Huya and Douyu have their own strengths and weaknesses in financial data.

Editor’s note: This article is from the WeChat official account “Node Finance” (ID: jiedian2018), author of the node Finance .

After the domestic live broadcast industry experienced the “thousand broadcast war”, only two US stock-listed live broadcast companies, Huya and Douyu, were in charge. Recently, Huya and Douyu respectively released their 2020 second quarter financial reports. Following the release of the financial report, the two companies also issued an announcement stating that they had received a non-binding preliminary proposal from the major shareholder Tencent, suggesting that the two companies merge by way of share swaps.

Data from the Mob Research Institute and the China Business Industry Research Institute show that as of the first quarter of 2020, in the list of active users of China’s game live broadcast platform, Huya Live has topped the list with approximately 31.68 million active users. Douyu has 25.2 million active users ranked second. As of the close of US stocks on August 20, Beijing time, the total market value of Huya was 5.39 billion US dollars and the total market value of Douyu was 4.68 billion US dollars.

This means that if the two companies merge, a new live broadcast platform with a market value of over US$10 billion and a market share of nearly 80% will be born. Regarding how the two companies merge and exchange shares, how the management will lead, there is no official information to disclose. However, under competitive pressure, the financial data of both parties may affect the right to speak after the merger to a certain extent.

Also backed by the major shareholder Tencent, and also as the leading platform in the domestic live broadcast field, Huya and Douyu have been competing in stalemate in the past few years, and the battle for “one brother” has never stopped. After the two mergers, who can have the dominant power? At multiple levels of company operations, which of these two live broadcast platforms is stronger? We may get a glimpse from the new quarterly earnings report.

Huya MAU is the first to surpass Betta fish,Betta fish’s net profit growth rate is amazing

Shengang Securities report pointed out that Douyu and Huya have their own characteristics due to their different backgrounds and operating strategies. Douyu has invested heavily in game anchors and e-sports, and the content-end dominance brings leading in traffic. Huya was born out of YY’s live broadcast and has a good operating genetics. In contrast, income,Leading in net profit and paid conversion rate.

Huya and Douyu recently released the 2020 Q2 financial report, showing that the overall performance of the two companies is eye-catching, with revenue and net profit reaching new highs, but the revenue growth rate has slowed down significantly. In fact, starting from Q2 of 2019, the year-on-year growth rate of the two companies’ revenue has continued to decline.

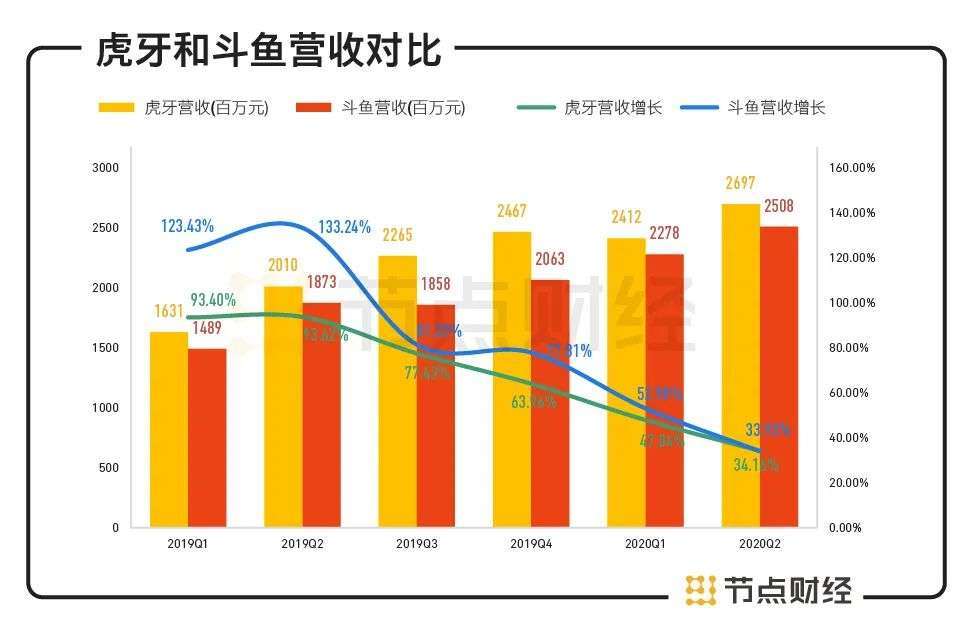

Data source: financial report

Comparing the scale of income horizontally, Huya’s revenue has been higher than that of Douyu in the past six quarters, but Douyu’s revenue has grown faster, and the gap between the two companies is gradually narrowing. By 2020 Q2, Huya’s revenue and revenue growth will be slightly higher than that of Douyu: Huya’s revenue was 2.697 billion yuan, an increase of 34.2% year-on-year; Douyu’s revenue was 2.5 billion yuan, an increase of 33.9%.

