At the critical moment of the handover of fuel vehicles and electric vehicles, the test is the core competence of auto companies.

Editor’s note: This article is from the micro-channel public number “into the passenger Tanker” (ID: SQinsight), Author: Xu Yun, editor: Feng Yu.

SAIC’s “bitter days” are not over yet.

In 2020, SAIC Motor achieved revenue of 723.043 billion yuan, a year-on-year decrease of 12.52%; net profit attributable to shareholders of listed companies was 20.431 billion yuan, a year-on-year decrease of 20.2%. This is the second year that SAIC Group has experienced negative performance growth, and its revenue has hit a record low in nearly five years, and the net profit attributable to shareholders of listed companies has hit a record low in nearly nine years.

In the capital market, SAIC’s performance is also weak. As a Chinese car company with the largest market value, SAIC Motor has become a net-breaking stock in 2020. Its market value has been surpassed by its performance and sales volume, which is far less than its own “brothers”, first by BYD, then by Weilai and other manufacturers. New car forces, and even Great Wall Motors, which is also a traditional car company, have achieved the latecomers.

Why did the SAIC Motor fall here? After successively developing new energy fields, is SAIC still worth investing in?

1, The hard days of selling crowns

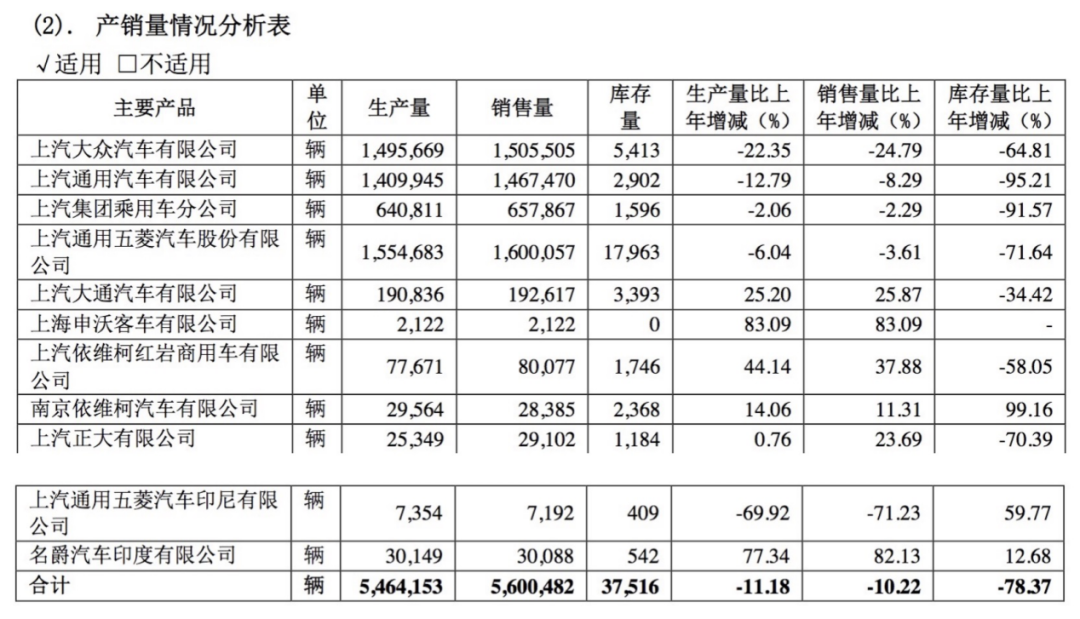

The 2020 financial report released by SAIC on the evening of March 25 showed that its annual cumulative sales reached 5.605 million, which is the sales champion of domestic auto companies. This is also the 15th consecutive year that SAIC has been in this position.

But there are also hidden worries behind the sales crown.

According to data from China Association of Automobile Manufacturers, in 2020, my country’s automobile production and sales will reach 25.225 million and 25.311 million, respectively, down 2% and 1.9% year-on-year. In the same period, the production and sales volume of SAIC Motor were 5,464,200 vehicles and 5,605,500 vehicles, a year-on-year decrease of 11.18% and 10.22% respectively. Obviously, SAIC underperformed the market.

