Replay Steam growth history

Editor’s note: This article is from the micro-channel public number “table appearance in” (ID: excel-ers), Author: Insight Data Institute.

Taptap, known as the “Steam for mobile games,” recently suffered a cut in its stock price.

I still remember that in the same period last year, TapTap’s share price also experienced a similar downward trend. Non-short-term “share price.”

The so-called long-term “value” refers to the improvement of research and development capabilities rather than the increase of company revenue, and the increase of user scale rather than the increase of company profits.

The vision was outlined and market sentiment was stirred up. The stock price continued to rise for nearly a year, from less than 20 to the highest point of 114.5, which was more than five times higher.

Now in less than a month, the stock price has been cut in half. Can’t help but make people wonder, is the long-term “value” untenable?

However, when we reviewed TapTap against the target Steam, we found that the problem may not lie here.

Data shows that in 2020, Steam’s MAU will reach 120.4 million and DAU will be 62.6 million, making it the world’s largest PC gaming platform.

To build such an industry position, the core driver lies in the bilateral network effect brought about by the supply of games and user growth. (The “long-term value” emphasized by Taptap)

As for why this is said, this article will answer by disassembling the life cycle of Steam user growth, specifically:

1. Concept period: After catching the express train of change, renew your life with self-study

2. Introductory period: user growth realizes “bilateral network effect”

3. Growth period: How to break through the boundaries of core competence?

4. Maturity: Under the threat of competition, can you adapt to new changes?

Concept phase: After catching the express train of change, continue your life with self-study

When the Steam platform was launched, PC gaming was a business model that had not yet been fully verified, but Steam’s early testsSuo laid the two foundations of the main business: “Start early” to catch the express train of industry change; and gain the first wave of key users with self-developed games.

In 2000, Valve (hereinafter referred to as “V Society”) launched the shooting game “Counter Strike”, setting off the “Golden Age” of FPS (First Person Shooting) games worldwide.

But when the V agency is going to make a big splash next, the problem comes.

The development team found that when updating games such as “Half-Life” and “Counter-Strike”, every patch released may cause most console game players to disconnect for several days.

Of course, this is not a technical problem of V, but a common problem that is increasingly acute for console games. Specific and related performances include:

·Product: The host game cannot automatically update the game, only the game card can be replaced to update the game.

·Price: The console game requires hardware and equipment, so it is expensive.

·Promotion: The distribution of console games is directly controlled by console vendors such as Nintendo and Sony, and the release price is relatively fixed.

·Channel (place): The game card of the host game must be selected and purchased at the physical store. Not only the sales efficiency is low, but the supporting services in the later period cannot keep up.

For the experience-focused entertainment and creative industry, when the pain points of the industry accumulate to irreconcilable, it means the arrival of change-the transformation of console games to PC games.

In this context, V agency decided to create a game distribution platform that can automatically update the game, and integrate a stricter anti-piracy and anti-cheating system. This platform is Steam.

Although the SteamPC platform has the advantages of cheaper game prices, unlimited updates, and freedom of purchase compared to console games, the initial generation of Steam does not give players the impressionGreat.

The ugly interface, many bugs, frequent updates, and too long networking time make players complain about Steam.

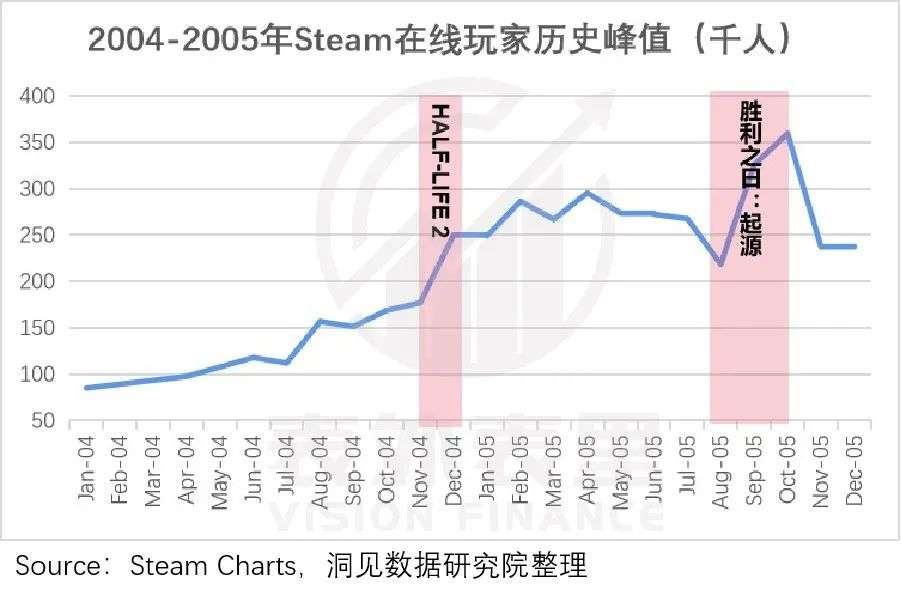

At the time of Steam’s critical survival, the V agency shooting game “Half-Life 2” was officially released and released exclusively on Steam. This turn-around operation attracted and retained the first batch of users on the platform. Become a turning point in Steam’s career.

