Ping An Group’s five major ecosystems, namely “financial services, healthcare, auto services, real estate services, and smart cities”.

Editor’s note: This article is from Economic Observer Online , Author: Hu Group, reproduced with permission

Consumer financial institutions are expanding again. This time it is Ping An Consumer Finance Co., Ltd. (hereinafter referred to as “Ping An Consumer Gold”) whose shareholders are players across multiple industries such as finance and technology.

On April 23, Ping An Consumer Gold officially opened in Shanghai. From the approval of the Shanghai Banking and Insurance Regulatory Bureau on April 9 to the official opening, it took only 2 weeks for Ping An Consumer Fund, which shows that its preliminary preparations are sufficient.

Another member of the fintech organization of the Department of Ping An. Ping An Consumer Finance is a national technology-based consumer finance company initiated and established by China Ping An Insurance (Group) Co., Ltd. as the main investor with the approval of the China Banking and Insurance Regulatory Commission. The company is located in Pudong New Area, Shanghai, with a registered capital of RMB 5 billion.

According to the disclosure, Ping An Consumer Finance ’s shareholding structure contributed RMB 1.5 billion from China Ping An Insurance (Group) Co., Ltd., accounting for 30% of the company ’s registered capital; Rongyi Co., Ltd. contributed RMB 1.4 billion, accounting for the company ’s registered capital 28%; Wei Kun (Shanghai) Technology Services Co., Ltd. invested RMB 1.35 billion, accounting for 27% of the company’s registered capital; Jin Jiong (Shenzhen) Technology Services Co., Ltd. invested RMB 750 million, accounting for 15% of the company’s registered capital.

By penetrating the equity relationship, the equity structure behind Ping An Consumer Finance is that China Ping An Insurance (Group) Co., Ltd. accounts for 30% of the company ’s registered capital, and Lufax Holding ’s related company shares account for 70%.

Ping An Consumer Finance Chairman Chen Dongqi said that as the first consumer finance company to be positioned as “technology + finance”, Ping An Consumer Finance will take the mission of “being a companion run-up for China’s upward young power” and serve the young and progressive in China. The consumer finance customer group provides a full-line premium consumer credit experience to meet their consumption upgrade needs, and is committed to building the first consumer finance brand exclusively for young people in China.

As China’s economic restructuring process accelerates, the consumer finance industry is also evolving. With the establishment of a number of consumer finance companies, the competition in the consumer finance industry is becoming fiercer. At the same time, commercial banks continue to sink their service focus and vigorously develop consumer loan business. Related business entities also participate in the consumer finance industry in various forms. Expand the scope of its business.

Previously, many banks such as China Merchants Bank, Industrial Bank, Postal Savings Bank of China, Bank of China, Bank of Beijing and other banks had obtained consumer finance licenses. However, the Department of Ping An did not obtain the Banking Regulatory Commission to build a consumer finance company until late November 2019.

Although Ping An Consumer Finance has a relativelyLate, and has been cultivating in the field of consumer finance for many years, and once opened, it has shown its “ambitions” to the market. The registered capital of Ping An Consumer Finance is 5 billion yuan, second only to Gitzo (7 billion) in the current market, higher than Immediate Consumer Finance (4 billion) and China Merchants Consumer Finance (3.868 billion).

Chen Dongqi said that Ping An Consumer Finance relies on the Ping An Group ’s scientific and technological strength and the five major ecosystems to cut into consumer credit scenarios, constantly consolidate the “smart +” ecological layout capabilities of the entire scenario, and will build a service ecosystem based on scenarios.

The five major ecosystems of Ping An Group are “financial services, medical and health care, automotive services, real estate services, and smart cities.” In the face of a new wave of technological revolution, Ping An Group has continued to promote the “financial + technology” and “financial + ecological” strategic transformation in recent years. According to China Ping An Annual Report, the number of technology patent applications in 2019 reached 21,383, an increase of 9,112 from the beginning of the year Items, of which the number of published patent applications in the fields of financial technology and digital medical technology ranks first and second in the world, respectively.

At present, Ping An Financial Services Ecosystem provides diversified financial services covering insurance, banking, and investment fields, achieving seamless connection and closed-loop transactions in various financial consumption scenarios, and completing assets and funds through “open platform + open market” The online link of the company has landed on multiple financial innovation platforms such as Financial One Account, One Wallet, etc., to meet customers’ all-round financial needs. China Ping An ’s annual report disclosed that as of December 31, 2019, the total number of APP users of core financial companies had reached 345 million, an increase of approximately 70.34 million from the beginning of the year.