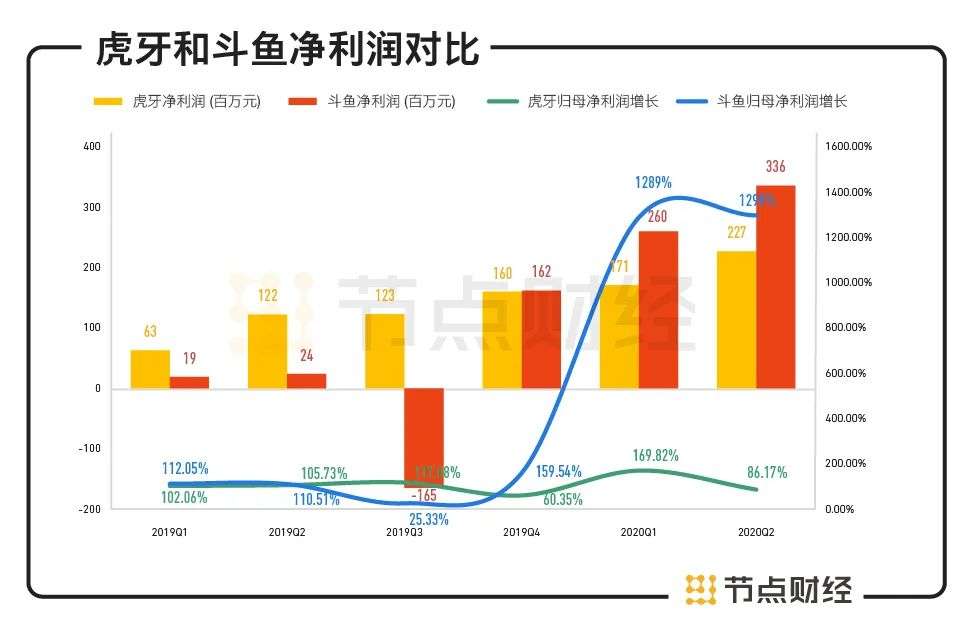

However, Douyu’s net profit growth rate is amazing. In the first and second quarters of 2020, the net profit of Douyu’s parent company maintained a 12-fold increase. Starting in 2019, Douyu and Huya began to make profits. 2020Q1 Douyu returns to its mother net profit to surpass Huya. Data show that Douyu Q2’s net profit attributable to its mother was 336 million yuan, a year-on-year increase of 1298%, achieving a historic breakthrough, while Huya’s net profit reached 227 million yuan, an increase of 86% year-on-year.

Data source: financial report

As the two leading domestic live broadcast platforms, Douyu and Huya have used financial data to prove that game live broadcasts can be profitable. However, the problem lies in the high degree of homogeneity of the development model.

In terms of business structure, the common problems faced by Douyu and Huya are the single monetization model and income structure. From the financial report, it can be found that over 90% of the revenue of the two companies comes from live broadcasting: in Q2 of 2020, Huya’s live rewarding revenue was 2.565 billion yuan, a year-on-year increase of 33.5%, accounting for more than 95% of revenue. During the period, Douyu’s live rewards also accounted for 93% of its revenue, a year-on-year increase.35.8% longer.

At present, both companies are beginning to increase their focus on advertising and other revenue. The financial report shows that Huya’s Q2 advertising and other revenues reached 130 million yuan, a year-on-year increase of 48.6%; Douyu advertising and other revenues increased by 14.5% year-on-year.