In 2005, V Agency took advantage of the victory and released another self-developed game “Victory Day: Origin” ( Day of Defeat: Source), once again creating the peak of online players.

The success of self-developed games may have made the platform realize that high-quality game supply is the key to attracting users. Then began to break through the limitation of self-developed supply, introduce non-self-developed games, and create an open platform ecology.

In the same year (2005), Steam released the first non-V club games “Ragdoll Kung Fu” (Ragdoll Kung Fu) and “Digital Warfare” (Darwinia).

Since then, Steam has become a real online game store from a download platform of V agency’s own games.

Introduction period: User growth achieves “bilateral network effect”

The opening of the supply side allows Steam to obtain a steady supply of games. While expanding the platform’s game resources, it also provides a basis for Steam to explore the bilateral effects of user growth in the next traffic era.

After 2006, “Orange Box”, “Resident Evil 5” (Resident Evil 5), Medal Of Honor (Medal Of Honor), “Bastion” and other seriesn style=”letter-spacing: 0px;”>Exploring the reasons behind it, we found that “CS:GO” is still in the category of shooting games, and “DOTA2” is a competitive game that has never appeared on the Steam platform before.

Therefore, the completely different market response during the initial release period may reveal a signal: As the scale of users expands, players’ demand and taste for game categories has become diversified. Compared to shooting games with similar routines, players will first try competitive games that they haven’t played.

In other words, the attractiveness of the platform to players depends on the number of game types provided. The more types of games, the greater the value of the platform to users, and the more people will be attracted to play.

More users will promote the launch of more self-developed and non-self-developed games. This cycle continues and strengthens each other, making the Steam platform have a “bilateral network effect”, and the user growth ability will naturally be solved.

Growth period: How to break through the boundaries of core competence?

The bilateral effect of supply and demand makes the core contradiction of Steam development no longer the ability to grow users. At this time, Steam’s challenge comes from itself-how to grow to the next magnitude on the basis of the largest platform in the game distribution field.

This requires the platform to find a new starting point to break through the boundaries of existing core capabilities.

For Steam, the new growth mainly comes from three aspects:

①Recruiting developers, expanding SKUs and new ones

Based on the above analysis, it is self-evident that games are important to the platform. In order to compete for good game resources, in addition to self-research, Steam has carried out a series of solicitations around game developers.

For small and medium-sized game developers, in order to lower their release threshold, Steam officially launched the Favored Light system in 2012, allowing players to vote to determine whether their games can be released on Steam.

In 2017, Steam upgraded the system to a “Direct Distribution” system (Steam Direct), fully releasing the functions of small and medium-sized developers.

Similar to this, there are also: Holding Steam Dev Days (summits) to expand the scope of contact with game developers through experience sharing and collision; setting up Steam Game Festival to provide game developers with opportunities to promote their works, etc.

Although the method is old-fashioned, the effect is still good.

Currently, there are 6208

The content ecological growth rate is weak, and the game platform wants to retain and capture more users, inevitably breaking the circle.

②Break the circle in e-sports and wake up old users

Steam’s breaking circle activities outside of content mainly focus on game events and live broadcasts. The purpose is to awaken the enthusiasm of old users for the game through continuous exposure and pull new ones, and activate them to return to Steam.

In recent years, the number of spectators watching e-sports events has continued to rise, and holding relevant competitive events has become a common means of breaking circles by major game parties.

So, what is the specific effect?

