Immediately, focus on China’s cloud gaming market.

Editor’s note: This article from the micro-channel public number “Tencent Research Institute” (ID: cyberlawrc), of: TRI x Newzoo.

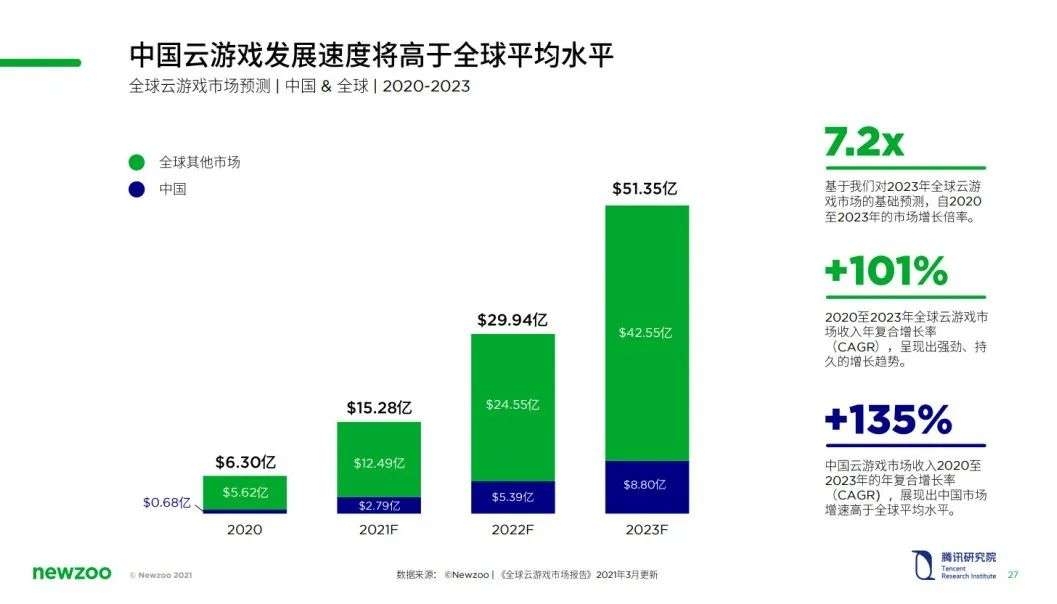

Today, Tencent Research Institute and Newzoo jointly released the “China Cloud Game Market Trend Report (2021)”, which aims to focus on the latest developments in China’s cloud game market and to analyze and compare the strategies of major cloud game service providers at home and abroad. Correct. The report also puts forward some key factors that may shape the future cloud gaming market-infrastructure, business models, technologies and standards, as well as the ongoing 5G construction, immersive content, living room entertainment, new peripherals and other opportunities. Hope to share with the industry Discuss the future trend of China’s cloud gaming development. The report predicts that between 2020 and 2023, the compound annual growth rate (CAGR) of China’s cloud gaming market revenue will reach 135%, far exceeding the global average of 101%.

In 2020, various business activities related to cloud gaming will increase significantly. World-renowned game and technology companies such as Microsoft, Google, Amazon, Nvidia, Valve, Tencent, etc. are actively polishing their products, adjusting their strategic positioning and business layout in this emerging field. In addition, short video live broadcast platforms, social media, and distribution channels in the game industry chain are also experimenting with diversified methods such as playable advertising, cloud trial play, live broadcast + cloud gaming, etc., to strive for cloud gaming Gain a place in the market. Small and medium-sized companies in some segments often choose more localization methods to fill in the gaps that other services cannot cover.

Although it is still in its infancy in terms of market size and user base, cloud gaming still shows huge potential that is incalculable. Players only need to ensure a good network status, they can enjoy the joy of the game anytime, anywhere without hardware restrictions. You can even use your smartphone to experience the high-quality game content originally exclusively owned by the host and PC for the first time.

