Restore the real central bank digital currency.

Editor’s note: This article comes from the WeChat public account “Xuehongyan Weiyu” (ID: hongyanweiyu) , author: Xue Hong Yan Su Ning, vice president of financial research.

Everyone loves RMB. The central bank’s digital currency is getting closer and closer, igniting everyone’s enthusiasm. Some people make up for currency knowledge and care about “what”, “why” and other knowledge; some people are keen to eat melon, “how to do Alipay”, “what is the prospect of Bitcoin”, “the fatal blow to the dollar hegemony” And other topics.

Fighting Alipay, kicking bitcoin, and challenging dollar hegemony, I have to say that too many melons in the entertainment industry have been eaten in the financial sector. What is the truth? In this article, we try to answer them one by one. The reason is to try to answer, because any unofficial interpretation has a subjective guess.

What is the central bank digital currency?

The central bank’s digital currency is first and foremost a currency.

What is the currency? Currency is a unit of account and a lubricant for economic activity. You can think of currency as a bill of lading, which corresponds to the right to claim goods and services, so currency has also become a symbol of wealth-people hold and store currency, which is intended to be exchanged for the goods and services they need one day.

Regarding currency, the economist Hyman Minsky has a famous saying, “Everyone can create currency, but the question is whether it can be accepted.” Meaning, everyone in the economic sense Can issue currency, but not everyone’s currency can be accepted by the public. Some people are willing to accept bitcoin, so bitcoin can also exercise its currency function within a certain range and become a “virtual currency” (many countries, including China, do not recognize its currency attributes).

In the modern economic context, currency usually refers to fiat currency, issued by the central bank, with legal and compulsory characteristics, and no one within the national boundaries can refuse to accept it. Renminbi is China’s legal currency, corresponding to different currency forms: paper currency is renminbi, behind bank deposits is renminbi, and central bank digital currency is also renminbi.

So, what is central bank digital currency? You can understand it as a renminbi in digital form. Since they are all renminbi, they can certainly be exchanged between different forms-digital currencies can be exchanged for cash or bank deposits. Conversely, cash and deposits can also be exchanged for central bank digital currencies.

The question is coming, cash and demand deposit accounts have been able to meet everyone’s payment needs. From the user’s perspective, why do we still need the central bank’s digital currency?

Indeed, when experts analyze the necessity of central bank digital currencies, they are mostly based on the perspective of central banks and financial institutions. For example, compared with cash, digital currencies can save printing costs, and there is no problem of damage and replacement and escort transportation. Reduce the cost of cash management in the financial system; compared with bank deposits, digital currency can trace the flow of funds, small to prevent credit funds from entering the stock market and property market, and most of them play a role in anti-money laundering and anti-terrorism financing.

What are the benefits to the people? The advantage is anti-theft and anti-theft, because it can be traced back, and it is not afraid of theft; the inconvenience is to re-cultivate a currency usage habit.

Of course, do n’t worry, maybe more and more scenarios will support digital currency in the future, but all scenarios will be compatible with cash and card payment. For users, whether they use central bank digital currency or not will not affect our daily life at all.

Central Bank digital currency, will replace cash?

To a certain extent, the issuance of digital currency by the central bank is also a trend that follows the trend of “cashless society” and provides a better payment carrier for the digital economy. Will central bank digital currency replace cash? will not.

The term “cashless society” was a big hit in 2017. Not only did the payment giants take advantage of the publicity, but even some merchants began to reject cash, which caused a lot of controversy. . Since then, no one has promoted a “cashless society”, but the “cashless society” has not stopped infiltrating.

