From the perspective of a vertical industry enterprise service head company, an example analysis is carried out to discuss the development status and broad prospects of enterprise service.

Editor’s note: This article comes from the WeChat public account “Yunqi Capital Yunqi” (ID: yunqipartners), author Yunqi Capital Investment Team.

After the epidemic, corporate services are continuously heating up, empowering traditional industries to transform, upgrade, and improve efficiency, and there are many opportunities.

Since its establishment in 2014, Yunqi has persisted in its early and mid-term investments around “Technology-Enhanced Industry Upgrade” , and has been deeply cultivating the layout in the field of “enterprise service SaaS” to build an upstream and downstream linkage ecosystem. Circle, and also made a series of professional research (; Enterprise service investment, where is the way? (2) | Yunqi Report ; ).

This article is mainly from the perspective of vertical industry enterprise service head companies to analyze the actual situation and discuss the development status and broad prospects of enterprise services. Group , on April 24 (Friday), the last session of the Online Demo Day of the Cloud Society business services SaaS special Coming soon, looking forward to meeting with you in the “cloud”, and jointly paying attention to the future of enterprise services.

➤➤➤ Express Express:

● Comparing the service fields of Chinese and American enterprises from various angles, we find that the United States is leading in all aspects, and each subdivided field has a head listed company. It also shows that there is still huge room for development in Chinese enterprise services.

● From an investment perspective, enterprise services are divided into six categories: business management, system management, data analysis, IT infrastructure, general services, vertical industry services . Yunqi Capital is already in IT In-depth layout in areas such as infrastructure and data analysis.

● Increasing opportunities in vertical industries, with engineering, law, insurance, industrial Internet and catering focused analysis of several industries, came to several conclusions:

− In 2017, the output value of the engineering and construction industry was 21.4 trillion, accounting for 1/4 of GDP, but the industry ’s overall informatization level is not high, and traditional software vendors mainly focus onProduction links such as drawing design and cost calculation. In the future, directions such as digital construction sites, smart construction sites and BIM will be the focus of the development of industry technology service providers.

− Compared with the US $ 500 billion legal service market, China ’s legal service still has a lot of room for market development (97.9 billion), With the development of AI and big data technology The technology’s empowerment of legal service scenarios can continuously enhance operational efficiency and reduce service costs .

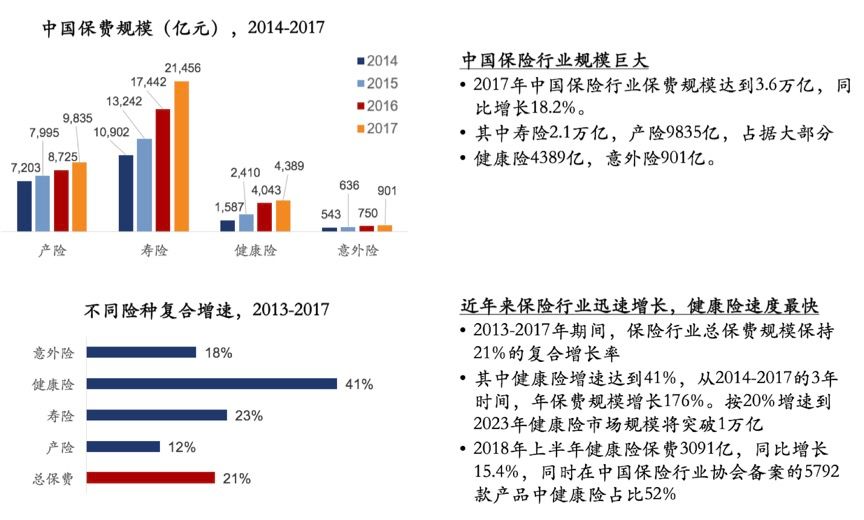

− The scale of China ’s insurance premiums reached 3.4 trillion in 2017, but the share of protective products is relatively low. In the future, protective products based on health insurance will usher in the spring Relying on data technology to serve insurance, insurance, insurance, control and other core links is an opportunity for future startups .

− In the year of 2019, the development of the Industrial Internet has gradually returned to rationality and steadily progressed. It can be seen that the industry application scenarios are constantly plump, and startup companies need to provide value as a criterion for serving customers , Industry solution companies are a better business model .