The flexibility and ease of use of cloud gaming will become one of the key elements for launching the next-generation gaming experience. The world of virtual and real symbiosis will become bigger, more detailed, more immersive, and easier to interact. For example, “Microsoft Flight Simulator” (Microsoft Flight Simulator) supports real-time transmission of massive amounts of data, which allows it to reproduce the earth with incredibly precise details, including real-time weather conditions. The number of online players in the same virtual space can be expanded and far exceeds the current limit of about 100. In the live broadcast, the control of the game content can be easily switched between the anchor and the audience, creating a novel interactive experience.

In order to achieve this vision, cloud games need to keep up with the pace of network infrastructure construction, promote technological innovation and standard formulation, so that the user experience of cloud games is basically the same as that of local games, or even better; on this basis, control additional investment In order to achieve a virtuous cycle of ecology, we will explore a win-win business model for multiple parties. In the long run, the “super digital scene” built on the cloud native engine will be the “killer” of cloud gaming technology.

Key data and findings

1 /CAGR of China’s cloud game market: 135%

Newzoo predicts that between 2020 and 2023, the compound annual growth rate (CAGR) of China’s cloud gaming market revenue will reach 135%, and the market growth rate will be significantly higher than the global average growth rate of 101%, making it the cloud with the most potential One of the leading game markets. According to the “Global Cloud Game Market Report” updated by Newzoo in March 2021, from 2020 to 2023, the global market for cloud games will grow approximately 7.2 times to reach US$5.135 billion.

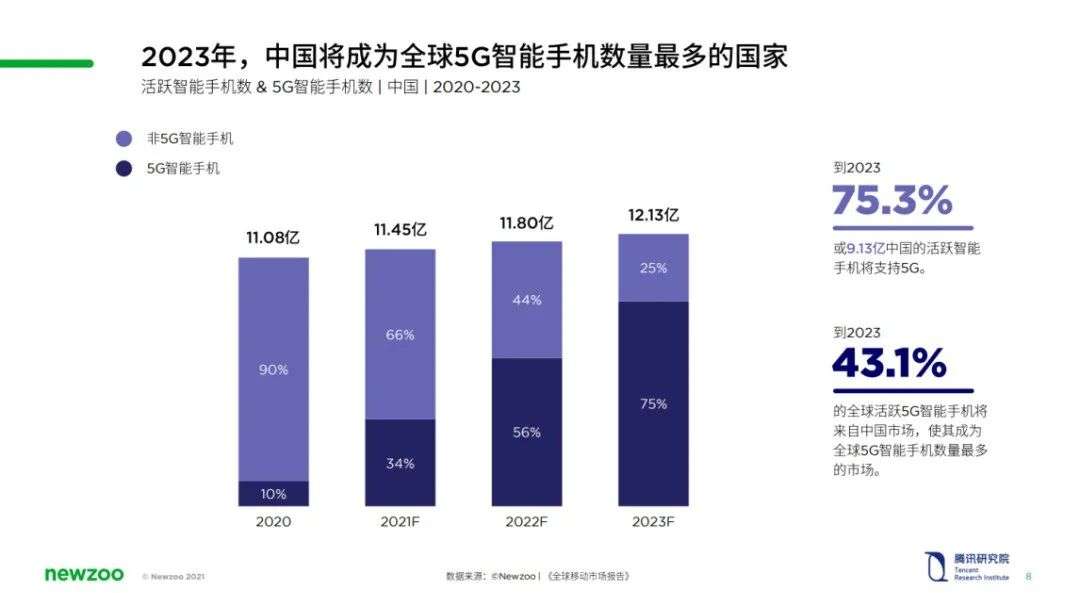

2 The number of 5G smartphones in China in 2023: 913 million

By 2023, it is estimated that there will be 913 million active smartphones supporting 5G in China, accounting for 75.3% of the total. In the fixed network/optical broadband, indoor local area network, and outdoor mobile network environments, mobile networks face greater challenges. The construction of 5G networks and the popularization of terminals are one of the ways to solve the challenge. The 5G network has lower air interface link latency, higher bandwidth, more devices connected at the same time, and promotes the sinking of edge computing nodes-these are all conducive to improving the cloud gaming experience under mobile network connections.