The use of cash bears a large cost of operation and management. The state has always encouraged the reduction of cash use in economic activities. For example, the “Provisional Regulations on Cash Management” issued in 1988 clearly states that “the State encourages account opening units and individuals to use economic transfers for settlement in economic activities to reduce the use of cash.” For enterprise units, it is clearly specified that they can only be used under limited conditions Cash cannot exceed a certain amount, otherwise it is suspected of being illegal. Without him, cash payment is difficult to track the flow of funds. Large cash transactions are often the hardest hit areas of gray transactions and illegal transactions. From the perspective of the enterprise, large cash payments will also bring problems such as anti-counterfeiting identification and cash storage, and are generally more inclined to accept electronic transactions.

But for small and sporadic transactions, cash has an irreplaceable advantage. The biggest advantage is its high flexibility and universality of the scene. It does not need to rely on third-party equipment and networks, and can be used for transactions anytime, anywhere. Groups and almost all small amount scenes. Looking back at the past, mobile payment is a siege, but no matter how smart the technology is, it is inevitable that there is a BUG. At this time, cash is the last security pad to ensure that the payment goes smoothly.

At the same time, considering the complexity of the currency payment scenario and the complexity of the customer base, the unimpeded approach of first- and second-tier cities may not be suitable for counties, and the payment methods sought by some people (such as young people) are not representative.Everyone’s choice. And cash is used by everyone.

Finally, the anonymity of cash is an unparalleled advantage. Most of the time, people do n’t mind that financial institutions have their own capital records, but there are also many times when people want some transactions to “know you know what you know”. Bitcoin and other “virtual currencies” were once favored for their anonymity characteristics, but it turns out that cash is truly and completely anonymous. In a sense, the traceability of the central bank’s digital currency will further highlight the anonymity of cash.

So, the central bank digital currency can replace cash in many scenarios, but not in all scenarios. In the foreseeable future, cash will still lie quietly in the wallet and accompany us.

Central Bank digital currency, let users abandon third-party payment?

In addition to cash, many people are worried that Alipay and WeChat Pay are in a leading position. Technically, the central bank’s digital currency can be “de-intermediate” for peer-to-peer transactions. As long as merchants and consumers have opened the central bank’s digital currency wallet, the two wallet addresses can be directly traded. There is neither mobile payment nor banking. what’s up.

However, the central bank issued digital currency naturally does not want to really “de-intermediate”, the two-tier operating mechanism of “central bank-financial institution-user” is still adopted. Users open accounts in financial institutions and do not directly conduct business with the central bank relationship.

The problem is coming, the central bank’s digital currency operates in two layers, and the third-party payment is a three-layer structure: the central bank-the bank-(UnionPay / Wanglian)-the third-party payment-the user. The central bank’s digital currency clearly states that it needs a bank account, and does it need a third-party payment account?

Theoretically, it is not necessary, just like when no third party pays, the payment transfer transaction will operate as usual. As far as the existing clearing and settlement system is concerned, third-party payment is an enhancement of the experience level, which is icing on the cake and has never been a necessity. The same is true of central bank digital currencies, without third-party payment, there will be no real impact.

The central bank’s digital currency is a new battlefield, and users are used to nurturing from zero. Now, the bank APP is the first to pilot, and the first-mover advantage is not here in third-party payment.

Of course, you do n’t have to overstate the impact. From the user’s point of view, there is no essential difference between the central bank’s digital currency and cash and bank card balances. Its early adopters can attract a small number of young groups who are seeking change. It is a long-term and gradual process to be accepted by the public. In this long process, the first-mover advantage brought by the bank’s first pilot is negligible.

Finally, the rise of third-party payment is not a product of regulators ’intentional promotion or spontaneous breeding of the financial system, but a reform and innovation catalyzed by market demand. In line with market demand, users are used to becoming the largest moat for third-party payment. As long as the user experience does not decline, third-party payment has vitality.

In the final analysis, the competition for payment has always been the competition of scenes and experiences.

Central Bank digital currency crushes the living space of Libra and Bitcoin?

Does not recognize the “virtual currency” currency attribute in China, and Libra and Bitcoin have no living space in China. The so-called central bank digital currency crushes the living space of Libra and Bitcoin, and more points to cross-border markets.