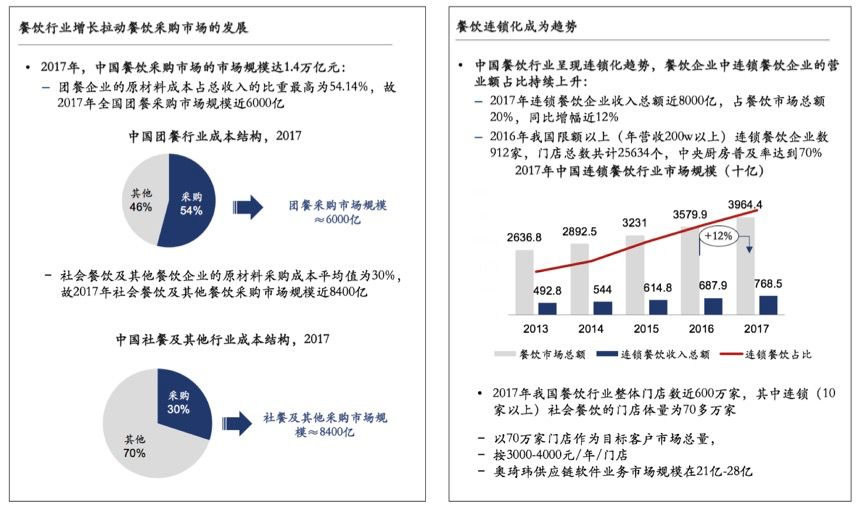

− The catering industry has a large scale (nearly 5 trillion), double high (high dispersion, high elimination rate), and the client has converged to the giant. The current industry integration opportunities mainly Focusing on the back-end supply chain, companies of various models emerge endlessly.

1

Building Technology

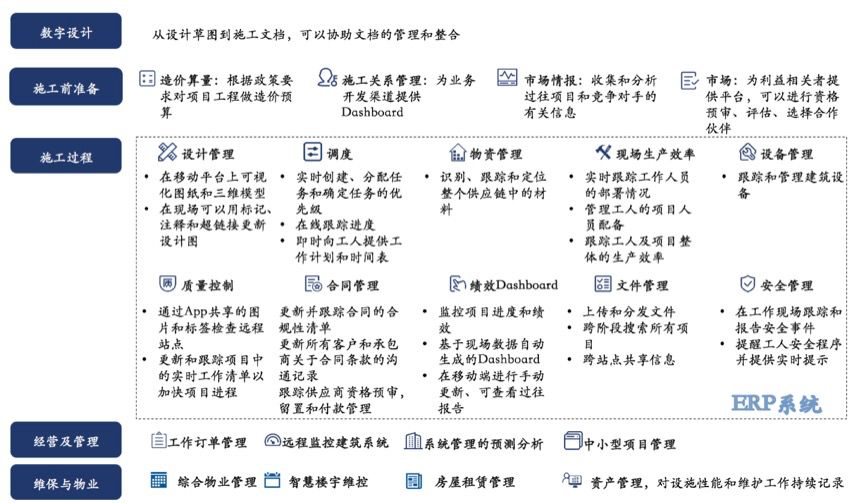

Analyze the application scenarios of house construction technical services, can be applied Complete life cycle of construction and maintenance projects, including digital design, pre-construction preparation, construction process, operation and management, maintenance and property Wait.

(Photo source: Yunqi Capital, McKinsey related research reports, public information)

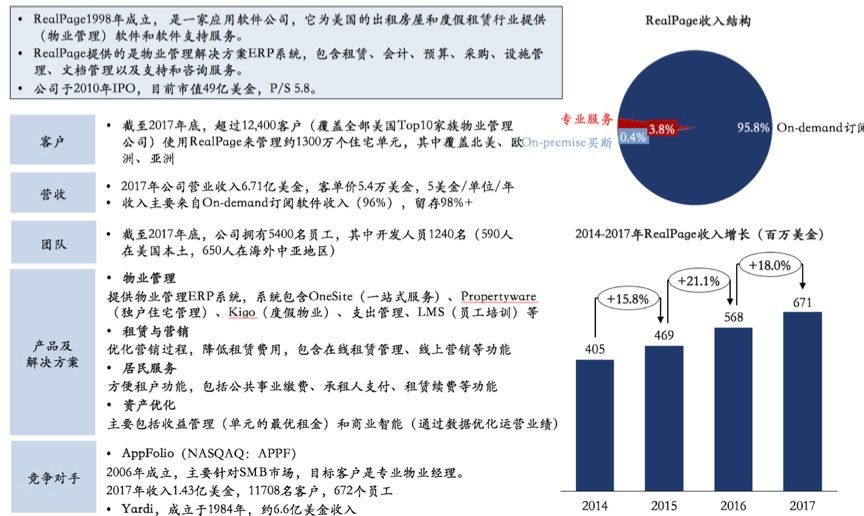

US SaaS company- RealPage

(Photo source: Yunqi Capital, RealPage Annual Report)