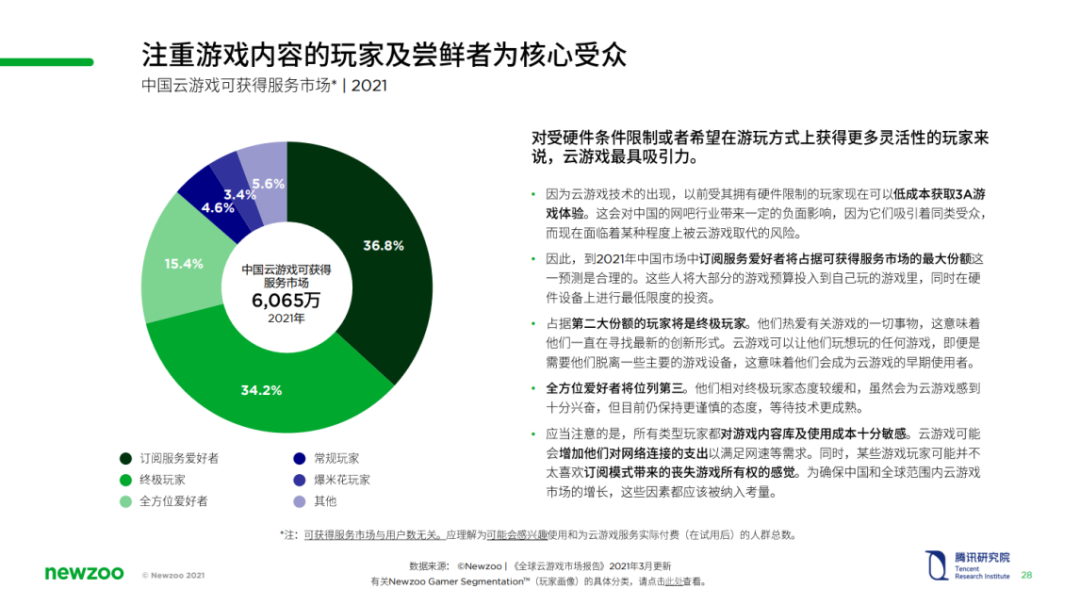

3 The number of potential users of cloud games in China in 2021: 60.65 million people

In 2021, China’s cloud gaming service market will reach 60.65 million people. This refers to the total number of people who may be interested in using and actually paying for cloud gaming services after the trial.

