Impressing Americans is only the first step. The key is to impress high-net-worth individuals.

As a former “P2P brother”, Lufax is in the limelight in 2015 Unexpectedly, I am the slowest and most tortuous road to going public among the mutual gold companies.

From the approaching listing to the transition to the mainland, to the lack of anxious penetration into the capital market, Lufax’s attitude towards listing has changed from clear to ambiguous and then silent over the past five years, under the strong supervision of the industry. Nowadays, Lufax, which has “reconstructed” its small achievements, has formally submitted a prospectus to the US Securities Regulatory Commission and will list on the New York Stock Exchange under the code “LU”.

Walking around, Lufax still has to step on the footsteps of a batch of mutual gold companies to go overseas and embark on the seemingly more “safe” IPO path. For the first time, Lufax’s real business situation was made public.

Clean up your vitality

In the prospectus, Lufax tried to weaken its financial attributes and emphasized its position as a technology platform. To tell this new “science and technology” story well, Lu Jin needs stronger financial support, and financing has become a top priority.

The P2P storm ebbs, and Lufax is no longer flourishing. TodayLufax, although its performance is growing, has left the highway.

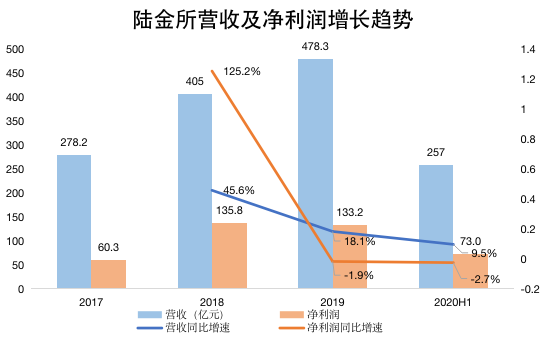

From 2017 to 2019, Lufax’s revenue increased year by year, but the year-on-year growth rate showed a trend of narrowing year by year. In the first half of 2020, Lufax’s revenue was 25.7 billion yuan, the year-on-year growth rate dropped to single digits for the first time, only 9.5%. In 2017, its revenue growth rate reached 125.2%. The net profit situation is also going down in tandem with revenue growth.

In 2019, Lufax’s net profit growth rate was negative. In the first half of this year, its net profit fell 2.7% year-on-year to 7.3 billion yuan.

Drawing; data source: prospectus

From a business perspective, Lufax’s main source of income is revenue based on technology platforms, which is subdivided into retail credit services.and wealth management services. The former relies on “Ping An HP” to provide loans to individuals, small business owners and working-class people, and the latter provides wealth management solutions for the middle class and the affluent. The main body of operation is due to the reputation of P2P business for a while. project-link” data-id=”455186″ data-name=”Lu Jinfu” data-logo=”https://img.36krcdn.com/20200729/v2_f7e37c6151c6425490b3cdc78e382699_img_000″ data-refer-type=”2″ href= “https://36kr.com/projectDetails/455186” target=”_blank”>Lu Financial Services.

Since 2017, Lufax’s retail credit and wealth management business income has both experienced volatility and decline. The growth rate of retail credit business income has dropped from 92.8% in 2018 to 9.1% in the first half of this year. Wealth management services The revenue growth rate turned from positive to negative, with a 53% year-on-year decline in the first half of the year.

Drawing; data source: prospectus

This change of Lufax is mainly attributed to the impact of “de-P2P”. The slowdown in retail credit income growth is due to the continuous decrease in funds from P2P business, and the decline in wealth management service income is directly attributable to the decline in P2P business Stop. In the second half of 2017, Lufax ceased B2C (business-to-personal e-commerce) products, and ceased P2P business in August 2019. Since the regulation of the mutual gold industry has become stricter, Lufax has gradually removed the “P2P brother” label that allowed it to reach the peak of its business.

In 2011, as Ping An of China will promote Integrated Finance part of the development model, Lufax was formally established, and its core business is P2P, which will be hot for the next few years. Four years after its establishment, Lufax has become the highest flying company in the P2P industry, and it has also taken the top spot in the global P2P business. In the third quarter of 2015, Lufax’s P2P business scale surpassed Lending Club, the originator of online lending in the United States.