Introduction to American construction technology companies

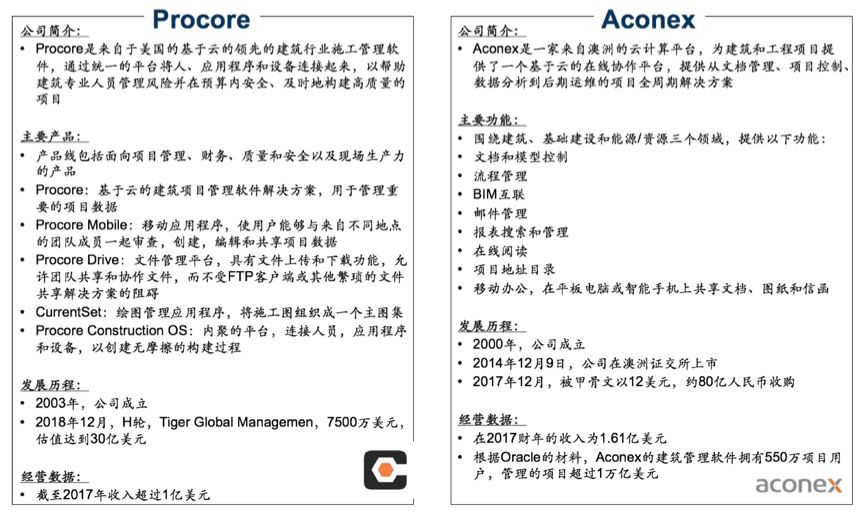

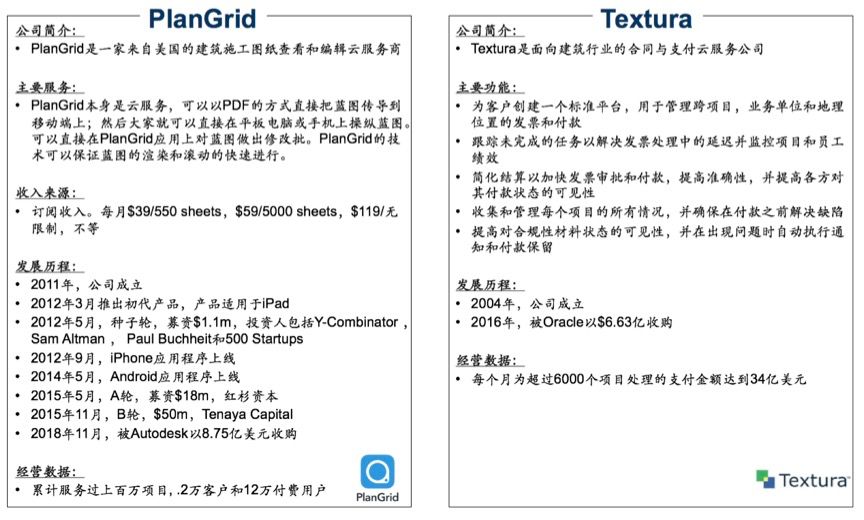

We analyzed four major service providers in the construction industry: Procore, Aconex, PlanGrid and Textura.

(Photo source: Yunqi Capital, public information)

China’s real estate construction market situation

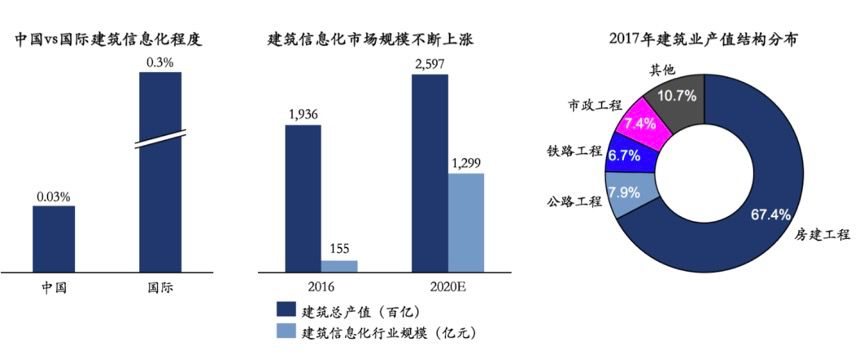

China’s construction industry has a large market volume and rapid growth, and the development potential of construction informatization is huge.

-

In 2017, the total output value of China’s construction industry was 21.4 trillion, a year-on-year increase of 10.5%, accounting for ¼ of GDP.

-

According to the type of project, housing construction accounts for 67.4%, infrastructure (railway, highway, municipal administration, etc.) accounts for 20% +, and other industrial projects (electricity, oil mines, etc.) account for 10%.

-

National construction enterprises 8.80,000, 55 million people in the construction industry, of which more than 10 million are engineering managers, 45 million are front-line workers.

-

There are about 600,000 projects under construction in the country each year. If the average IT budget of a project is 100,000 yuan, the theoretical market scale of building informatization is about 60 billion.

(Photo source: Yunqi Capital, Ministry of Housing and Construction Statistics, China Industry Information Network, McKinsey Report, Northeast Securities Research Report)

Leading company in the field of construction informatization-Guanglianda

In 2017, the operating income was 2.357 billion yuan, the net profit was 494 million yuan, and the market value was nearly 24 billion yuan. The main business was engineering cost.

-

Guanglianda was founded in 1998 and started with the cost of software business. After nearly 20 years of development, the company’s business field has expanded from the bidding stage to the design stage and the construction stage; the product has expanded from a single budget software to nearly one hundred software products in multiple business sectors such as engineering cost, engineering construction, and industrial finance. The company’s next stage goal is to become a platform service provider for the entire life cycle of construction projects.