Picture / 2020 Annual Report of SAIC Motor

The downturn of SAIC Motor in 2020 even alarmed Shanghai’s senior officials. In May 2020, the Shanghai Securities News reported that in response to SAIC’s (sales) “sudden brake” situation, ShanghaiThe main leaders in charge attach great importance to it and give special instructions to require SAIC to conduct research on existing problems in various aspects such as brand, quality and sales. Relevant departments in Shanghai will increase support for the nine major brands and a variety of new cars under SAIC, and support this important auto company in Shanghai.

“If it weren’t for the rescue of the Shanghai government, SAIC would be even more miserable.” Zeng Piquan, deputy secretary-general of the New Energy Automobile Branch of the China Automobile Dealers Association, bluntly said to “Tanker Tanker”.

In the eyes of the outside world, SAIC Group’s long-term performance and sales depend on joint ventures such as SAIC Volkswagen, SAIC-GM and SAIC-GM-Wuling, but the joint venture’s poor performance in 2020 is an important reason for the decline in SAIC’s performance and sales.

In 2020, SAIC Volkswagen achieved sales of 1.555 million vehicles, a year-on-year decrease of 24.79%; the net profit attributable to the parent company was 15.489 billion yuan, a year-on-year decrease of 22.65%. What’s embarrassing is that FAW-Volkswagen, also a joint venture company of Volkswagen in China, achieved sales of 2,161,800 vehicles in 2020, a year-on-year increase of 1.5%, in sharp contrast with SAIC Volkswagen.

In addition to the impact of external factors such as the epidemic, SAIC Volkswagen’s Passat’s evaluation of the Zhongbao Research Institute has triggered a crisis of consumer trust in the quality of its products. It is also regarded by the outside world as an important factor affecting SAIC Volkswagen’s sales in 2020. According to data from the Travel Association, the cumulative sales of SAIC Volkswagen Passat in 2020 were 128,882 (excluding PHEV models), a year-on-year decrease of 31.9%.

As for the sales gap between SAIC-Volkswagen and FAW-Volkswagen, Zeng Piquan analyzed “Tanker Tanker”. From the perspective of consumers, FAW-Volkswagen’s overall models are very good-looking and can better cater to consumers’ needs.

“At present, China’s auto market is no longer dependent on government support and assistance as it used to be. It is now completely dependent on the market and adapts to market behavior. It has changed from policy-oriented to market-oriented. FAW-Volkswagen’s overall models are good, especially New energy vehicles are generally high-end and can meet consumer preferences.” Zeng Piquan further pointed out that whether product design and quality are suitable for consumer preferences is the only dominant factor in the market.

SAIC General Motors, another major sales force of SAIC Group, did not perform well in 2020. Its annual sales volume was 1,467,500 vehicles, down 8.29% year-on-year; net profit attributable to the parent company was 4.103 billion yuan, down 62.56% year-on-year .

SAIC-GM-Wuling’s sales decline was relatively small, down 3.61% year-on-year, and sales reached 1.6 million vehicles, but the net profit attributable to the parent company was only 142 million yuan, a sharp decline of 91.62% year-on-year.

In terms of capacity utilization, SAIC-Volkswagen, SAIC-GM and SAIC-GM-Wuling are the top three subsidiaries of SAIC Group in terms of production capacity, but they all experienced declines in 2020. Among them, SAIC Volkswagen’s capacity utilization rate dropped from 104% in 2019 toFrom 72% in 2020, SAIC-GM has dropped from 85% to 74%, and SAIC-GM-Wuling has dropped from 94% to 88%.