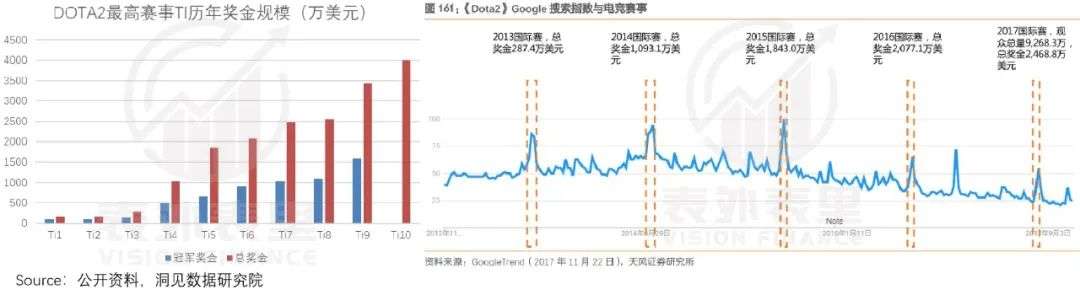

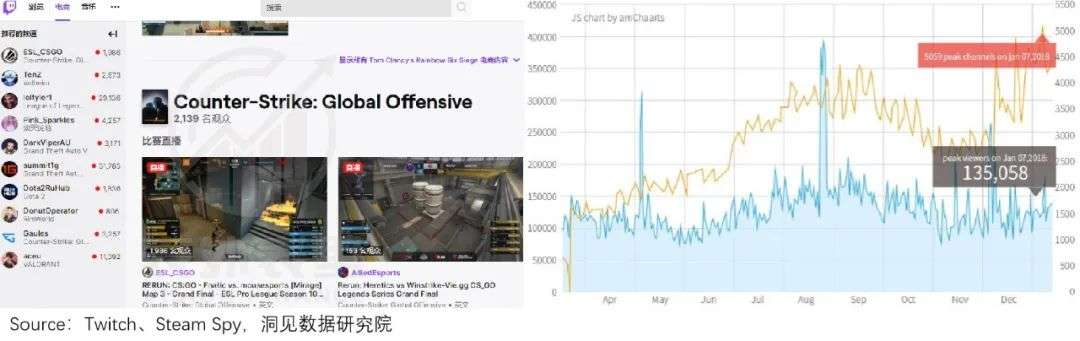

Take Steam’s largest prize money “DATA2” International Invitational (Ti) as an example. The competition has been held for 10 times since 2011. As the prize pool increases year by year, it has repeatedly attracted attention.

As shown in the figure below (right), during the previous Ti competitions, the Google search index of “DATA2” will have a significant peak.

Note: Ti10 does not hold a competition

For users, watching competitive events is not about technology, but about exciting battles. Both offensive and defensive on the public screen, in the confrontation and lore you come and go, what is projected is the passionate youth of the players.

“LordIn the atmosphere of “green back”, it is a great opportunity for the gaming platform to recall old players.

However, it is not an easy task to hold a huge event. Buying feelings in this way is too expensive. And another more “money saving” way-game live broadcast, has become a new carrier for game awakening.

It can be seen that the increase in users of live broadcast platforms such as Huya and Douyu is positively related to the live broadcast of popular games such as “Honor of Kings” and “Jedi Survival” (Eating Chicken) on the platform.

Nowadays, the live game track has been ignited. As a PC gaming giant, Steam naturally joins this strategic blue ocean. For example, “CS:GO” and “PUGB” on Steam have corresponding live channels on the live platform Twitch.

The peak number of live channels of “PUBG” on Twitch is as high as 5,000, and the peak number of viewers reaches 130,000.

Note: The yellow line on the right is the number of live broadcast channels on the day (right axis); the blue bar graph is the number of live broadcast viewers that day (left axis)

However, due to the frequency of events and the short time for Steam to introduce live broadcasts, the specific awakening effect of the platform on the breaking circle needs to be observed later.

Whether it is to pull in new ones or wake up old users, the purpose is to allow players to stay on the platform. To achieve this, the gaming experience of the platform is particularly important.

③The “plug-in” is dead, how to retain users?

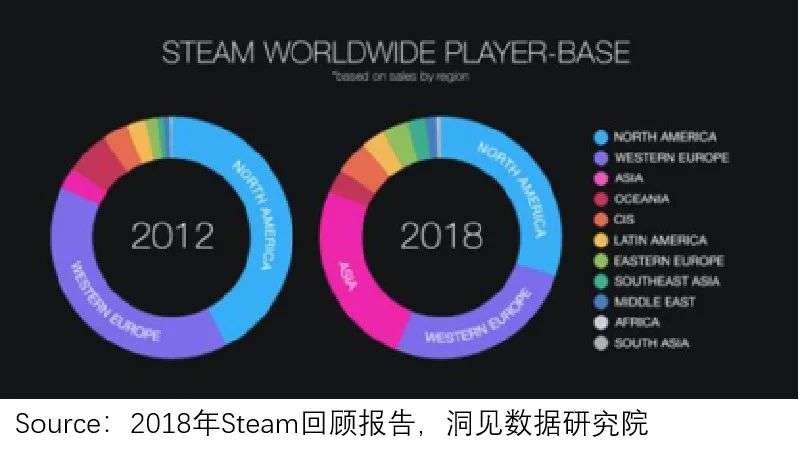

Based on Steam’s global platform attributes, language and currency have become the first level that affects the player’s gaming experience.

