipment. In addition, for the delivery contract, the seller must tell the buyer about the bank and other relevant information before 12 pm on the third day before the settlement date. In other words, in the last three days of maturity, it is no longer possible to apply for a physically delivered futures contract. In the investment contract, because there is no other way out in the last three days, plus the modification of the rule that the exchange price can be negative, the shorts are directly forced the bulls to a dead end and strangled.

In analogy, the United States’ largest crude oil ETF, the US Petroleum Index Fund (USO), has received billions of dollars in new funds in recent weeks, and its positions account for a quarter of WTI’s May contract outstanding. The American Petroleum ETF is a fund itself, and it is impossible to choose to contact physical commodities. Therefore, this ETF fund must also choose to sell the May contract.

Crude oil treasure-can not be delivered, only can be slaughtered …

5. How to regulate and operate the crude oil treasure shifting month?

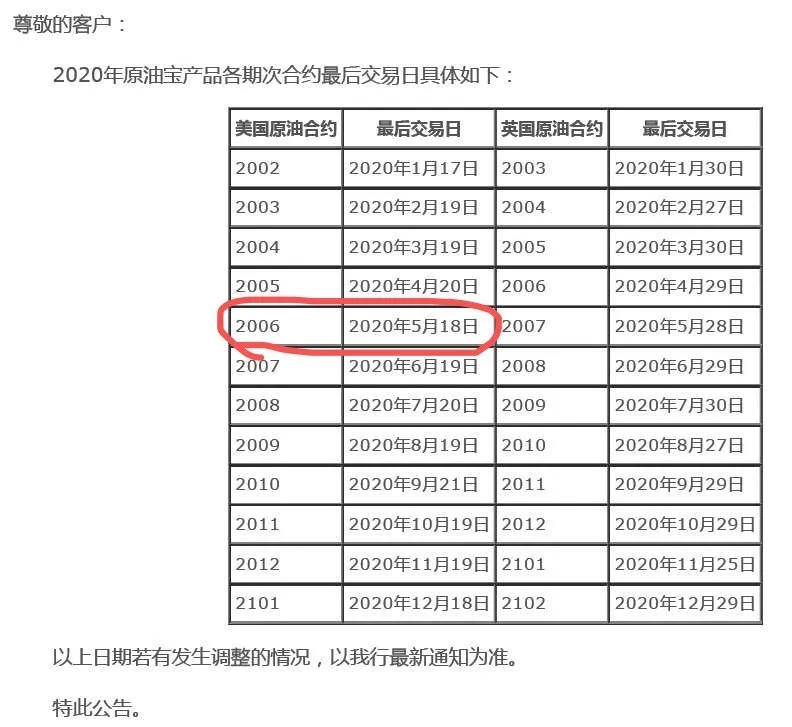

From the product manual, we can see that the last trading day of each month’s contract of BOC crude oil treasure:

That is to say, BOC Crude Oil Investors, they can decide at their own discretion to move positions for a certain period of time (extension). This is like investors in the futures market. In the face of the contract is about to expire, they can choose to move their positions for a certain day before the expiration. For example, if you bought the crude oil treasure of Bank of China’s 06 US crude oil contract, the last trading day is May 18. Then, before this trading day, you can freely choose to move positions for a month (rollover) at any time on May 5, 10, and 13th.

Before closing a contract, in theory, BOC does not have the power to automatically renew customers. Unless the account expires on the last trading day of the contract and your account is still not in operation, then BOC will intervene to force you to move the position and change the month (extension).

However, BOC set the month (extension period) of shifting positions on the last day-April 20, which was agreed in advance in the product description and agreement, and it has always been done in the past. Until the last trading day, BOC does not have the power to operate the customer’s account.

Some investors questioned that at a specific time, if the product design of BOC Crude Oil is the last trading day of the contract, the trading time is 8: 00-22: 00. Why is there no shifting of positions for the month at 10 pm? If BOC moves positions according to trading hours, investor losses can be reduced.

Bank of China announcement reply, stop at 10pmThe transaction does not mean that the position will be moved at ten o’clock in the evening. The delivery price refers to the official settlement price of the futures contract of the exchange on the day. On the trading day, the Bank of China crude oil treasure was extended on April 20, and it happened to encounter the lowest settlement price in history -37.63.