(Photo source: Yunqi Capital, Guanglianda Annual Report, Ministry of Housing and Urban-Rural Development)

Traditional building information manufacturers

-

Traditional construction informatization companies mainly focus on cost calculation, project management, bidding, etc. Most of the companies have backgrounds in architectural design institutes and construction project management. Ten thousand income level.

-

With the development of new technologies and policy requirements for engineering projects, smart construction sites, BIM has become an emerging direction in recent years.

2

Legal Technology

Introduction to the US legal services market

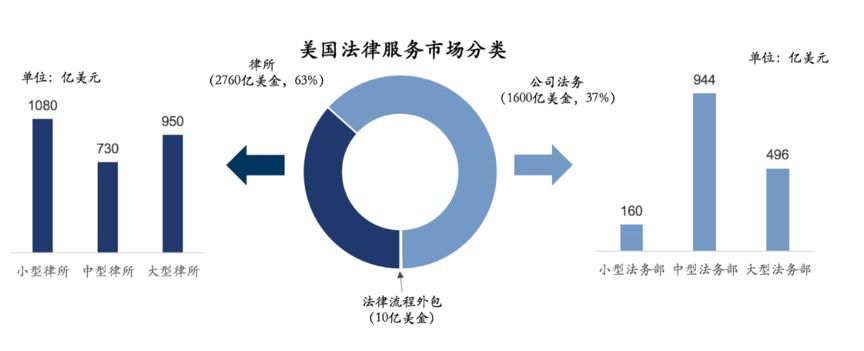

The United States has a relatively mature legal service market with a scale of nearly US $ 500 billion.

-

The US legal services market is huge, with a market size of US $ 437 billion in 2017, accounting for approximately 2% of US GDP.

-

In the United States, there are about 50,000 law firms, 10,000 corporate legal departments, and 1.33 million licensed lawyers (maintaining an average annual growth rate of 1.5% from 2007 to 2018)

-

The legal technology market is worth US $ 16 billion, of which US $ 9.4 billion comes from the law firm ’s service market and US $ 6.5 billion comes from the company ’s legal department ’s service market.

-

In recent years, the main expenditures have been for corporate legal management, contract management and knowledge document management.

(Photo source: Yunqi Capital, Thomson Reuters, Catalyst Research)

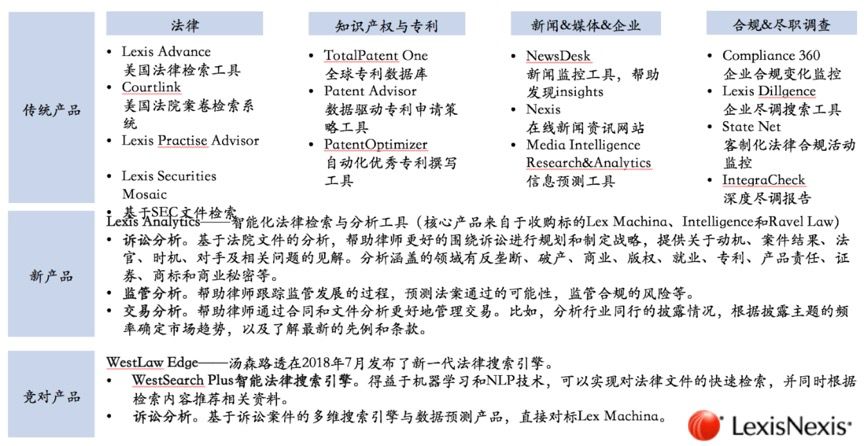

Introduction to the head legal technology company-LexisNexis

LexisNexis is the world ’s largest legal consulting database:

-

The company’s predecessor was Lexis and online news and business information provider Nexis.com (founded in 1979).

-

LexisNexis was founded in 1993 by RLEX Group, the world ’s second largest publishing group, and is mainly engaged in publishing services and online databases for legal, business and other news.

-

The company is headquartered in New York and has more than 18,000 employees. It is mainly divided into two businesses: Legal Professional (65%) and Risk Solution (35%).

(Photo source: Yunqi Capital, LexisNexis official website)

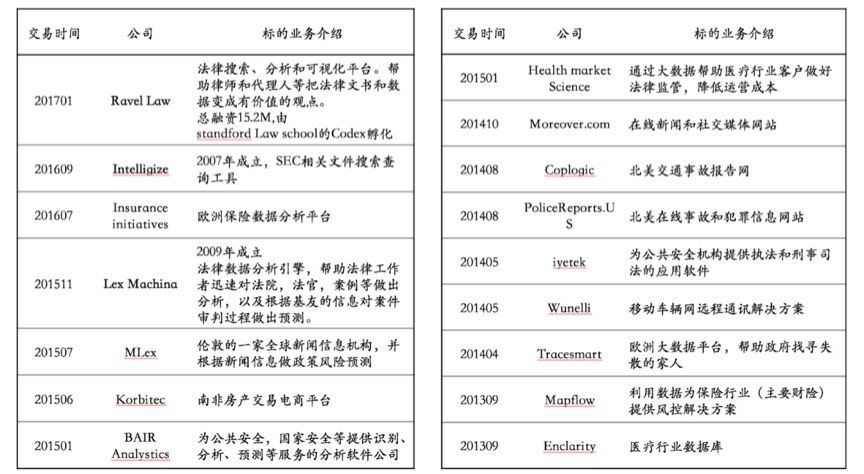

Continuous expansion of products and businesses through mergers and acquisitions:

(Photo source: Yunqi Capital, LexisNexis official website, Crunchbase)

Introduction to the Chinese legal service market

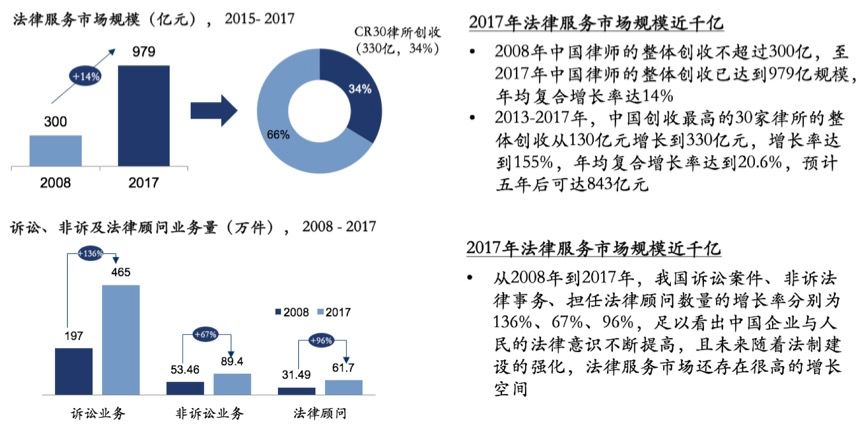

In 2017, the scale of the Chinese legal market reached nearly 100 billion yuan:

-

In 2017, the scale of China ’s legal services market was 97.9 billion yuan. The top 30 law firms generated 33.03 billion yuan in revenue, accounting for 33.74% of the market. The average revenue generated by each law firm was 1.101 billion yuan.

-

As of the end of 2017, there were 28,000 law firms and 365,000 practicing lawyers nationwide, including 323,000 full-time lawyers, 18,000 public lawyers, 12,000 part-time lawyers, and 3800 company lawyers. Assisted 6,600 lawyers and 1,500 military lawyers.

(Photo source: Yunqi Capital, Crunchbase)

China Legal Service Market-Legal Technology

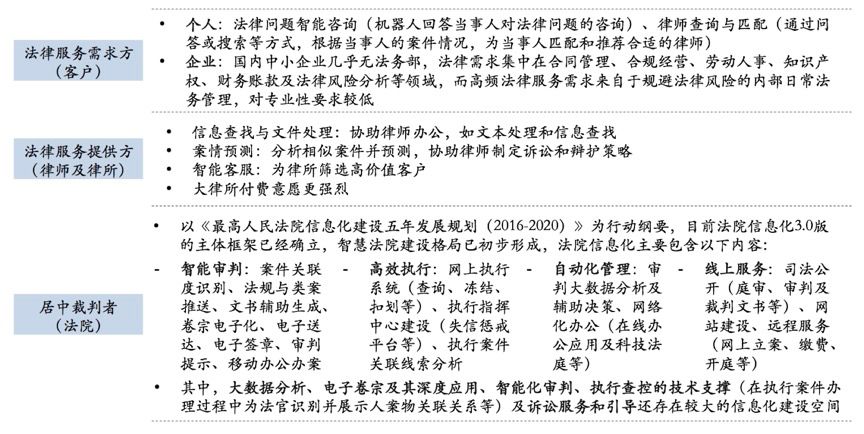

AI technology empowers legal services

-

Participants in legal events have three main bodies, which are: Legal service demand side (individual or enterprise), legal service provider (lawyer and law firm, etc.) and central referee (court and procuratorate) Etc.), Faced with different subjects, AI-based products and services are also different.

-

At present, the application of AI in the legal field is mainly reflected in four forms: information retrieval, document review, case prediction, and intelligent consultation .

(Photo source: Yunqi Capital, Crunchbase)

3

Insurance Technology

US insurance industry environment

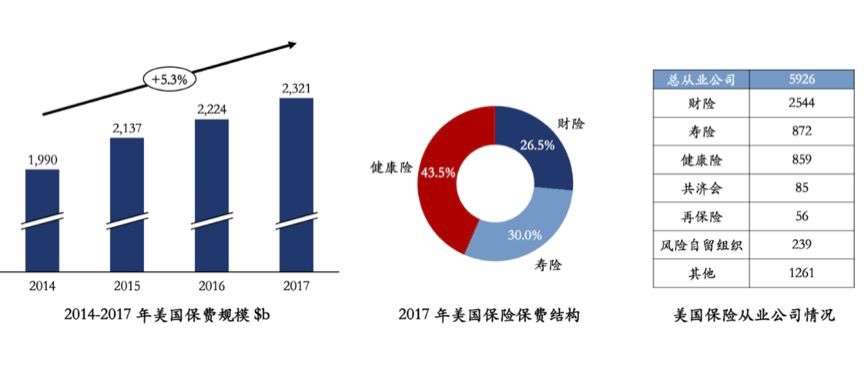

After nearly 300 years of development, the US insurance industry has reached 40% of the global market, with health insurance contributing 43.5%.