Xu Weidong, associate professor of Hangzhou University of Electronic Science and Technology, said that from the information available, Ping An Consumer Gold will follow the road of technology-based consumer consumption and ecological consumer consumption. The way to acquire customers is not the marketing dimension like traditional banks, but to acquire customers in the Internet scene. Together with a wide range of online and offline partners, we will jointly mine customer consumption needs from the scene. This is the future of safe consumption. The dream is not as simple as market speculation to undertake P2P transformation, or Ping An inclusive business.

Currently, affected by the epidemic, consumption is still hovering at a low level. Immediately Consumer Finance founder and CEO Zhao Guoqing told the Economic Observer that the long-term upturn in China’s consumer finance industry will not change because of the epidemic. Under the effective control of the domestic epidemic, domestic demand consumption will gradually recover, the leading role in driving the economy will be more obvious, and consumer finance will continue to play a more important role in driving domestic demand, promoting consumption upgrades, and serving the real economy.

Ping An Group, which is backed by Ping An Group, is clearly gaining momentum, and the competition in the consumer finance market will become more intense in the future. Compared with the leading consumer finance companies in the current market, Ping An Consumer Gold was born in the face of adversity, can it win the favor of young Chinese in the wind and rain? After all, quite a few young people are now accustomed to using products such as Gitzo, China Merchants Finance, and Immediate Finance, and even Huabian borrowing and Jingdong Baitiao.

Recently, Gitzo, China Merchants Finance, and Immediate Finance have all raised funds by issuing ABS and financial bonds. Through the relevant documents, we can see some of the operating data of the above three companies.

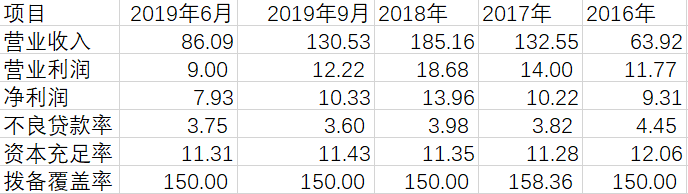

Data source: Gitzo Financial ’s 2016-2018 audit report and unaudited financial statements for the third quarter of 2019

As one of the first consumer finance pilot companies, Gitzo currently has more than 290,000 POS Point-of-Sales in China, with about 43,000 full-time employees. As of the end of September 2019, Gitzo Financial achieved a net profit of 1.033 billion yuan, the amount of new loans issued was approximately 69.547 billion yuan, the loan balance was 92.653 billion yuan, the capital adequacy ratio was 11.43%, and the non-performing loan rate was 3.60%. Both the capital adequacy ratio and the core tier one capital adequacy ratio are 10.49%.

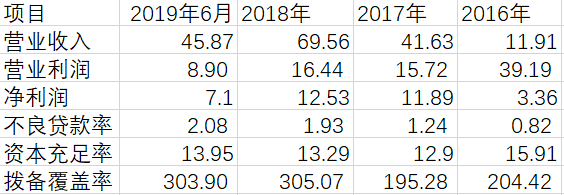

China Merchants Consumer Finance Co., Ltd.’s 2020 third phase financial bond issuance document

China Merchants Finance is the first consumer finance company in China to be positioned as “Internet Finance”. As a consumer finance company jointly established by China Merchants Bank and China Unicom, China Merchants Bank has received strong support from shareholders in terms of brand, channel, capital, risk management, etc. Unicom’s huge customer resources and network resources to expand customers, you can also use the bank’s mature risk control system. In the past three years and the end of the first half of 2019, China Merchants Financial achieved net profit of 336 million yuan, 1.189 billion yuan, 1.253 billion yuan and 710 million yuan respectively, with a compound annual growth rate of 92.99%. However, its non-performing loan ratio is also rising. In the past three years and the end of the first half of 2019, the non-performing loan ratio was 0.82%, 1.24%, 1.93% and 2.08%, respectively.

According to China Merchants Bank’s 2019 annual report, as of the end of the reporting period, China Merchants’ total assets were 92.697 billion yuan and net assets were 9.36 billion yuan; during the reporting period, it achieved a net profit of 1.466 billion yuan.