Mapping / Tanker

Data from the National Bureau of Statistics show that the capacity utilization rate of the automobile manufacturing industry in 2020 is 73.5%. Among the 11 SAIC subsidiaries, the capacity utilization rates of SAIC Volkswagen, SAIC Maxus, Nanjing Iveco, SAIC Zhengda, SAIC-GM-Wuling Motor Indonesia Co., Ltd. and MG Motor India Co., Ltd. are all below the industry level. This is obviously not a good sign.

It is worth mentioning that the performance of SAIC’s autonomous sector in 2020 is relatively not so bleak. SAIC passenger vehicles, which is responsible for the research and development, manufacturing and sales of SAIC Group’s own brand vehicles, will have a slight drop of 2.29% year-on-year in 2020 sales. However, compared with joint venture brands, the sales volume of 658,900 vehicles has not yet formed strong support.

In Zeng Piquan’s view, the decline in sales and performance of SAIC Motor is not due to its dependence on the development of joint ventures, but the poor development of its own brands. “Whether the design of independent brands can adapt to changes in the market is the most important thing. Ultimately, it must adapt to the market, and at the same time, it also depends on consumers’ acceptance of the products. SAIC’s products have always been mediocre. It is related to the nature of state-owned enterprises, development is influenced by the system, and innovation is insufficient.”

“For example, many SAIC models, including Roewe, are targeted for sale, which restricts the development of its entire car brand, especially its own brands, which are more obvious and not sufficiently innovative.” Zeng Piquan gave an example.

2, Be overtaken by “little brother”

The performance and sales are not good, and SAIC’s performance in the capital market is also unsatisfactory.

Looking back on 2020, it is undoubtedly the age of “suppression” for traditional car companies. Tesla, Weilai, Xiaopeng, Ideal and other new Chinese car-making forces, despite the company’s difficult profitability and the “niche” sales of new energy vehicles, large traditional vehicles that will still occupy the mainstream position of the auto market in terms of market value Qi left behind.

In China’s auto industry, the most aggrieved one is probably SAIC.

BYD, which holds the new energy vehicle and power battery business, has become the most shining new energy vehicle leader in A-shares in 2020 when the car sales and performance scale are far less than SAIC., On July 7, 2020, it achieved the first time to catch up with SAIC in market value, replacing SAIC’s status as the “big brother in market value of Chinese auto companies”.

“It is inevitable that new car manufacturers have a higher valuation than traditional car companies. On the one hand, the losses of new energy car companies are shrinking, and the sunset industry is going down, while traditional car companies are still too big and there is no way to completely transform.” Regarding the valuation difference between new energy car companies and traditional car companies, Xinding Capital’s chairman Zhang Chi once said to “Tanker”.

During the transition period of the automobile industry moving towards the new energy era, major traditional car companies have also accelerated the pace of transformation and made greater noise in the field of new energy vehicles. The Wuling Hongguang MINIEV, which is positioned as the “people’s scooter” under SAIC-GM-Wuling, is priced at only 28,800 to 38,800 yuan, which is very close to the people. After being listed, it quickly became a hot product and has long occupied the top spot in the sales of electric vehicles.

In 2020, SAIC achieved sales of 320,000 new energy vehicles, an increase of 73.4% year-on-year. The group’s sales of new energy vehicles ranked first in China and third in the world.

However, the name of the new energy sales title is just “looks beautiful”. From the current point of view, this will only give a limited boost to SAIC’s share price. As of April 2nd, BYD had a market value of 503.2 billion yuan, more than twice the market value of SAIC Group’s 232.5 billion yuan; the market value of Weilai, a new car-building power that was only established for 6 years, closed at 62.246 billion U.S. dollars (about 408.514 billion yuan). , Is also far ahead of SAIC.

“SAIC’s sales volume is No. 1 in the country, but the best-selling one is Wuling. Its price cannot be compared with BYD and Weilai. The sales of BYD Han and Weilai ES6, ES8 and other models are all good, and the average price is basically a few. One hundred thousand, but how much does Wuling sell for? So SAIC does have sales, but its market value is not as high as BYD and Weilai.” Zeng Piquan bluntly told “Tanker”.