-

The first US insurance company was established in 1735 (282 years ago).

-

The United States has the world’s largest insurance market (premium revenue accounts for about 40% of the world’s total). Today, there are more than 5,900 companies with 5 million employees.

-

In 2017, US premiums amounted to US $ 2.3 trillion, mainly from health insurance (43.5%), life insurance (30%) and property insurance (26.5%).

(Photo source: Yunqi Capital, NAIC, IDRR)

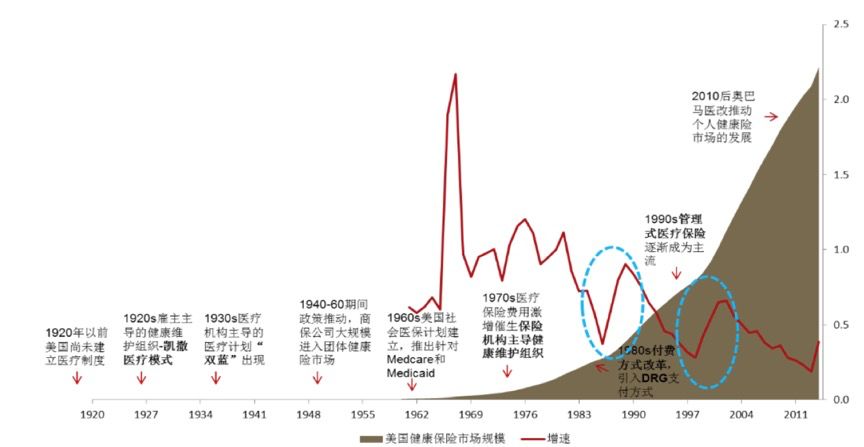

History of the US health insurance industry:

-

From 1920 to 1930, the Caesar model and the “Double Blue” plan emerged, indicating that the United States began to enter the market-oriented medical supply system, which is the initial stage of managed medical care.

-

From 1940 to 1960, commercial health insurance companies entered the group insurance market on a large scale.

-

After 1970, insurance companies led the model of HMO (Health Maintenance Organization) health maintenance organization.

-

In 1983, the United States introduced DRGs (Diagnosis-related Group) payment reform, which greatly improved the ability of health insurance to control fees.

-

Since 1990, managed medical insurance has gradually become mainstream.

-

The 2010 Obama Medical Reform Act ACA has greatly promoted the growth of the personal health insurance market.

(Photo source: Yunqi Capital, Founder Securities)

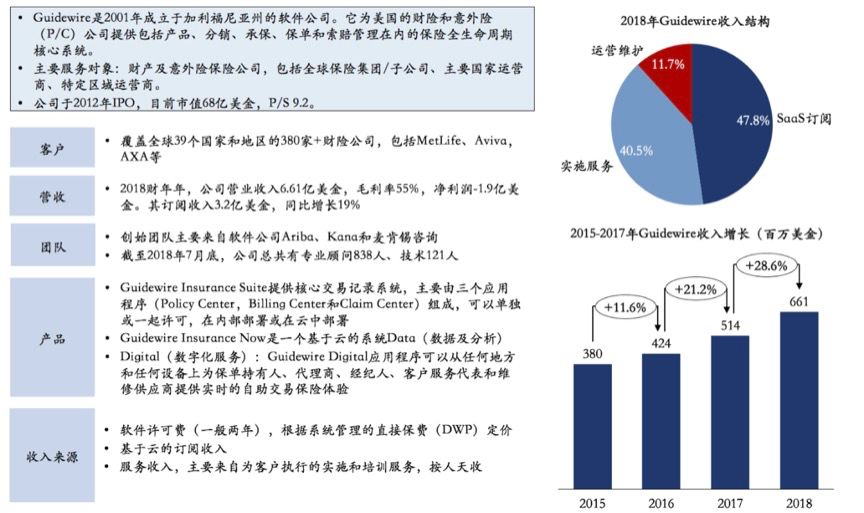

SaaS companies in the US insurance industry-Guidewire:

The following is the introduction of Guidewire:

(Photo source: Yunqi Capital, Guidewire Annual Report)

Introduction to China ’s insurance market

The insurance industry is huge and has grown rapidly in recent years, especially the health insurance business.