But this problem is not difficult to solve. Steam has supported 26 languages, 39 currencies and 80 payment methods (Alipay and WeChat entered Steam in 2016), Achieve a certain degree of resolution.

Compared with the language barrier, “plug-in” is the key slot for the player’s poor experience during the game.

How bad is the impact of plugins?

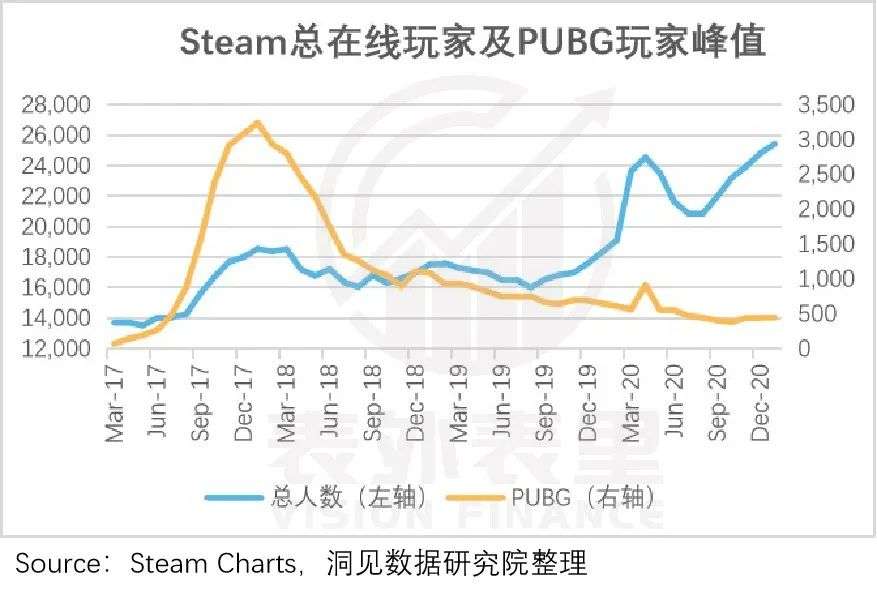

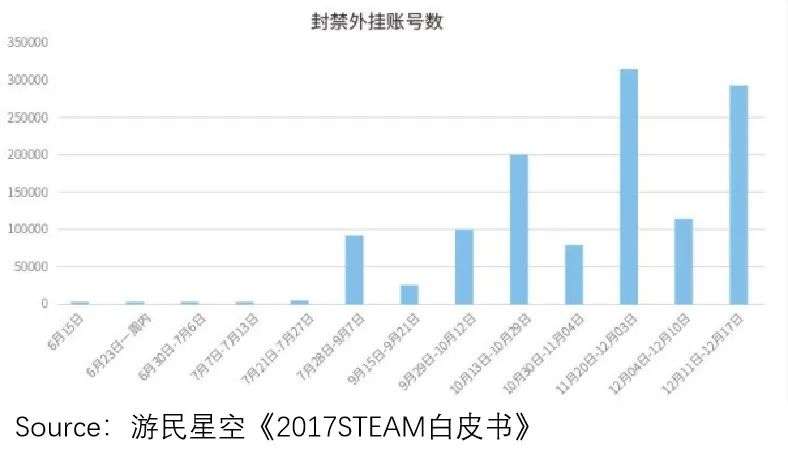

Take the phenomenon-level popular “PUBG” as an example. Due to the endless emergence of various plug-ins, the player experience is seriously affected. The number of players of “PUBG” on the Steam platform reached its peak in January 2018 and has been showing a downward trend.

In this case, not only does Steam have a headache, but also the Blue Hole that produces “PUBG”.

Since 2017, Blue Hole has been cooperating with Battleye to detect plug-in accounts and ban them, with a ban rate of over 5%.

On the Steam platform, there are dual protections to prevent “plug-in” phenomena, namely the account protection system (Steam Guard) and the Villefort anti-cheat system (VAC). Although this move cannot eliminate “plug-in”, it purifies the gaming experience to a certain extent.

The ever-expanding rich SKUs, the circle-breaking effect on the awakening of old users, and the optimization of the game experience have brought Steam’s volume to a node of over 100 million: In 2018, Steam’s monthly active users reached 90 million, which is higher than that in Germany. The population is still large.

But also this year, a game mall called Epic jumped out. Under competitive pressure, the core contradiction of the Steam platform is once againchange.

