New house transactions increased by 40% year-on-year

Editor’s note: This article comes from the Daily Economic News, and every time the reporter perceives Jingjing.

In the first quarter of this year, how did the real estate market perform?

On March 31, data released by the Zhongzhi Research Institute, Crane, Yihan Think Tank, Shell Research Institute and other institutions showed that in the first quarter, the property market and the prefecture market continued to maintain the transaction enthusiasm at the end of last year, and the sales of real estate companies To record a new high, the transaction volume of new housing markets in all tiers of cities surged, and the transaction volume of second-hand housing surpassed the level of the same period in the previous four years.

However, with the tightening of regulatory policies in various regions since the beginning of the year, will the real estate market usher in a “small sunshine” or an inflection point in the second quarter?

New house transactions increased by 40% year-on-year

Due to the low base and concentrated launches in various regions, the transaction volume of the new housing market surged in the first quarter.

According to data from the Shell Research Institute, in the first quarter of this year, the transaction volume of new houses in 66 cities nearly doubled year-on-year. Compared with the same period in 2019, the increase rate reached 40%. The first-tier cities are particularly active in the start-up market, continuing the momentum of concentration and heavy volume at the end of 2020. Compared with the same period in 2019, in the first quarter of 2021, the number of new home transactions in first-tier cities increased by 58.5%, second-tier cities increased by 32.6%, and third- and fourth-tier cities increased by 43.8%.

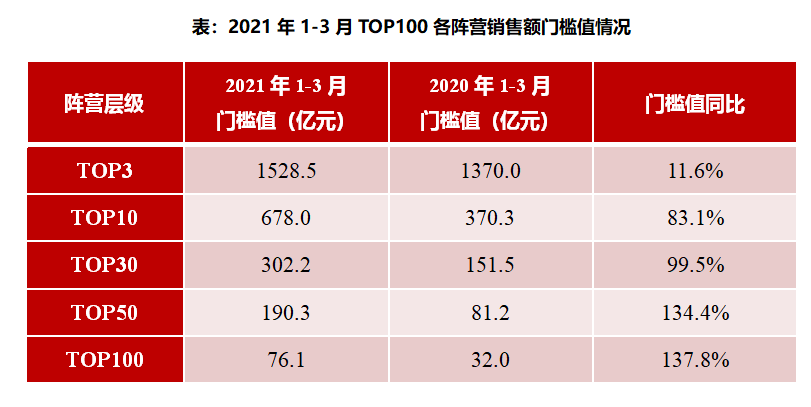

In the first quarter, the sales of the top 100 real estate companies also increased significantly. The “Daily Economic News” reporter statistics found that the total sales of “Bi Wanheng” from January to March were 523.1 billion yuan, and the total sales of TOP10 real estate enterprises exceeded one trillion yuan. In the first quarter, five real estate companies with a value of 100 billion yuan were born, an increase of 2 over the same period in 2020, and there are 76 real estate companies with a value of more than 10 billion yuan.

Under the dual effects of strong demand and increased marketing, the threshold value of each echelon of real estate companies increased for the first time from January to March: the threshold value of TOP3 real estate companies increased by 11.6% to 152.85 billion yuan; the threshold value of TOP10 real estate companies increased by 83.1% to 67.80 billion yuan, but the fastest growth is TOP30, TOP50 and TOP100, which rose by 99.5%, 134.4% and 137.8%, respectively.

Data source: Middle Finger Research Institute

In this regard, Liu Shui, deputy research director of the Corporate Business Department of the Zhongzhi Research Institute, told the reporter of “Daily Business News”: “First of all, these medium-sized real estate companies have sales of tens of billions of dollars for many years, and they have strong scale growth and rapid growth. The development demands require that they grow into a leading real estate company with a value of 100 billion yuan as soon as possible, so as to improve market competitiveness and market position; secondly, these companies are in a relatively small situation.Wonderful, speed up the scale of expansion and speed up one step can become a leading enterprise, and a slower step will cause it to fall behind and enter the ranks of small and medium-sized enterprises. “

It is worth noting that in 2021, real estate companies have begun to exert “strategic cooperation”, and there are many initiatives by leading real estate companies to expand their industrial scope and lay out new markets.

