Under the severe damage, where is Gree Electric’s second growth curve?

Editor’s note: This article from the public micro-channel number ” new entropy “(ID: baoliaohui) , author: Shu FOR THERMAL editor: Hanqing.

The former “Elder Brother Home Appliance” who failed to guard the challengeGree Electric is currently undergoing considerable internal adjustments and business changes. One is Dong Mingzhu’s live broadcast and the other is Gree’s second round of repurchase The plan has thrown a lot of talk to the outside world.

On the evening of October 13, Gree Electric issued an announcement that it intends to use its own funds to repurchase the company’s shares in a centralized bidding transaction. The amount of funds will be between 3-6 billion yuan, and the price of the repurchase will not exceed 70 yuan/ share. It is worth mentioning that this is already the second round of equity repurchase of Gree Electric this year. Based on the maximum repurchase amount, the two rounds of equity repurchase may cost more than 10 billion.

The announcement issued by Gree Electric shows that the second round of repurchase plan is proposed by its largest shareholder “Zhuhai Mingjun”, and the person behind “Zhuhai Mingjun” is Hillhouse Capital. For the capital side behind the enterprise, dividends and repurchases are normalized and maximize shareholders’ interests.

Nevertheless, this move is hard not to remind Gree Electric’s current situation-weak air-conditioning business, plummeting stock prices, and backward channel reforms. The capital market also vaguely transmits signals of damage to shareholders’ interests.

Air-conditioning performance is under pressure, and channel reform is lagging behind

For Gree Electric, 2019 is already very difficult, but 2020 will be even more difficult.

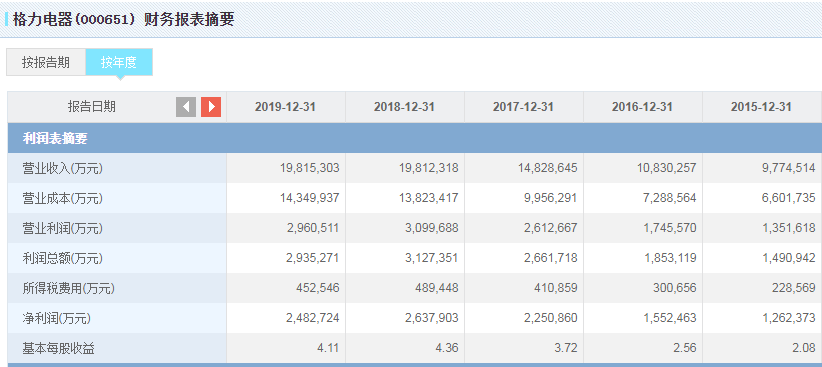

At the end of April this year, Gree Electric released its 2019 and 2020 first quarter performance reports. Last year, Gree Electric achieved operating income of 198.153 billion yuan, a year-on-year increase of 0.02%. This revenue growth rate has shown weakness; the net profit attributable to shareholders of listed companies was 24.697 billion yuan, a year-on-year decline of 5.75%, Gree’s first net profit in five years Decline. However, weaker performance is only the beginning.

Affected by the epidemic, Gree Electric’s 2020 quarterly revenue continued to decline. According to its interim report, revenue for the first half of the year was approximately 69.5 billion yuan.A year-on-year decline of 28.57%; net profit attributable to shareholders of listed companies was approximately 6.362 billion yuan, a year-on-year decline of 53.73%. Compared with last year’s second quarter report, profitability was significantly weakened.

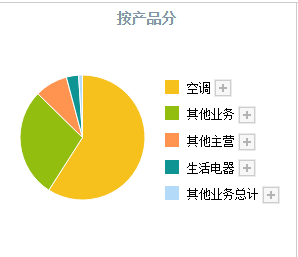

Gree Electric’s revenue has fallen sharply, and its single business model is to blame. Air-conditioning performance is under pressure and other business growth is not obvious.

The “black swan raid” of the epidemic caused the entire air-conditioning industry to enter a downturn. The terminal market sales and installation activities were limited, and terminal consumer demand was weakened. This led to Gree Electric’s air-conditioning business revenue shrinking and retail sales almost half-cut. The “Report on the First Quarter of China’s Home Appliance Industry in 2020” shows that in the first quarter of this year, China’s air-conditioning market dropped by 57.2%, and the price was also at a record low.

Affected by this, in the first half of this year, Gree Electric’s air-conditioning revenue was 41.333 billion yuan, a year-on-year decrease of 47.89%. The decline in air-conditioning revenue and the insignificant growth of other businesses were the main reasons for the significant decline in Gree’s net profit.