Maturity: Under the threat of competition, can you adapt to new changes?

Although a group of new players such as Humble, UPlay, and Origin have emerged in the PC game field immediately after Steam, these game platforms have not challenged Steam. As mentioned above, Steam is always the main platform for developers to sell games.

The emergence of the Epic platform has allowed Steam to face threats directly.

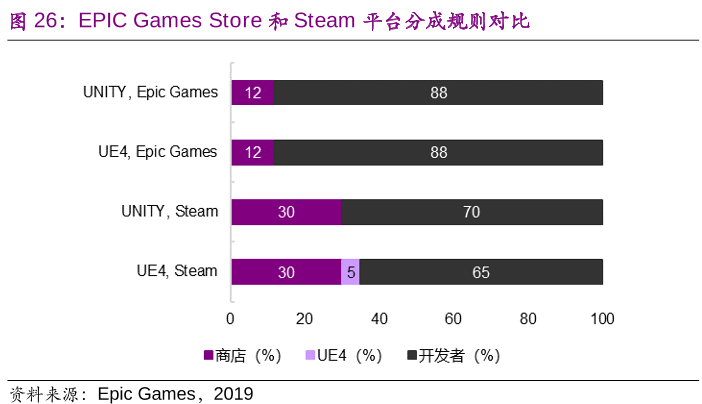

In recent years, game manufacturers have been dissatisfied with Steam’s 30% rake, believing that Steam will charge 30% of the game platform’s rake like traditional console makers without having to bear the obligations of physical stores, logistics, and game promotion. The ratio is too high.

In 2018, in response to the conflict of interest between Steam and CP, Epic took a trick to draw salaries.

With a lower 12% rake, and the use of Unreal Engine to develop and provide an additional 5% rake reduction and other low-sharing strategies, and Steam grab game developer resources.

This move forced Steam to introduce a new sharing rule: For games with sales of $10-50 million, the split ratio will be adjusted to 25%; sales For games with a value of more than US$50 million, the platform only pays 20%.

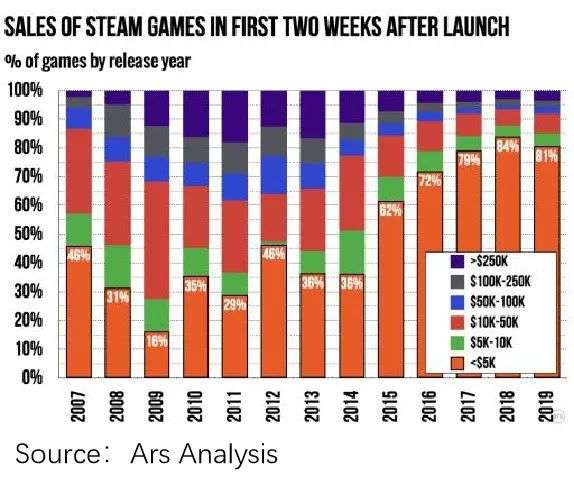

But in fact, more than 80% of the games on Steam in 2019 earned less than $5,000 in revenue two weeks after the release, and most of them were independent games.

This means that Steam’s compromise on sharing can only benefit some major manufacturers. As a result, it is difficult for Steam to block Epic’s “new addition” process by virtue of the new sharing agreement.

According to Epic founder Tim Sweeney: The platform currently (2020) has a 15% market share, and this number is still growing.

However, in the short term, several exclusive games from Epic Games are unlikely to subvert Steam’s market position. But I am afraid that there is often more than one variable.

Now, the game industry has once again come to a moment of change.

The rise of “click and play” cloud games has had a certain impact on PC games, just like PC games challenged console games.

However, in the new situation, Steam does not have the first-mover advantage as in the PC era. In fact, together with the concept of cloud gaming, the cloud gaming platform has “a hundred flowers blooming”, and no one wants to miss the opportunity.

Under such a background, if Steam cannot adapt to changes and make timely adjustments, the next story may not be so easy to tell.

Summary

From the very poor user experience at the beginning, to becoming the world’s largest PC gaming platform. In the course of nearly 20 years of development, Steam started by grasping the transformation from console games to PC games, and has mastered the first-mover advantage.

Then relying on self-developed games to harvest key users, explode strategies, and find new hands (expanding CP, breaking circles to optimize game experience) and other core contradictions, the platform has smoothly passed the stages of germination, introduction, and growth. So far, the development logic of Steam R&D and user growth has been verified.

Just after entering the mature development period, the game industry will usher in a new change in the transformation of the game industry to cloud games. As for Steam, where the first-mover advantage no longer exists, how to deal with new challenges is currently full of unknowns.