Libra and Bitcoin are both positioned as international currencies. Relying on blockchain technology, they are not restricted by national borders or the existing international settlement and settlement system. Under the background that many countries consider virtual currencies illegal, cross-border scenarios become The fundamental source of the vitality of virtual currency.

At the technical level, the central bank digital currency can significantly enhance the cross-border payment experience, but the central bank digital currency, as China ’s legal national currency, has a sovereign national color and does not have non-sovereign currencies such as Libra and Bitcoin at the level of international acceptance. Flexibility. For example, some countries such as Japan accept Bitcoin as a payment tool, but it is impossible to accept RMB for their domestic transaction scenarios, which involves currency sovereignty issues.

So, we can compare the “virtual currency” spontaneously bred in various markets from a technical level, but we cannot simply define the sovereign currency technically. Sovereign currency is an economic issue, a financial issue, a social issue and a political issue. It is not a technical issue.

The essence of central bank digital currency is RMB, and RMB is the legal currency of China. The internationalization of central bank digital currency is equivalent to the internationalization of RMB. But the internationalization of the renminbi has never encountered a technical bottleneck. Behind it is the powerful inertia of the dollar hegemony system and the power game between the big powers.

Therefore, the influence of the central bank’s digital currency in cross-border payments will not exceed the scope of RMB internationalization. There is no real pressure on “virtual currencies” such as Bitcoin and Libra.

The real pressure on Bitcoin and Libra comes from various sovereign countries. Bitcoin imagined the establishment of a currency system that spans sovereignty and global circulation. Its early anti-inflationary logo did attract some people, but currency has never been a protagonist of society, but only an accessory tool. What kind of society and economy there is corresponds to what kind of currency system; how can there be a unified currency in the world without a society with the same world?

Of course, the world is so big, and the ideal of world harmony still has room to live. Accordingly, Bitcoin and Libra can always find a foothold; however, it is also limited to a foothold.

Central Bank digital currency, challenging the hegemony of the US dollar?

What is dollar hegemony?To put it simply, the US dollar as an international hard currency gives the United States a unique advantage-when money is needed, the United States only needs to start the money printing machine, and other countries can only exchange it for commodities, as former French President Charles de Gaulle said, < / p>

“The United States enjoys the super privilege and tearless deficit created by the US dollar. It uses worthless waste paper to plunder the resources and factories of other peoples.”

Since the global resources and commodities are denominated in US dollars, then theoretically, the United States can operate the printing machine to buy all the commodities and assets needed globally. For ease of understanding, imagine an extreme situation: all Americans do not work, and they can live a happy life by buying and buying on the world by printing money from the Federal Reserve (in fact, American consumers have always spent more than income and earned 1 It costs 2 yuan for each dollar, which cannot be separated from the support of dollar hegemony).

Of course, there will actually be constraints. When the US currency printing is too excessive, it will cause the US dollar to depreciate and shake the world ’s confidence in the US dollar. Central banks will turn to other alternative assets such as gold or the euro and shake the hard currency of the US dollar. status. The problem is that there is still no real competitor for the dollar in the world.