The reason is that P2P has the advantage of light assets. The platform only serves as an information intermediary and does not bear credit risk. The scale of assets can expand rapidly. Backed by Ping An Group’s Lujin, it has better credit backing than its peers.Book, at the same time the early P2P industry developed too quickly. It almost grew wildly in a “regulatory vacuum” environment. Where there are loopholes, there are business opportunities. Of course, this is also < /span>A huge risk is brewing.

After the peak is the trough, P2P business has become a product that takes off quickly and falls heavily in the mutual gold field. In the domestic market, the P2P interest rate outside of the securities and financing business exceeds the bank’s savings and wealth management products, which has a strong impact on the traditional financial model. At the same time, the risk control and credit abuses of this private equity product are slowly exposed and wandering. On the verge of illegal fundraising and Ponzi schemes.

In 2016, the trend of the industry changed, and strong supervision came in. The special rectification of Internet financial risks was launched in April, and Lufax’s listing plan was also on the verge of shedding. Just in 2017 when Lufax stopped B2C products, the “double drop” (the number of business institutions and business scale) was first written to the official The document, followed by Circular 141, was issued to rectify the “cash loan” business. Since then, the stock prices and market value of a batch of mutual gold stocks have been cut several times, and domestic P2P companies have suffered a more tragic reshuffle of the storm.

In 2018, the P2P industry was even more sad. The “double down” was upgraded to the “three down” (reduction of stock size, loan balance, number of investors). Under high pressure, mutual gold companies embraced compliance while seeking transformation. “Financialization” and moving closer to technology are the key points.

This is also the path of transformation that Lufax has chosen. In the prospectus, Lufax has tried to weaken its financial attributes, only calling itself a “technology-driven personal financial service platform.” After 14 months of suspending the P2P business, Lufax gradually came out of the painful period of transformation and relaunched its listing plan in the name of “technology”. This is a dream come true, and it is also a capital pool.

However, the time slot when the enthusiasm for listing in Hong Kong A has been repeated and the Chinese concept stocks have returned one after another may be the loose conditions of the overseas capital market. Lufax is no longer obsessed with The Hong Kong stock market chose to go overseas.

With the core of lending money

Currently, Lufax is already full of urgency to go public.

From the perspective of the market competition environment, the ants that are in the same ranks as the financial technology giants of LufaxThe group announced the simultaneous listing of A+H, and Jingdong Digital Technology has also determined to settle on the Science and Technology Innovation Board. As the former leader in the mutual gold field, when Lujin’s competitors launch listings, they must respond to maintain their position in the industry.

From the perspective of its own business, going overseas is the most “safe” choice for the successful listing of Qi.

The prospectus for the U.S. disclosed the transcript of Lufax’s clearing and withdrawal of P2P business. As of June 30, 2020, its online loan asset balance was 47.8 billion yuan, a decrease of 85.8 compared to 336.4 billion yuan at the end of 2017. %, but it will take two years to “clear”. This means that if Lufax chooses to list in the country, it will still face strict regulatory review.

Drawing; data source: prospectus

For Lufax, P2P business can be said to be a “sweet burden”, and it cannot be completely cut off because of the listing.

In the two main businesses of Lufax, from the perspective of revenue scale, retail credit has completely dominated Lufax’s revenue trend. In the first half of 2020, the revenue accounted for 80.7%, which was highlighted. And’s wealth management business only contributed 2.7% of revenue.

In order to be able to walk on two legs, Lufax’s wealth management business also needs to extend its non-online loan business. From 2017 to 2019, the revenue of non-online loan business under the wealth management sector was 280 million yuan, 410 million yuan, and 460 million yuan, respectively. The revenue in the first half of this year was 420 million yuan.Carry the banner.

The development of non-online loan business cannot bypass the acquisition of new customers. Lufax’s early P2P business has accumulated a large number of users. It is the most convenient way to convert these online loan users into non-online loan business customers. Look, after the business switch, user retention has been achieved, but the conversion has not yet been completed. According to the prospectus, as of June 30, 2020, its “old product” user retention rate is 95%.