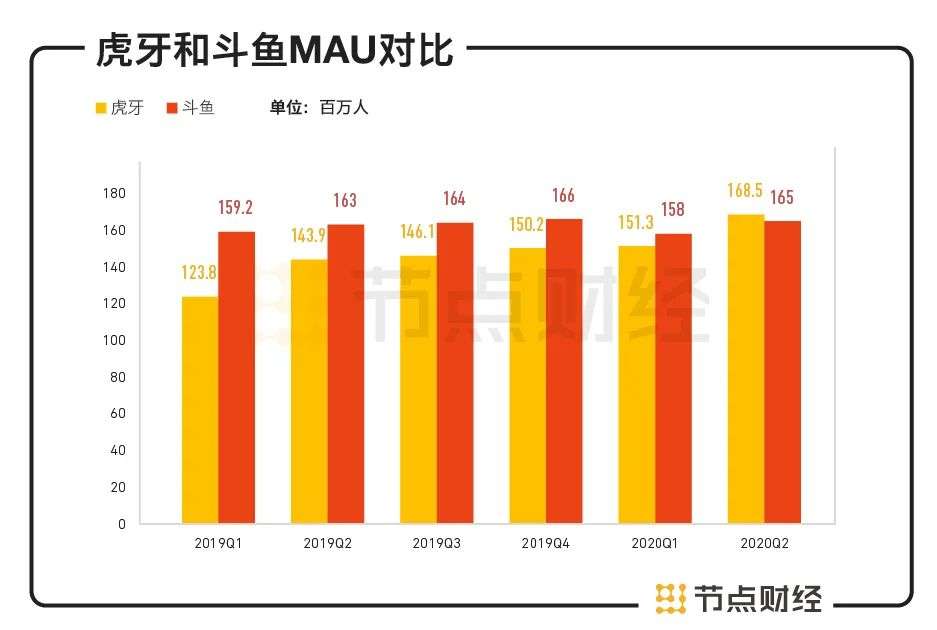

In the post-Internet era, peaking of traffic is a problem for almost all Internet companies. From the perspective of the chain growth rate, the user scale growth of Douyu and Huya has almost stagnated in the past three quarters: Douyu MAU (average monthly active users) basically fluctuates around 160 million; Huya MAU grew rapidly before Q3 2019 , But then basically maintained a slow quarter-on-quarter growth of several million yuan per quarter.

Before, Douyu had an advantage in MAU scale, while Huya was even better in paid conversion. Now the advantages of the two have been reversed: In Q1 of 2020, the average MAU of the two companies is very close. By the second quarter , Huya MAU increased by 11.4% year-on-year to 169 million, surpassing Douyu with a slight advantage of 3.2 million for the first time. Meanwhile, in terms of mobile MAU in Q2, Huya has 75.6 million users, 1.29 times that of Douyu.

Data source: financial report

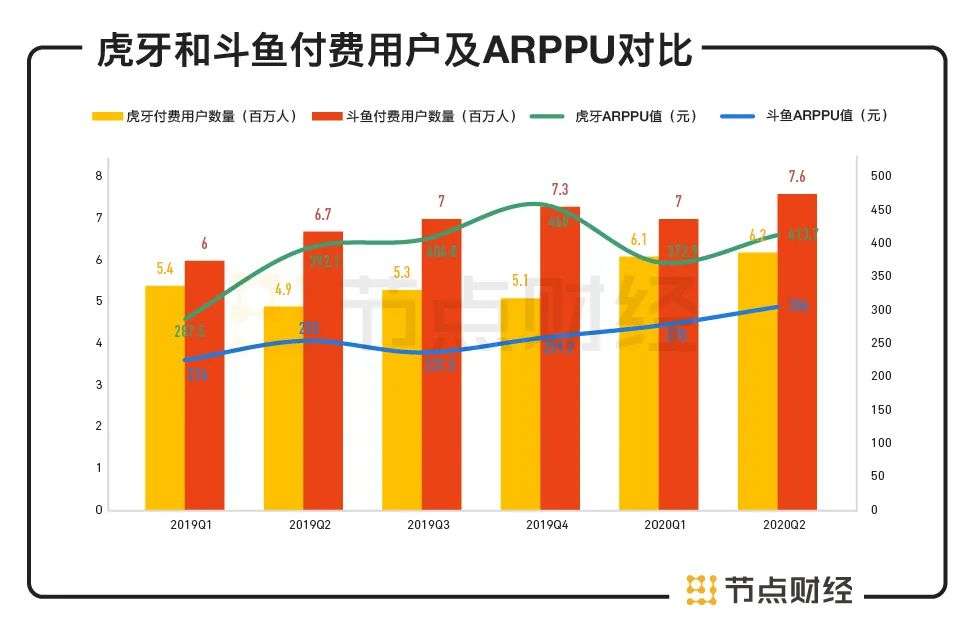

In the case of slow user growth, the current growth in the number of paying users on both sides is somewhat weak. Based on the total MAU, Douyu and Huya will have 4.6% and 3.7% of paying users in Q2 2020. In comparison, the payment capabilities of both parties have their own merits.