Offline channels are blocked, and the shortcomings of online channels have not yet been filled. Gree Electric, whose performance is under pressure, urgently needs reform and innovation.

Compared with the earlier Occitan, Midea and other peers, Gree Electric The channel reform of China has lagged far behind. Perhaps the leader of the industry has been sitting for too long, and Gree Electric’s insight into market changes has been somewhat less sensitive. With the development of e-commerce and logistics, Gree’s competitors are aiming at the online market. Oaks actively embraces e-commerce. Business Mutual< /a>On the Internet, Midea has also carried out a flattening reform of traditional channels, while the relatively conservative Gree Electric is still proud of its advantages in offline channels.

Gree Electric, which focuses on offline store business, has established a complete offline dealer system under Dong Mingzhu’s appointment. A multi-level model from general agent to agents and distributors, and a series of rebate models to achieve deep binding of the interests of distributors and enterprises. This has also become a weapon for Gree to sit firmly as the “boss” of the industry. However, under the epidemic, this weapon has made Gree passive.

Compared with traditional channels, the direct sales model of e-commerce platforms eliminates the profit distribution link of distributors, and consumers can obtain products and services at lower prices. Under the impact of new retail channels, the profit margins of traditional dealers have been repeatedly compressed. To ensure dealers’ profit, the price of terminal products is bound to be higher than that of e-commerce platforms. The failure of channels and prices has caused a big impact on traditional channels. If Gree Electric continues to Stick to multiple levels The distribution model will miss more opportunities.

The offline channel advantages that Gree Electric has accumulated over the years have become a “short board” under the subversion of the general environment of the home appliance industry.

The entire home appliance industry has become more aware of the importance of the online market, and Gree, which has come to realize it, has also begun to make efforts in the online market. This year, the “Gree Dong Mingzhu Store” promoted the new retail model nationwide, and focused on the reform of sales channels and internal management. Following the bigwigs such as Lei Jun and Zhang Chaoyang, Dong Mingzhu also joined the live-streaming and delivery camp, paving the way for the transformation of its new retail business.

According to “China Economic Weekly”, Dong Mingzhu has hosted 10 live broadcasts since April, with a cumulative sales of 41.6 billion yuan. One after another live broadcasts with goods also heralded the urgency of Gree’s business transformation, but “carrying goods” did not fundamentally reverse Gree’s loss.

In addition, Gree Electric’s efforts in new retail will inevitably affect the original dealer system. The increase in online product sales will have an impact on dealers as sales will decrease and profit margins will be compressed again. Although Dong Mingzhu repeatedly denied that the live broadcast was abandoning dealers, the situation of Gree distributors became increasingly difficult, and the contradiction between the two became increasingly acute.

Capital blessing, share repurchase speed up

In addition to the channel changes, Gree Electric’s share repurchase plan is also accelerating.

On April 10, Gree Electric launched its first repurchase plan, intending to repurchase 6 billion yuan. As of September 30, it has spent nearly 5.2 billion yuan to repurchase approximately 1.57% of the company’s shares. Within five days of the launch of the repurchase program, Gree Electric’s share price rose briefly, with the highest quoted price being 56.99 yuan. On April 15, Gree Electric closed down 3.53% to 54.41 yuan, with a total market value of 327.316 billion yuan.

In the short term, share repurchase is a good behavior for Gree Electric. The decrease in the number of individual stocks in circulation will increase the liquidity of the stock. After the share capital is reduced, the single-share income will increase, which will generate a positive market response. Shareholders and investors can also obtain positive excess returns. For shareholders, repurchase is also another form of dividends. Within three days of the announcement of the second repurchase announcement, Gree Electric rose by about 0.59%, with the highest price reported at 58.47. On October 9, Gree’s share price was only 48.16 yuan.

Just in May of this year, Gree Electric and Midea Group also staged the play of chasing you after me, The market value gap is only tens of billions. After 5 months, the relatively balanced competition situation was broken, Gree Electric’s stock price decline became more and more obvious, share repurchase and business transformation were combined, but Midea Group still opened nearly 200 billion market value.

Not to mention Dong Mingzhu, even the capital behind it should be anxious. As a result, Hillhouse Capital, the major shareholder, went overboard and Gree Electric started a second round of repurchase plans. Previously, Gree Electric had invested nearly 5.2 billion to buy back shares, and the repurchase was accelerated again, spending nearly 10 billion in two rounds. What calculations are Gree making?