For example, China Communications Group and Vanke Group signed a strategic cooperation agreement in Shenzhen. The two parties will carry out in-depth cooperation in the fields of land development, urban complex, property management, industrial parks, ice and snow vacations, and complement the industrial chain; Shimao Strait and Shanghai Kun Group reached a strategic cooperation in the Guangdong region to jointly invest in the development of the Guangdong-Hong Kong-Macao Greater Bay Area and the Guangxi market; Sunac began to get involved in the hotel industry and established a joint venture with Huazhu to jointly deploy the high-end hotel market.

Liu Shui believes, “For the market, on the one hand, increasing cooperation between different companies, such as the cooperation between companies with capital and companies with land resources, is equivalent to accelerating the flow of market elements and improving the efficiency of resource element allocation; On the other hand, strong alliances between large companies increase their competitiveness, which will accelerate the concentration of resource elements and market shares to large companies, thereby increasing market concentration. For companies, they can complement each other’s advantages, maximize their strengths and avoid weaknesses, and enhance competition. Power and increase market share.”

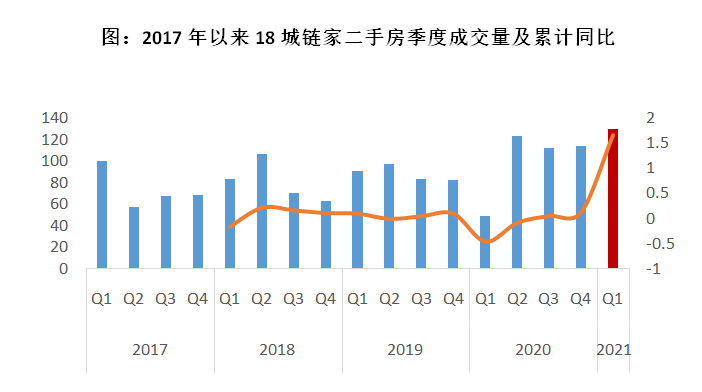

Second-hand housing transactions hit a new quarterly high

Monitoring data from the Shell Research Institute shows that in the first quarter of this year, the transaction volume of second-hand houses in the first quarter of this year in key 18 cities across the country hit a record high in a single quarter since 2017, an increase of 14% from the fourth quarter of last year, which is about 2.6 times that of the same period last year. , An increase of 14% over the fourth quarter of 2020. Due to the low base under the influence of the epidemic in the first quarter of 2020, the volume of second-hand housing transactions in the first quarter increased by 120% year-on-year. In particular, the overall market in first-tier cities is very hot. In January, the second-hand housing transaction volume in Shenzhen and Beijing increased by more than 30% month-on-month, and the month-on-month growth in Shanghai also reached 20%.

Data source: Shell Research Institute

Cao Jingjing, research director of the Index Division of the China Index Research Institute, pointed out to the reporter of “Daily Economic News” that “a variety of factors have jointly promoted the activity of the second-hand housing market in hot cities, such as “Chinese New Year in situ” before the release of demand for home ownership in hot cities. The second-hand housing replacement chain, driven by the shifting, school district housing attention, is clearly active, and the relatively loose credit environment in the early stage is superimposed by the expected tightening of credit. At the same time, the supply of new houses in short-term hot cities is in short supply, squeezing demand back to the secondary housing market. An important reason.”

In the promotion of massive transactionsThe price of second-hand houses nationwide continued to rise from the previous month. The price index of second-hand housing in 35 cities monitored by Shell maintained an increase of 1.4% month-on-month in March, and has risen by 3% since December 2020. The increase in housing prices in first-tier cities has led the country.

The “high fever” market has also triggered further tightening of regulation and stricter financial supervision. Among them, Shenzhen’s “second-hand housing guidance price” policy has achieved significant effects. In the week of the New Deal, Shenzhen’s second-hand housing transaction entered a trough, down 70% from before the New Deal. The transaction volume in the entire first quarter fell by 20% month-on-month and 4% year-on-year; price index month-on-month The growth rate continued to narrow after January and ended in March.