In 2020, SAIC-GM-Wuling will achieve a production volume of 1.5547 million vehicles and a sales volume of 1.601 million vehicles, ranking first among the subsidiaries of the SAIC Group. However, SAIC-GM-Wuling’s 2020 net profit attributable to the parent company has fallen sharply by 91.62% year-on-year to only 142 million yuan, which is the bottom of the major holding companies of SAIC Motor. Obviously, SAIC chose to use profits in exchange for market share.

Picture / 2020 Annual Report of SAIC Motor

If the skyrocketing market value of BYD and NIO is mainly due to the light of the new energy concept, then Great Wall Motor’s surpassing should be more important.The vigilance of traditional car companies such as auto.

In 2020, Great Wall Motors announced its high-profile transformation to a global technology travel company. It launched the three major technology brands of “lemon”, “tank” and “coffee intelligence” in one go. The technological ecology of “new energy” integration.

“Great Wall is an innovative company, with many new cars coming out.” Zeng Piquan pointed out.

According to the financial report of Great Wall Motors, its 2020 performance and car sales volume are not as good as SAIC, but they are all growing. Among them, revenue increased by 8.62% year-on-year to 103.308 billion yuan; net profit attributable to shareholders of listed companies increased by 19.25% year-on-year to 5.362 billion yuan; cumulative sales of automobiles for the year were 1.1159 million vehicles, a year-on-year increase of 5.41%.

The capital market is quite buying it. As of April 2, Great Wall Motor’s market value reached 315.5 billion yuan, which has also surpassed SAIC. The importance of change is self-evident.

3, Is there a “money way”?

It can be seen that in 2020, SAIC has had a very difficult time. So, is SAIC still worth looking forward to in the future?

In this regard, SAIC itself appears quite confident. SAIC Group has set a business target of achieving 6.17 million vehicle sales in 2021, an increase of 10.2% year-on-year, with an estimated total operating income of 830 billion yuan and operating costs of 720 billion yuan.

Wei Yong, vice president and chief financial officer of SAIC, said at the performance briefing that such predictions are mainly based on two judgments. One is the general trend of domestic automobiles this year, and the other is SAIC’s performance in new energy vehicles and overseas markets Good trend.

Although SAIC will be left behind by new energy concept stocks in market value in 2020, from the perspective of SAIC’s many layouts in the new energy field in recent years, especially in 2021, SAIC’s transformation battle is worth looking forward to.

In terms of new energy, SAIC has not only invested heavily in companies related to the industry chain such as Weimar Motors and Momenta Autonomous Driving, but also launched R cars, and cooperated with Ali and Zhangjiang Hi-Tech to build a new energy brand Zhiji Automobile.

According to Wei Yong, Zhiji Auto will take the high-end route and create a deep intelligent experience. Three models will be released successively this year; and the R standard is defined as the “new force national team”, mainly to meet differentiated needs The smart cockpit scene supports users to purchase smart driving services on demand. Two models are planned to be launched in April and October next year; Roewe and MG are mainly cost-effective.

On the joint venture brand, SAIC Volkswagen’s ID.4 X, the first electric car in the ID family built on the MEB platform, has been officially launched recently.Ten thousand yuan-272,900 yuan. It is reported that before the listing of ID.4 X, SAIC Volkswagen has completed the landing of more than 250 ID.4 X dealers.

SAIC Volkswagen Co., Ltd. Volkswagen brand marketing executive director Yang Siyao said that SAIC Volkswagen has set a sales target of approximately 300,000 new energy vehicles this year, which will release the first-stage production capacity of its MEB plant. SAIC Volkswagen hopes that it will achieve a 9% market share in China’s new energy market, and this goal will be completed by the three new ID. series electric vehicles that will be launched this year-ID.4, ID.6, and ID.3. Among them, ID.4 X will contribute 50,000 to 60,000 vehicles.