Apart from its “difficult to give up” stock P2P business, Lufax’s retail credit business may also trigger sensitive regulatory nerves. Retail credit is provided by Ping An Hewlett-Packard, which is still doing “lending” business, but the service target has been upgraded from individual users to small and micro enterprises with relatively more secure risk control. The essence of Lufax as a matching platform No changes have occurred.

While going overseas to go public and bypassing the supervision, it also has the experience of successful listing in the same industry. For Lufax, which is eager to go public, it is a low-risk option for stability.

But by knocking on the door of foreign markets, Lufax also missed the opportunity of the domestic capital market.

Since this year, the domestic capital market reform has been gradually implemented. The Sci-tech Innovation Board and the ChiNext registration system have created a more relaxed listing environment for new economy industry companies. In addition, in the domestic capital market, institutions have fully grasped the pricing power to give new The higher valuation of listed companies is something that Lufax will miss.

In the face of the U.S. stock market’s more open attitude towards financial technology, Lufax, which is under high regulatory pressure, how to tell about the decline in performance from 2018 to 2019, and how to convince investors that history will not repeat itself , Is a key step for it to gain market recognition in the United States. This step is not easy because the changes in the domestic regulatory environment are largely unpredictable in advance.

Do high-net-worth individuals still buy it?

At present, the scale of Lufax’s listing in the United States has not been disclosed. If according to the market’s reported financing scale of US$2 to 3 billion, Lufax will become the largest financial technology IPO in US stocks, and this fundraising financial The new story told by Lu Jin is also crucial.

Before that, the C round of valuation was completed in 2018 with a valuation of 39.4 billion U.S. dollars. Lufax, which has not received financing for nearly two years, is not only for participating in its various rounds of financing. The shareholder’s late explanation is also saving “grain and grass” for his unfinished transformation.

The road from the financial capital to financial technology is not easy to follow. Lufax is in a state of “high failure, low failure”.

Lufax initially focused on Hewlett-Packard Finance, and now it’s wealth management businessServing the middle-class and affluent people, Lu Jinn’s high platform user base also determines that it cannot achieve a substantial increase in user scale. This is not good news for platform companies. Focusing on the level of high-net-worth users, wealthy people with more freedom to control their own assets can take higher risks to obtain higher return on investment However, the financial products provided by Lufax’s platform are limited by policy constraints on interest rates, which can hardly be said to fully meet the needs of target users.

If it is to extend the target users downwards, Lufax must be completely exposed to the giant players.

In the prospectus, Lujin said that it is based on the financial technology platform supported by traditional financial institutions and Internet companies (such as Ant Group, WeBank, Tencent Wealth Management, etc.) cannot serve markets. Specially mentioned Ant Group, etc., and pointed out the differences in business models and their own advantages, and emphasized the significance of differentiated competition, but in essence, both have overlapping services to provide individuals with credit.

In contrast, Lufax and Ant Group have a large gap in user and credit scale.

As of June 30, 2020, the “micro-credit technology platform” under the Ant Group responsible for personal credit business has facilitated a total credit of 21,500 yuan and has 1.07 billion registered users; during the same period, the total retail credit balance of Lufax was 5350 It has 44.7 million registered users and 12.8 million active investors.

Chacha’s retail credit business is Lufax’s current revenue pillar, with revenue of 39.3 billion in 2019, accounting for 93.8% of financial technology platform revenue, and revenue of 20.75 billion in the first half of this year, increasing its proportion to 96.7%. While the wealth management business has shrunk year after year and retail credit has thrived, Lufax’s leading business has been restrained by competition.

Ant Group is backed by the Ali department, is a natural traffic player, and is supported by many consumption scenarios, so the leading business scale is inevitable. This also reflects LuThe transformation dilemma after the “de-P2P” of the gold exchange is that in the broader mass market, the Ant Group has obvious advantages, and Lufax has nowhere to go.

Lufax’s ability to settle in US stocks is fulfilling its long-cherished wish to go public, but the uneven development of its main business, the core of the P2P business, and the contradiction in the direction of transformation are all difficult to erase within a short time after its listing. Flaws, facing American investors, Lufax’s transformation story needs to be perfected.

Scan the QR code to enter the group