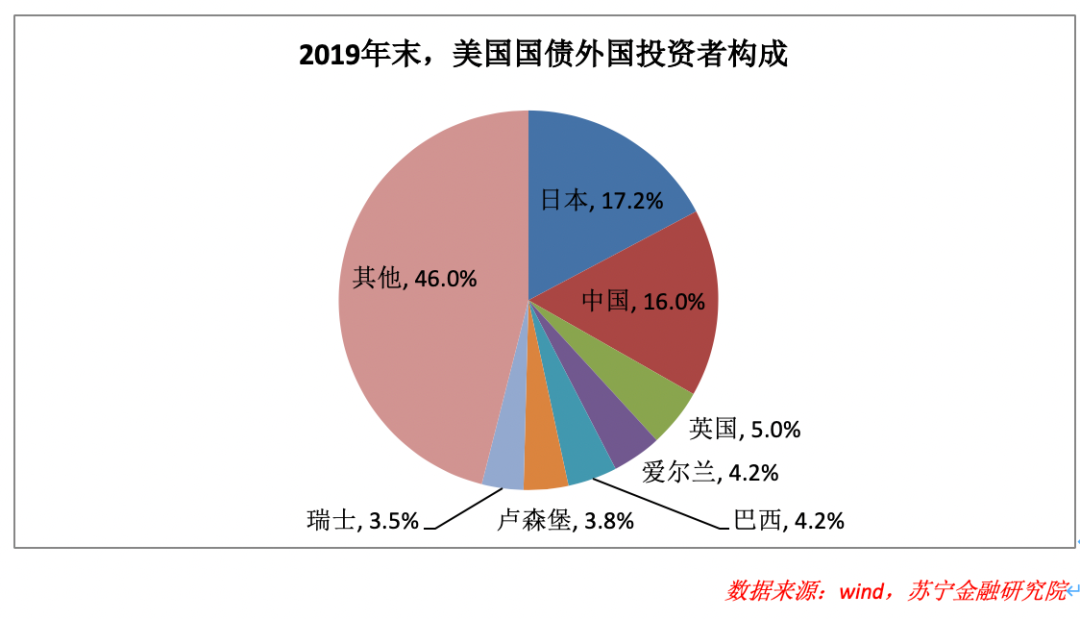

After the new crown epidemic, the Fed once again launched an epic “big water release”, and opened the motor to print money, but the US dollar appreciated. Because the outbreak of the global outbreak, hedging funds have nowhere to go, only to go to the United States and buy US debt. At the end of 2019, foreign investors held a total of US $ 6.7 trillion in US Treasury bonds, accounting for approximately 30% of the outstanding balance of US Treasury bonds.

The hegemonic status of the US dollar has made many of the Fed ’s “god operations” fearless, giving birth to various cases of “dollar-cutting leeks” that have been widely circulated in the world, which has distorted the international financial system.

There should not be only one kind of hard currency in the world. After the 2008 financial crisis, many countries could not bear the “American sneeze, global cold” drama, and set off a wave of “finding dollar replacements” around the world. Many countries have turned their attention to the renminbi, objectively promoting the acceleration of the internationalization of the renminbi; but China has turned its attention to a super-sovereign currency-SDR (special drawing rights, anchoring the dollar, euro, yuan, yen and pound sterling, etc. The basket of currencies can be used to repay the IMF’s debts and make up for the balance of payments deficits among member governments.)

In 2009, Zhou Xiaochuan, then governor of the central bank, proposed to better play the role of SDR to promote international trade and bulkSDR pricing is used in commodity pricing, investment, and corporate accounting, which in turn creates an international reserve currency that is decoupled from sovereign countries and can maintain long-term currency stability.

Now, SDR does not replace the US dollar. Looking around, the US dollar has no rivals: the euro is trapped in the financial crisis of EU countries, the Japanese yen is dragged down by Japan ’s “lost thirty years”, and the pound is the hegemon of the last era. After looking around, people will still focus on the RMB.

RMB internationalization is a reflection of China ’s global economic impact at the financial level. There is still a long way to go to upgrade China ’s economic structure, improve quality and increase efficiency. Naturally, RMB internationalization cannot be achieved overnight. The central bank’s digital currency can enhance the experience of the RMB at the level of cross-border transactions, which is nothing more than unnecessary interpretation.

The international financial system should not be limited to the US dollar, nor does the international financial system expect another dollar. The dollar today will not be the renminbi tomorrow. The renminbi needs to find a new way to integrate into the world as a tool for mutual benefit rather than a tool for “cutting leeks”.

Reference:

1. [US] Nouriel Roubini, Stephen Meme, “Crisis Economics”, Zhejiang People’s Publishing House, 2018.