Crude Oil Treasure-Move the warehouse for another month, step on the cliff …

6. Can crude oil treasure fall to a negative value?

On April 15, the CME Group Clearing House issued a test announcement saying that if there is a zero or negative price, all trading and clearing systems of CME will continue to operate normally and the test preparations have been completed, but seeing this news We just want the pill. With our previous experience in building such a trading platform, we must have sufficient data to prepare it for the terrorist in advance.

It ’s not over yet. Negative oil prices in the financial market may become the norm. It is reported that the Intercontinental Exchange (ICE) is preparing for the Brent crude oil contract transaction price to be negative. CME Group will allow oil options with negative quotes to be listed starting April 22.

So, according to the product description and agreement, Crude Oil is linked to US oil futures, so it is no surprise that there is a negative value.

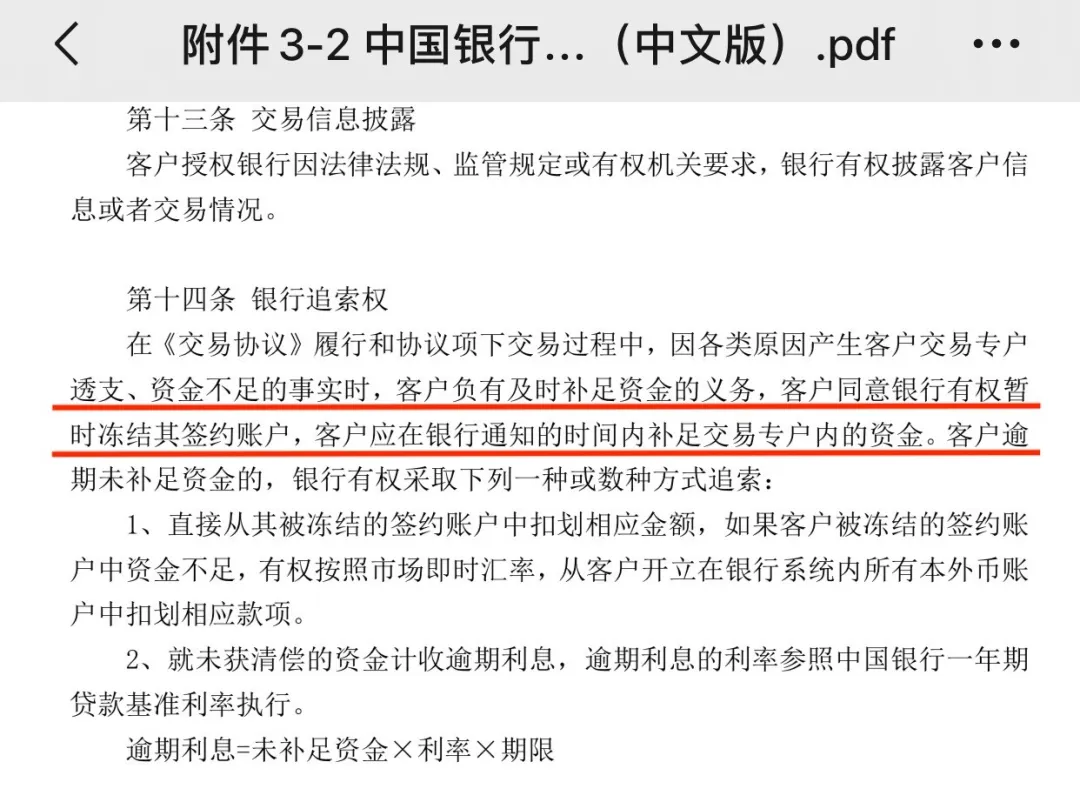

7. The most important question is coming, does BOC have the right to recourse on the “through position” account?

In the “Bank of China Co., Ltd. Personal Account Commodity Business Transaction Agreement” applicable to BOC Crude Oil, there are clear provisions for banks’ right of recourse:

One is to deduct the corresponding amount directly from the frozen contracted account. If the customer’s frozen contracted account has insufficient funds, he has the right to deduct the corresponding amount from all accounts opened by the customer in the banking system at the market’s instant exchange rate.

Second, the overdue interest is charged on the unpaid funds. The interest rate of the overdue interest is implemented with reference to the Bank of China one-year loan benchmark interest rate.