Under the “121 New Deal”, Shanghai’s second-hand housing transaction volume dropped slightly from the previous month. After the Spring Festival, the transaction volume fell by 23% compared with before the Spring Festival; the price index in March narrowed to 3.6% month-on-month, which is two consecutive months. Narrowing; Although Beijing’s transaction volume in the first quarter increased by 20% from the previous quarter, it declined significantly after the Spring Festival, and the trend of market adjustment began to appear.

On the other hand, since the first quarter, financial supervision has been tightened. Cities such as Beijing, Shanghai, Guangzhou, Shenzhen, Haikou, Hangzhou, Xi’an, and Chengdu have strictly reviewed the illegal entry of operating loans into the real estate market. In addition, many places and many banks are also quietly raising mortgage interest rates to directly cool down the enthusiasm for buying houses in first-tier cities. In March, the average first and second home loan interest rates in 60 cities monitored by the Shell Research Institute increased by 6 and 7 basis points respectively from December last year.

The market in first-tier cities is suppressed, while the core second-tier cities continue to be hot. Hefei’s second-hand housing transaction volume in the first quarter increased by about 60% month-on-month, Chengdu and Wuhan increased by about 30% month-on-month, and Xi’an increased by 10% month-on-month. Entering March, the transaction volume of each representative city has reached a record high since 2019, and the price index of second-hand housing has continued to rise and the increase has expanded.

It is worth noting that many cities in the north have undergone an adjustment period of about 3 years, and they have begun to usher in cyclical market repairs. In the first quarter, the second-hand housing transaction in Langfang increased by about 30% from the previous quarter, and the transaction volume in March was second only to the peak in the first quarter of 2017; the second-hand housing transaction volume in Qingdao increased by about 20% in the first quarter, and the price index stopped falling and turned up in March. In addition, the transaction volume of second-hand housing in Jinan and Yantai increased by 27% and 15% respectively from the previous month. The price index of second-hand housing maintained a steady rise, and the market as a whole recovered steadily.

“Entering the second quarter, the above-mentioned factors will continue to weaken the support of the second-hand housing market. Large-scale house land sales will alleviate the anxiety of the new housing market in hot cities, which will lead to a slowdown in the overall second-hand housing market. In addition, short-term school district The pursuit of second-hand housing will gradually cool down.”

Cao Jingjing pointed out that, on the whole, it is expected that the overall transaction enthusiasm for second-hand housing in hot cities in the second quarter will decline, but the overall transaction scale will remain relatively high. In terms of regional structure, with the gradual return of rational home ownership, it is expected that the operation of the property market in hot cities will be more stable, and the market hot spots may sink to the periphery of core cities in developed urban agglomerationsStronger third- and fourth-tier cities, and some second-tier cities in the central and western regions, have undergone more profound cycle adjustments. The current cycle has gradually come out of the bottom, and there is room for short-term markets.

How will real estate companies obtain land under the new land supply regulations?

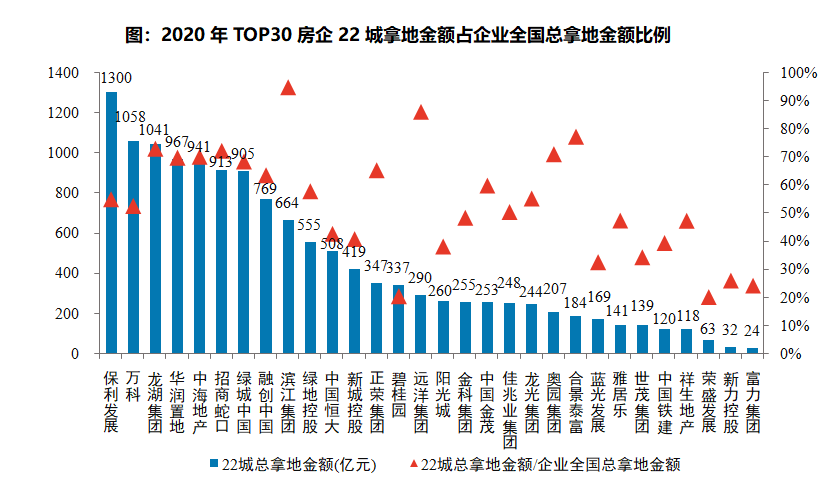

According to the data of the Zhongzhi Research Institute, from January to March, the total amount of land acquired by TOP100 enterprises was 558.8 billion yuan, and the scale of land acquisition increased by 22.7% year-on-year. Poly Development, Sunac China and Greentown China occupy the top three positions on the list. The total value of TOP10 companies from January to March is 587.4 billion yuan, accounting for 32.9% of the TOP100 companies, and the market concentration is significant.

