Apple is gradually shifting to a subscription-based business model.

Editor’s note: This article is from the WeChat official account “Beast Finance” (ID: mengshoucaijing ) , author: beast Finance.

Apple’s hardware and services are gradually shifting to a subscription-based business model.

On the one hand, the shift to a subscription-based business model will put pressure on Apple’s operating performance in the short to medium term.

On the other hand, this approach can bring long-term stable and sustainable growth.

In this article, we want to discuss why Apple has become a subscription-based company and what impact this policy change will have on opportunities and risks.

Apple (AAPL) is currently the world’s most valuable company and the most profitable company.

As we mentioned before, Apple announced amazing quarterly results, and each region, product division and financial indicators achieved growth. In the long run, Apple has a very solid foundation and should continue to expand its business.

Nevertheless, Apple’s sales strategy is undergoing a slow but sure change. We are particularly aware of this sales strategy called “subscription software as a service” (saas).

Although most people believe that Apple provides services to increase hardware sales, we believe that the opposite is true. Apple is increasingly providing hardware on a subscription basis. According to reports, Apple plans to launch new product bundles to convey the impression that Apple is becoming a subscription company and therefore deserves a higher valuation.

In this article, we will discuss the implications of the potential opportunities and risks of this strategy.

Apple’s transformation to a subscription company

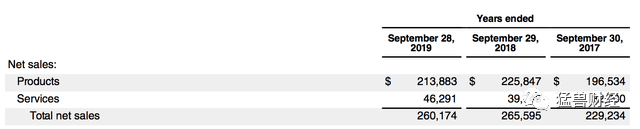

As shown in the figure below, service revenue accounted for 18% of Apple’s total revenue in fiscal 2019, and it is on the rise.

Source: Apple’s fiscal year 2019 financial statements

In addition, iphone, ipaQuarterly records.

Conclusion

As mentioned in this article, Apple is gradually shifting to a subscription-based business model for its hardware and services.

In this case, the subscription model of trade-in and monthly interest-free payment played an important role. This policy change may cause Apple to launch a product portfolio composed of various hardware and service packages in different price ranges.

Apple’s advantage is that the company has the opportunity to keep consumers in its own ecosystem and upsell various products and services.

For consumers, the advantage of this is that the price for users to buy new products will be more affordable, even for users with a very low budget.

Investors should pay more and more attention to this model change when evaluating Apple, instead of simply treating Apple as a traditional hardware company based on past valuation models.

Although the shift to a subscription-based business model will put pressure on the company’s operating performance in the short to medium term, in the long run, this approach can bring stable and sustainable growth.

According to our valuation model, according to different calculation methods, Apple’s current fair value is between 338-366 US dollars, which is equivalent to 27-32% downside potential.

However, based on the current market momentum, we would not be surprised if Apple’s P/E ratio reaches double digits, reaching 16 times, which is the same as most SaaS companies.

Other potential drivers may be the upcoming holiday season, the release of 5g iPhones, the release of AR/VR glasses, and the provision of additional product packages.

Downside risks are particularly present, as more and more companies have joined the criticism of Apple’s App Store practices and 30% revenue cuts. We are worried that the corresponding court order may put tremendous pressure on Apple’s stock price in the short term.

The above is only for investment exchanges and does not represent investment advice.