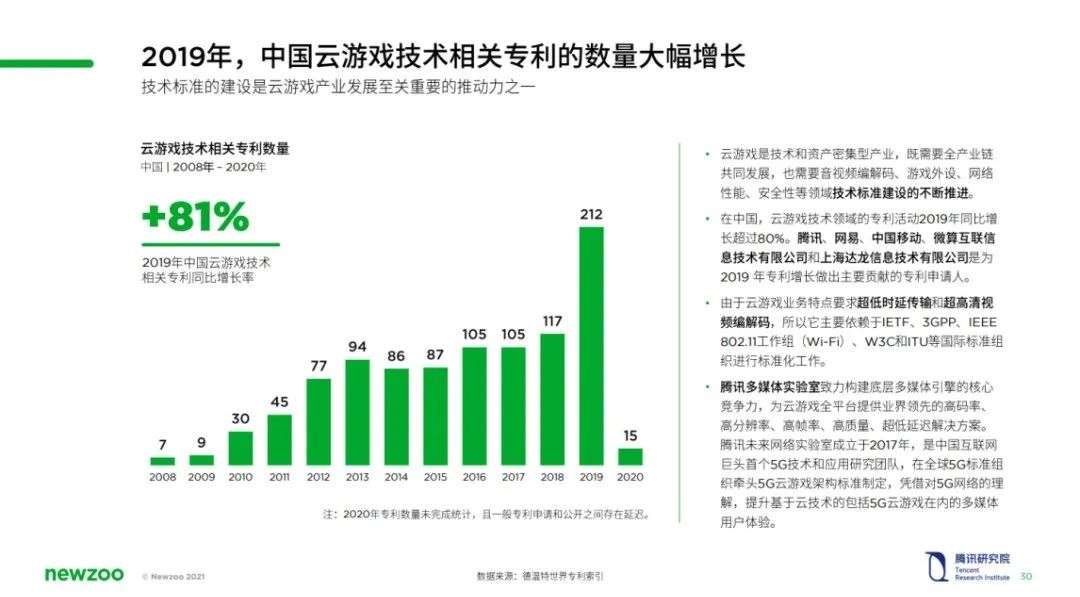

4 /2019 China’s cloud game technology-related patent growth rate: 81%

In China, patent activity in the field of cloud gaming technology increased by more than 80% year-on-year in 2019. Tencent, NetEase, China Mobile, Microcomputing Internet Information Technology Co., Ltd. and Shanghai Dalong Information Technology Co., Ltd. are the patent applicants who have made major contributions to this growth.

Other core views

1 / China and overseas: mobile first vs diversified development

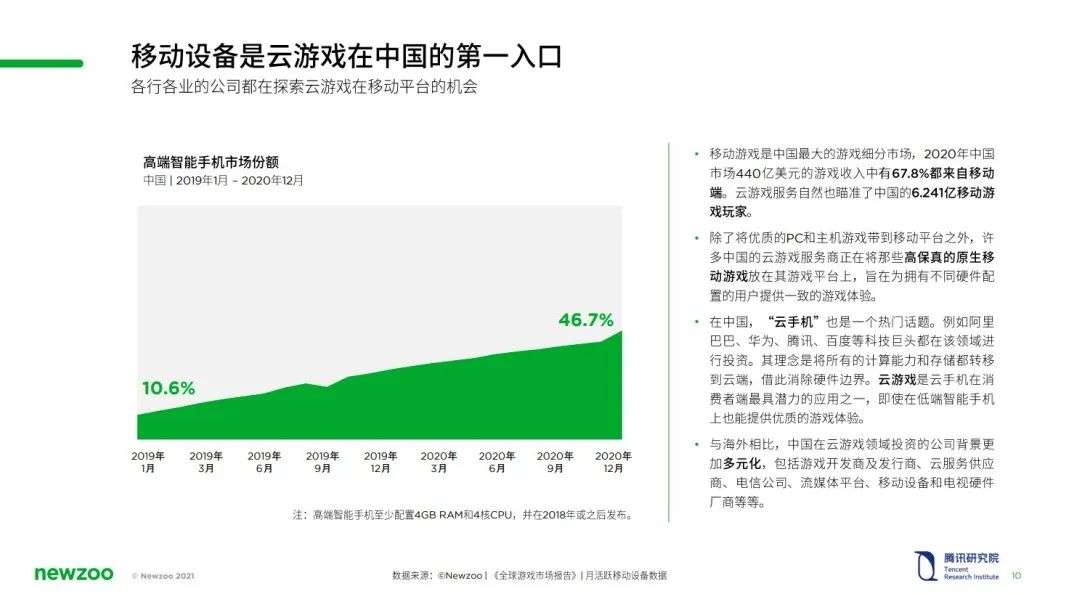

Mobile games are China’s largest game segment. In 2020, 67.8% of the US$44 billion in game revenue in the Chinese market will come from mobile. Cloud gaming services naturally target 624.1 million mobile game players in China.

The success of a large number of high-quality game content in China shows that Chinese players have increased their consumption demand for large-scale and highly immersive game content. Under the limitation of the computing and storage capabilities of mobile devices, cloud games provide solutions for the experience of accessing such games on mobile platforms.

Most of the major technology companies in overseas markets have entered the cloud gaming field, and there are many smaller but ambitious companies that provide B2B and B2C services. They tend to focus on PC and console games, and support or plan to implement them on mobile devices, web browsers and TVs as soon as possible.