(Photo source: Yunqi Capital, China Insurance Association, Chioce)

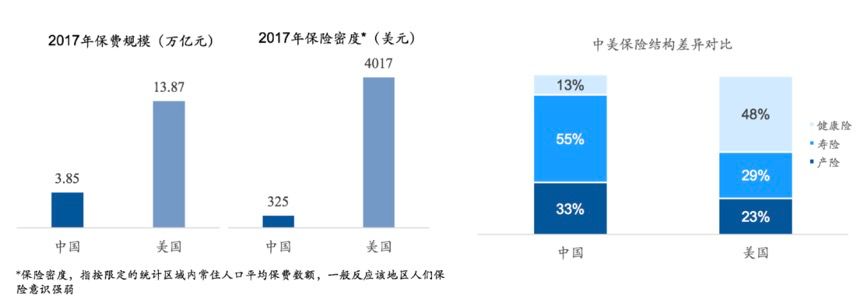

Comparison of China and US insurance market status

Compared with the United States, China’s insurance industry still has great room for development:

-

Comparing with the United States, it is not difficult to see that China ’s insurance industry is still in its infancy. The scale of insurance premiums in the United States is nearly four times that of China, and the insurance density is more than 10 times that of China.

-

In the United States, health insurance is the main expense, which is related to the tax deductibility of employers ’purchase of health insurance. Compared with China, premium income mainly comes from savings-type life and property insurance.

(Photo source: Yunqi Capital, China Insurance Association, Chioce)

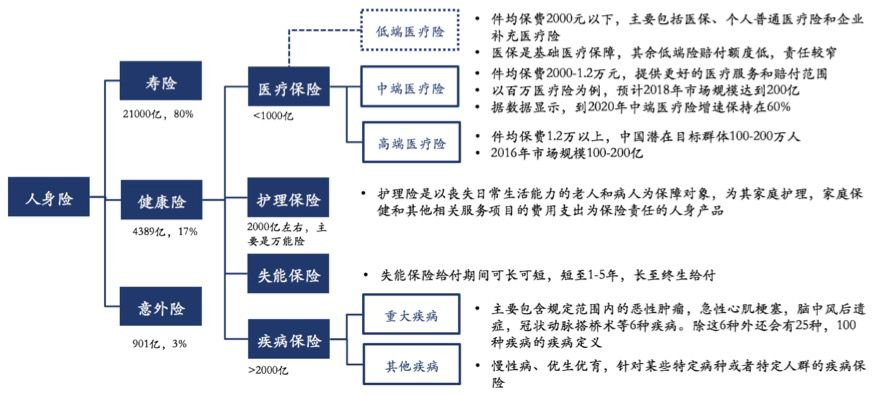

China’s commercial health insurance situation

The health insurance 430 billion market is dominated by wealth management and savings products, and protective products are the focus of development.

(Photo source: Yunqi Capital, China Insurance Association, public information)

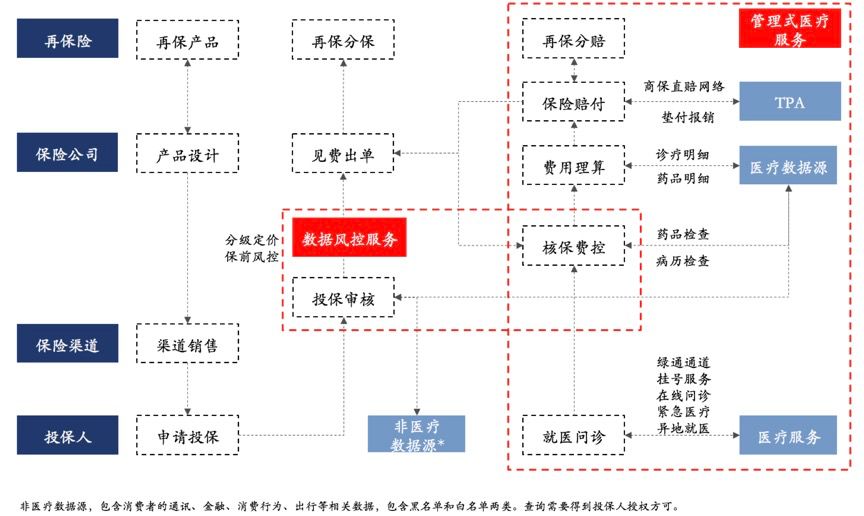

Overview of the commercial health insurance industry chain

Data risk control and managed medical services are the focus of the future.

(Photo source: Yunqi Capital, public information)

4

Industrial Internet

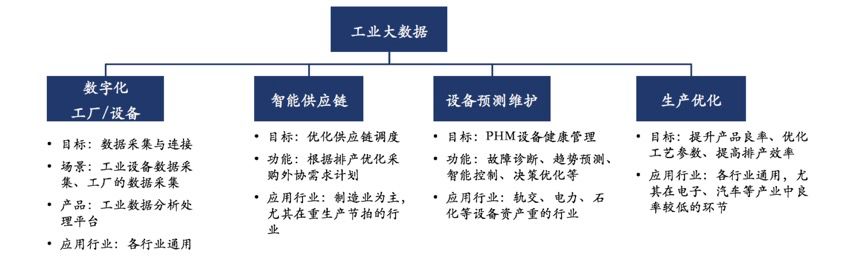

The Industrial Internet has the following four landing directions:

(Photo source: Yunqi Capital, public information)

5

Catering industry

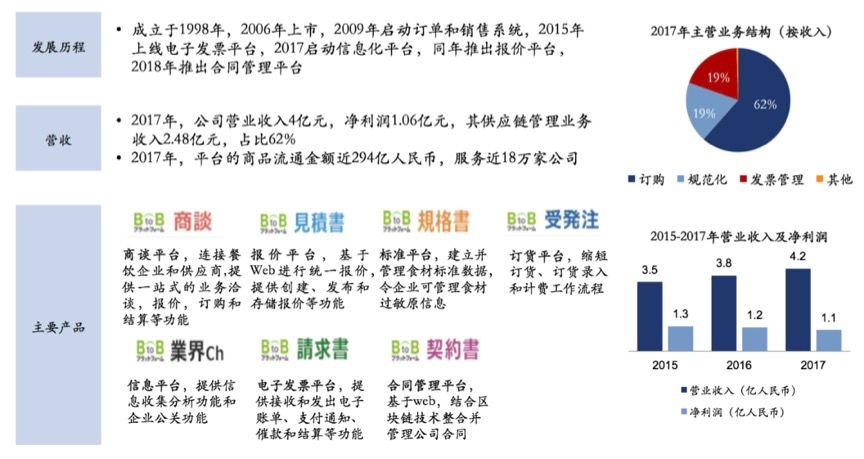

Looking abroad, InfoMart is a leading company in the SaaS industry in the Japanese catering supply chain, with revenue of 400 million yuan and net profit of 110 million yuan in 2017.

-

Founded in 1998 and listed in 2006, it is a SaaS industry leader in the Japanese catering supply chain. In 2017, its operating income was 420 million yuan and its net profit was 110 million yuan.

(Photo source: Yunqi Capital, Infomart Annual Report)

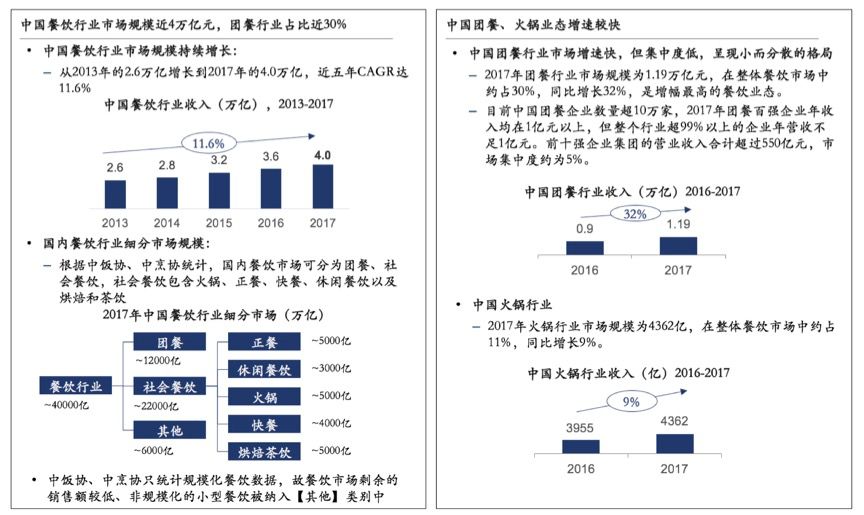

Market scale of catering industry

In 2019, the market scale of China’s catering industry was nearly 4.6 trillion yuan, and the scale of the catering procurement market was nearly one trillion. The chain of catering has become a trend.

(Photo source: Yunqi Capital, Yiou Think Tank, Haidilao Prospectus, etc.)

The above is Yunqi Example analysis from the perspective of vertical industry enterprise service companies , comparing the development and trends at home and abroad, discussing the prospects of China ’s enterprise service venture capital, if you have some information about enterprises The cognition and thinking of the service industry, please feel free to discuss with us.

Meanwhile, April 24 (Friday)

The second “cloud meeting” The last one

“Enterprise Service SaaS Session” will soon open an online roadshow.

Welcome to scan the code to register, after review, we will

Send the Zoom online roadshow link (each link is limited to one person only) and project manual details via email ,

Remaining places are limited, sign up from, looking forward to meeting you in the “cloud”.

About Yunqi Capital

Since its establishment in 2014, Yunqi Capital has always focused on early and mid-term investments in “technologically empowered industry upgrades”, covering industries such as artificial intelligence big data, enterprise SaaS and services, B2B supply chain platforms, intelligent equipment, and advanced manufacturing. The investment portfolio includes Nearly 100 excellent startup companies such as PingCAP, Coca-Cola, Qinglang Technology, Bingjian Technology, ZILLIZ, Find Steel Net, Baibu, Gongpinhui, Wisdom Tooth Technology, 360 Finance, Zhongtian Anchi, and Neolithic.

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-