According to wind data, Gree Electric launched its first repurchase plan this year, while its “old rival” Midea Group launched an equity repurchase plan in 2018. Compared with Midea Group’s many small calculations, this Sub-Gree Electric’s large-scale repurchase seems quite anxious. Regarding the repurchase of shares, Gree Electric stated that it is based on the recognition and expectation of the company’s development prospects, and the repurchased shares are used for employee stock ownership or equity incentives to further enhance the company’s competitiveness.

For Gree chose to launch a large repurchase plan at this time, a third-party research institution lens company research The founder Kuang Yuqing analyzed, “This repurchase will not only increase the long-term return of Gree shareholders, but also help stabilize Gree’s stock price expectations and ensure the financing safety of the mixed reform fund Zhuhai Mingjun.”

As the entire home appliance market fluctuates downward, advancing the share repurchase plan may be a necessary measure for Gree Electric to stabilize its stock price in the short term.

Generally speaking, repurchase programs can boost stocks in the short term. However, in the long run, the share repurchase plan addresses the symptoms but not the root cause. Over 80% of the first round of share repurchase has been completed, but Gree’s stock price is still volatile. The second repurchase invests more funds to push up the stock price instead of focusing on it. For the business transformation layout, this is very detrimental to the long-term development of the enterprise. Gree still needs to find a new way out if it wants to get out of the predicament.

Broken game or “evil cycle”?

The end of capital isIt remains to be seen whether the true repurchase or underweight trap is. In the first half of this year, A shares set off a repurchase trend. Nearly 600 companies released repurchase plans, Ping An of China Harmonicare Group’s repurchase amount is at the forefront. Except for Ping An’s 6 billion yuan repurchase amount, the repurchase amount of Suning Tesco, OCT A and other companies is around 1 billion yuan.

Compared with the repurchase amount of other companies, Gree Electric’s “big deal” is a bit thought-provoking. While repurchase can provide equity incentives, it may also create arbitrage space due to rising stock prices and encourage market bubbles.

During the repurchase period, shareholders of many companies will increase their holdings but also plan to reduce their holdings. Within the period of Gree’s first round of repurchase plans, Gree Electric’s other shareholder, Hebei Beijing Haiguarantee Investment Co., Ltd., announced that it would reduce its shareholding, which is expected to not exceed 4,281,778 shares, and cash out approximately 2.587 billion yuan. Jinghai Guarantee holds 8.91% of Gree Electric Appliances shares, ranking the third largest shareholder. The repurchase with the reduction of shareholders’ holdings has somewhat increased the risk and uncertainty of the enterprise.

It is intriguing that the shareholders of “Jinghai Guarantee” are Gree Electric’s largest regional distributors in the country, and one cannot help but doubt Dong Mingzhu’s high-profile live broadcast Touched the sensitive nerves of the dealer. Channel reform is not a simple online and offline linkage, it also means the redistribution of the benefits of traditional dealers, and the expansion of Gree Electric’s online business will inevitably affect the changes in the pattern of the offline dealer system.

Gree Electric wants to open up online and offline roads, and the transformation pains of dealers are inevitable. How to deal with the balance between online market drainage and offline dealer system will also be a severe test for Gree Electric.

In addition to the channel problem, Gree Electric has always been questioned by the outside world as well as its product structure. The performance of major appliances has declined.Home appliances are not taken seriously, smart devices are still in the money-burning research and development stage, and the arrival of the epidemic has exposed the low risk tolerance of its single product line.

As early as 2016, Dong Mingzhu announced that he would enter “diversification”. However, after the air-conditioning business encountered Waterloo, Gree Electric has not yet found a second growth curve, and diversified development is struggling.

The “old rival” Midea Group is developing horizontally, covering consumer appliances, HVAC, robot automation, smart supply chain and other fields, focusing on diversification. Under the epidemic, Gree’s air-conditioning business has declined by nearly 5 years. However, Midea only fell by more than 10%, and its diversified business model showed greater resistance to risks.

In addition, the low inventory turnover rate is also a “thunder” in the operation of Gree Electric’s business. In 2020H1 Midea’s inventory turnover days were 47.08 days, and Gree’s inventory turnover days rose from 55.31 days last year to 82.07 days, a relatively high inventory. The backlog has brought a lot of pressure on Gree Electric to destock.

In the current market environment, Gree’s share repurchase speeds up again. Although it can temporarily change the state of stock price downturn, it cannot become the driving force for Gree’s business to rise. In particular, after the current air-conditioning market has entered a period of weakness, the industry’s overall room for growth is limited. Gree Electric, whose main business is air-conditioning, urgently needs to find new value-added space. At the same time, Gree Electric still has a long way to go, whether it is channel changes or product iterations.