In order to obtain high-quality content, some cloud gaming platforms have established multiple partnerships with publishers, and even provide embedded subscription services. For example, Xbox Game Pass Ultimate includes EA Play content; players can also subscribe to Stadia or Luna to play Ubisoft+ games.

2 / Enthusiasts and early adopters are important early user groups

In China, the ice-breaking of cloud games largely comes from the demand for “leapfrog” experience masterpieces of players with low-end devices, to make up for the actual hardware shortcomings of the lack of coverage of consoles, high-end PCs or mobile devices.

Cloud games are still in the early stage of innovation and diffusion on the market side, and hardware rigid players are important seed users. According to the i-MUR survey results of Tencent’s Market and User Research Department, early users who have actually experienced cloud games include two types of typical users: geek early adopters and hardware rigid demand users. Cloud gaming can ease equipment constraints, partially replace Internet cafes, and experience 3A games at low cost. They are sensitive to content lineups and usage costs. Comprehensive factors such as excessive tariffs, lack of ownership in the rental model, and derivative costs such as traffic are all obstacles to the continued use of cloud games.

3 /The living room cloud game entertainment scene has potential

During the new crown epidemic and during the recovery period, the education, meeting, entertainment, and social functions of the living room TV are activated, and the interactive entertainment in the living room may be cloudGame development provides opportunities. According to data from the China Internet Network Information Center (CNNIC), by March 2020, 287 million Internet users in China will access the Internet through TV. Since home Internet connections are generally more stable, cloud gaming on TVs will be less limited by data speed and latency.

Some large companies such as Tencent, China Mobile, and Shun.com have formulated relevant TV cloud gaming strategies. Strengthen cooperation and ecological construction with IPTV and OTT, and expand supporting peripherals such as boxes and handles, and actively develop social and interesting game content suitable for home entertainment scenarios.

4 /Technology and standard construction promote the sound development of industrial ecology

In order to fully realize the potential of cloud gaming, all core technologies need to go hand in hand. On the whole, the current cloud gaming industry focuses on optimizing virtualization solutions, increasing the number of single graphics card containers, while reducing data transmission and server costs, and applying flexible expansion to reduce computing costs. In addition, the ability to dynamically adjust video streams based on terminal equipment and network conditions is equally important.

Cloud gaming is a technology and asset-intensive industry. It not only requires the joint development of the entire industry chain, but also the continuous advancement of the construction of technical standards in the fields of audio and video codec, game peripherals, network performance, and security.

5 /Content is still the core competitiveness of cloud game services

Content will become the main driving force for users to choose and retain game services. For leading game publishers, the best strategy is to develop their own cloud game services. Head game developers have the ability to explore native cloud game engines, develop native cloud game products, and achieve full-realistic scenes and multi-user interactions far beyond the support of local computing power.

For small and medium-sized or independent developers, you can reduce development costs by signing an exclusive cooperation agreement with a third-party cloud game platform. In addition, a smaller and more focused content library in the subscription service will make the game easier to discover by players. In order to make the game service stand out from the platform-agnostic future trend, own IPAnd getting exclusive cooperation will be more important than ever.

Cloud gaming may also become one of the important contributors to the future “metaverse” (metaverse).

On the whole, as the technology and network infrastructure are not yet perfect, the operating cost is high, and the experience is not good, cloud gaming has not yet completed the establishment of a sustainable business model in China, nor has it created an increase in game revenue and experience. Therefore, it is still in the product distribution link for the time being, and it is mainly based on the subscription system and the provision of monthly fees and monthly services. It has not really changed and shaken the existing game development, distribution, and consumption ecology. The native cloud game engine and content are still on the way, and infringement of some game content still occurs. From the perspective of purely “push streaming” and “move to the cloud”, the technical threshold of cloud gaming is not high, but before fulfilling the promise of cloud gaming to the industry and players, we still need to invest in new technologies, new scenarios, and new content. Waiting for change.