Vertical middlemen are getting harder and harder to do.

Editor’s note: This article href=”https://mp.weixin.qq.com/s/Ai4zir7_ZBSrVBa4hiMamQ”> “Capital detective” from the micro-channel public number , Author: Hong key.

In recent months, the luxury industry has been particularly lively.

On the one hand, brands have accelerated the digitalization process in China. For example, LV, Prada, Dior and Burberry have settled on WeChat video numbers; Prada, Armani and MiuMiu have successively landed on Tmall; LV is even on the Xiaohong book The first e-commerce live broadcast was conducted.

On the other hand, luxury e-commerce platforms are also constantly moving. On January 30, Farfetch, a British luxury e-commerce platform, announced that it had received a US $ 125 million investment from Tencent. In March, Wanlimu, a cross-border luxury shopping platform under Qudian, went online and launched a luxury goods price war with the “10 billion subsidy” project.

The high-cold big names are becoming more and more “grounded”, and new players who see online luxury opportunities are entering the market to stir the pattern, so the industry has added many variables.

For Siku, a luxury shopping service platform founded in 2008, big brands go online as an opportunity, but the new competitive environment poses greater challenges and may exacerbate its existing predicament.

On April 30, Siku Group released the fourth quarter and full-year performance report for 2019. The core financial indicators for the fourth quarter are as follows:

-

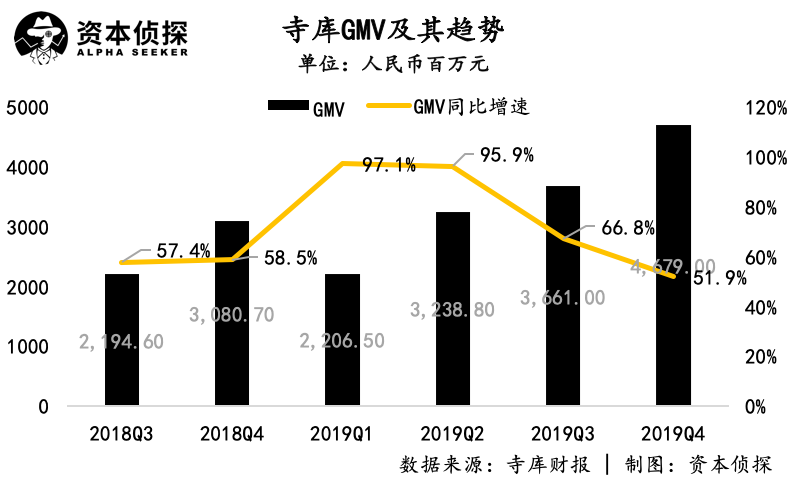

GMV is 4.679 billion yuan (no special instructions, the unit is RMB), an increase of 51.9% year-on-year;

-

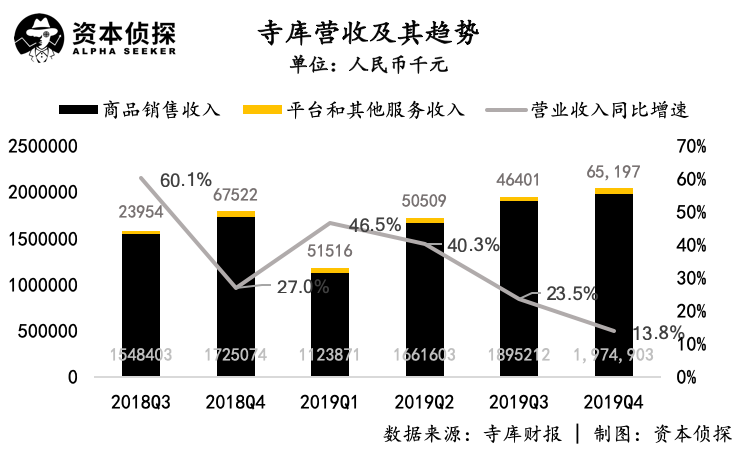

Revenue was 2.04 billion yuan, a year-on-year increase of 13.8%;

-

The net profit attributable to shareholders of ordinary shares was 40.99 million yuan, compared with 46.47 million yuan in the same period last year;

-

Non-GAAP ’s net profit attributable to shareholders of ordinary shares was 40.75 million yuan, compared with RMB 52.91 million in the same period last year.

In the annual performance:

-

GMV was 13.785 billion yuan, a year-on-year increase of 71.3%;

-

Revenue was 6.869 billion yuan, a year-on-year increase of 27.5%;

-

Net profit attributable to shareholders of ordinary shares was 154 million yuan, compared with 152 million yuan in 2018;

-

Non-GAAP ’s net profit attributable to ordinary shareholders is 163 million yuan, compared with 176 million yuan in 2018.

Compared with e-commerce peers who traded money for scale, Siku has always maintained a profitable state, but its performance in the capital market has been unsatisfactory. After listing on the Nasdaq in 2017, Seco’s stock price has continued to decline, and now it floats around $ 3, which is more than 75% lower than the issue price of $ 13.

Continued profitability, but the stock price is sluggish. Such an example is not uncommon in the capital market. Capital wants to grow more than profit.

Image source: Snowball

Despite Siku ’s attempt to change the label of “luxury e-commerce” to “premium lifestyle platform”, judging from its financial performance, the sale of luxury goods is still its biggest basic market, and it relies too much on verticals. This has caused Siku’s growth dilemma today.

01 Growth frustrated, cut costs and ensure profits

Siku ’s GMV increased by 51.9% year-on-year in the fourth quarter of 2019, but compared with the previous nearly doubled growth, this quarter ’s growth rate declined significantly. From the first quarter of 2019, Seco’s GMV growth rate has continued to decline.

The decline in GMV growth rate corresponds to the dilemma of revenue growth. In the fourth quarter of 2019, Siku ’s revenue was 2.04 billion yuan, which was lower than the lower limit of the performance guidance range. Throughout 2019, the quarterly growth rate of Siku’s revenue continued to decline, and the 13.8% growth in the fourth quarter was significantly lower than the previous level.

The main source of Siku ’s revenue is sales revenue and

-