“This year is a big year for our products. In addition to the ID. series will launch three products, the most important products of Tuon, Tiguan, and Passat will launch new models. At the end of this year and the beginning of next year, Lingdu will also achieve Replacement.” Yang Siyao revealed.

Obviously, SAIC, which has been stagnant in fuel vehicles and the capital market, wants to regain a city with new energy.

“SAIC’s investment and deployment in new energy is very strong, and it takes a long-term view. It continues to promote innovation, which is considered to be at the forefront and recognized in the industry.” Zeng Piquan told Tanker, many new energy car companies They are all willing to tap SAIC talents, especially technical talents.

However, Zeng Piquan pointed out that R car is currently relatively flat on the marketing side, “because its marketing is only in the WeChat Moments and Douyin, and it disappears. There is not much marketing and hot spots. , This will result in a good car, but the entire sales volume will not rise.”

In addition to new energy, the SAIC Audi project also has new developments. On April 1, SAIC Volkswagen announced that Jia Mingdi, the former general manager of SAIC Volkswagen Sales Company, was transferred to the Executive Deputy General Manager of the Audi Marketing Division of SAIC Volkswagen. According to media reports, SAIC Audi’s first domestically produced model A7L will officially debut at the Shanghai Auto Show in April this year.

After many layouts, it can be seen that despite the overall decline in the market after the Spring Festival, SAIC’s share price is also in a downward state, as of April 2, it closed at 19.9 yuan, which is a relatively high level in recent years. Low position, but some brokerage research reports are still optimistic about it.

Photo / Oriental Fortune Net

Bank of China Securities gave a buy rating on the day after the SAIC Group’s financial report was released (March 26). The reasons include: comprehensive deployment of smart electric vehicles to build a long-term competitive advantage; domestic Volkswagen ushered in a new product cycle,Foreign markets help long-term development.

Although Soochow Securities lowered the SAIC Group’s 2021-2022 profit forecast, it adjusted SAIC’s “overweight” rating. In its research report, it pointed out that it is expected to open a new brand with the company’s Zhiji + new R standard high-end smart electric brand. In the energy market, and continue to expand overseas markets, SAIC Volkswagen and GM are expected to bottom out and stabilize.

From the perspective of changes in the number of shareholders, investors in the secondary market have paid more attention to SAIC Motor. As of December 31, 2020, the number of shareholders of SAIC Motor reached 209,078, and as of February 28, 2021, the number of shareholders reached 260,466, an increase of 51,388 during the period.

In the exchanges with “Tanker Tanker”, many investors in the secondary market believed that SAIC’s state-owned enterprise system reform was relatively slow and the traditional car companies’ own thinking was easy to solidify, but they still believed that they could be expected in the long run and could wait for opportunities to buy the bottom.

“It’s good to buy now.” Zhou Cheng (a pseudonym), a secondary market investor, believes that SAIC Motor’s performance in the Q4 quarter of 2019 has declined significantly. In 2020, it will be affected by the epidemic and new energy, and even broke the net for a time. From the data point of view, it is now at an oversold level.

Huang Xingsen (pseudonym), another secondary market investor, reminded to be alert to short-term volatility risks, “I bought it early when I bought about 25 yuan per share. However, in the long run, I am still more optimistic about SAIC’s future transformation.”

Huang Xingsen revealed that he has recently increased positions in SAIC several times, with an investment of about 50,000 yuan.

4. Conclusion

There is no doubt that in the current auto market, the electrification, connectivity, intelligence and sharing of the “new four modernizations” of automobiles are setting off a technological revolution.

Young new carmakers can use new energy to achieve overtaking in the auto industry, but traditional car companies can’t change it. In the current auto market, it can be seen that traditional auto companies, including SAIC, have taken the pace of change, whether they are willing or forced by the market.

However, change does not necessarily mean success. At the critical moment of the handover of fuel vehicles and electric vehicles, the test will be the core competence of auto companies.

Special note: This article does not constitute investment advice. Investment is risky, so you need to be cautious when entering the market.