Betta fish is even better in terms of paying users. After overtaking Huya in Q1 of 2019, Douyu has been leading the way in the number of paying users. The financial report shows that the number of paying users of Huya in Q2 2020 will be 6.2 million, a year-on-year increase of 26.5%. The number of paying users of Douyu was 7.6 million, which was the same as Q1 and increased by 13.4% year-on-year.

But Huya’s ARPPU (average revenue per paying user) is higher than Douyu. The ARPPU value is an important indicator to measure the monetization ability of the platform and an important criterion for whether the growth of the company’s paying users can be converted into revenue. In Q2 of 2020, Huya’s ARPPU increased by 11% from the previous month to 413.7 yuan, while Douyu’s ARPPU was 306 yuan during the same period.

Data source: financial report

It can be seen that although Huya’s payment conversion is not as good as Douyu, it surpasses Douyu in unit income. Now the gap between the payment rate and unit income of both parties is narrowing, and the two companies are more similar.

In general, Huya and Douyu’s revenue and user growth slowed down because of intensified industry competition and the approaching ceiling of the live broadcast industry. With new competitors such as Station B and Kuaishou aggressively entering the game live broadcast, Huya and Douyu seem to have reached the stage where they have to merge. The financial report shows that in 2020 Q1 value-added service revenue (live broadcast, VIP membership, etc.) of station B will reach 790 million, a year-on-year increase of 172%. According to data from Guosheng Securities, in 2020, the overall MAU of the Kuaishou platform will exceed 300 million, and the live broadcast DAU (daily active users) will exceed 100 million. The live broadcast upstarts are rising at an alarming rate.

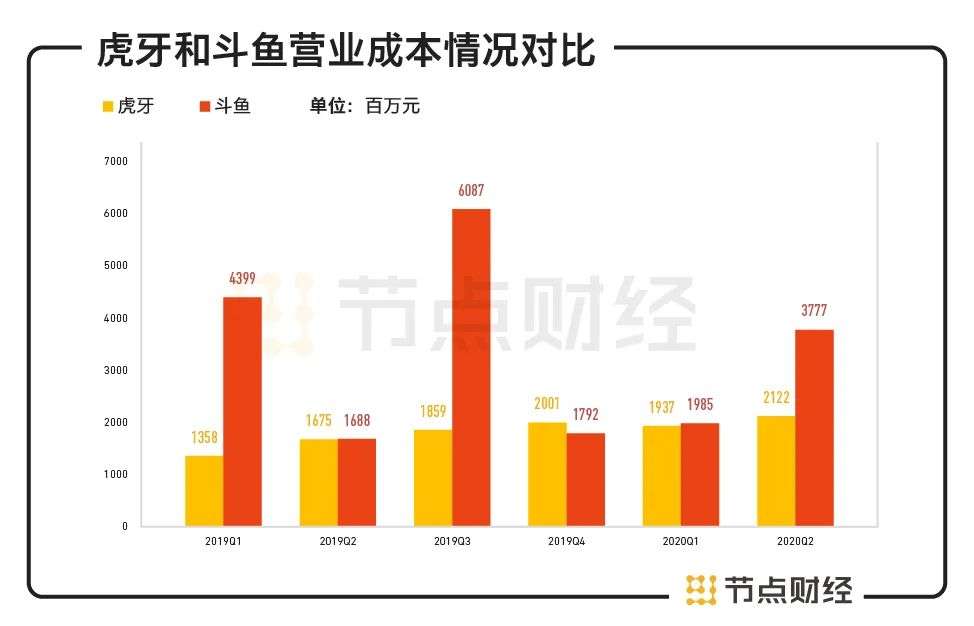

Betta fish’s operating cost is nearly twice that of Huya

In recent years, the domestic live broadcast market has entered a fierce competition for inventory. The consumption problems caused by mutual digging and dismantling platforms among live broadcast platforms have become increasingly prominent, which has led to rising costs for related companies.

Betta fish and Huya were not spared either. Rather than seeking new users and exploring more operating methods, the platform needs to think more about how to dig deeper into live broadcast revenue and increase user payment efficiency based on existing users.

According to the financial report, in the past six quarters, the operating costs of Huya and Douyu have both shown an increasing trend, but the latter has increased more sharply. Especially in Q1 of 2019 and Q3 of 2019, Douyu’s revenue cost has shown explosive growth, reaching 4.4 billion yuan and 6.087 billion yuan respectively.

Data source: financial report

By 2020 Q2, Douyu’s operating costs will still be as high as 3.77 billion yuan, a year-on-year increase of 27%; Huya’s operating costs will be 2.11 billion yuan, a year-on-year increase of 26.7%.