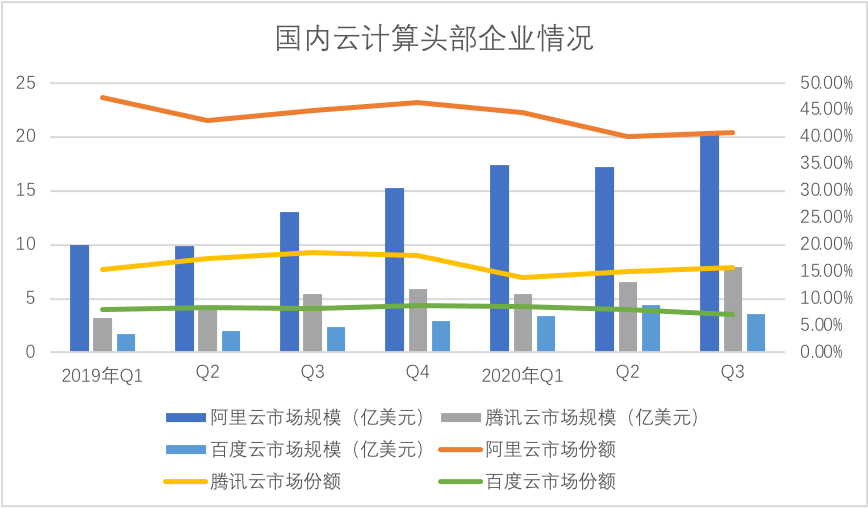

The market share changes of cloud computing vendors are shown in the figure below

BAT is a leading domestic Internet company. Although different companies have different attitudes in the early stage of cloud computing (typically Tencent and Baidu, the launch of cloud computing is later than Ali), before 2020, these three companies are in cloud computing The total share is constantly increasing, and the industry concentration is more obvious, but after that, the total market share of the BAT camp began to decline, and the shares of the three companies are falling.

Although the cloud computing revenues of these three companies are all hitting their respective historical highs, the cake of this cloud computing is getting bigger and bigger, but there are obviously more people who share the cake, that is Huawei Cloud, Huawei Cloud in 2020 The domestic cloud computing market share rose from 14.1% in Q1 to 16.2% in Q3, and officially surpassed Tencent Cloud in Q2, officially ranking second in cloud computing.

Why is this?

After the cloud computing industry has entered a new round of high growth due to “new infrastructure”, how has the original industry structure changed? In our previous analysis of the government cloud, we thought that under the administrative reform goal of “one network, one door, one time”, to realize the data flow between different government departments and the SaaS service on the user terminal as the entry point, Ali and Tencent also has two phenomenal products, Alipay and WeChat, which has created a confluence of SaaS and IaaS. Its investment and advantages in terminals and underlying technologies have also established Internet companies’ sense of leadership in cloud computing.

Alibaba Cloud has incorporated DingTalk into its business subset and promoted the “cloud and nail integration” strategy. We also believe that this is a signal that the cloud computing industry is accelerating from IaaS to SaaS, highlighting the development of both the underlying technology and the application side.

But in 2020, we believe that the industry has not fully followed this forecast.

We tried to find relevant clues through the fixed asset investment catalog published by the National Bureau of Statistics. The total fixed asset investment of the computer, communications and other electronic equipment manufacturing industry in 2020 increased by 12.5% from the previous year. “Inspired, digitization began to permeate various industrial subsets, such as automobile manufacturing, smart factories, etc., and the electronic equipment manufacturing industry is undergoing significant capacity expansion. We believe that the speed of cloud computing in key industrial areas in 2020 may exceed expected.

Although in Q1 of 2020, due to the epidemic, the continuation of normal production and investment behavior was restricted, but afterwards, we observed in the data of the National Bureau of Statistics that fixed asset investment in some areas has an accelerated trend in the second half of the year, such as chemical Industrial product manufacturing, special equipmentThe investment in fixed assets in the manufacturing, electrical machinery and other fields is not much different from the previous year, which shows the intensity of investment in the second half of the year.

On the one hand, the country advocates “new infrastructure”, hoping to achieve a qualitative leap in China’s manufacturing, and hopes to use the new infrastructure that is different from the previous reinforced concrete to reshape the image of China’s manufacturing industry through digitalization. On the other hand, The production capacity of electronic equipment will be significantly expanded in 2020, coupled with the acceleration of fixed asset investment in key areas, we have reason to believe that industrial cloud will accelerate in 2020.

In 2019, we judged that industrial cloud investment would be difficult to boost in the short-term due to excessive pressure on profit margins. However, despite the outbreak of the black swan incident in 2020, due to the early control of the epidemic in China, production resumed in time. On the contrary, industrial exports took this opportunity to enlarge, the trade surplus expanded, and, with the support of loose monetary policy, enterprises achieved a hot start (there are also factors such as rising capital market and the increase in direct financing capabilities of enterprises). By November 2020, they will be above scale. The operating conditions of the company have been fundamentally improved. Not only has the capacity utilization rate returned to a normal level, but the operating efficiency has also been fully demonstrated.

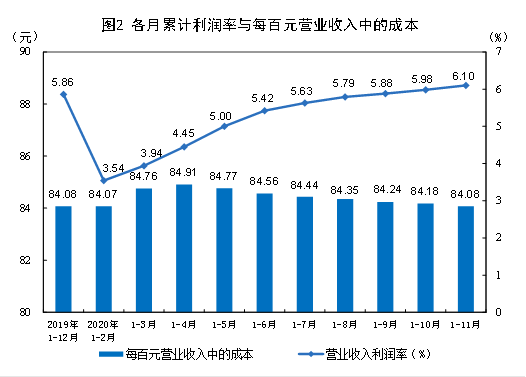

We have extracted the cumulative profit rate of each month and the cost per hundred yuan of operating income of enterprises above designated size from the National Bureau of Statistics, see the figure below

In November 2020, the cost of operating income per hundred yuan of industries above designated size in my country has been optimized to the level of the end of the previous year, and the cumulative profit rate of each month is also higher than that of the end of the previous year. These have created conditions for the continued expansion of the industrial cloud.

It is worth noting that due to the impact of the epidemic, the consumption scene of ordinary people is restricted, and the increase in savings rate is used to hedge against uncertain risks, which makes the annual PPI in a low range. If the epidemic is achieved after the popularization of the vaccine in 2021 Fundamental control, domestic demand has been fully released, and the oversupply situation has been completely reversed. Combined with the fact that the above-mentioned operating efficiency is improving the channel, industrial enterprises may have greater fixed investment in 2021, especially cloud computing investment willingness.

Back to 2020, we believe that the acceleration of cloud migration in the industrial sector may be an important reason for the adjustment of the cloud computing situation.

According to data from the Ministry of Industry and Information Technology, my country’s industrial Internet network system has accelerated construction. As of October 2020, it has covered 300 cities and connected 180,000 industrial enterprises.

The number of industrial equipment connected to the platform reached 40 million sets, the number of industrial apps exceeded 250,000, and more than 350,000 industrial enterprises went to the cloud.

This set of data can also support our above analysis.

If the new infrastructure provides the prerequisites for the development of the above smart factories, then the next national policy support here, as well as the cloud enterprises’ control over product quality and pricing power after efficiency enhancement, will also accelerate We don’t think that the cloud computing landscape has stabilized as the industry changes. On the contrary, the prologue has just begun.