However, in March, the policy has undergone certain changes. Following the new “three red lines” financing regulations in the second half of last year, the land market ushered in an important policy-“Two Concentrations of Housing Land Supply in 22 Key Cities” “New regulations (that is, centrally issuing transfer announcements and centrally organizing transfer activities).

According to the statistics of the Chinese Academy of Sciences, in 2020, the sales area of commercial housing in these 22 cities will account for 24.3% of the country’s total sales, and the sales will account for 39.9% of the country’s sales of commercial housing; residential land transfer fees will account for 37% of the country’s homeland transfer fees. Based on this, it can be seen that the 22 cities, which account for close to success, will present another market pattern under the new policy of “two centralizations” of land supply.

Among the 22 key cities, Hangzhou, Beijing, Suzhou, Guangzhou, Shanghai and other cities are obviously more favored by leading real estate companies. From January to March this year, among the TOP10 cities with land acquired by 50 representative real estate companies, Hangzhou continued to occupy the first place with cumulative advantages. Among the TOP10 cities, the regions are relatively scattered. Except for Hangzhou, Suzhou, Wenzhou, and Nanjing, which are cities in the Yangtze River Delta, the remaining 6 cities involve Chengdu-Chongqing, Midwestern, Beijing-Tianjin-Hebei and other urban clusters.

Data source: Middle Finger Research Institute

Affected by the “two concentrations” policy of land supply, the scale of land acquisition by typical companies in March was affected to varying degrees. Regional deep-farming enterprises such as Binjiang Group and Guangzhou Metro have greatly affected the monthly land acquisition amount; Poly Development and China Overseas Real Estate and other nationally distributed enterprises are less affected. The land acquisition amount in March exceeded 10 billion yuan.

Lu Wenxi, an analyst at Centaline Real Estate, told the reporter of “Daily Economic News”: “Regional deep-cultivation enterprises depend on where they are located. From the perspective of land acquisition, real estate companies still favor first- and second-tier cities. Centralized supply is short-term concentration. The release of multiple plots of land for sale will cause funds to flow to high-quality areas. If the real estate enterprises in these regional cities are deeply cultivated, they may be squeezed by multiple sources of funds., The competition will be fierce. On the contrary, if it is a third- and fourth-tier cities where the intensity is not high, the pressure will not be too great. “

“Specifically, some large-scale real estate companies, taking Binjiang as an example, are also deeply plowing and experienced companies in the region. The market response is not weak. Everyone needs to adapt to the new land supply rules. This is fair to all companies. . Companies have enough land reserves, even if there is a short-term impact, it is quite limited.” Lu Wenxi said.

Reviewing the land acquisition situation of various enterprises in 2020, Poly Development has acquired up to 130 billion yuan in land acquisition in 22 cities, and Vanke, Longhu, China Resources, China Shipping, China Merchants Shekou, Greentown and other enterprises have exceeded 90 billion yuan; from the specific enterprise In terms of the proportion of land acquisition in 22 cities, Binjiang Group reached 94.7%, and Sino-Ocean, KWG, Longfor, China Merchants Shekou, Aoyuan, China Shipping and other companies accounted for more than 70%. These companies have a more concentrated strategic layout in 22 cities. , Will become an important participant in 22 cities in the future.

“As more large companies join forces, market concentration will accelerate and there will be fewer opportunities for small companies.” Liu Shui analyzed.

Lu Wenxi believes, “Small and medium-sized real estate companies still have certain opportunities to obtain land. Centralized supply of land, no matter how large a real estate company can’t take care of all the land parcels, there are always areas that cannot be taken care of. Opportunities for land. Giving small and medium-sized real estate companies a certain opportunity to develop products also enriches market products, prevents large real estate companies from monopolizing the market, and is also beneficial to the stable and healthy operation of the real estate market.”